|

市場調查報告書

商品編碼

1940666

超高分子量聚乙烯(UHMWPE):市佔率分析、產業趨勢與統計、成長預測(2026-2031)Ultra-high Molecular Weight Polyethylene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

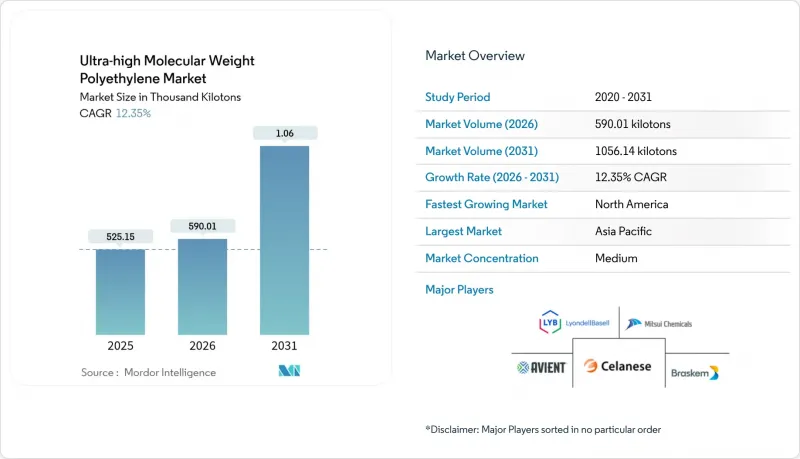

2025 年超高分子量聚乙烯 (UHMWPE) 市值為 525.15 千噸,預計到 2031 年將達到 1,056.14 千噸,高於 2026 年的 590.01 千噸。

預測期(2026-2031 年)的複合年成長率預計為 12.35%。

這種成長軌跡反映了其在電池隔膜、整形外科植入和海洋繩索等領域的廣泛應用,在這些領域,該樹脂的超長鏈結構、低摩擦係數和生物相容性至關重要。電氣化項目的擴展、關節重建手術的增加以及深海基礎設施的建設推動了市場需求。生產商在北美實現供應本地化,並在亞太地區擴張,縮短了前置作業時間,降低了物流風險,並為電池和醫療專用等級產品開闢了新的生產能力。永續性需求正促使供應商轉向生物基乙烯生產路線和低溫加工技術,這些技術在維持超高分子量特性的同時,也能降低能耗。

全球超高分子量聚乙烯(UHMWPE)市場趨勢及洞察

電動汽車電池中高性能聚合物的替代品

電動車電池製造商正擴大從傳統的聚烯隔膜轉向超高分子量聚乙烯(UHMWPE)隔膜。 UHMWPE隔膜在140°C以上的高溫下仍能維持尺寸穩定性,同時還能製造出更薄的薄膜,進而提高能量密度。 Braskem公司在德克薩斯州計劃5,000萬美元,獲得美國能源局(DOE)的支持,將新增2萬噸專用電池級UHMWPE隔膜產能,並創造250個技術職位,顯示UHMWPE市場與北美電氣化策略高度契合。採用纏結技術的隔膜生產線可將電解吸收率提高15%,並降低內阻,這對於長續航里程的電動車至關重要。

維生素E穩定超高分子量聚乙烯(UHMWPE)在關節重建手術的快速應用

維生素E穩定的超高分子量聚乙烯(UHMWPE)樹脂具有優異的氧化穩定性,與第一代交聯型樹脂相比,磨損產生的碎屑減少了42%。碎屑減少意味著植入使用壽命更長,因此,對於年輕一代的髖關節和膝關節關節重建手術而言,UHMWPE樹脂是首選材料。自2024年以來,FDA核准的含有此類樹脂的醫療設備穩定成長,增強了臨床信心,並鞏固了UHMWPE市場的長期成長。

與生物基替代品相比,加工能耗強度

傳統的齊格勒-納塔製程需要約250°C的反應器溫度和高壓擠出,這會增加範圍1的排放。布拉斯科公司以甘蔗為原料的乙烯生產路線可減少60%的碳足跡,但原料成本增加12%。歐盟買家越來越重視生物基原料,但生質能供應有限,使得規模化生產難以實現。

細分市場分析

到2025年,粉末將主導超高分子量聚乙烯(UHMWPE)市場,佔總市場佔有率的44.63%。 100µm至150µm之間的精細粒徑控制可確保用於溜槽襯裡和防彈板的壓模片材均勻燒結。到2031年,粉末的複合年成長率將達到12.62%,超過纖維和薄膜。這主要是由於電動車隔膜製造商對窄分子量分佈的需求,而目前只有粉末生產才能滿足這項需求。

該領域也受惠於觸媒技術的進步,該技術可在不增加黏度的情況下將分子量提升至1000萬g/mol,從而實現食品加工機械用棒材的高速擠壓成型。因此,對粉末生產能力的投資正在為更廣泛的超高分子量聚乙烯(UHMWPE)市場擴張奠定基礎。纖維是第二種產品形式,在船舶和國防領域的需求得到保障,而片材和薄膜則正在滲透到薄壁分離器市場。棒材和管材雖然屬於小眾市場,但對於使用壽命超過5萬小時的化學泵浦應用至關重要。

超高分子量聚乙烯 (UHMWPE) 報告按形態(粉末、纖維、片材/薄膜、棒材/管材等)、終端用戶產業(汽車、航太/國防、醫療、化學、電子等)和地區(亞太地區、北美、歐洲、南美、中東和非洲)進行細分。市場預測以千噸為單位。

區域分析

預計到2025年,亞太地區將以44.55%的市佔率引領超高分子量聚乙烯(UHMWPE)市場,這主要得益於該地區擁有完善的石化產業中心,能夠為下游纖維和薄膜工廠提供充足的原料。中國的「一帶一路」計劃正在推動新港口對輕質、耐腐蝕繩索的需求成長,而日本醫療設備供應商也已簽訂了長期粉末採購合約。此外,中日沿海地區離岸風力發電的快速發展也進一步增加了深水繫錨碇纜繩對纖維的需求。

預計北美將維持全球最快的成長速度,到2031年複合年成長率將達到12.97%。聯邦政府的激勵措施正在推動三座新的膜工廠的建設,這些工廠的核心是一條專門用於生產超高分子量聚乙烯(UHMWPE)的生產線,旨在降低供應風險。布拉斯科公司在德克薩斯州的擴張計畫獲得了美國能源局5000萬美元的津貼支持,這標誌著製造業回流的勢頭強勁,並凸顯了UHMWPE市場在電池價值鏈中的戰略價值。

在以永續性為導向的 PFAS 替代和積極的循環經濟目標的推動下,歐洲保持著溫和的個位數成長。德國的一個試點計畫展示了醫用襯墊的閉合迴路回收利用,推進了該地區的回收理念。南美洲和中東及非洲是新興但具有重要戰略意義的市場,巴西鹽鹽層下油田鑽井平台和沙烏地阿拉伯的石化多元化發展為超高分子量聚乙烯 (UHMWPE) 開闢了獨特的應用領域,並逐步提高了其在該地區市場的滲透率。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電動汽車電池中高性能聚合物的替代趨勢

- 快速採用維生素E高分子量聚乙烯進行關節重建手術(2025年及以後)

- 亞太地區對造船和船用繩索的需求快速成長

- 3D列印超高分子量聚乙烯整形外科植入

- 實現醫療級循環利用的回收途徑

- 市場限制

- 與生物基替代品相比,加工能耗強度

- 低熔點是承載複合材料的限制因素。

- 對亞洲粉末出口徵收貿易救濟稅

- 價值鏈分析

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按形式

- 粉末

- 纖維

- 片材和薄膜

- 桿和管

- 其他

- 按最終用戶行業分類

- 車

- 航太/國防

- 醫療保健

- 化學

- 電子設備

- 其他

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Asahi Kasei Corporation

- Avient Corporation

- Braskem

- Celanese Corporation

- dsm-firmenich

- DuPont

- Honeywell International Inc.

- Korea Petrochemical Ind. Co., LTD.

- LyondellBasell Industries Holdings BV

- Mitsui Chemicals Inc.

- Rochling SE & Co. KG

- Shandong Longforce Engineering Material Co., Ltd

- TEIJIN LIMITED

第7章 市場機會與未來展望

The Ultra-high Molecular Weight Polyethylene Market was valued at 525.15 kilotons in 2025 and estimated to grow from 590.01 kilotons in 2026 to reach 1056.14 kilotons by 2031, at a CAGR of 12.35% during the forecast period (2026-2031).

This trajectory reflects broad adoption in battery separators, orthopedic implants, and marine ropes, where the resin's distinct combination of very long chains, low friction, and biocompatibility is indispensable. Widening electrification programs, accelerated joint-replacement procedures, and deep-water infrastructure all reinforce demand. Producers' moves to localize supply in North America and expand in Asia-Pacific shorten lead-times, mitigate logistics risk, and unlock new capacity for grades tailored to battery and medical specifications. Sustainability mandates are pushing suppliers toward bio-based ethylene routes and lower-temperature processing technologies that cut energy intensity while preserving ultra-high molecular weight attributes.

Global Ultra-high Molecular Weight Polyethylene Market Trends and Insights

High-performance Polymer Substitution in EV Batteries

Electric-vehicle cell makers are switching from conventional polyolefins to UHMWPE separators because the latter remain dimensionally stable above 140 °C while allowing thinner films that raise energy density. Braskem's USD 50 million DOE-backed project in Texas will add 20 kilo tons of dedicated battery-grade capacity and create 250 skilled jobs, underscoring the Ultra-high Molecular Weight Polyethylene market's alignment with North American electrification policy. Separator lines adopting disentangled-chain technology improve electrolyte uptake by 15% and cut internal resistance, attributes critical for longer-range vehicles.

Rapid Adoption of Vitamin-E HXLPE in Joint Arthroplasty

Vitamin E-stabilized UHMWPE resins exhibit superior oxidative stability, reducing wear debris generation by 42% versus first-generation cross-linked grades. Lower debris translates into longer implant lifespans, a priority as younger patients undergo hip and knee replacements. FDA approvals for devices containing these resins have risen steadily since 2024, reinforcing clinical confidence and locking in long-term growth for the Ultra-high Molecular Weight Polyethylene market.

Processing Energy Intensity Vs. Bio-Based Alternatives

Traditional Ziegler-Natta pathways demand reactor temperatures near 250 °C and high-pressure extrusion, inflating Scope-1 emissions. Braskem's sugarcane-derived ethylene route offers a 60% lower carbon footprint but raises feedstock costs by 12%. EU buyers increasingly favor bio-attributed volumes, yet limited biomass availability restrains scale.

Other drivers and restraints analyzed in the detailed report include:

- Surge in APAC Shipbuilding and Offshore Ropes Demand

- 3-D Printed UHMWPE Orthopedic Implants

- Low Melting Point Limits High-Load Composites

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Powder accounted for 44.63% of the 2025 volume, making it the backbone of the Ultra-high Molecular Weight Polyethylene market. Tailored particle sizes between 100 µm and 150 µm ensure uniform sintering in compression-molded sheets used for chute liners and ballistic plates. Powder's 12.62% CAGR to 2031 outpaces fiber and film because EV separator producers prefer a tight molecular weight distribution that only powder routes currently guarantee.

The segment also benefits from catalyst advances that push molecular weight to 10 million g/mol without raising viscosity, enabling higher-speed ram-extrusion of rods for food-processing machinery. Investments in powder capacity, therefore, underpin broader Ultra-high Molecular Weight Polyethylene market expansion. Fibers, the second-largest form, secure marine and defense demand, while sheets and films penetrate thin-wall separators. Rods and tubes remain niche but critical for chemical pumps where wear life eclipses 50,000 hours.

The Ultra-High Molecular Weight Polyethylene Report is Segmented by Form (Powder, Fibers, Sheets and Films, Rods and Tubes, and Others), End-User Industry (Automotive, Aerospace and Defense, Medical, Chemical, Electronics, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Kilo Tons).

Geography Analysis

Asia-Pacific dominated the Ultra-high Molecular Weight Polyethylene market with a 44.55% share in 2025, leveraging integrated petrochemical hubs that feed downstream fiber and film plants. China's Belt and Road projects intensify demand for lightweight, corrosion-proof ropes in new ports, while Japan's medical-device suppliers secure long-term powder contracts. Regional offshore wind build-out along Chinese and Japanese coasts further multiplies fiber consumption for deep-water mooring lines.

North America is on track for a 12.97% CAGR up to 2031, the fastest globally. Federal incentives are catalyzing three new separator-film plants, each structured around captive UHMWPE lines to de-risk supply. Braskem's Texas expansion, supported by a USD 50 million DOE grant, illustrates domestic re-shoring momentum and underscores the Ultra-high Molecular Weight Polyethylene market's strategic value in battery supply chains.

Europe maintains mid-single-digit growth through sustainability-driven substitution of PFAS and aggressive circular-economy goals. Pilots in Germany demonstrate closed-loop reclaim of medical liners, aligning with the continent's recycling ethos. South America and MEA remain emerging but strategically significant, with Brazil's pre-salt rigs and Saudi petrochemical diversification opening localized applications that will gradually raise regional Ultra-high Molecular Weight Polyethylene market penetration.

- Asahi Kasei Corporation

- Avient Corporation

- Braskem

- Celanese Corporation

- dsm-firmenich

- DuPont

- Honeywell International Inc.

- Korea Petrochemical Ind. Co., LTD.

- LyondellBasell Industries Holdings B.V.

- Mitsui Chemicals Inc.

- Rochling SE & Co. KG

- Shandong Longforce Engineering Material Co., Ltd

- TEIJIN LIMITED

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High?Performance Polymer Substitution in EV Batteries

- 4.2.2 Rapid Adoption of Vitamin E HXLPE In Joint Arthroplasty (Post-2025)

- 4.2.3 Surge in APAC Shipbuilding and Offshore Ropes Demand

- 4.2.4 3-D Printed UHMWPE Orthopedic Implants

- 4.2.5 Recycling Routes Enabling Medical-Grade Circularity

- 4.3 Market Restraints

- 4.3.1 Processing Energy Intensity Vs. Bio-Based Alternatives

- 4.3.2 Low Melting Point Limits High-Load Composites

- 4.3.3 Trade-Remedy Duties on Asian Powder Exports

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Form

- 5.1.1 Powder

- 5.1.2 Fibers

- 5.1.3 Sheets and Films

- 5.1.4 Rods and Tubes

- 5.1.5 Others

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.2 Aerospace and Defense

- 5.2.3 Medical

- 5.2.4 Chemical

- 5.2.5 Electronics

- 5.2.6 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Asahi Kasei Corporation

- 6.4.2 Avient Corporation

- 6.4.3 Braskem

- 6.4.4 Celanese Corporation

- 6.4.5 dsm-firmenich

- 6.4.6 DuPont

- 6.4.7 Honeywell International Inc.

- 6.4.8 Korea Petrochemical Ind. Co., LTD.

- 6.4.9 LyondellBasell Industries Holdings B.V.

- 6.4.10 Mitsui Chemicals Inc.

- 6.4.11 Rochling SE & Co. KG

- 6.4.12 Shandong Longforce Engineering Material Co., Ltd

- 6.4.13 TEIJIN LIMITED

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

超高分子量聚乙烯市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場進行預測。

超高分子量聚乙烯市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場進行預測。 超高分子量聚乙烯市場:依產品、等級、製程、功能、終端用戶產業及通路分類-2026-2032年全球市場預測全球抗靜電超高分子量聚乙烯(UHMWPE)板材市場:按類型、厚度範圍、抗靜電等級、應用和終端用戶產業分類,2026-2032年預測

超高分子量聚乙烯市場:依產品、等級、製程、功能、終端用戶產業及通路分類-2026-2032年全球市場預測全球抗靜電超高分子量聚乙烯(UHMWPE)板材市場:按類型、厚度範圍、抗靜電等級、應用和終端用戶產業分類,2026-2032年預測 超高分子量聚乙烯市場規模、佔有率及成長分析(按類型、應用、終端用戶產業及地區分類)-2026-2033年產業預測

超高分子量聚乙烯市場規模、佔有率及成長分析(按類型、應用、終端用戶產業及地區分類)-2026-2033年產業預測 醫用超高分子量聚乙烯:全球市佔率及排名、總收入及需求預測(2025-2031年)

醫用超高分子量聚乙烯:全球市佔率及排名、總收入及需求預測(2025-2031年) 超高分子量聚乙烯 (UHMWPE) 市場預測(至 2032 年):以基礎材料、形式、等級、最終用戶和地區進行的全球分析

超高分子量聚乙烯 (UHMWPE) 市場預測(至 2032 年):以基礎材料、形式、等級、最終用戶和地區進行的全球分析 全球醫用超高分子量聚乙烯單體市場全球超高分子量(UHMW)聚乙烯市場

全球醫用超高分子量聚乙烯單體市場全球超高分子量(UHMW)聚乙烯市場 全球醫用超高分子量聚乙烯市場規模(依產品類型、應用、最終用戶、區域範圍、預測)

全球醫用超高分子量聚乙烯市場規模(依產品類型、應用、最終用戶、區域範圍、預測) 超高分子量聚乙烯板材市場報告:趨勢、預測和競爭分析(至 2031 年)

超高分子量聚乙烯板材市場報告:趨勢、預測和競爭分析(至 2031 年)