|

市場調查報告書

商品編碼

1940640

3D列印耗材:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)3D Printing Filament - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

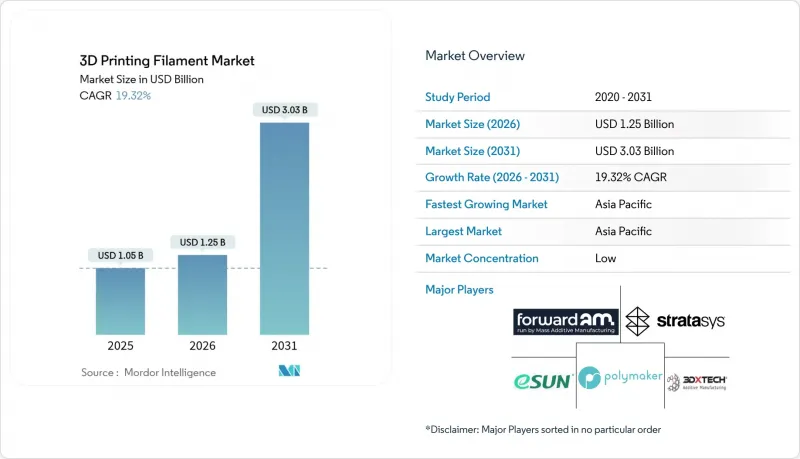

預計到 2025 年,3D 列印耗材市場價值將達到 10.5 億美元,從 2026 年的 12.5 億美元成長到 2031 年的 30.3 億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 19.32%。

桌上型印表機價格的下降,加上材料科學的穩定發展,正推動積層製造技術在航太、醫療和消費品等產業從原型製作階段走向大規模生產階段。中型製造商擴大採用熔融沈積成型 (FDM) 生產線生產終端零件,其性能可與射出成型相媲美,但模具成本更低。塑膠仍然是主要材料,種類繁多,從生物基 PLA 到工程級 PEEK,幾乎可以針對所有應用場景最佳化成本和性能。從區域來看,亞太地區在產量方面主導,這得益於其整合了印表機組裝和線材混合的緊密供應鏈。同時,北美和歐洲則專注於符合嚴格法規結構的認證高性能配方。

全球3D列印耗材市場趨勢及洞察

將積層製造從原型製作轉向大規模生產

隨著航太和汽車製造商對用於座艙零件、引擎室支架和夾具的FDM(熔融沈積成型)零件進行認證,市場需求正轉向經過認證的工程熱塑性塑膠。大型製造商通常會在零件從設計實驗室進入生產車間的過程中,將其線材採購量增加兩倍。市場正在向那些能夠保證批次間尺寸精度在±1%以內的公司擴展。採購部門現在優先考慮那些在聚合控制和ISO 13485及AS9100品管系統方面擁有成熟投資的成熟聚合物供應商,材料品質保證的重要性日益超過價格競爭力。

消費品和醫療保健領域大規模客製化的經濟學

醫院擴大採用3D列印技術製作患者客製化的鑽孔導板和顱骨板,從而將手術時間縮短多達45分鐘。高昂的材料成本很容易被抵銷。義肢製造商報告稱,在改用經認證的PEEK(聚醚醚酮)或PEKK(聚醚酮酮)長絲後,與機械加工相比,單位成本降低了40-60%。消費品牌也採用類似的小批量生產模式來製造個人化耳機和鞋墊。透過用材料溢價換取模具投資,他們得以維持毛利率。單一產品生產量固有的波動性進一步推動了靈活的積層製造工作流程,從而為能夠維持材料機械性能(無論顏料或批量大小)的專業混料商創造了穩定的需求。

工業印表機和後處理需要高額資本投入。

高溫聚合物的加工需要封閉式成型腔和在線連續退火工藝,系統價格超過10萬美元。中小企業的預算限制減緩了高階長絲的普及,並限制了短期內的需求成長。北美以外地區設備租賃市場的不成熟,使得許多新興市場製造商無法進入高性能材料生態系統。供應商正透過瞄準能夠快速攤銷資本的一級航太和醫療客戶來彌補銷售量成長的緩慢。

細分市場分析

2025年,塑膠在3D列印耗材市場佔據71.90%的佔有率,預計到2031年將以21.05%的複合年成長率成長。成長主要集中在特種尼龍、碳纖維增強PETG和PEKK等等級的材料上,這些材料的模量接近鋁,且可在性能更優的桌面級3D列印系統上進行列印。雖然PLA和ABS等通用材料仍供應教育機構和消費性電子產品,但工程熱塑性塑膠目前已佔據3D列印耗材市場塑膠收入的大部分。製造商正利用高通量雙螺桿擠出機,將碳纖維、芳香聚醯胺或陶瓷填料融入材料中,以提高拉伸強度,同時避免噴嘴磨損超過硬化鋼噴嘴的磨損程度。擁有閉合迴路參數資料庫的材料供應商正在提高首次列印成功率,減少廢棄物,並為汽車和模具用戶提供極具吸引力的單件成本優勢。

金屬絲材市場屬於小眾市場,僅佔3D列印耗材市場總量的不到5%,但不鏽鋼和鈦合金絲材對於輕型航太支架和需要燒結後高密度化的醫療植入至關重要。陶瓷填充樹脂適用於高溫感測器和介電絕緣體,但由於需要多次脫脂循環,其生產效率受到限制。提供脫脂爐和燒結製程參數與粉末填充絲材技術捆綁銷售的供應商,簡化了從粉末層熔融技術過渡到3D列印的實驗室的流程。這種整合方案除了材料利潤外,還能帶來業務收益。

區域分析

亞太地區預計2025年將貢獻39.05%的收入,主要得益於深圳、蘇州和首爾等地印表機和耗材產業叢集的協同發展。當地化學巨頭大規模供應ABS、PLA和PETG等原料,而代工生產商則負責混合工程配方以出口。政府的經濟刺激措施推動了專業積層製造產業園區的發展,降低了新參與企業的資金籌措成本,並促進了印表機硬體的創新。國內桌上型印表機領導者正在將專有材料設定檔預先載入到切片軟體中,從而強化了支撐耗材消費的品牌生態系統。

北美市場專注於那些認證和可追溯性至關重要的應用領域。美國在醫用級PEEK和碳纖維增強PEKK的銷售中佔據主導地位,這得益於供應商在FDA主文件提交和AS9100品質系統方面的大量投資。出於安全考慮,國防相關企業優先選擇國內採購,這進一步保障了高階長絲的利潤空間。此外,隨著汽車製造商為遵守《通貨膨脹與復甦法案》(IRA)的激勵措施而縮短供應鏈,生產回流趨勢也推動了需求成長。

在歐洲,環境保護是重中之重,迫使終端用戶選擇符合REACH和RoHS法規的生物基或再生材料。德國汽車製造商指定使用25%玻璃纖維增強的再生PET作為內飾支架材料,而法國消費品製造商正在試點使用甘蔗基PLA混合物,以滿足企業排放目標。歐盟對生命週期評估(LCA)審核和材料創新的補貼,使本地供應商在研發方面擁有優勢。因此,歐洲3D列印耗材市場向中高階市場傾斜,兼顧了永續性和高效能。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 將積層製造從原型製作轉向大量生產

- 消費品和醫療保健領域大規模客製化的經濟學

- 桌上型印表機價格的快速下降正在擴大業餘愛好者市場。

- 推動永續性,採用生物基/再生PET和PLA長絲

- 人工智慧最佳化PEEK/PEKK航太零件的高速列印

- 市場限制

- 工業印表機和後處理的高額資本投入

- 通用PLA和ABS的機械和熱學局限性

- 氣候變遷影響玉米供應,導致PLA原料價格波動。

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按類型

- 金屬

- 鈦

- 不銹鋼

- 其他金屬

- 塑膠

- 聚對苯二甲酸乙二醇酯(PET)

- 聚乳酸(PLA)

- 丙烯腈丁二烯苯乙烯(ABS)

- 尼龍

- 其他塑膠

- 陶瓷

- 其他類型

- 金屬

- 透過使用

- 航太/國防

- 車

- 醫療和牙科

- 電子學

- 其他用途

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 馬來西亞

- 泰國

- 越南

- 印尼

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 土耳其

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 南非

- 奈及利亞

- 埃及

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- 3DXTECH

- Amolen

- BASF

- Braskem

- Covestro AG

- Evonik Industries AG

- Fillamentum

- Forward AM

- Village Plastics

- Markforged

- Mitsubishi Chemical Group

- NatureWorks LLC

- Polymaker

- SABIC

- Shenzhen Esun Industrial Co., Ltd.

- Solvay

- Stratasys

第7章 市場機會與未來展望

The 3D Printing Filament Market was valued at USD 1.05 billion in 2025 and estimated to grow from USD 1.25 billion in 2026 to reach USD 3.03 billion by 2031, at a CAGR of 19.32% during the forecast period (2026-2031).

Rising desktop-printer affordability, coupled with steady material-science advances, continues to pull additive manufacturing from prototyping toward scaled production settings across aerospace, healthcare, and consumer products. Momentum builds as mid-sized manufacturers deploy fused-deposition modeling (FDM) lines for end-use parts that match injection-molded performance while removing tooling costs. Plastics remain the dominant material family because suppliers now offer grades ranging from bio-based PLA to engineering-level PEEK, enabling cost-to-performance matching for virtually every use case. Regionally, Asia-Pacific commands volume leadership, supported by cohesive supply chains that integrate printer assembly with filament compounding, while North America and Europe concentrate on certified, high-performance formulations that meet stringent regulatory frameworks.

Global 3D Printing Filament Market Trends and Insights

Additive Manufacturing Shift from Prototyping to Serial Production

Demand is migrating toward certified engineering thermoplastics as aerospace and automotive producers qualify FDM (Fused Deposition Modeling) parts for cabin components, under-hood brackets, and jigs. Large manufacturers typically triple filament purchases once a part moves from design lab to production floor. Batch traceability and statistical process control have become baseline supplier requirements, opening space for companies that can guarantee +-1 % dimensional consistency lot-to-lot. Procurement teams now prioritize legacy polymer suppliers that invested in polymerization control and ISO 13485 or AS9100 quality management, underlining how material assurance eclipses price sensitivity.

Mass-customisation Economics in Consumer and Medical Sectors

Hospitals increasingly print patient-specific drill guides and cranial plates, cutting operating-room time by up to 45 minutes and absorbing premium material costs with ease. Prosthetic manufacturers report 40-60 % unit savings versus subtractive machining after switching to certified PEEK (Polyetheretherketone) or PEKK (Polyetherketoneketone) filaments. Consumer brands adopt the same small-lot logic for personalized earbuds and footwear midsoles, trading tooling investments for material premiums that leave gross margins intact. Volume volatility inherent in individualized production further incentivizes flexible additive workflows, pushing steady demand to specialized compounders that can hold mechanical properties across pigments and lot sizes.

High Cap-ex for Industrial Printers and Post-processing

Processing high-temperature polymers requires enclosed build chambers and in-line annealing that push system prices beyond USD 100,000. Budget constraints among small and mid-size enterprises delay adoption, limiting near-term pull-through for premium filaments. Equipment leasing is nascent outside North America, leaving many emerging-market manufacturers locked out of high-performance material ecosystems. Suppliers offset sluggish volume growth by targeting Tier 1 aerospace and medical customers able to amortize capital quickly.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Desktop-printer Price Erosion Expanding Hobbyist Base

- Sustainability Push for Bio-based/recycled PET and PLA Filaments

- Mechanical/thermal Limits of Commodity PLA and ABS

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastics held 71.90 % of 3D Printing Filament market share in 2025 and are projected to deliver a 21.05 % CAGR to 2031. Growth concentrates in specialty nylons, carbon-fiber reinforced PETG, and PEKK grades that approach aluminum's modulus yet print on modified desktop systems. Commodity PLA and ABS continue to supply classroom and consumer gadgets, but engineering thermoplastics now command over half of plastics revenue inside the 3D printing filament market. Manufacturers leverage high-throughput twin-screw extrusion to blend carbon fibers, aramid, or ceramic fillers that raise tensile strength without introducing abrasive wear beyond hardened-steel nozzles. Material suppliers with closed-loop parameter databases improve first-time print success, trimming scrap and validating cost-per-part economics attractive to automotive and tooling users.

Metal filaments remain a niche at less than 5 % of 3D Printing Filament market size, yet stainless-steel and titanium blends are indispensable for lightweight aerospace brackets and medical implants requiring high-density after sintering. Ceramic-loaded resins address high-temperature sensors and dielectric insulators but face throughput bottlenecks due to multiple debind cycles. Vendors that bundle de-binder ovens and sintering profiles along with powder-in-filament technology simplify adoption for labs migrating from powder-bed fusion. Their integrated approach generates service revenue streams in addition to material margins.

The 3D Printing Filament Market Report is Segmented by Type (Metals, Plastics, Ceramics, and Other Types), Application (Aerospace and Defense, Automotive, Medical and Dental, Electronics, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

The Asia-Pacific region generated 39.05 % of revenue in 2025, underpinned by synergistic printer-and-filament clusters in Shenzhen, Suzhou, and Seoul. Local chemical giants supply ABS, PLA, and PETG feedstocks at scale, while contract compounding houses blend engineering formulations for export. Government stimulus packages fund additive-focused industrial parks, which lower financing costs for new entrants and stimulate printer hardware innovation. Domestic desktop-printer leaders preload slicer software with proprietary material profiles, reinforcing brand ecosystems that keep filament consumption sticky.

North America emphasizes applications where certification and traceability are mandatory. The United States dominates sales of medical-grade PEEK and carbon-fiber PEKK because suppliers have invested heavily in FDA master-file submissions and AS9100 quality systems. Defense contractors favor domestic procurement for security reasons, which further insulates high-end filament margins. Demand growth also benefits from the onshoring trend as automakers shorten supply chains to meet Inflation Reduction Act incentives.

Europe champions environmental stewardship, compelling end users to select bio-based or recycled grades that meet REACH and RoHS compliance. German automotive firms specify recycled PET with 25 % glass fibers for interior brackets, while French consumer-goods makers pilot sugarcane-derived PLA blends to hit corporate emissions goals. EU grants subsidize LCA audits and material innovation, giving local suppliers an R&D edge. The 3D printing filament market size in Europe thus skews toward mid-to-premium segments where sustainability and performance blend.

- 3DXTECH

- Amolen

- BASF

- Braskem

- Covestro AG

- Evonik Industries AG

- Fillamentum

- Forward AM

- Village Plastics

- Markforged

- Mitsubishi Chemical Group

- NatureWorks LLC

- Polymaker

- SABIC

- Shenzhen Esun Industrial Co., Ltd.

- Solvay

- Stratasys

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Additive Manufacturing Shift from Prototyping to Serial Production

- 4.2.2 Mass-customisation Economics in Consumer and Medical Sectors

- 4.2.3 Rapid Desktop-printer Price Erosion Expanding Hobbyist Base

- 4.2.4 Sustainability Push for Bio-based/recycled PET and PLA Filaments

- 4.2.5 AI-optimised High-speed Printing of PEEK/PEKK Aerospace Parts

- 4.3 Market Restraints

- 4.3.1 High Cap-ex for Industrial Printers and Post-processing

- 4.3.2 Mechanical/thermal Limits of Commodity PLA and ABS

- 4.3.3 PLA feed-stock Price Swings Linked to Climate-hit Corn Supply

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Metals

- 5.1.1.1 Titanium

- 5.1.1.2 Stainless Steel

- 5.1.1.3 Other Metals

- 5.1.2 Plastics

- 5.1.2.1 Polyethylene Terephthalate (PET)

- 5.1.2.2 Polylactic Acid (PLA)

- 5.1.2.3 Acrylonitrile Butadiene Styrene (ABS)

- 5.1.2.4 Nylon

- 5.1.2.5 Other Plastics

- 5.1.3 Ceramics

- 5.1.4 Other Types

- 5.1.1 Metals

- 5.2 By Application

- 5.2.1 Aerospace and Defense

- 5.2.2 Automotive

- 5.2.3 Medical and Dental

- 5.2.4 Electronics

- 5.2.5 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Australia

- 5.3.1.6 Malaysia

- 5.3.1.7 Thailand

- 5.3.1.8 Vietnam

- 5.3.1.9 Indonesia

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Nordics

- 5.3.3.8 Turkey

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 South Africa

- 5.3.5.5 Nigeria

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3DXTECH

- 6.4.2 Amolen

- 6.4.3 BASF

- 6.4.4 Braskem

- 6.4.5 Covestro AG

- 6.4.6 Evonik Industries AG

- 6.4.7 Fillamentum

- 6.4.8 Forward AM

- 6.4.9 Village Plastics

- 6.4.10 Markforged

- 6.4.11 Mitsubishi Chemical Group

- 6.4.12 NatureWorks LLC

- 6.4.13 Polymaker

- 6.4.14 SABIC

- 6.4.15 Shenzhen Esun Industrial Co., Ltd.

- 6.4.16 Solvay

- 6.4.17 Stratasys

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

基於TPU長絲的3D列印市場規模、佔有率和成長分析:按類型、製造方法、應用、終端用戶產業、通路和地區分類-產業預測(2026-2033年)

基於TPU長絲的3D列印市場規模、佔有率和成長分析:按類型、製造方法、應用、終端用戶產業、通路和地區分類-產業預測(2026-2033年) 3D列印線材生產線市場按材料類型、直徑、應用和最終用途產業分類-2026-2032年全球預測軟性3D列印耗材市場:依材料類型、顏色及最終用途產業分類-2026-2032年全球預測

3D列印線材生產線市場按材料類型、直徑、應用和最終用途產業分類-2026-2032年全球預測軟性3D列印耗材市場:依材料類型、顏色及最終用途產業分類-2026-2032年全球預測 可回收3D列印耗材市場規模、佔有率及趨勢分析報告:依產品、應用、地區及細分市場預測(2025-2033年)

可回收3D列印耗材市場規模、佔有率及趨勢分析報告:依產品、應用、地區及細分市場預測(2025-2033年) 3D列印耗材市場-2025-2030年預測3D列印耗材市場:依材料類型、技術、終端用戶產業、應用及通路分類-2025-2032年全球預測

3D列印耗材市場-2025-2030年預測3D列印耗材市場:依材料類型、技術、終端用戶產業、應用及通路分類-2025-2032年全球預測 3D列印長絲市場:按類型、材料類型、應用和地區

3D列印長絲市場:按類型、材料類型、應用和地區 PVA 3D列印線材市場報告:至2031年的趨勢、預測與競爭分析

PVA 3D列印線材市場報告:至2031年的趨勢、預測與競爭分析 全球 3D 列印長絲市場(按類型、最終用途產業和地區分類)- 預測至 2030 年

全球 3D 列印長絲市場(按類型、最終用途產業和地區分類)- 預測至 2030 年 可回收 3D 列印長絲市場分析及預測至 2033 年:按類型、產品、服務、技術、應用、材料類型、製程、最終用戶、安裝類型和解決方案

可回收 3D 列印長絲市場分析及預測至 2033 年:按類型、產品、服務、技術、應用、材料類型、製程、最終用戶、安裝類型和解決方案