|

市場調查報告書

商品編碼

1940686

美國智慧電視:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)US Smart TV - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

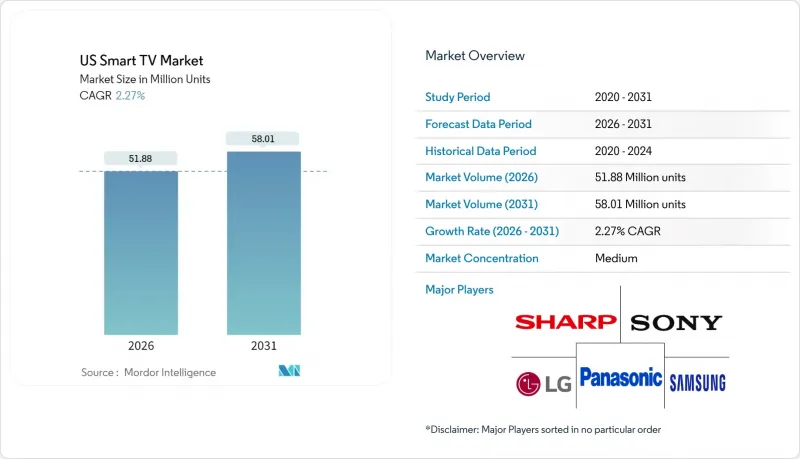

2025年美國智慧電視市場價值為5,073萬台,預計2031年將達到5,801萬台,高於2026年的5,188萬台。

預計在預測期(2026-2031 年)內,複合年成長率將達到 2.27%。

儘管成熟消費性電子產品類別的整體成長放緩,但終端用戶的需求正轉向更高的影像品質、整合串流環境和遊戲功能。雖然55-64吋的大尺寸電視仍然主導著主流市場,但超大螢幕(75吋以上)正成為消費者夢寐以求的購買選擇。同時,面板技術創新週期的加速發展(層級構造OLED、mini-LED和新興的RGB背光技術)正在縮短更換週期。透過聯網電視(CTV)廣告實現的平台獲利正在抵消硬體價格上漲的影響,幫助品牌在面對來自中國新興廠商的價格壓力時保持市場佔有率。最後,各州層級的節能激勵措施和日益嚴格的資料隱私法規正在推動產品研發的優先事項,凸顯了美國智慧型電視市場複雜的法規環境。

美國智慧電視市場趨勢與洞察

快速 4K/8K 升級週期

儘管4K超高清電視的出貨量仍佔一半以上,但製造商正透過推廣支援8K的處理器和先進的背光技術來縮短技術週期。三星的2025年RGB Mini-LED原型機實現了OLED等級的對比度,同時保持了與LCD電視的成本競爭力。 LG的層級構造OLED架構將峰值亮度提升了40%,並克服了先前阻礙高階機型普及的HDR限制。這些突破性進展可能會促使現有用戶更快更換,尤其是在串流媒體服務和次世代遊戲主機逐步提供原生8K內容的情況下。

內建串流媒體和應用生態系統

智慧型電視作業系統如今已能複製外部電視棒的功能,將應用程式商店、支付和定向廣告整合到電視品牌之下。 Roku OS 仍佔據最大的市場佔有率,但 Google TV 的成長速度最快,搜尋個人化功能顯著提升了用戶的觀看時間。 LG 報告稱,其 webOS 廣告技術的收入將在 2024 年超過 1 兆韓元,這證明平台經濟效益正在抵消硬體利潤率下降的影響。

透過智慧型手機/平板電腦觀看內容而導致的同類相食

行動裝置螢幕日益佔據白天的娛樂時間,限制了以往促使人們更換到更大螢幕的共用觀看機會。美國聯邦貿易委員會 (FTC) 2024 年的一項研究指出,串流平台過度最佳化其行動裝置的 UI 設計,強化了單人觀看的習慣。然而,遊戲和優質電影內容仍然是電視的優勢所在,在某種程度上緩解了這種蠶食效應。

細分市場分析

55-64吋尺寸段將保持領先地位,到2025年仍將佔據34.02%的出貨量佔有率,鞏固其作為主流用戶理想尺寸的地位。然而,75吋以上尺寸的電視市場將以2.69%的複合年成長率成長最快,超過美國智慧電視市場的整體成長速度。早期採用者之所以願意以低於2000美元的促銷價格購買更大尺寸的面板,是因為他們追求身臨其境型的遊戲體驗和影院級串流媒體播放效果。三星憑藉其microLED供應鏈和積極的促銷策略,已佔據超大尺寸電視市場約三分之一的佔有率。同時,由於價格親民的平板電腦和適合緊湊型住宅的窄邊框中型電視的興起,入門級45英寸以下尺寸的電視市場將持續萎縮。

安裝人員報告稱,無線分線盒可將安裝時間縮短約 40%,從而加速現有住宅中 75 吋壁掛式螢幕的普及。能源之星 (ENERGY STAR) 的數據顯示,每平方英吋的功耗下降速度快於面板面積的成長速度,這緩解了注重節能的消費者對電費的擔憂。綜上所述,這些趨勢意味著大尺寸顯示器將繼續成為美國智慧型電視市場的關鍵驅動力。

4K 超高清已成為標配,預計到 2025 年出貨量將達到 54.02%。新興的 8K 市場預計將以 3.17% 的複合年成長率成長,這主要得益於人工智慧影像增強引擎彌補了片源不足的問題。微軟的 Xbox Series X 和SONY的 PlayStation 5 Pro 將在 2025 年透過韌體更新支援 8K 輸出,串流媒體服務供應商也已開始在部分市場試行 8K 視訊點播服務。為了抵消更高的價格,商家提升銷售8K 面板與短期分期付款計劃結合,鼓勵早期採用者每三到四年更換。目前,全高清電視主要以特賣產品的形式出現在旅館業和注重性價比的零售商處。

OLED 廠商聲稱,亮度提升將縮小 8K 相對於高品質 4K HDR 的優勢,但調查數據顯示,早期遊戲玩家尤其傾向於選擇 8K 電視,因為其擁有卓越的性能標竿。隨著壓縮轉碼器的成熟,8K 串流媒體的頻寬開銷將降低,從而消除大規模部署的最後一道技術障礙。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 快速 4K/8K 升級週期

- 內建串流媒體和應用生態系統

- 65吋以上產品的銷售量激增

- 與OEM廠商分享CTV廣告收入

- 遊戲最佳化電視功能(可變更新率、雲端遊戲中心)

- 符合「能源之星9.0」標準的節能產品可享稅收優惠

- 市場限制

- 智慧型手機和平板電腦爭奪觀看時間

- 透過低成本的中國品牌降低價格

- 作業系統層面的資料隱私保護措施限制了遙測資料的價值

- 迷你LED背光燈供應鏈波動

- 價值鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 產業價值鏈圖

第5章 市場規模與成長預測

- 按螢幕尺寸

- 小於 45 英寸

- 45 至 54 英寸

- 55 至 64 英寸

- 65 至 74 英寸

- 75吋或以上

- 按解析度類型

- HDTV

- 全高清

- 4K UHD

- 8K UHD

- 透過面板技術

- LCD/LED

- QLED

- OLED

- Mini-LED

- 按價格範圍

- 低於 500 美元

- 500-999美元

- 1,000-1,999 美元

- 超過2000美元

- 按作業系統

- Roku OS

- Google/Android TV

- Tizen OS

- webOS

- Fire TV OS

- VIDAA U

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 供應商市場排名分析

- 公司簡介

- Samsung Electronics Co., Ltd.

- LG Electronics Inc.

- Sony Group Corporation

- TCL Electronics Holdings Ltd.

- VIZIO Holding Corp.

- Hisense Group Co., Ltd.

- Panasonic Holdings Corporation

- Sharp Corporation

- Koninklijke Philips NV

- Skyworth Group Ltd.

- Xiaomi Corp.

- Amazon.com Inc.(Fire TV Devices)

- Apple Inc.(Apple TV & tvOS Integrations)

- Haier Smart Home Co., Ltd.

- Funai Electric Co., Ltd.(Magnavox/Sanyo)

- Westinghouse Electric Corp.

- Sceptre Inc.

- Insignia Systems Inc.(Insignia TV)

- JVC Kenwood Corp.

- Pioneer Corp.

- Seiki Digital Inc.

- Element Electronics LLC

- Hitachi Ltd.

- LeEco(LeTV)

- Metz Consumer Electronics GmbH

- B&O A/S(Bang & Olufsen)

第7章 市場機會與未來展望

The US Smart TV market was valued at 50.73 million units in 2025 and estimated to grow from 51.88 million units in 2026 to reach 58.01 million units by 2031, at a CAGR of 2.27% during the forecast period (2026-2031).

End-user demand is shifting toward premium picture quality, integrated streaming ecosystems, and gaming-ready features, even as overall growth moderates in a maturing consumer electronics category. The momentum behind large formats, notably 55-64 inch sets, continues to anchor mainstream volumes, while ultra-large 75-inch-plus screens turn into the primary aspirational purchase. At the same time, panel innovation cycles, 4-stack OLED, mini-LED, and emerging RGB backlighting, are shortening replacement timelines. Platform monetization through connected-TV (CTV) advertising now subsidizes hardware prices, helping brands defend unit share against aggressive price compression from new Chinese entrants. Finally, state-level energy incentives and tightening data-privacy rules both shape product development priorities, underlining the complex regulatory environment surrounding the US Smart TV market.

US Smart TV Market Trends and Insights

Rapid 4K/8K upgrade cycle

4K UHD already dominates more than half of shipments, yet manufacturers are shortening the technology cycle by mainstreaming 8K-ready processors and advanced backlighting. Samsung's RGB mini-LED prototypes shown in 2025 promise OLED-level contrast while holding LCD cost parity. LG's four-stack OLED architecture lifts peak brightness by 40%, solving HDR limitations that once slowed premium adoption. These step-changes jointly nudge existing owners toward earlier replacement, especially as streaming and next-gen consoles gradually expose 8K native content.

Built-in streaming and app ecosystems

Smart-TV operating systems now replicate the functionality of external sticks, bringing storefronts, payments, and targeted ads under the television brand. Roku OS still accounts for the largest footprint, but Google TV is the fastest riser as search personalization drives watch-time. LG reports that its webOS ad-tech revenue surpassed KRW 1 trillion in 2024, proof that platform economics increasingly offset hardware margin compression.

Smartphone/tablet viewing cannibalization

Mobile screens increasingly capture daytime entertainment minutes, limiting shared viewing occasions that traditionally justified large-screen upgrades. The Federal Trade Commission's 2024 study highlights how streaming platforms over-index their UI design for handheld devices, reinforcing single-user consumption habits. Yet gaming and premium cinematic content remain television strongholds, tempering the cannibalization effect.

Other drivers and restraints analyzed in the detailed report include:

- Surge in larger-than-65" purchases

- CTV advertising revenue sharing creates new business models

- Price compression from low-cost Chinese brands

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 55-64 inch band retained a leading 34.02% shipment share in 2025, confirming its role as the mainstream sweet spot. However, the 75-inch-plus segment is set to grow fastest at 2.69% CAGR, outpacing overall US Smart TV market growth. Early adopters cite immersive gaming and theater-grade streaming as justification for purchasing panels that now cost under USD 2,000 at promotion. Samsung commands roughly one-third of ultra-large formats by leveraging its micro-LED supply chain and aggressive channel promotions. Entry-level sub-45-inch models continue sliding, squeezed by cheap tablets for personal viewing and by mid-sized sets that increasingly fit smaller apartments thanks to bezel minimization.

Installers report that wireless breakout boxes reduce setup time by almost 40%, accelerating acceptance of wall-mounted 75-inch screens in existing homes. ENERGY STAR data suggest power consumption per square inch is falling faster than panel area is rising, muting electricity-cost objections among energy-conscious buyers. Collectively, these trends mean that large-format displays will remain the headline growth driver inside the US Smart TV market.

4K UHD reached 54.02% shipment share in 2025, having already become table stakes. The nascent 8K segment is projected to post a 3.17% CAGR, aided by AI-upscaling engines that mask source-content scarcity. Microsoft's Xbox Series X and Sony's PlayStation 5 Pro both enabled 8K output in 2025 firmware updates, and streaming providers have begun test runs of 8K VOD in limited markets. Upsell tactics pair 8K panels with shorter finance plans to offset sticker shock, ensuring early adopters rotate into the pool every 3-4 years. Full-HD models now survive mainly in hospitality and price-first retail doorbusters.

OLED providers argue that brightness gains close the perceived advantage of 8K over high-quality 4K HDR, but survey data show that early gamers disproportionately choose 8K sets for their benchmarking bragging rights. As compression codecs mature, bandwidth overhead for 8K streams will fall, removing one of the last technical hurdles to mass deployment.

The US Smart TV Market Report is Segmented by Screen Size (Up To 45", 45-54", 55-64", 65-74", 75" & Above), Resolution Type (HDTV, Full HD, 4K UHD, 8K UHD), Panel Technology (LCD/LED, QLED, OLED, Mini-LED), Price Band (less Than USD 500, USD 500-999, and More), Operating System (Roku OS, Google/Android TV, and More), and Geography. The Market Forecasts are Provided in Terms of Volume (Units).

List of Companies Covered in this Report:

- Samsung Electronics Co., Ltd.

- LG Electronics Inc.

- Sony Group Corporation

- TCL Electronics Holdings Ltd.

- VIZIO Holding Corp.

- Hisense Group Co., Ltd.

- Panasonic Holdings Corporation

- Sharp Corporation

- Koninklijke Philips N.V.

- Skyworth Group Ltd.

- Xiaomi Corp.

- Amazon.com Inc. (Fire TV Devices)

- Apple Inc. (Apple TV & tvOS Integrations)

- Haier Smart Home Co., Ltd.

- Funai Electric Co., Ltd. (Magnavox/Sanyo)

- Westinghouse Electric Corp.

- Sceptre Inc.

- Insignia Systems Inc. (Insignia TV)

- JVC Kenwood Corp.

- Pioneer Corp.

- Seiki Digital Inc.

- Element Electronics LLC

- Hitachi Ltd.

- LeEco (LeTV)

- Metz Consumer Electronics GmbH

- B&O A/S (Bang & Olufsen)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid 4K/8K upgrade cycle

- 4.2.2 Built-in streaming and app ecosystems

- 4.2.3 Surge in larger-than-65" purchases

- 4.2.4 CTV advertising-revenue sharing with OEMs

- 4.2.5 Gaming-optimized TV features (VRR, cloud gaming hubs)

- 4.2.6 Energy-efficiency tax incentives for "ENERGY STAR 9.0" sets

- 4.3 Market Restraints

- 4.3.1 Smartphone/tablet viewing cannibalization

- 4.3.2 Price compression from low-cost Chinese brands

- 4.3.3 OS-level data-privacy pushback curbing telemetry value

- 4.3.4 Supply-chain volatility in mini-LED backlights

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Industry Value-Chain Mapping

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By Screen Size

- 5.1.1 Up to 45"

- 5.1.2 45-54"

- 5.1.3 55-64"

- 5.1.4 65-74"

- 5.1.5 75" and Above

- 5.2 By Resolution Type

- 5.2.1 HDTV

- 5.2.2 Full HD

- 5.2.3 4K UHD

- 5.2.4 8K UHD

- 5.3 By Panel Technology

- 5.3.1 LCD/LED

- 5.3.2 QLED

- 5.3.3 OLED

- 5.3.4 Mini-LED

- 5.4 By Price Band

- 5.4.1 less than USD 500

- 5.4.2 USD 500-999

- 5.4.3 USD 1,000-1,999

- 5.4.4 More than USD 2,000

- 5.5 By Operating System

- 5.5.1 Roku OS

- 5.5.2 Google/Android TV

- 5.5.3 Tizen OS

- 5.5.4 webOS

- 5.5.5 Fire TV OS

- 5.5.6 VIDAA U

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Vendor Market Ranking Analysis

- 6.5 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.5.1 Samsung Electronics Co., Ltd.

- 6.5.2 LG Electronics Inc.

- 6.5.3 Sony Group Corporation

- 6.5.4 TCL Electronics Holdings Ltd.

- 6.5.5 VIZIO Holding Corp.

- 6.5.6 Hisense Group Co., Ltd.

- 6.5.7 Panasonic Holdings Corporation

- 6.5.8 Sharp Corporation

- 6.5.9 Koninklijke Philips N.V.

- 6.5.10 Skyworth Group Ltd.

- 6.5.11 Xiaomi Corp.

- 6.5.12 Amazon.com Inc. (Fire TV Devices)

- 6.5.13 Apple Inc. (Apple TV & tvOS Integrations)

- 6.5.14 Haier Smart Home Co., Ltd.

- 6.5.15 Funai Electric Co., Ltd. (Magnavox/Sanyo)

- 6.5.16 Westinghouse Electric Corp.

- 6.5.17 Sceptre Inc.

- 6.5.18 Insignia Systems Inc. (Insignia TV)

- 6.5.19 JVC Kenwood Corp.

- 6.5.20 Pioneer Corp.

- 6.5.21 Seiki Digital Inc.

- 6.5.22 Element Electronics LLC

- 6.5.23 Hitachi Ltd.

- 6.5.24 LeEco (LeTV)

- 6.5.25 Metz Consumer Electronics GmbH

- 6.5.26 B&O A/S (Bang & Olufsen)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

智慧電視市場:2026-2032年全球市場預測(按顯示技術、螢幕大小、解析度、銷售管道和應用分類)

智慧電視市場:2026-2032年全球市場預測(按顯示技術、螢幕大小、解析度、銷售管道和應用分類) 智慧電視市場:按螢幕大小、顯示技術、作業系統和地區分類網路電視市場:2026年至2032年全球預測(依顯示技術、解析度、螢幕大小、作業系統和應用程式分類)

智慧電視市場:按螢幕大小、顯示技術、作業系統和地區分類網路電視市場:2026年至2032年全球預測(依顯示技術、解析度、螢幕大小、作業系統和應用程式分類) 2026年全球體育賽事線上影片市場報告智慧電視晶片市場:按類型、解析度、最終用戶和地區分類

2026年全球體育賽事線上影片市場報告智慧電視晶片市場:按類型、解析度、最終用戶和地區分類 智慧電視市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、功能、安裝類型、最終用戶及模式分類

智慧電視市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、功能、安裝類型、最終用戶及模式分類 全球智慧電視市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球智慧電視市場規模、佔有率、趨勢和成長分析報告(2026-2034) 智慧型電視晶片市場:按類型、解析度、最終用戶、國家和地區分類-全球產業分析、市場規模、市場佔有率及2025年至2032年預測

智慧型電視晶片市場:按類型、解析度、最終用戶、國家和地區分類-全球產業分析、市場規模、市場佔有率及2025年至2032年預測 智慧電視市場規模、佔有率、趨勢和預測(按解析度類型、螢幕大小、螢幕類型、技術、平台、分銷管道、應用和地區分類),2026-2034年

智慧電視市場規模、佔有率、趨勢和預測(按解析度類型、螢幕大小、螢幕類型、技術、平台、分銷管道、應用和地區分類),2026-2034年 智慧電視市場規模、佔有率和趨勢分析報告:按解析度、螢幕尺寸、作業系統、分銷管道、技術、地區和細分市場預測(2026-2033 年)

智慧電視市場規模、佔有率和趨勢分析報告:按解析度、螢幕尺寸、作業系統、分銷管道、技術、地區和細分市場預測(2026-2033 年)