|

市場調查報告書

商品編碼

1940685

非洲包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Africa Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

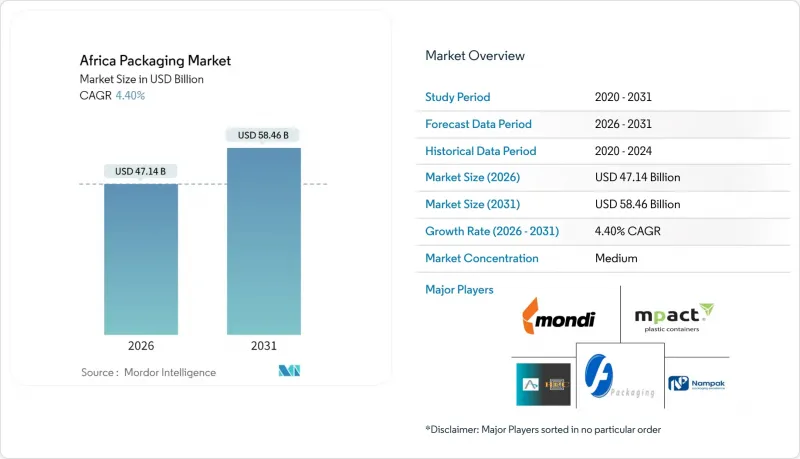

預計非洲包裝市場將從 2025 年的 451.5 億美元成長到 2026 年的 471.4 億美元,並預計到 2031 年將達到 584.6 億美元,2026 年至 2031 年的複合年成長率為 4.4%。

這一穩定成長的趨勢歸功於都市區的成長、電子商務活動的擴張以及整個非洲大陸對永續性的積極政策支持。快速的都市化正在改變消費者的消費習慣,使其轉向品牌產品和分量控制產品,而現代零售連鎖店和數位商務通路則進一步提升了對能夠最佳化保存期限和物流的靈活包裝的需求。儘管塑膠仍佔據最大佔有率,但政府對一次性塑膠的禁令為紙質包裝的替代方案創造了即時機會。全球飲料和汽車品牌的基礎設施投資也推動了對符合生產者延伸責任制(EPR)計畫的一級、二級和三級包裝的需求。受港口長期擁擠的限制,供應鏈本地化舉措正促使品牌所有者在更靠近終端市場的地區採購原料,從而縮短前置作業時間並穩定投入成本。

非洲包裝市場趨勢與洞察

不斷壯大的都市區中產階級推動了快速消費品消費。

預計到2050年,非洲的都市區將增加7億,這將使加工食品和品牌化妝品的購買力更加集中。隨著家庭收入的成長,消費者更傾向於選擇衛生、便利且保存期限長的包裝產品。軟包裝袋和單份包裝袋價格實惠,方便控制份量。零售商正在擴大自有品牌產品線,這促使人們對跨境統一包裝規範的需求日益成長,並加速了區域標準化進程。 《非洲大陸自由貿易協定》(AfCFTA)促進了跨境分銷,並鼓勵加工商部署寬幅印刷和擠出生產線,使其能夠從單一地點服務多個國家。因此,非洲包裝市場對輕質複合材料和專為常溫食品設計的阻隔膜的訂單不斷成長。

電子商務包裝需求快速成長

預計到2026年,數位商務規模將達到720億美元,年成長率達25%,這將支撐獨特的物流鏈,進而推動對二級和三級包裝的需求。與實體店配送相比,線上訂單需要經過更多處理步驟,這迫使品牌所有者指定使用邊緣加固、帶有緩衝墊和防篡改功能的紙板運輸箱。行動支付的普及,尤其是在肯亞,使得貨到付款模式得以延續,這就要求小包裹在付款確認前能夠承受多次處理。中小企業(SME)目前正利用本地B2B市場分銷工業備件和農業用品,從而推動了對保護性包裝膜和氣泡郵寄袋的需求。永續性仍然是關注的重點,這促使人們採用符合回收目標且不影響跌落測試表現的單一材料郵寄袋。隨著加工商將業務拓展到客製化印刷的電商包裝套和回郵信封領域,這些相互關聯的趨勢為非洲包裝市場提供了進一步的成長潛力。

聚合物、紙漿和紙張價格波動

自2024年以來,由於西非貨幣走弱和運費溢價上漲,基準聚丙烯價格波動劇烈。儘管奈及利亞年產90萬噸的丹格特集團為區域供應提供了穩定性,但出口利潤豐厚,對國內價格的影響有限。同樣,加彭的森林砍伐限制和喀麥隆造紙廠的縮減規模也減少了當地原料供應,給紙板市場帶來壓力。這種波動正在侵蝕加工商的利潤率,並使與品牌所有者的年度價格調整談判變得更加複雜。一些軟包裝薄膜生產商正在使用碳酸鈣填料來減少樹脂用量,但性能的妥協限制了其應用範圍,使其僅適用於低阻隔產品。由此產生的成本轉嫁風險預計將使非洲包裝市場近期複合年成長率預測值下降至多0.7個百分點。

細分市場分析

到2025年,塑膠包裝將維持43.62%的非洲包裝市場佔有率,這主要得益於其成本效益以及在瓶裝、袋裝和熱成型托盤等多種包裝形式上的多功能性。 PET和PP材料因其透明度和抗摔性,在碳酸飲料和個人保健產品領域仍佔據重要地位。然而,由於生產者延伸責任制(EPR)的擴展導致合規成本不斷增加,這一領域正面臨挑戰。因此,消費品製造商正在對紙製品進行預先認證,以作為外帶食品包裝和購物袋的替代品。儘管紙板的基準,但預計其在非洲包裝市場中將以6.05%的複合年成長率快速成長,因為折疊紙盒和瓦楞紙箱既滿足了監管要求,也滿足了品牌永續性的迫切需求。金屬罐和玻璃瓶憑藉惰性和現有的回收循環,在啤酒、能量飲料和製藥行業佔據了穩固的市場佔有率。然而,除南非和埃及以外,玻璃熔爐產能有限,這將限制其市場佔有率的快速成長。聚烯生產商正透過創新生產更薄的薄膜和一體式瓶蓋來應對挑戰,這些產品符合減少廢棄物排放的法規。總體而言,這些變化表明,儘管塑膠仍將保持其銷售主導地位,但非洲包裝市場的增值將轉向纖維材料和混合結構,這些材料和結構既能滿足廢棄物處理標準,又不影響產品保護。

阻隔性能、成本和政策的互補動態正在影響加工商的投資決策。瓦楞紙板廠正在升級晶粒設備,以生產底部帶有壓鎖的電商運輸箱,從而服務國內中小企業和跨國履約中心。同時,區域樹脂分銷商正在提供與布蘭特原油價格掛鉤的長期供應契約,以此作為一項針對大批量用戶的價格緩解措施。在研發方面,一個南非產學研聯盟正在測試一種甘蔗衍生的生物基聚乙烯薄膜,可在現有擠出生產線上運作。這些措施旨在促進原料的在地採購和循環經濟,標誌著「產品組合多元化時代」的到來,並將在未來五年內逐步重新平衡非洲包裝產業的材料結構。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 不斷壯大的都市區中產階級推動了快速消費品消費。

- 電子商務包裝需求快速成長

- 現代零售連鎖店在非洲的擴張

- 政府對一次性塑膠製品的禁令推動了對替代材料的需求。

- 生鮮食品出口低溫運輸物流的興起

- 進口散件汽車需要三級保護包裝

- 市場限制

- 聚合物、紙漿和紙張價格波動

- 由於電力供應不穩定,工廠營運費用(OPEX)增加

- 由於港口堵塞,原料流入延遲

- 回收基礎設施的缺乏限制了再生PET(rPET)的廣泛應用。

- 產業價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 競爭對手之間的競爭

- 替代品的威脅

- 宏觀經濟因素如何影響市場

- 投資分析

- 全球包裝市場概覽

第5章 市場規模與成長預測

- 按包裝類型

- 塑膠包裝

- 按類型

- 硬質塑膠包裝

- 依材料類型

- 聚乙烯(PE)

- 聚丙烯(PP)

- 聚對苯二甲酸乙二醇酯(PET)

- 聚氯乙烯(PVC)

- 聚苯乙烯(PS)和發泡聚苯乙烯(EPS)

- 其他材料類型

- 依產品類型

- 瓶子和罐子

- 瓶蓋和封口

- 托盤和容器

- 其他產品類型

- 按最終用途行業分類

- 食物

- 飲料

- 製藥

- 化妝品和個人護理

- 工業的

- 其他終端用戶產業

- 依材料類型

- 軟塑膠包裝

- 依材料類型

- 聚乙烯(PE)

- 雙軸延伸聚丙烯(BOPP)

- 流延聚丙烯(CPP)

- 其他材料類型

- 依產品類型

- 小袋和包裝袋

- 薄膜和包裝

- 其他產品類型

- 按最終用途行業分類

- 食物

- 飲料

- 製藥

- 化妝品和個人護理

- 工業的

- 其他終端用戶產業

- 依材料類型

- 硬質塑膠包裝

- 依產品類型

- 瓶子和罐子

- 小袋和包裝袋

- 散裝產品

- 其他產品類型

- 按最終用途行業分類

- 食物

- 飲料

- 化妝品和個人護理

- 製藥

- 工業的

- 其他終端用戶產業

- 按類型

- 紙包裝

- 依產品類型

- 折疊紙箱

- 瓦楞紙箱

- 液態紙板

- 其他產品類型

- 按最終用途行業分類

- 食物

- 飲料

- 電子商務

- 其他終端用戶產業

- 依產品類型

- 容器玻璃

- 按顏色

- 綠色的

- 琥珀色

- 燧石

- 其他顏色

- 按最終用途行業分類

- 食物

- 飲料

- 酒精飲料

- 不含酒精的飲料

- 個人護理和化妝品

- 藥品(不含管瓶和安瓿瓶)

- 香水

- 按顏色

- 金屬罐和容器

- 依材料類型

- 鋼材

- 鋁

- 依產品類型

- 能

- 鼓和桶

- 瓶蓋和封口

- 其他產品類型

- 按最終用途行業分類

- 食物

- 飲料

- 化學品/石油

- 工業的

- 油漆和塗料

- 其他終端用戶產業

- 依材料類型

- 塑膠包裝

- 按包裝類型

- 難的

- 靈活的

- 按最終用途行業分類

- 食物

- 飲料

- 製藥和醫療保健

- 個人護理和化妝品

- 工業的

- 電子商務

- 其他終端用戶產業

- 按國家/地區

- 埃及

- 奈及利亞

- 肯亞

- 南非

- 其他非洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Amcor plc

- Mondi plc

- Nampak Ltd

- Mpact Ltd

- Tetra Pak International SA

- Sealed Air Corp.

- Constantia Flexibles Group GmbH

- Consol Holdings(Pty)Ltd

- Astrapak Ltd(RPC Packaging Holdings Ltd)

- Foster Packaging International(Pty)Ltd

- East African Packaging Industries Ltd

- Bonpak(Pty)Ltd

- Huhtamaki Oyj

- Ardagh Group SA

- Smurfit WestRock

- Novus Holdings Ltd

- Greif Inc.

- Sonoco Products Company

- Frigoglass SAIC

第7章 市場機會與未來展望

The Africa packaging market is expected to grow from USD 45.15 billion in 2025 to USD 47.14 billion in 2026 and is forecast to reach USD 58.46 billion by 2031 at 4.4% CAGR over 2026-2031.

This steady trajectory stems from rising urban populations, expanding e-commerce activity, and active policy support for sustainability across the continent. Rapid urbanization is reshaping consumer habits toward branded, portion-controlled goods, while modern retail chains and digital commerce channels are deepening demand for flexible packs that optimize shelf life and logistics. Government bans on single-use plastics are creating immediate substitution opportunities for paper-based formats, even as plastic retains the biggest share. Infrastructure investments by global beverage and automotive brands are also lifting demand for primary, secondary, and tertiary packs that comply with Extended Producer Responsibility programs. Supply-chain localization efforts-triggered by chronic port congestion- are prompting brand owners to source materials closer to end markets, shortening lead times and stabilizing input costs.

Africa Packaging Market Trends and Insights

Growing Urban Middle Class Boosting FMCG Consumption

Africa's cities are projected to add 700 million residents by 2050, channeling purchasing power toward processed foods and branded personal-care items. As household incomes rise, consumers prefer packaged goods that promise hygiene, convenience, and longer shelf life. Flexible pouches and unit-dose sachets cater to portion control while meeting affordability thresholds. Retailers are expanding private-label assortments that demand consistent pack specifications across borders, accelerating regional standardization. The African Continental Free Trade Agreement is smoothing cross-border flows, encouraging converters to install wider web presses and extrusion lines that can serve multiple countries from one hub. Consequently, the Africa packaging market is experiencing higher order volumes for lightweight laminates and barrier films tailored to shelf-stable groceries.

E-commerce Packaging Demand Surge

Digital commerce is forecast to reach USD 72 billion by 2026, growing 25% annually and underpinning a distinct logistics chain that elevates secondary and tertiary packaging needs. Online orders endure more touch points than store-delivered goods, compelling brand owners to specify corrugated shippers with reinforced edges, void fill, and tamper-evident closures. Mobile-money prevalence, notably in Kenya, sustains cash-on-delivery models that require parcels to withstand multiple handling events before payment confirmation. SMEs now leverage regional B2B marketplaces that move industrial spares and agricultural inputs, expanding demand for protective wraps and bubble mailers. Sustainability remains top of mind, spurring the uptake of mono-material mailers that meet recyclability targets without sacrificing drop-test performance. These intertwined dynamics add headroom for the Africa packaging market as converters diversify into custom-printed e-commerce sleeves and return-ready envelopes.

Volatile Polymer and Paper Pulp Prices

Benchmark polypropylene prices have whipsawed since 2024 as West-African currencies weakened and freight surcharges mounted. While Nigeria's 900,000-tonne Dangote complex offers regional supply security, exports capture premium margins overseas, muting domestic price relief. Paperboard markets are likewise pressured by forestry caps in Gabon and mill curtailments in Cameroon, shrinking local furnish availability. Such volatility erodes converter margins and complicates annual price-adjustment negotiations with brand owners. Some flexible-film producers are substituting calcium-carbonate fillers to trim resin content, but property trade-offs limit usage to low-barrier SKUs. The resulting cost-pass-through risk subtracts up to 0.7 percentage points from the Africa packaging market's near-term CAGR forecast.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Modern Retail Chains Across Africa

- Government Bans on Single-Use Plastics Driving Alternative Materials

- Power-Supply Instability Increasing Plant OPEX

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastic packaging retained 43.62% Africa packaging market share in 2025 on the back of cost-efficiency and versatility in bottles, pouches and thermoformed trays. PET and PP formats remained vital for carbonated beverages and personal-care items owing to clarity and drop resistance. Yet the segment faces escalating compliance costs as Extended Producer Responsibility levies expand, prompting fast-moving consumer-goods companies to pre-qualify paper substitutions for takeaway food wraps and carrier bags. Paperboard, while holding a smaller baseline, is slated for a 6.05% CAGR, the fastest within Africa packaging market, as folding cartons and corrugated cases satisfy both regulatory and brand-sustainability mandates. Metal cans and glass bottles occupy resilient niches in beer, energy drinks and pharmaceuticals, benefitting from inertness and existing recycling loops. However, limited glass furnace capacity outside South Africa and Egypt constrains rapid share gains. Polyolefin producers navigate this landscape by marketing down-gauged films and tethered-cap innovations that align with litter-reduction rules. Collectively, these shifts indicate that while plastics will continue to dominate volumes, incremental value creation in the Africa packaging market will migrate toward fiber and hybrid structures that meet end-of-life criteria without compromising product protection.

The complementary dynamics of barrier performance, cost and policy shape converter investment decisions. Corrugated board plants are upgrading to die-cutters capable of making e-commerce shippers with crash-lock bottoms, serving both domestic SMEs and multinational fulfillment centers. Meanwhile, regional resin distributors are offering long-term supply contracts pegged to Brent crude in a bid to de-risk volatility for high-volume users. On the R&D front, academia-industry consortia in South Africa are testing sugarcane-based bio-PE films that can run on existing extrusion lines, aiming to localize feedstock and reinforce circularity narratives. These initiatives underscore an era of portfolio diversification that will gradually recalibrate material splits within the Africa packaging industry over the next five years.

The Africa Packaging Market Report is Segmented by Packaging Type (Plastic, Paper, Container Glass, Metal Cans), Packaging Format (Rigid, Flexible), End-Use Industry (Food, Beverage, Pharmaceuticals, Personal Care, Industrial, E-Commerce), and Geography (Egypt, Nigeria, Kenya, South Africa, Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amcor plc

- Mondi plc

- Nampak Ltd

- Mpact Ltd

- Tetra Pak International SA

- Sealed Air Corp.

- Constantia Flexibles Group GmbH

- Consol Holdings (Pty) Ltd

- Astrapak Ltd (RPC Packaging Holdings Ltd)

- Foster Packaging International (Pty) Ltd

- East African Packaging Industries Ltd

- Bonpak (Pty) Ltd

- Huhtamaki Oyj

- Ardagh Group SA

- Smurfit WestRock

- Novus Holdings Ltd

- Greif Inc.

- Sonoco Products Company

- Frigoglass SAIC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing urban middle class boosting FMCG consumption

- 4.2.2 E-commerce packaging demand surge

- 4.2.3 Expansion of modern retail chains across Africa

- 4.2.4 Government bans on single-use plastics driving alternative materials

- 4.2.5 Rise of cold-chain logistics for fresh produce exports

- 4.2.6 Automotive CKD imports requiring protective tertiary packaging

- 4.3 Market Restraints

- 4.3.1 Volatile polymer and paper pulp prices

- 4.3.2 Power - supply instability increasing plant OPEX

- 4.3.3 Port congestion delaying raw-material inflows

- 4.3.4 Inadequate recycling infrastructure limiting rPET uptake

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

- 4.8 The Impact of Macroeconomic Factors on the Market

- 4.9 Investment Analysis

- 4.10 Overview of the Global Packaging Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Packaging Type

- 5.1.1 Plastic Packaging

- 5.1.1.1 By Type

- 5.1.1.1.1 Rigid Plastic Packaging

- 5.1.1.1.1.1 By Material Type

- 5.1.1.1.1.1.1 Polyethylene (PE)

- 5.1.1.1.1.1.2 Polypropylene (PP)

- 5.1.1.1.1.1.3 Polyethylene Terephthalate (PET)

- 5.1.1.1.1.1.4 Polyvinyl Chloride (PVC)

- 5.1.1.1.1.1.5 Polystyrene (PS) and Expanded Polystyrene (EPS)

- 5.1.1.1.1.1.6 Other Material Types

- 5.1.1.1.1.2 By Product Type

- 5.1.1.1.1.2.1 Bottles and Jars

- 5.1.1.1.1.2.2 Caps and Closures

- 5.1.1.1.1.2.3 Trays and Containers

- 5.1.1.1.1.2.4 Other Product Types

- 5.1.1.1.1.3 By End-use Industry

- 5.1.1.1.1.3.1 Food

- 5.1.1.1.1.3.2 Beverage

- 5.1.1.1.1.3.3 Pharmaceutical

- 5.1.1.1.1.3.4 Cosmetics and Personal Care

- 5.1.1.1.1.3.5 Industrial

- 5.1.1.1.1.3.6 Other End-use Industry

- 5.1.1.1.1.1 By Material Type

- 5.1.1.1.2 Flexible Plastic Packaging

- 5.1.1.1.2.1 By Material Type

- 5.1.1.1.2.1.1 Polyethylene (PE)

- 5.1.1.1.2.1.2 Biaxially Oriented Polypropylene (BOPP)

- 5.1.1.1.2.1.3 Cast Polypropylene (CPP)

- 5.1.1.1.2.1.4 Other Material Types

- 5.1.1.1.2.2 By Product Type

- 5.1.1.1.2.2.1 Pouches and Bags

- 5.1.1.1.2.2.2 Films and Wraps

- 5.1.1.1.2.2.3 Other Product Types

- 5.1.1.1.2.3 By End-use Industry

- 5.1.1.1.2.3.1 Food

- 5.1.1.1.2.3.2 Beverage

- 5.1.1.1.2.3.3 Pharmaceutical

- 5.1.1.1.2.3.4 Cosmetics and Personal Care

- 5.1.1.1.2.3.5 Industrial

- 5.1.1.1.2.3.6 Other End-use Industry

- 5.1.1.1.2.1 By Material Type

- 5.1.1.1.1 Rigid Plastic Packaging

- 5.1.1.2 By Product Type

- 5.1.1.2.1 Bottles and Jars

- 5.1.1.2.2 Pouches and Bags

- 5.1.1.2.3 Bulk-Grade Products

- 5.1.1.2.4 Other Product Types

- 5.1.1.3 By End-use Industry

- 5.1.1.3.1 Food

- 5.1.1.3.2 Beverages

- 5.1.1.3.3 Cosmetics and Personal Care

- 5.1.1.3.4 Pharamceuticals

- 5.1.1.3.5 Industrial

- 5.1.1.3.6 Other End-use Industry

- 5.1.1.1 By Type

- 5.1.2 Paper Packaging

- 5.1.2.1 By Product Type

- 5.1.2.1.1 Folding Carton

- 5.1.2.1.2 Corrugated Boxes

- 5.1.2.1.3 Liquid Paperboard

- 5.1.2.1.4 Other Product Type

- 5.1.2.2 By End-use Industry

- 5.1.2.2.1 Food

- 5.1.2.2.2 Beverages

- 5.1.2.2.3 E-commerce

- 5.1.2.2.4 Other End-use Industry

- 5.1.2.1 By Product Type

- 5.1.3 Container Glass

- 5.1.3.1 By Color

- 5.1.3.1.1 Green

- 5.1.3.1.2 Amber

- 5.1.3.1.3 Flint

- 5.1.3.1.4 Other Colors

- 5.1.3.2 By End-use Industry

- 5.1.3.2.1 Food

- 5.1.3.2.2 Beverage

- 5.1.3.2.2.1 Alcoholic

- 5.1.3.2.2.2 Non-Alcoholic

- 5.1.3.2.3 Personal Care and Cosmetics

- 5.1.3.2.4 Pharmaceuticals (excluding Vials and Ampoules)

- 5.1.3.2.5 Perfumery

- 5.1.3.1 By Color

- 5.1.4 Metal Cans and Containers

- 5.1.4.1 By Material Type

- 5.1.4.1.1 Steel

- 5.1.4.1.2 Aluminum

- 5.1.4.2 By Product Type

- 5.1.4.2.1 Cans

- 5.1.4.2.2 Drums and Barrels

- 5.1.4.2.3 Caps and Closures

- 5.1.4.2.4 Other Product Type

- 5.1.4.3 By End-use Industry

- 5.1.4.3.1 Food

- 5.1.4.3.2 Beverage

- 5.1.4.3.3 Chemicals and Petroleum

- 5.1.4.3.4 Industrial

- 5.1.4.3.5 Paints and coatings

- 5.1.4.3.6 Other End-use Industry

- 5.1.4.1 By Material Type

- 5.1.1 Plastic Packaging

- 5.2 By Packaging Format

- 5.2.1 Rigid

- 5.2.2 Flexible

- 5.3 By End-Use Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceuticals and Healthcare

- 5.3.4 Personal Care and Cosmetics

- 5.3.5 Industrial

- 5.3.6 E-commerce

- 5.3.7 Other End-use Industry

- 5.4 By Country

- 5.4.1 Egypt

- 5.4.2 Nigeria

- 5.4.3 Kenya

- 5.4.4 South Africa

- 5.4.5 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Mondi plc

- 6.4.3 Nampak Ltd

- 6.4.4 Mpact Ltd

- 6.4.5 Tetra Pak International SA

- 6.4.6 Sealed Air Corp.

- 6.4.7 Constantia Flexibles Group GmbH

- 6.4.8 Consol Holdings (Pty) Ltd

- 6.4.9 Astrapak Ltd (RPC Packaging Holdings Ltd)

- 6.4.10 Foster Packaging International (Pty) Ltd

- 6.4.11 East African Packaging Industries Ltd

- 6.4.12 Bonpak (Pty) Ltd

- 6.4.13 Huhtamaki Oyj

- 6.4.14 Ardagh Group SA

- 6.4.15 Smurfit WestRock

- 6.4.16 Novus Holdings Ltd

- 6.4.17 Greif Inc.

- 6.4.18 Sonoco Products Company

- 6.4.19 Frigoglass SAIC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

感官包裝市場:依技術、材料、感測器類型、包裝形式和應用分類-2026-2032年全球市場預測

感官包裝市場:依技術、材料、感測器類型、包裝形式和應用分類-2026-2032年全球市場預測 2026年全球包裝與標籤服務市場報告氣泡膜市場:2026-2032年全球市場預測(依材料、厚度、應用、最終用戶及通路分類)復古包裝市場:按材料、類型、最終用途、印刷技術和通路-2026-2032年全球預測紙質復古包裝市場:依材料、包裝類型、銷售管道、最終用戶、應用程式分類,全球預測(2026-2032)多功能零件市場按產品類型、價格範圍、應用、垂直產業和分銷管道分類,全球預測(2026-2032年)紙塑包裝器材市場:依機器類型、材料、操作類型和應用分類,全球預測(2026-2032年)全球電子順磁共振波譜儀市場(按產品類型、頻率、工作模式、組件、應用和最終用戶分類)預測(2026-2032年)按包裝類型、材料、最終用途、分銷管道和應用分類的常溫紙盒市場—全球預測,2026-2032年

2026年全球包裝與標籤服務市場報告氣泡膜市場:2026-2032年全球市場預測(依材料、厚度、應用、最終用戶及通路分類)復古包裝市場:按材料、類型、最終用途、印刷技術和通路-2026-2032年全球預測紙質復古包裝市場:依材料、包裝類型、銷售管道、最終用戶、應用程式分類,全球預測(2026-2032)多功能零件市場按產品類型、價格範圍、應用、垂直產業和分銷管道分類,全球預測(2026-2032年)紙塑包裝器材市場:依機器類型、材料、操作類型和應用分類,全球預測(2026-2032年)全球電子順磁共振波譜儀市場(按產品類型、頻率、工作模式、組件、應用和最終用戶分類)預測(2026-2032年)按包裝類型、材料、最終用途、分銷管道和應用分類的常溫紙盒市場—全球預測,2026-2032年 新加坡包裝市場

新加坡包裝市場