|

市場調查報告書

商品編碼

1940637

覆層:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Cladding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

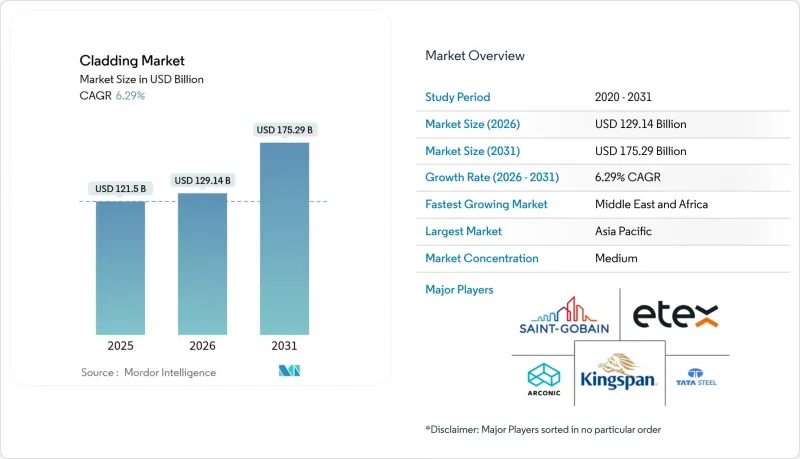

據估計,到 2026 年,覆層市場價值將達到 1,291.4 億美元,高於 2025 年的 1,215 億美元,預計到 2031 年將達到 1,752.9 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 6.29%。

這一上升趨勢是由更嚴格的能源效率法規、強制性建築幕牆防火測試以及都市區熱島效應緩解計劃共同推動的,這些因素正在重塑材料規格和採購慣例。新建設和快速成長的維修週期之間的需求保持平衡,這就要求老舊的建築幕牆滿足規範要求的防火性能、降低營運碳排放並提高隔熱性能。主要製造商的垂直整合以及金屬和礦物板材生產的日益本地化增強了供應側的韌性,從而保護計劃免受關稅波動導致的價格波動影響。持續的數位化,特別是利用數位雙胞胎進行資產監控,正在降低生命週期成本,並影響競標決策,使其傾向於能夠即時記錄性能的系統。外部風險仍然存在:鋁價波動正在擠壓EPC(工程、採購和施工)利潤空間,技術純熟勞工短缺正在延長工期,而不斷變化的消防安全標準可能迫使人口密集的城市中心進行超出預算的建築幕牆更換。

全球覆層市場趨勢與洞察

收緊淨零能耗建築標準

2024 年國際能源效率標準將引入高性能建築圍護結構的閾值,而加州 2025 年的標準將要求採用與熱泵相容的圍護結構和先進的熱工設計。參考這些標準的州和地方擴展標準將要求新計畫採用高效能(高 R 值)和隔熱的外牆組件。商業地產業主正在優先考慮整合式建築幕牆系統,以控制營運成本並從綠色租賃中獲得溢價。建築覆材市場正受益於建築材料選擇標準從成本轉向性能的轉變。

高層維修中外牆的強制性耐火性能測試

格倫費爾大廈火災後的改革促使不燃性要求被納入2024年國際建築規範及相應的國家標準。高層建築業主現在會在外牆維修前委託進行NFPA 285測試或同等評估,從而加速以礦物纖維或固體鋁材解決方案取代可燃性鋁複合材料系統。能夠提供合規組件認證的供應商在競標週期中獲得了更快的響應速度,這進一步推動了建築外牆市場向金屬和岩絨芯材傾斜。

鋁價波動對EPC利潤率帶來壓力

美國2025年生效的關稅政策導致美國中西部地區鋁材溢價飆升,使得幕牆和雨幕工程的競標定價更加複雜。承包商試圖透過避險和價格上漲條款來規避風險,但競標規則通常會限制成本轉嫁的幅度,從而降低利潤率並延誤計劃啟動。

細分市場分析

金屬板材將成為最大的收入來源,到2025年將佔據建築覆材市場30.54%的佔有率,這主要得益於高層建築對不可燃覆材的監管要求。木質覆材在2031年之前將以6.50%的複合年成長率成長,這主要得益於排碳權計劃和防火處理技術的進步,目前已被應用於多個淨零能耗學校建築和公共計劃中。陶瓷雨幕因其色牢度和抗凍融性能,仍然是高階商業建築幕牆的關鍵產品。石材裝飾層板的銷售量正在成長,這主要得益於旨在提高外牆隔熱性能(R值)並同時保留建築風格的維修項目。

「其他」類別(石灰外牆、玻璃、纖維水泥、乙烯基)的需求與區域建築規範趨勢密切相關。纖維水泥板在計劃和大型多用戶住宅中得到越來越廣泛的應用,這得益於聯邦政府「建設美國」計劃推動的1.5億美元國內產能擴張。智慧玻璃建築幕牆也日益普及,其動態遮陽功能有助於滿足冷凍負載預算要求。隨著建築規範更加重視性能而非材料成本,能夠認證低碳足跡以及整合防火隔熱性能的供應商將更有利於在建築外牆市場佔據市場佔有率。

區域分析

到2025年,亞太地區將佔全球收入的36.48%。儘管住宅速度放緩,中國的城市改造資金支持計畫仍在繼續推進建築幕牆翻新項目。地方政府正在二線城市推廣使用反射性屋頂膜,以降低夏季用電高峰。印度的國家基礎設施走廊計畫正在推動倉庫和物流園區對防火金屬板的需求。材料成本的上漲被建築融資的增加所抵銷。日本較低的成本環境使得小規模飯店計劃能夠採用薄壁陶瓷雨幕來應對地震位移。包括印尼努沙登加拉首都城市規劃在內的區域永續性憲章,正在總體規劃層面納入低碳建築幕牆目標,從而加強對建築外觀市場的長期承諾。

預計中東和非洲地區將經歷最高的成長率,到2031年複合年成長率將達到6.58%。沙烏地阿拉伯的「2030願景」計畫已宣佈建設項目總額超過1.1兆美元,該計畫明確規定使用能夠在極端熱循環條件下保持性能的不可燃建築幕牆系統。阿拉伯聯合大公國的資料中心建設正以每年36%的速度成長,需要使用高隔熱性能的夾芯板來管理空調負荷。為了滿足阿拉伯聯合大公國的標準,開發商擴大在地採購。承包商表示,採購透明度、永續發展認證和數位雙胞胎應對力是關鍵的得標標準,該地區58%的受訪公司都通用這些標準。儘管北美地區的建築支出成長放緩至年比2%,但該地區仍是成長的主要引擎。僅西雅圖市預計在2025年就將獲得174億美元的新契約,這主要得益於科研和生命科學設施的擴張,這些設施指定組裝性能為0.30 W/m²-K的單元式玻璃建築幕牆。美國基礎建設資金正惠及州立大學的維修,以透氣纖維水泥覆層取代老舊的預製混凝土。在歐洲,格倫費爾大火後,為滿足阻燃法規要求而進行的維修計劃正在穩定市場需求。法國的維修稅收優惠政策在新建設許可數量下降的同時,也支撐了市場需求。南美洲的成長主要集中在巴西東北部的大都會區,當地社會住宅的外牆擴大採用纖維水泥材料,以應對該國潮濕的熱帶氣候。這些趨勢表明,建築覆材市場既具有全球性,又具有高度本地化的特徵。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場促進因素

- 加強「淨零排放就緒」建築能源標準

- 高層建築維修時,必須對外部牆體進行耐火性能測試。

- 在城市熱島緩解獎勵下,對冷屋頂覆材給予優先待遇

- 抗冰雹金屬板保險費率加速折扣

- 利用數位雙胞胎進行預測性維護以降低生命週期成本(被低估了)

- 對低碳、生物基覆材(例如麻石板)的需求不斷成長(被低估了)

- 市場限制

- 鋁價波動對EPC利潤率帶來壓力

- 由於各地消防安全法規存在差異,導致產品核可延誤。

- 技術純熟勞工短缺導致安裝工期延長(未充分報告)

- 主要城市易燃建築幕牆的保險除外責任(未充分報告)

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 買方和消費者的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 定價分析

第5章 市場規模與成長預測

- 材料

- 陶瓷製品

- 木頭

- 石材

- 金屬

- 其他(石灰外牆、玻璃、纖維水泥、乙烯基)

- 依建築類型

- 新建工程

- 翻新

- 透過使用

- 商業設施

- 住宅

- 基礎設施

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、合資、交易)

- 市佔率分析

- 公司簡介

- Kingspan Group

- Compagnie de Saint-Gobain SA

- Arconic Corporation

- Etex Group

- James Hardie Industries PLC

- Tata Steel Ltd

- Alucobond(3A Composites)

- Nichiha Corporation

- CSR Limited

- Boral Limited

- Rockwool International

- Swisspearl Group

- Alucoil(Grupo Aliberico)

- Cembrit Holding A/S

- Alcoa Corporation

- Dow Building & Construction

- Hunter Douglas NV

- Shandong Century Sunshine

- Guangzhou Xingfa Aluminium

- Yaret Industrial Group

第7章 市場機會與未來展望

Cladding market size in 2026 is estimated at USD 129.14 billion, growing from 2025 value of USD 121.5 billion with 2031 projections showing USD 175.29 billion, growing at 6.29% CAGR over 2026-2031.

The upward trajectory is underpinned by stricter energy-efficiency rules, compulsory facade fire-performance testing, and municipal heat-island mitigation programs that collectively reshape material specifications and procurement practices. Demand is balanced between green-field activity and a fast-intensifying retrofit cycle in which aging facades need code-compliant fire resistance, lower operational carbon, and improved thermal performance. Supply-side resilience draws on vertical integration moves by large manufacturers and rising localization of metal and mineral panel production to shield projects from tariff-driven price swings. Ongoing digitalization-especially the use of twin-enabled asset monitoring-lowers lifecycle costs and influences bid decisions toward systems that can document performance in real time. External risks remain visible: aluminum price volatility can squeeze EPC margins, skilled-labor shortages lengthen installation schedules, and evolving fire codes can force unbudgeted facade replacements in dense urban cores.

Global Cladding Market Trends and Insights

Tightening Net-Zero-Ready Building Energy Codes

The 2024 International Energy Conservation Code introduces higher-performance envelope thresholds, while California's 2025 standards require heat-pump-ready shells and advanced insulation detailing. State and municipal stretch codes that reference these benchmarks compel new projects to specify high-R, thermally broken cladding assemblies. Commercial landlords are prioritizing integrated facade systems to curb operational expenses and secure green-lease premiums. The building cladding market benefits as material choices shift from cost-driven to performance-driven selection.

Mandatory Facade Fire-Performance Testing in High-Rise Retrofits

Post-Grenfell reforms embed non-combustibility requirements into the 2024 International Building Code and parallel national standards. High-rise owners now commission NFPA 285 testing or equivalent assessments before recladding, accelerating the swap-out of combustible ACM systems for mineral fiber or solid aluminum solutions. Suppliers able to certify compliant assemblies see faster bid-cycle conversions, reinforcing the building cladding market's tilt toward metal and stone wool cores.

Volatile Aluminum Prices Squeezing EPC Margins

Pending 2025 U.S. tariffs pushed Midwest aluminum premiums sharply higher, complicating bid pricing for curtain-wall and rainscreen packages. Contractors attempt hedging or escalation clauses, yet competitive tender rules often cap pass-through, eroding margins and delaying project starts.

Other drivers and restraints analyzed in the detailed report include:

- Urban Heat-Island Mitigation Incentives Favouring Cool-Roof Cladding

- Accelerated Insurance Premium Rebates for Hail-Resistant Metal Panels

- Skilled-Labour Shortages Lengthening Installation Schedules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal panels generated the single-largest revenue block, equal to 30.54% building cladding market share in 2025, as regulators demanded non-combustible exteriors on high rises. Wood cladding, buoyed by carbon-credit schemes and improved fire-retardant treatments, is registering a 6.50% CAGR through 2031 and is already specified on several net-zero schools and civic projects. Ceramic rainscreens continue to anchor premium commercial facades due to colorfastness and freeze-thaw resilience. Brick and stone veneer sales rise in renovation programs aiming to preserve architectural vernacular while boosting envelope R-values.

Demand in the "others" basket-stucco, glass, fiber-cement, and vinyl-follows region-specific code rhythms. Fiber-cement boards, supported by a USD 150 million domestic capacity expansion that aligns with federal "Build America" rules, secure listings on infrastructure projects and large multifamily builds. Smart glass facades gain traction where dynamic shading helps projects comply with cooling-load budgets. As codes prioritize performance attributes over material cost, suppliers that can certify low-carbon footprints and integrated fire-plus-thermal resistances position best for share capture within the building cladding market.

The Cladding Market Report is Segmented by Material (Ceramic, Wood, Brick and Stone, Metal, Others), Construction Type (New Construction, Renovation), Application (Commercial, Residential, Infrastructure), and Geography (North America, South America, Europe, Asia-Pacific, Middle East & Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 36.48% of global revenue in 2025. China's urban-renewal funding packages keep facade replacement programs active even as residential starts cool, while local governments in second-tier cities incentivize reflective roof membranes to cut summer power peaks. India's national infrastructure corridors spur demand for fire-rated metal panels in warehousing and logistics parks, with material cost inflation offset by improved construction finance availability. Japan's moderated cost environment unlocks small-footprint hospitality projects that deploy thin-gauge ceramic rainscreens to withstand seismic drift. Regional sustainability charters, including Indonesia's Nusantara capital plan, embed low-carbon facade targets at master-plan level, reinforcing long-run engagement for the building cladding market.

The Middle East & Africa region posts the fastest growth at a projected 6.58% CAGR through 2031. Saudi Arabia's Vision 2030 pipeline, surpassing USD 1.1 trillion in announced construction value, specifies non-combustible facade systems able to perform under extreme thermal cycling. UAE data-center builds, growing at 36% annually, demand highly insulated sandwich panels to manage HVAC loads, and developers increasingly source these panels locally to meet Emiratization thresholds. Contractors cite procurement visibility, sustainability passporting, and digital-twin readiness as top award criteria, a trend mirrored by 58% of firms surveyed in the region. North America remains a volume engine despite slower 2% year-on-year construction spending growth. Seattle alone expects USD 17.4 billion in new contracts in 2025, underpinned by laboratory and life-science expansions that specify unitized glass-and-panel facades capable of 0.30 W/m2-K assembly performance. Federal infrastructure funds cascade into state university retrofits where aged precast is replaced by ventilated fiber-cement cladding. Europe's demand stabilizes on retrofit projects that must meet post-Grenfell combustibility bans; French renovation tax credits sustain volumes even as green-field permits soften. South American growth concentrates in Brazil's northeastern urban nodes, where social-housing facades increasingly use fiber-cement to resist humid tropical conditions. Together, these dynamics illustrate why the building cladding market is simultaneously global and intensely local.

- Kingspan Group

- Compagnie de Saint-Gobain SA

- Arconic Corporation

- Etex Group

- James Hardie Industries PLC

- Tata Steel Ltd

- Alucobond (3A Composites)

- Nichiha Corporation

- CSR Limited

- Boral Limited

- Rockwool International

- Swisspearl Group

- Alucoil (Grupo Aliberico)

- Cembrit Holding A/S

- Alcoa Corporation

- Dow Building & Construction

- Hunter Douglas N.V.

- Shandong Century Sunshine

- Guangzhou Xingfa Aluminium

- Yaret Industrial Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Tightening "net-zero ready" building energy codes

- 4.1.2 Mandatory facade fire-performance testing in high-rise retrofits

- 4.1.3 Urban heat-island mitigation incentives favouring cool-roof cladding

- 4.1.4 Accelerated insurance premium rebates for hail-resistant metal panels

- 4.1.5 Digital twin-enabled predictive maintenance lowering lifecycle cost (under-reported)

- 4.1.6 Growing demand for low-carbon, bio-based cladding such as hemp-crete panels (under-reported)

- 4.2 Market Restraints

- 4.2.1 Volatile aluminium prices squeezing EPC margins

- 4.2.2 Fragmented local fire codes delaying product approvals

- 4.2.3 Skilled-labour shortages lengthening installation schedules (under-reported)

- 4.2.4 Insurance exclusions for combustible facades in key metros (under-reported)

- 4.3 Value / Supply-Chain Analysis

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Buyers/Consumers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Pricing Analysis

5 Market Size & Growth Forecasts (Value)

- 5.1 By Material

- 5.1.1 Ceramic

- 5.1.2 Wood

- 5.1.3 Brick and Stone

- 5.1.4 Metal

- 5.1.5 Others (Stucco, Glass, Fibre Cement, Vinyl)

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Renovation

- 5.3 By Application

- 5.3.1 Commerical

- 5.3.2 Residential

- 5.3.3 Infrastructure

- 5.4 By Region

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East & Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East & Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, Deals)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Kingspan Group

- 6.4.2 Compagnie de Saint-Gobain SA

- 6.4.3 Arconic Corporation

- 6.4.4 Etex Group

- 6.4.5 James Hardie Industries PLC

- 6.4.6 Tata Steel Ltd

- 6.4.7 Alucobond (3A Composites)

- 6.4.8 Nichiha Corporation

- 6.4.9 CSR Limited

- 6.4.10 Boral Limited

- 6.4.11 Rockwool International

- 6.4.12 Swisspearl Group

- 6.4.13 Alucoil (Grupo Aliberico)

- 6.4.14 Cembrit Holding A/S

- 6.4.15 Alcoa Corporation

- 6.4.16 Dow Building & Construction

- 6.4.17 Hunter Douglas N.V.

- 6.4.18 Shandong Century Sunshine

- 6.4.19 Guangzhou Xingfa Aluminium

- 6.4.20 Yaret Industrial Group

7 Market Opportunities & Future Outlook

覆材市場-2026-2032年全球市場預測

覆材市場-2026-2032年全球市場預測 2026 年至 2035 年外牆系統的市場機會、成長要素、產業趨勢分析與預測。

2026 年至 2035 年外牆系統的市場機會、成長要素、產業趨勢分析與預測。 防火覆層市場:按類型、應用、最終用途行業和地區分類。覆層系統市場:按材料、類型、應用和地區分類

防火覆層市場:按類型、應用、最終用途行業和地區分類。覆層系統市場:按材料、類型、應用和地區分類 覆材市場報告:按材料、組件、最終用戶和地區分類(2026-2034 年)

覆材市場報告:按材料、組件、最終用戶和地區分類(2026-2034 年) 2026年全球覆層系統市場報告

2026年全球覆層系統市場報告 覆材市場規模、佔有率及趨勢分析報告:依產品、應用、地區及細分市場預測(2026-2033 年)

覆材市場規模、佔有率及趨勢分析報告:依產品、應用、地區及細分市場預測(2026-2033 年) 全球覆層系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球衛浴覆層市場報告

全球覆層系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球衛浴覆層市場報告 覆層系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(按材料、應用、組件類型、地區和競爭格局分類,2021-2031年)

覆層系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(按材料、應用、組件類型、地區和競爭格局分類,2021-2031年)