|

市場調查報告書

商品編碼

1940707

表面黏著技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Surface Mount Technology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

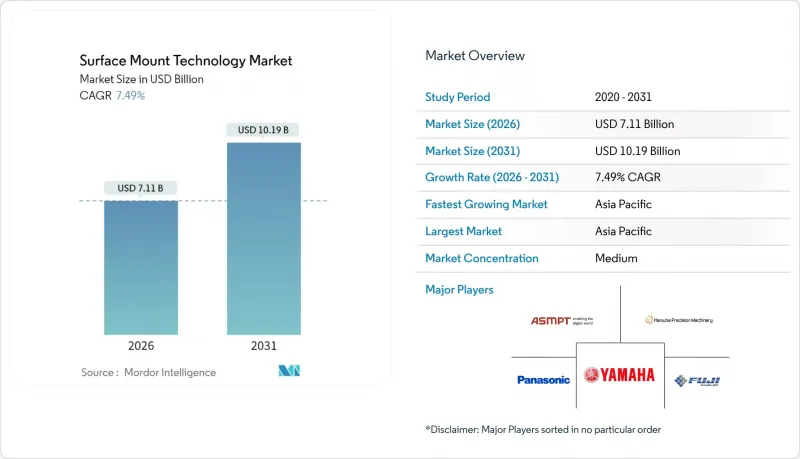

2025年表面黏著技術(SMT)市值為66.1億美元,預計2031年將達到101.9億美元,高於2026年的71.1億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 7.49%。

這一成長趨勢主要受消費性電子、電動車和工業自動化領域對更小、更緊湊電子元件的需求所驅動。 5G基礎設施的加速部署、人工智慧伺服器的成長以及邊緣運算和物聯網產品的普及,使得亞洲、北美和歐洲的生產線幾乎滿載運作。汽車製造商現在需要能夠承受-40°C至150°C溫度波動的車規級SMT解決方案,這進一步提高了設備的要求。同時,微型LED和系統級封裝(SiP)技術的創新,將貼裝精度要求從±25μm提升至10μm以下。儘管終端市場基本面良好,但供應鏈的不穩定性,尤其是在半導體和高精度陶瓷領域,仍是近期產量成長的主要阻礙因素因素。

全球表面黏著技術(SMT)市場趨勢與洞察

物聯網和穿戴式裝置推動超高密度印刷電路板的應用

如今,設備製造商在一隻智慧型手錶中整合了超過10,000個積層陶瓷電容,是五年前的三倍。為了印刷小於50µm的導電走線和小於75µm的微孔,組裝製程依賴於能夠以±25µm精度穩定處理01005封裝的貼片工具。符合FCC輻射限制和IEC安全要求進一步加強了電磁干擾(EMI)屏蔽措施,從而推動了對精密焊膏檢測和自動光學檢測(AOI)系統的需求。

汽車ADAS電子設備的普及重塑了可靠性要求

電動車參考設計每輛車包含超過10,000個多層陶瓷電容器(MLCC)和200個電控系統(ECU),其生命週期認證期限為三年或更長,同時表面貼裝技術(SMT)的產量也不斷成長。強制性的ISO 26262功能安全標準以及-40 度C至150 度C的動作溫度範圍要求供應商通過汽車PPAP和AEC-Q200壓力測試認證。能夠檢驗焊點長期可靠性的設備製造商已在歐洲和日本獲得多年供貨合約。

高額的初始資本投入是中小企業發展的障礙。

新一代安裝平台整合了在線連續SPI、AOI和X光檢測設備,每條生產線的成本可能高達300萬美元以上。預測性維護分析可以降低整體擁有成本,但許多中小型EMS供應商難以證明其投資回收期少於三年的合理性。設備租賃和基於績效的服務協議正在興起,但在Tier 1 OEM廠商之外仍然不常見。

細分市場分析

到2025年,主動元件將佔據表面黏著技術(SMT)市場佔有率的65.74%,這主要得益於人工智慧伺服器和電動汽車對微控制器(MCU)、專用積體電路(ASIC)和電源管理組件的需求加速成長。在異構片上系統(SoC)設計和高壓電晶體日益普及的推動下,預計到2031年,該細分市場將以8.62%的複合年成長率成長。被動元件將繼續受益於5G終端和汽車牽引逆變器中元件數量的增加,但陶瓷和鉭材料的短缺仍然考驗著供應鏈的韌性。

客戶期望正從元件成本控制轉向基板級整合密度和長期可靠性。原始設備製造商 (OEM) 要求故障率低於 10 ppm,現場使用壽命長達 15 年,這促使基板供應商、元件製造商和組裝設備供應商之間進行更緊密的合作。提供協作式主動和被動元件設計庫以及完整的面向組裝設計 (DFA) 評審的供應商,正在加速新產品量產,並確立自身作為先進穿戴式設備和工業IoT閘道器首選供應商的地位。

即使到了2025年,貼片設備仍將佔據表面黏著技術(SMT)市場42.62%的佔有率,其中檢測設備成長最快,複合年成長率(CAGR)高達8.83%。高速貼片設備採用機器學習視覺系統自動調整貼片頭壓力,加工速度可達每小時10萬個零件,精確度為±10μm。焊接設備由於無鉛合金對溫度梯度要求嚴格,製程窗口較窄;而絲網印刷平台則採用封閉回路型SPI回饋來提高一次產量比率。

投資趨勢青睞利用深度學習技術將誤報率降低90%、偵測速度提升四倍的AOI和X光系統。 ViTrox和Koh Young皆採用IPC-CFX連接技術,可實現即時分析,在幾分鐘內偵測出降低產量比率的趨勢。設備融資方案與分析訂閱服務捆綁銷售,可降低前期高昂成本,並鼓勵東歐和東南亞的二級電子製造服務(EMS)企業升級其生產線。

區域分析

亞太地區將主導表面黏著技術(SMT)市場,預計到2025年將佔據48.05%的市場佔有率,並預計在2031年之前以8.12%的複合年成長率成長。 2027年,中國大陸、台灣和韓國預計將在新建300毫米晶圓廠方面總合投資超過840億美元,以確保上游工程基板和元件產能。日本熊本產業叢集以台積電JASM 200億美元的擴建計畫為核心,每月將新增超過10萬片12吋晶圓的產能,並創造3,400個高科技就業機會。

北美地區雖然發展落後,但在《晶片技術創新與應用法案》(CHIPS Act)的推動下正加速前進。已公佈的計劃預計將使該地區的資本支出加倍,從2024年的120億美元增加到2027年的247億美元。亞利桑那州和紐約州的先進封裝先導計畫旨在實現人工智慧加速器10微米以下的晶片佈局,從而減少對跨太平洋航線的依賴。日益嚴格的生產流程監管,尤其注重網路安全措施,正促使工廠努力取得CMMC和IPC-1791認證的可信任製造商資格。

歐洲正聚焦汽車功率半導體和寬能能隙帶裝置,英飛凌和意法半導體等公司正大力投資,以支持800V電動車逆變器的發展。該地區RoHS指令的擴展以及即將訂定的生態設計規則鼓勵使用可修復的印刷電路板,從而刺激了對選擇性焊接和返修平台的需求。歐洲技能契約(Skills Pact)旨在提升勞動力技能,該計劃與IPC認證的互連設計師課程相結合,目標是在2029年前解決14.6萬的勞動力缺口。

在中東和非洲,沙烏地阿拉伯和阿拉伯聯合大公國正透過主權財富基金投資科技園區,逐步推動相關工作。這些科技園區將電子製造服務(EMS)激勵措施與公用事業收費折扣結合。南非豪登省的科技園區吸引了電信設備翻新商,他們需要模組化表面貼裝技術(SMT)生產線來處理週轉時間短、種類繁多的維修訂單。然而,基礎設施匱乏和熟練勞動力短缺阻礙了撒哈拉以南非洲大多數市場採用先進設備。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 物聯網和穿戴式裝置的興起正在推動對高密度印刷電路基板的需求。

- 汽車ADAS電子設備應用趨勢

- 5G基礎設施和高頻基板的擴展

- 智慧型手機中的系統級封裝(SiP)整合

- 微型LED顯示器製造要求

- 新興經濟體的OEM外包給EMS公司

- 市場限制

- 高速裝配線需要較高的初始資本投入

- 無鉛焊料因熱限制造成的產量比率損失

- 半導體供應鏈波動導致運轉率下降

- 人工智慧驅動的檢測系統面臨技術純熟勞工短缺問題

- 價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 宏觀經濟趨勢的影響分析

第5章 市場規模與成長預測

- 按組件

- 被動元件

- 電阻器

- 電容器

- 主動元件

- 電晶體

- 積體電路

- 被動元件

- 透過裝置

- 放置設備

- 高速拾取放置設備

- 焊接設備

- 回流焊接爐

- 波峰焊接系統

- 檢測設備

- 自動光學檢測(AOI)

- 焊膏檢測 (SPI)

- X光

- 網版印刷設備

- 放置設備

- 按組裝類型

- 高品種、小批量生產(HMLV)

- 高容量/高混合 (HVHM)

- 按最終用戶行業分類

- 家用電子電器

- 車

- 工業電子

- 航太/國防

- 衛生保健

- 通訊和IT基礎設施

- 其他最終用戶

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 非洲

- 南非

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ASMPT Limited

- Fuji Corporation

- Yamaha Motor Co., Ltd.(SMT Division)

- Panasonic Holdings Corporation(Panasonic Smart Factory Solutions)

- Hanwha Precision Machinery Co., Ltd.

- Mycronic AB

- Juki Corporation

- Nordson Corporation

- Koh Young Technology Inc.

- Saki Corporation

- Test Research, Inc.(TRI)

- Viscom SE

- Europlacer Holdings Ltd.

- Shenzhen JT Automation Equipment Co., Ltd.

- Rehm Thermal Systems GmbH

- Heller Industries, Inc.

- MIRTEC Co., Ltd.

- Shenzhen NEODEN Technology Co., Ltd.

- Shenzhen JAGUAR Automation Equipment Co., Ltd.

- Hanwa Precision Machinery Co., Ltd.

第7章 市場機會與未來展望

The Surface Mount Technology market was valued at USD 6.61 billion in 2025 and estimated to grow from USD 7.11 billion in 2026 to reach USD 10.19 billion by 2031, at a CAGR of 7.49% during the forecast period (2026-2031).

Demand for miniaturized, high-density electronics in consumer devices, electric vehicles, and industrial automation is underpinning this trajectory. Accelerated deployment of 5 G infrastructure, growth in artificial-intelligence servers, and the spread of edge and IoT products are keeping production lines close to full capacity across Asia, North America, and Europe. Automotive original-equipment manufacturers now specify automotive-grade SMT solutions able to tolerate -40 °C to 150 °C thermal swings, further tightening equipment requirements. Meanwhile, micro-LED and System-in-Package (SiP) innovations are shifting placement accuracy expectations from +-25 µm toward the sub-10 µm realm. Supply-chain volatility, especially for semiconductors and high-precision ceramics, remains the primary brake on near-term throughput despite healthy end-market fundamentals.

Global Surface Mount Technology Market Trends and Insights

IoT and Wearables Fuel Ultra-Dense PCB Adoption

Device makers now pack more than 10,000 multilayer ceramic capacitors into a single smartwatch, tripling the count seen five years ago. To print conductive traces below 50 µm and microvias under 75 µm, assemblies rely on placement tools that consistently handle 01005 packages at +-25 µm accuracy. Compliance with FCC emissions limits and IEC safety requirements is pushing additional electromagnetic-interference shielding steps, elevating demand for precision solder-paste inspection and automated optical inspection systems.

Automotive ADAS Electronics Adoption Reshapes Reliability Needs

Electric-vehicle reference designs use upward of 10,000 MLCCs and more than 200 electronic control units each, lifting SMT volumes even as lifecycle qualification stretches beyond three years. ISO 26262 functional-safety mandates and -40 °C to 150 °C operating windows compel suppliers to certify processes under automotive PPAP and AEC-Q200 stress tests. Equipment makers that can validate long-term solder-joint reliability are winning multiyear supply agreements across Europe and Japan.

High Upfront Capex Constrains Smaller Firms

Next-generation placement platforms cost upward of USD 3 million per line when bundled with in-line SPI, AOI, and x-ray testers. Although predictive-maintenance analytics lower total cost of ownership, many small and medium EMS providers struggle to justify payback within three years. Equipment rental and outcome-based service contracts are emerging but remain uncommon outside Tier-1 OEMs.

Other drivers and restraints analyzed in the detailed report include:

- 5G Infrastructure and High-Frequency Boards

- System-in-Package Integration in Smartphones

- Lead-Free Solder Thermal Constraints Lower Yield

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Active Components accounted for 65.74% of the Surface Mount Technology market share in 2025 as MCU, ASIC, and power-management demand accelerated in AI servers and electric vehicles. The segment is forecast to grow at an 8.62% CAGR to 2031 on the back of increased adoption of heterogenous SoC designs and high-voltage transistors. Passive Components still benefit from rising unit counts in 5G handsets and automotive traction inverters, but ceramic and tantalum material shortages continue to test supply-chain resiliency.

Customer expectations are evolving from component cost control to board-level integration density and long-tail reliability. OEMs request sub-10 ppm failure rates and 15-year field lifetimes, driving closer collaboration between substrate vendors, component makers, and placement-equipment suppliers. Suppliers that deliver active-passive co-design libraries and full Design-for-Assembly review accelerate new-product ramps, securing supplier-of-choice status for advanced wearables and industrial IoT gateways.

Placement Equipment still commands 42.62% of the Surface Mount Technology market size in 2025, but Inspection Equipment is rising fastest with a 8.83% CAGR. High-speed pick-and-place machines now hit 100 k cph with +-10 µm accuracy, aided by machine-learning vision systems that auto-tune head pressure. Soldering Equipment faces process-window squeezes as lead-free alloys demand tighter thermal gradients, while Screen-Printing platforms adopt closed-loop SPI feedback to boost first-pass yield.

Investment momentum favors AOI and x-ray systems that harness deep learning to cut false-call rates by 90 % and raise inspection speed four-fold. ViTrox and Koh Young incorporate IPC-CFX connectivity for real-time analytics that flag yield-eroding trends within minutes. Equipment finance packages bundling analytics subscriptions help offset sticker shock, enticing Tier-2 EMS firms in Eastern Europe and Southeast Asia to upgrade lines.

The Surface Mount Technology Market Report is Segmented by Component (Passive Components [Resistors, Capacitors], and More), Equipment Type (Placement Equipment [High-Speed Pick-And-Place Machines], and More), Assembly Line Type (High-Mix/Low-Volume, and More), End-User Industry (Consumer Electronics, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated with 48.05% Surface Mount Technology market share in 2025 and is forecast to post an 8.12% CAGR through 2031. China, Taiwan, and South Korea together are slated to invest more than USD 84 billion in new 300 mm fabs by 2027, securing upstream substrate and component capacity. Japan's Kumamoto cluster, anchored by TSMC JASM's USD 20 billion expansion, adds over 100,000 12-inch wafers per month while creating 3,400 high-tech roles.

North America trails but is accelerating under the CHIPS Act, with announced projects doubling regional capacity investment from USD 12 billion in 2024 to USD 24.7 billion by 2027. Advanced packaging pilots in Arizona and New York target sub-10 µm placement for AI accelerators, reducing dependence on trans-Pacific shipping lanes. Regulatory emphasis on cyber-secure production flows nudges factories toward CMMC and IPC-1791 trusted builder accreditation.

Europe focuses on automotive power semiconductors and wide-band-gap devices, with Infineon and STMicroelectronics driving capital expenditure to support 800 V EV inverters. The region's RoHS expansion and incoming Ecodesign rules favor repairable PCBs, stimulating demand for selective soldering and rework platforms. Workforce upskilling programs under Europe's Pact for Skills align with IPC's certified interconnect designer curriculum, aiming to close a 146,000-worker gap by 2029.

Middle East and Africa makes incremental gains as Saudi Arabia and the UAE funnel sovereign-fund capital into tech parks that bundle EMS incentives with reduced utility tariffs. South Africa's Gauteng hub attracts telecom-equipment refurbishers that rely on modular SMT lines to process short-run, high-mix repair orders. Still, infrastructure gaps and limited specialist labor temper adoption of cutting-edge equipment in most sub-Saharan markets.

- ASMPT Limited

- Fuji Corporation

- Yamaha Motor Co., Ltd. (SMT Division)

- Panasonic Holdings Corporation (Panasonic Smart Factory Solutions)

- Hanwha Precision Machinery Co., Ltd.

- Mycronic AB

- Juki Corporation

- Nordson Corporation

- Koh Young Technology Inc.

- Saki Corporation

- Test Research, Inc. (TRI)

- Viscom SE

- Europlacer Holdings Ltd.

- Shenzhen JT Automation Equipment Co., Ltd.

- Rehm Thermal Systems GmbH

- Heller Industries, Inc.

- MIRTEC Co., Ltd.

- Shenzhen NEODEN Technology Co., Ltd.

- Shenzhen JAGUAR Automation Equipment Co., Ltd.

- Hanwa Precision Machinery Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of IoT and wearables driving high-density PCB demand

- 4.2.2 Automotive ADAS electronics adoption

- 4.2.3 Expansion of 5G infrastructure and high-frequency boards

- 4.2.4 System-in-Package (SiP) integration in smartphones

- 4.2.5 MicroLED display manufacturing requirements

- 4.2.6 OEM outsourcing to EMS firms in emerging economies

- 4.3 Market Restraints

- 4.3.1 High upfront capex for high-speed placement lines

- 4.3.2 Lead-free solder thermal constraints lowering yield

- 4.3.3 Semiconductor supply-chain volatility causing under-utilisation

- 4.3.4 Skilled labour shortage for AI-driven inspection systems

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Macroeconomic Trends Impact Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Component

- 5.1.1 Passive Components

- 5.1.1.1 Resistors

- 5.1.1.2 Capacitors

- 5.1.2 Active Components

- 5.1.2.1 Transistors

- 5.1.2.2 Integrated Circuits

- 5.1.1 Passive Components

- 5.2 By Equipment Type

- 5.2.1 Placement Equipment

- 5.2.1.1 High-speed Pick-and-Place Machines

- 5.2.2 Soldering Equipment

- 5.2.2.1 Reflow Ovens

- 5.2.2.2 Wave Solder Systems

- 5.2.3 Inspection Equipment

- 5.2.3.1 Automated Optical Inspection (AOI)

- 5.2.3.2 Solder Paste Inspection (SPI)

- 5.2.3.3 X-ray Inspection

- 5.2.4 Screen Printing Equipment

- 5.2.1 Placement Equipment

- 5.3 By Assembly Line Type

- 5.3.1 High-Mix / Low-Volume (HMLV)

- 5.3.2 High-Volume / High-Mix (HVHM)

- 5.4 By End-user Industry

- 5.4.1 Consumer Electronics

- 5.4.2 Automotive

- 5.4.3 Industrial Electronics

- 5.4.4 Aerospace and Defense

- 5.4.5 Healthcare

- 5.4.6 Telecom and IT Infrastructure

- 5.4.7 Other End-users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 India

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Saudi Arabia

- 5.5.4.2 United Arab Emirates

- 5.5.4.3 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ASMPT Limited

- 6.4.2 Fuji Corporation

- 6.4.3 Yamaha Motor Co., Ltd. (SMT Division)

- 6.4.4 Panasonic Holdings Corporation (Panasonic Smart Factory Solutions)

- 6.4.5 Hanwha Precision Machinery Co., Ltd.

- 6.4.6 Mycronic AB

- 6.4.7 Juki Corporation

- 6.4.8 Nordson Corporation

- 6.4.9 Koh Young Technology Inc.

- 6.4.10 Saki Corporation

- 6.4.11 Test Research, Inc. (TRI)

- 6.4.12 Viscom SE

- 6.4.13 Europlacer Holdings Ltd.

- 6.4.14 Shenzhen JT Automation Equipment Co., Ltd.

- 6.4.15 Rehm Thermal Systems GmbH

- 6.4.16 Heller Industries, Inc.

- 6.4.17 MIRTEC Co., Ltd.

- 6.4.18 Shenzhen NEODEN Technology Co., Ltd.

- 6.4.19 Shenzhen JAGUAR Automation Equipment Co., Ltd.

- 6.4.20 Hanwa Precision Machinery Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

表面黏著技術市場:全球市場預測,2026-2032年

表面黏著技術市場:全球市場預測,2026-2032年 2026-2030年全球表面黏著技術(SMT)設備市場

2026-2030年全球表面黏著技術(SMT)設備市場 全球表面黏著技術(SMT)設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球表面黏著技術(SMT)設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 表面黏著技術市場:依設備和地區分類表面黏著技術開關市場:依產品類型、驅動力、安裝位置和應用分類-2026-2032年全球預測

表面黏著技術市場:依設備和地區分類表面黏著技術開關市場:依產品類型、驅動力、安裝位置和應用分類-2026-2032年全球預測 全球表面黏著技術市場:依設備、服務、應用、國家及地區分類-產業分析、市場規模、佔有率及2025年至2032年未來預測

全球表面黏著技術市場:依設備、服務、應用、國家及地區分類-產業分析、市場規模、佔有率及2025年至2032年未來預測 表面黏著技術(SMT) 市場分析及預測至 2035 年:依類型、產品類型、服務、技術、組件、應用、製程、最終用戶、設備分類全球表面黏著技術開關市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

表面黏著技術(SMT) 市場分析及預測至 2035 年:依類型、產品類型、服務、技術、組件、應用、製程、最終用戶、設備分類全球表面黏著技術開關市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球表面黏著技術(SMT)設備市場報告

2026年全球表面黏著技術(SMT)設備市場報告 表面黏著技術市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、終端用戶產業、地區及競爭格局分類,2021-2031年)

表面黏著技術市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、終端用戶產業、地區及競爭格局分類,2021-2031年)