|

市場調查報告書

商品編碼

1940683

證書頒發機構:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)Certificate Authority - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

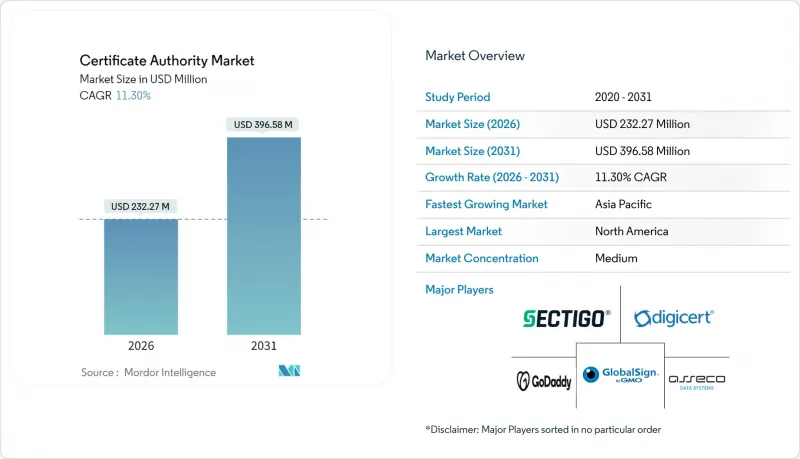

預計到 2026 年,憑證授權單位 (CA) 市場規模將達到 2.3227 億美元,高於 2025 年的 2.0868 億美元。

預計到 2031 年將達到 3.9658 億美元,2026 年至 2031 年的複合年成長率為 11.3%。

隨著企業從基於邊界的防禦轉向以身分為中心的模式(該模式依賴於對每次數位互動的加密檢驗),PKI 的採用速度加快。證書生命週期的縮短、向後量子加密技術的早期過渡以及零信任的快速普及,都增加了證書續訂量,並將自動化提升到了董事會層面的優先事項。瀏覽器廠商扮演著事實上的監管機構的角色,尤其是谷歌 Chrome 嚴格的根證書計劃執行,使得供應商的選擇不再僅僅基於價格,而是基於合規歷史。同時,雲端管理的 PKI 服務表明,外包專業知識能夠提供手動流程無法實現的速度和一致性。亞太地區電子商務的快速成長,加上政府對 PKI 的強制性要求,使得該地區的成長速度遠超更成熟的北美和歐洲市場。

全球證書頒發機構市場趨勢與洞察

嚴格的法規和合規義務

瀏覽器根憑證儲存區擁有者正在加強合規性,最顯著的例子是Chrome宣布將不再信任2024年10月之後頒發的Entrust憑證。因此,企業買家越來越重視證書頒發機構(CA)的紀律記錄以及其技術實力,這一趨勢正在持續重塑證書頒發機構市場。新的CA/瀏覽器論壇規則將TLS憑證的最大有效期縮短至47天(到2029年3月),這將增加續約量,並有利於具備即時自動化功能的供應商。託管PKI供應商已經開始強調獨立審核結果,以證明其合規性。同時,金融和醫療保健等受監管行業正在加快與一級CA的續訂,以避免未來失去信任帶來的聲譽風險。

擴展基於雲端的 PKI 服務

對於那些不想維護自有硬體安全模組 (HSM)、憑證撤銷清單 (CRL) 分發點和審核控制措施的組織而言,雲端服務已成為預設的起點。 DigiCert 於 2024 年 12 月將其旗艦平台上架 Microsoft Azure Marketplace,實現了點擊購買和付費使用制的擴展模式。例如,Paddy Power Betfair 在遷移到 HashiCorp Vault 即服務後,證書頒發前置作業時間從一周縮短至一小時。隨著市場朝向近乎持續續期模式發展(例如蘋果公司推廣 47 天有效期),這些效率優勢顯得格外重要。那些提供自動密鑰輪換、策略執行和即時吊銷功能的供應商,相比傳統的按數量計費的 SSL經銷商,已經獲得了明顯的定價優勢。

自簽名證書的普遍性

預算有限且擁有舊有應用程式的團隊仍然繼續部署自簽名證書,因為他們認為內部網路是可信的。然而,像戴爾的 eDellRoot 事件這樣備受矚目的事故凸顯了這些證書可能被利用進行中間人攻擊的風險。自簽章部署對小規模的IT 部門,尤其是在新興市場,仍然具有吸引力,因為它們可以避免使用憑證授權單位 (CA) 的費用。因此,商業 CA 提供捆綁式的發現和遷移工具包,幫助用戶了解隱藏的自簽名資產,並量化風險降低帶來的收益。

細分市場分析

到2025年,憑證類型將佔總收入的67.80%,這主要得益於瀏覽器在所有面向公眾的Web端點強制使用SSL/TLS協定所帶來的需求成長。然而,服務板塊將成為成長的真正驅動力,其複合年成長率將達到20.35%,因為企業越來越重視營運效率而非單一文件的購買。隨著蘋果47天證書有效期的臨近,手動續訂流程已難以為繼,促使企業轉向整合發現、策略執行和機器優先頒發引擎的託管式PKI訂閱服務。

服務供應商已證明其能夠將平均續約時間從幾天縮短至幾分鐘,同時也為監管機構提供審核追蹤。自動化還實現了大規模撤銷和關鍵證書洩露後的即時重新頒發。因此,分析師預測,到2030年,服務業的市場規模將超過證書類型產業,這標誌著證書頒發機構(CA)市場結構性轉變的開始。這一發展趨勢凸顯了CA產業如今為何在平台穩健性而非單張證書價格方面展開競爭。

到2025年,大型企業將佔總支出的63.70%,反映出複雜的多重雲端環境需要多層信任模式。隨著零信任計畫的擴展,預算持續成長,進一步擴大了憑證授權單位市場的絕對規模。然而,中小企業市場的成長速度更快,複合年成長率達到18.10%。雲端原生PKI解決方案透過訂閱模式提供企業級功能,無需硬體安全模組和公鑰專家。

預先整合的 ACME 連接器與 SaaS 計費系統結合,使Start-Ups能夠在註冊網域後幾分鐘內部署可信任證書。例如,在印度尼西亞,QRIS 數位支付框架利用標準化的 PKI 基礎架構,幫助小規模企業安全地開展線上業務。這些用例表明,即使在網路安全專業知識和預算有限的地區,經濟實惠且自動化的 PKI 也具有釋放數位商務潛力的巨大潛力。

憑證授權單位市場報告按以下因素細分:按元件(SSL/TLS 憑證、程式碼簽署憑證等)、組織規模(大型企業、中小企業)、最終用戶垂直行業(銀行、金融服務和保險、IT 和電信、零售和電子商務等)、憑證檢驗等級(網域檢驗、組織檢驗等)、部署模式(本地 PKI、雲端/託管 PKI)和地區。

區域分析

到2025年,北美將佔全球收入的35.20%,這主要得益於成熟的網路安全預算、積極的零信任部署計畫以及向3072位元RSA金鑰的早期過渡。諸如白宮第14028號行政命令等聯邦指令促使政府機構採用持續證書監控,從而擴大了合規工具證書頒發機構的市場規模。該地區的成長目前依賴於生命週期營運的自動化和後量子演算法先導計畫,DigiCert於2025年4月宣布推出Dilithium試點證書便印證了這一點。

亞太地區以16.55%的複合年成長率成為成長最快的地區,這主要得益於無現金支付的普及、數據本地化法律的實施以及印度、越南和印尼等國政府主導的公鑰基礎設施(PKI)部署。印度儲備銀行關於數位支付信任錨的指導方針鼓勵當地銀行對其證書工作流程進行現代化改造。國內雲端服務供應商與全球證書頒發機構(CA)合作,將承包頒發功能嵌入其電子商務平台,使數百萬中小企業無需內部專業知識即可實現合規。中國大力推動自主演算法研發,幫助區域供應商擴展了相容性範圍,從而實現了供應商多元化。

在歐洲,GDPR隱私法規的實施持續穩定地推進,要求資料處理者記錄其加密和金鑰管理實務。 eIDAS修正案進一步推動了對合格網站驗證證書(QVC)的需求,在更廣泛的證書頒發機構(CA)市場中開闢了一個高階細分領域。同時,中東和非洲市場隨著智慧城市和開放銀行計劃的推進,對TLS的採用率也在不斷提高,儘管基礎設施的差異在某些情況下延緩了大規模自動化證書頒發。南美洲的進展緩慢但穩健,政府入口網站現在要求使用TLS,而巴西的金融科技沙盒正在利用與ACME相容的證書頒發機構快速推出新服務。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 人們對安全網路存取的意識日益增強

- 嚴格的監管和合規要求

- 電子商務和線上交易的激增

- 基於雲端的PKI服務的成長

- DevSecOps主導的憑證自動化

- 零信任網路中對機器身分的需求

- 市場限制

- 新興中小企業缺乏安全證書意識

- 自簽名證書的普遍性

- 超大規模環境下的證書生命週期複雜性

- 關於後量子標準的監管不確定性

- 重要法規結構評估

- 價值鏈分析

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 關鍵相關人員影響評估

- 主要用例和案例研究

- 宏觀經濟因素對市場的影響

- 投資分析

第5章 市場區隔

- 按組件

- 證書類型

- SSL/TLS憑證

- 代碼簽署證書

- 安全電子郵件證書

- 身份驗證/客戶端憑證

- 服務

- 證書類型

- 按組織規模

- 主要企業

- 中小企業

- 按最終用戶行業分類

- BFSI

- 資訊科技和電信

- 零售與電子商務

- 醫療保健和生命科學

- 政府和公共部門

- 按證書檢驗級別

- 領域驗證(DV)

- 組織驗證(OV)

- 擴展檢驗(EV)

- 按部署模式

- 本地部署的PKI

- 雲端/託管 PKI

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- ASEAN

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DigiCert Inc.

- Sectigo Ltd.

- GoDaddy Group(Starfield Tech.)

- GlobalSign(KGZ)

- Entrust Corp.

- IdenTrust Services LLC

- Let's Encrypt/ISRG

- Actalis SpA

- SSL.com LLC

- Trustwave SecureTrust

- Network Solutions LLC

- WISeKey Intl. Holdings Ltd.

- SwissSign AG

- OneSpan Inc.

- Camerfirma SA

- Buypass AS

- QuoVadis Trustlink(Bermuda)Ltd.

- Certum(Asseco Data Systems SA)

- Amazon Trust Services

- Google Trust Services LLC

- Microsoft Azure TLS

- Oracle Cloud CA

- Cloudflare Inc.

- DigiSigner LLC

- HARICA(Hellenic Academic CA)

第7章 市場機會與未來展望

Certificate Authority market size in 2026 is estimated at USD 232.27 million, growing from 2025 value of USD 208.68 million with 2031 projections showing USD 396.58 million, growing at 11.3% CAGR over 2026-2031.

Adoption accelerated as organizations shifted from perimeter-based defenses to identity-centric models that rely on cryptographic validation for every digital interaction. Shorter certificate lifecycles, early moves toward post-quantum cryptography, and rapid zero-trust rollouts increased renewal volumes and elevated automation to a board-level priority. Browser vendors acting as de facto regulators, notably through Google Chrome's stricter root-program enforcement, reshaped supplier selection around compliance history rather than price. At the same time, cloud-managed PKI services demonstrated that outsourced expertise can deliver speed and consistency impossible to match with manual processes. Asia-Pacific's e-commerce boom, combined with government PKI mandates, placed the region on a markedly steeper growth curve than mature North American and European markets..

Global Certificate Authority Market Trends and Insights

Stringent Regulations and Compliance Mandates

Browser root-store owners enforced stricter compliance, best illustrated when Chrome announced distrust of Entrust certificates issued after October 2024. Enterprise buyers consequently evaluated CAs on their disciplinary record as much as on technical merit, a trend that continues to reshape the Certificate Authority Market. The forthcoming CA/Browser Forum rule that cuts TLS maximum validity to 47 days by March 2029 will magnify renewal volumes and favor providers equipped with real-time automation. Managed PKI vendors already highlight independent audit results to demonstrate readiness for this compliance wave. Meanwhile, regulated industries such as finance and healthcare accelerated contract renewals with Tier-1 CAs to avoid the reputational risk tied to potential future distrust events.

Expansion of Cloud-Based PKI Services

Cloud delivery became the default starting point for organizations unwilling to maintain hardware security modules, CRL distribution points, and audit controls in-house. DigiCert placed its flagship platform on Microsoft Azure Marketplace in December 2024, enabling click-through procurement and pay-as-you-go scaling. Case studies such as Paddy Power Betfair cut certificate issuance lead times from one week to one hour after migrating to HashiCorp Vault-as-a-Service. These gains matter even more as Apple's push for 47-day validity moves the market toward almost continuous renewal. Vendors differentiating on automated key-rotation, policy enforcement, and instant revocation earned clear pricing power over legacy, unit-based SSL sellers.

Prevalence of Self-Signed Certificates

Legacy applications and budget-constrained teams continued to deploy self-signed certificates, believing that interior networks remained trustworthy. High-profile failures, such as Dell's eDellRoot incident, illustrated how these certificates can be exploited for man-in-the-middle attacks. Because self-signed deployments avoid CA fees, they still appeal to small IT departments, especially in emerging markets. Commercial CAs, therefore, bundled discovery and migration toolkits to expose hidden self-signed assets and calculate risk savings in monetary terms.

Other drivers and restraints analyzed in the detailed report include:

- DevSecOps-Led Certificate Automation

- Machine-Identity Demand in Zero-Trust Networks

- Regulatory Uncertainty on Post-Quantum Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Certificate Types retained 67.80% of 2025 revenue, anchored by SSL/TLS demand that browsers enforce for every public web endpoint. However, Services generated the momentum, expanding at 20.35% CAGR as customers realized that operational excellence matters more than purchasing individual files. With Apple's 47-day validity on the horizon, manual renewal processes became untenable, pushing enterprises toward managed PKI subscriptions that bundle discovery, policy enforcement, and machine-first issuance engines.

Services providers showed they could shrink mean-time-to-renewal from days to minutes while supplying audit trails for regulators. Automation also enabled bulk revocation and immediate re-issuance during key-compromise events. As a result, analysts projected Services to surpass Certificate Types by value before 2030, marking a structural shift in the certificate authority market. This evolution underscores why the certificate authority industry now competes on platform robustness rather than on certificate unit price.

Large Enterprises generated 63.70% of total spending in 2025, reflecting complex multi-cloud estates that require layered trust models. Their budgets continued to climb as zero-trust initiatives expanded, reinforcing the certificate authority market size in absolute terms. Yet the SME segment exhibited the steeper trajectory at an 18.10% CAGR. Cloud-native PKI offerings delivered enterprise-grade functionality via subscription, removing the need for hardware security modules or public-key specialists.

SaaS invoicing and pre-integrated ACME connectors allowed start-ups to deploy trusted certificates within minutes of domain registration. In Indonesia, for example, QRIS digital payment frameworks used standardized PKI rails to bring micro-merchants online securely. These use cases validated the idea that affordable, automated PKI can unlock digital commerce in regions where cybersecurity expertise and budgets remain limited.

The Certificate Authority Market Report is Segmented by Component (SSL/TLS Certificates, Code-Signing Certificates, and More), Organization Size (Large Enterprises, and SMEs), End-User Vertical (BFSI, IT and Telecom, Retail and E-Commerce, and More), Certificate Validation Level (Domain Validation, Organization Validation, and More), Deployment Model (On-Premise PKI, and Cloud/Managed PKI), and Geography.

Geography Analysis

North America retained 35.20% of global revenue in 2025 on the back of mature cybersecurity budgets, aggressive zero-trust roadmaps, and early migration to 3072-bit RSA keys. Federal directives such as the White House Executive Order 14028 prompted agencies to adopt continuous certificate monitoring, reinforcing the certificate authority market size for compliance tooling. The region's growth now hinges on automating lifecycle tasks and pilot projects for post-quantum algorithms, evidenced by DigiCert's Dilithium test-certificates released in April 2025.

Asia-Pacific posted the swiftest CAGR at 16.55%, sparked by cashless-payment expansion, data-localization statutes, and government PKI rollouts in India, Vietnam, and Indonesia. The Reserve Bank of India's guidelines for digital-payment trust anchors spurred local banks to modernize certificate workflows. Domestic cloud providers partnered with global CAs to embed turnkey issuance into e-commerce platforms, allowing millions of SMEs to comply without in-house expertise. China's push for indigenous algorithms also encouraged regional vendors to expand compatibility matrices, broadening supplier variety.

Europe maintained steady momentum under GDPR's privacy regime, where data processors must document encryption and key-management practices. The eIDAS revision additionally drives demand for qualified website authentication certificates, creating a premium niche within the broader certificate authority market. Meanwhile, Middle East and Africa markets showed rising adoption tied to smart-city and open-banking projects, though uneven infrastructure sometimes slowed large-scale automated issuance. South America's trajectory remained moderate but positive; governments there increasingly required TLS on public-sector portals, while fintech sandboxes in Brazil leveraged ACME-compatible issuers to launch new services rapidly.

- DigiCert Inc.

- Sectigo Ltd.

- GoDaddy Group (Starfield Tech.)

- GlobalSign (KGZ)

- Entrust Corp.

- IdenTrust Services LLC

- Let's Encrypt / ISRG

- Actalis S.p.A

- SSL.com LLC

- Trustwave SecureTrust

- Network Solutions LLC

- WISeKey Intl. Holdings Ltd.

- SwissSign AG

- OneSpan Inc.

- Camerfirma SA

- Buypass AS

- QuoVadis Trustlink (Bermuda) Ltd.

- Certum (Asseco Data Systems SA)

- Amazon Trust Services

- Google Trust Services LLC

- Microsoft Azure TLS

- Oracle Cloud CA

- Cloudflare Inc.

- DigiSigner LLC

- HARICA (Hellenic Academic CA)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing awareness of secure web access

- 4.2.2 Stringent regulations and compliance mandates

- 4.2.3 Surge in e-commerce and online transactions

- 4.2.4 Expansion of cloud-based PKI services

- 4.2.5 DevSecOps-led certificate automation

- 4.2.6 Machine-identity demand in zero-trust networks

- 4.3 Market Restraints

- 4.3.1 Low security-certificate awareness in emerging SMBs

- 4.3.2 Prevalence of self-signed certificates

- 4.3.3 Certificate lifecycle complexity at hyperscale

- 4.3.4 Regulatory uncertainty on post-quantum standards

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact Assessment of Key Stakeholders

- 4.9 Key Use Cases and Case Studies

- 4.10 Impact on Macroeconomic Factors of the Market

- 4.11 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Component

- 5.1.1 Certificate Types

- 5.1.1.1 SSL/TLS Certificates

- 5.1.1.2 Code-Signing Certificates

- 5.1.1.3 Secure Email Certificates

- 5.1.1.4 Authentication/Client Certificates

- 5.1.2 Services

- 5.1.1 Certificate Types

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises (SMEs)

- 5.3 By End-user Vertical

- 5.3.1 BFSI

- 5.3.2 IT and Telecom

- 5.3.3 Retail and E-commerce

- 5.3.4 Healthcare and Life Sciences

- 5.3.5 Government and Public Sector

- 5.4 By Certificate Validation Level

- 5.4.1 Domain Validation (DV)

- 5.4.2 Organization Validation (OV)

- 5.4.3 Extended Validation (EV)

- 5.5 By Deployment Model

- 5.5.1 On-premise PKI

- 5.5.2 Cloud/Managed PKI

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Russia

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 ASEAN

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 DigiCert Inc.

- 6.4.2 Sectigo Ltd.

- 6.4.3 GoDaddy Group (Starfield Tech.)

- 6.4.4 GlobalSign (KGZ)

- 6.4.5 Entrust Corp.

- 6.4.6 IdenTrust Services LLC

- 6.4.7 Let's Encrypt / ISRG

- 6.4.8 Actalis S.p.A

- 6.4.9 SSL.com LLC

- 6.4.10 Trustwave SecureTrust

- 6.4.11 Network Solutions LLC

- 6.4.12 WISeKey Intl. Holdings Ltd.

- 6.4.13 SwissSign AG

- 6.4.14 OneSpan Inc.

- 6.4.15 Camerfirma SA

- 6.4.16 Buypass AS

- 6.4.17 QuoVadis Trustlink (Bermuda) Ltd.

- 6.4.18 Certum (Asseco Data Systems SA)

- 6.4.19 Amazon Trust Services

- 6.4.20 Google Trust Services LLC

- 6.4.21 Microsoft Azure TLS

- 6.4.22 Oracle Cloud CA

- 6.4.23 Cloudflare Inc.

- 6.4.24 DigiSigner LLC

- 6.4.25 HARICA (Hellenic Academic CA)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment