|

市場調查報告書

商品編碼

1940627

無菌醫療包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Sterile Medical Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

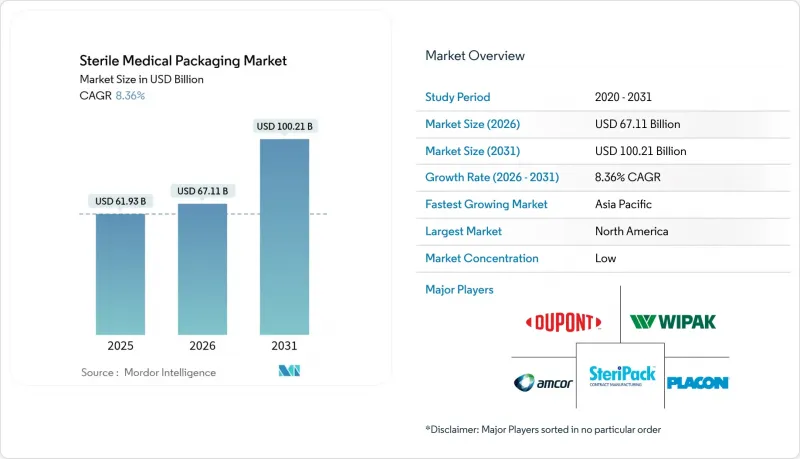

無菌醫療包裝市場預計將從 2025 年的 619.3 億美元成長到 2026 年的 671.1 億美元,預計到 2031 年將達到 1002.1 億美元,2026 年至 2031 年的複合年成長率為 8.36%。

這一成長反映了藥物傳輸領域向無污染方向的重大轉變、日益嚴格的全球標準以及材料的快速創新。手術量的成長、生物製藥產品線的不斷擴展以及一次性醫療器材的普及推動了市場需求,而更嚴格的環氧乙烷排放法規則迫使製造商轉向多樣化的滅菌方法。數位化檢驗工具、基於風險的品質體係以及人工智慧驅動的檢測平台正在重塑生產經濟模式和競爭策略。同時,永續性發展的迫切需求促使供應商開發高阻隔阻隔性可回收基材,而樹脂價格的波動以及有關再生材料含量的法規則增加了成本和技術複雜性。

全球無菌醫療包裝市場趨勢與洞察

嚴格的感染控制法規和標準

美國食品藥物管理局 (FDA) 將於 2026 年 2 月前使其品管系統法規與 ISO 13485:2016 標準接軌,強制要求在整個無菌醫療包裝市場實施基於風險的驗證和容器密封測試。歐洲藥品管理局 (EMA) 修訂的 GMP 附錄 1 已開始鼓勵製藥公司合格其初級包裝,從而推動了對經過驗證的無菌屏障系統的高階需求。 ISO 11607 的修訂擴展了這些風險管理原則,並鼓勵供應商採用可追溯性和數位化文件。在製藥產業叢集附近設立近岸滅菌中心,透過減少運輸過程中的風險暴露並確保隨時準備接受審核,可以有效配合這些法規。像 West Pharmaceutical Services 這樣的先驅報告稱,符合這些更高標準的 NovaPure 組件訂單強勁。

手術量增加及慢性疾病負擔加重

受人口老化和微創手術興起的推動,預計到2024年,全球手術量將增加12%。從可重複使用器械到一次性器械包的轉變,推動了複雜器械套裝無菌包裝的需求。糖尿病管理就是這個趨勢的典型例證:預計到2024年,預填充胰島素筆的使用率將成長18%,這就要求包裝能承受家庭環境中的溫度波動,同時保持無菌狀態。門診和居家照護的普及,也促使人們需要易於開啟、防篡改且提供清晰使用說明的包裝設計。目前,67%的大型包裝廠已採用基於人工智慧的視覺檢測技術,這有助於製造商在不影響品質的前提下管理不斷成長的產量。

樹脂價格波動和供應鏈中斷

2024年,受能源價格上漲和天氣相關供應中斷的影響,聚乙烯成本較去年同期飆升28%。中型包裝製造商的利潤率下降了12%至15%,被迫提高安全庫存水平,營運資金也受到限制。更嚴格的環氧乙烷排放法規導致產能關閉,暫時延長了滅菌前置作業時間,進一步加劇了這種情況。一些公司試圖透過簽訂多年樹脂合約或垂直整合薄膜擠出製程來緩解價格波動,但短期壓力仍然存在。對再生材料含量的監管基準值進一步擾亂了原料規格,需要進行大量檢驗,並增加了營運資金。

細分市場分析

到2025年,塑膠將佔無菌醫療包裝市場67.62%的佔有率,主要得益於聚丙烯的耐滅菌循環性和聚乙烯的抗穿刺性。然而,紙張和紙板將以9.98%的複合年成長率引領該細分市場,這主要受醫院永續性目標和品牌對回收承諾的推動。 PETG正擴大取代PVC用於熱成型托盤,以提高手術包的可見度。預計到2031年,紙基無菌醫療包裝市場規模將達到106.4億美元,主要得益於可耐受蒸氣和等離子滅菌的透氣塗層技術。然而,再生材料的加入會影響阻隔性能的穩定性,需要對材料科學進行大量投資並進行額外的保存期限測試。將消費後樹脂應用於泡殼包裝的供應商正在採用先進的純化工藝,以確保符合ISO 11607標準。雖然由於運輸成本壓力,玻璃的使用量正在下降,但玻璃的惰性特性仍然支撐著對濕度敏感的生物製藥的特定需求,這彌補了其重量上的劣勢。

第二代塑膠因其在進程內添加了便於分類的添加劑,正逐漸成為合規解決方案。這些單一材料複合材料無需使用傳統上阻礙回收的黏合劑,並維持了良好的微生物阻隔性能,使製造商能夠達到歐盟25%的再生材料含量目標。然而,製藥經銷商仍需遵循美國藥典的指導原則,該原則仍建議對高風險注射劑型使用新型聚合物。隨著樹脂供應商推出物料平衡認證的材料,品牌所有者無需改變包裝的化學成分即可獲得永續性積分,這提供了一種過渡性解決方案,預計將在2027年之前廣泛應用。

截至2025年,熱成型托盤將維持28.26%的無菌醫療包裝市場佔有率,其剛性強、加工效率高。儘管該細分市場的成長趨於平緩,但無菌瓶和容器的成長卻以12.18%的複合年成長率加速,這主要得益於吹灌封生產線降低了無菌轉移的風險。新型吹灌封生產線模組的年產能可達每家工廠1.7億件,足以滿足大眾市場吸入療法的需求。袋裝產品在高通量輸液和透析迴路中越來越受歡迎,這得益於其靈活的供應鏈經濟優勢。

儘管管瓶和西林瓶仍然是注射劑填充的基礎,但即用型包裝正在削弱對玻璃脫氧隧道的需求。即用型產品聯盟(Gerresheimer、Stevanato Group 和 SCHOTT Pharma)正在對包裝規格和滅菌工藝進行標準化,以簡化填充和表面處理工程。受患者自我給藥的推動,預填充式注射器正以每年 22% 的速度成長,而與自動注射器相容的包裝則保持著較高的價格。包裝、瓶蓋和無菌密封件仍然是必不可少的輔助配件,而帶有氟聚合物薄膜的新型彈性體塞則有助於減少蛋白質生物製藥中的藥物相互作用。預計所有規格的注射器系統的無菌醫療包裝市場將從 2026 年的 97.2 億美元成長到 2031 年的 169.6 億美元,這表明醫療器械的融合程度正在不斷提高。

這份醫用滅菌包裝市場報告材料類型(塑膠、紙/紙板、玻璃等)、產品類型(熱成型托盤、滅菌瓶/容器、包裝袋/包裝盒、泡殼包裝等)、應用領域(藥品/生技藥品、外科/醫療器械等)、滅菌方法(化學滅菌、輻射滅菌、熱滅菌等)和地區進行細分。市場預測以美元計價。

區域分析

北美地區憑藉嚴格的法律規範和豐富的生物製藥研發管線,預計到2025年將佔據無菌醫療包裝市場38.45%的佔有率。該地區的領先地位得益於持續的再投資:格雷斯海默公司在洛爾投資1.08億美元興建的氧氣混合熔爐,不僅減少了40%的排放,還提高了熔爐的生產能力,並確保了美國注射劑玻璃的供應。即將實施的FDA品管系統報告(QMSR)要求迫使美國本土製造商加強數位化文件管理,並推廣採用基於雲端的審核平台。然而,樹脂價格的波動以及美國環保署(EPA)對環氧乙烷的監管,推高了營運成本,促使滅菌能力轉移到鄰近主要製藥叢集的地區。

亞太地區預計將成為成長最快的地區,到2031年複合年成長率將達到11.42%,並在2028年實現絕對值超過歐洲。中國國家藥品監督管理局(NMPA)的改革與國際人用藥品註冊技術協調會(ICH)指南相一致,並放寬了出口壁壘,吸引了新的投資湧入江蘇和浙江兩省。安姆科位於雪蘭莪的包衣工廠建立了亞洲首條氣刀醫療器材生產線,展現了成熟市場的技術轉移。印度的學名藥中心正在擴建泡殼包裝和吹灌封(BFS)設施,以支持出口擴張,印度藥品協會(IPA)成員公司中有67%計劃在2026年前升級其包裝設施。東南亞(泰國、越南)擁有成本效益高的無塵室勞動力,吸引了合約包裝商為區域疫苗聯盟提供服務。

歐洲持續引領創新,歐盟包裝廢棄物法規 (EU) 2025/40 要求到 2030 年塑膠包裝中必須含有 25% 的再生材料。原始設備製造商 (OEM) 為獲得環保標籤優勢,正努力接受更高的材料成本,例如 Sudpac 的 PharmaGuard 榮獲國家永續性獎。德國、義大利和荷蘭正在擴大輻射加工產能,以填補環氧乙烷 (EO) 的供不應求。波蘭等東歐國家正崛起為標籤印刷和包裝袋加工的轉運中心,既能滿足歐盟的醫藥需求,也能避免西歐高昂的人事費用成本。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 嚴格的感染控制法規和標準

- 手術量增加和慢性病負擔加重

- 生物製藥和注射需求激增,需要高度可靠的包裝

- 阻隔性可再生塑膠和紙張的快速材料創新

- 將「消毒服務」基地近岸外包至製藥產業叢集附近

- 人工智慧驅動的貨櫃近距離完整性(CCI)檢測數位雙胞胎

- 市場限制

- 樹脂價格波動和供應鏈中斷

- 多司法管轄區的監管複雜性和合規成本

- 法律強制規定最低再生材料含量,這可能會影響包裝的完整性。

- 由於排放法規,環氧乙烷(EtO)產能短缺。

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 產業間競爭

- 定價分析

第5章 市場規模與成長預測

- 依材料類型

- 塑膠

- 聚丙烯

- 聚乙烯

- 聚對苯二甲酸乙二酯

- 聚氯乙烯

- 聚苯乙烯

- 其他塑膠

- 紙和紙板

- 玻璃

- 其他材料類型

- 塑膠

- 依產品類型

- 熱成型托盤

- 無菌瓶和容器

- 小袋和袋子

- 泡殼包裝

- 管瓶和安瓿

- 預填充式注射器和吸入器

- 包裝和蓋子

- 無菌封蓋和塞子

- 透過使用

- 藥品和生物製藥

- 外科和醫療器械

- 體外診斷(IVD)試劑盒和試劑

- 醫療植入和一次性醫療設備

- 其他用途

- 透過滅菌方法

- 化學

- 輻射

- 熱感的

- 冷等離子和臭氧

- 基於無菌/過濾

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- ASEAN

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 中東

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、合資、產能擴張)

- 市佔率分析

- 公司簡介

- Amcor plc

- DuPont de Nemours Inc.

- 3M Company

- Nelipak Healthcare Packaging

- Tekni-Plex Inc.

- Oliver Healthcare Packaging

- Wipak Group

- Steripack Group

- Placon Corporation

- Sonoco Products Co.

- Billerud

- Paxxus Inc.

- Charter Next Generation

- Riverside Medical Packaging

- Technipaq Inc.

- DWK Life Sciences

- Sigma Medical Supplies

- Sterimed Holdings

- West Pharmaceutical Services

- WestRock Company

- Gerresheimer AG

- APTAR Group

第7章 市場機會與未來展望

The sterile medical packaging market is expected to grow from USD 61.93 billion in 2025 to USD 67.11 billion in 2026 and is forecast to reach USD 100.21 billion by 2031 at 8.36% CAGR over 2026-2031.

This expansion reflects a decisive move toward contamination-free drug delivery, tighter global standards, and rapid material innovation. Heightened surgical volumes, growing biologics pipelines, and the migration to single-use devices are accelerating demand, while stricter emission rules for ethylene oxide are steering manufacturers toward diversified sterilization methods. Digital validation tools, risk-based quality systems, and AI-driven inspection platforms are reshaping production economics and competitive strategy. At the same time, sustainability mandates are pressuring suppliers to engineer high-barrier recyclable substrates, even as resin price volatility and recycled-content legislation add cost and technical complexity.

Global Sterile Medical Packaging Market Trends and Insights

Stringent Infection-Control Regulations and Standards

The FDA will fully align its Quality Management System Regulation with ISO 13485:2016 by February 2026, making risk-based validation and container-closure integrity testing mandatory across the sterile medical packaging market. EMA's revised GMP Annex 1 is already compelling pharmaceutical firms to requalify primary packs, spurring premium demand for validated sterile barrier systems. ISO 11607 amendments extend these risk-management principles, encouraging suppliers to embed traceability and digital documentation. Near-shoring of sterilization hubs close to pharma clusters complements these rules by cutting transit exposures and ensuring audit readiness. Early adopters like West Pharmaceutical Services report stronger order books for NovaPure components that conform to these upgraded standards.

Rise in Surgical Volumes and Chronic Disease Burden

Global procedure counts climbed 12% in 2024, led by aging populations and greater access to minimally invasive surgery. Single-use kits are replacing reusables, multiplying sterile pack demand for complex instrument sets. Diabetes management illustrates the trend: prefilled insulin pen uptake grew 18% in 2024, requiring packs that resist household temperature swings while safeguarding sterility. The shift to outpatient and home settings intensifies design needs for easy-open formats, tamper evidence, and clear instructions. AI-based visual inspection, now operating in 67% of large packaging plants, helps producers keep pace with rising volume without compromising quality.

Volatile Resin Pricing and Supply-Chain Shocks

Polyethylene costs jumped 28% year-over-year in 2024 on energy price spikes and weather-related disruptions. Mid-tier packagers saw 12-15% margin squeeze and were forced to raise safety-stock levels, tying up working capital. Ethylene-oxide emission curbs worsened the picture, as capacity shutdowns briefly raised sterilization lead times. Some firms locked multiyear resin contracts or vertically integrated film extrusion to tame volatility, yet exposure remains a near-term drag. Legislated recycled-content thresholds further destabilize raw-material specifications, demanding extensive validation that inflates working capital.

Other drivers and restraints analyzed in the detailed report include:

- Boom in Biologics and Injectables Needing High-Integrity Packs

- Rapid Material Innovations in High-Barrier Recyclable Plastics and Papers

- Multi-Jurisdiction Regulatory Complexity and Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastics delivered 67.62% sterile medical packaging market share in 2025, led by polypropylene's sterility-cycle tolerance and polyethylene's puncture resistance. Paper and paperboard, however, are pacing the segment at a 9.98% CAGR, pushed by hospital sustainability targets and brand commitments to recyclability. PETG is replacing PVC in thermoformed trays for clearer visualization of surgical kits. The sterile medical packaging market size for paper formats is on track to reach USD 10.64 billion in 2031, enabled by breathable coatings that pass both steam and plasma sterilization. Yet recycled-content inclusion complicates barrier consistency, prompting widespread investment in material science and additional shelf-life testing. Suppliers integrating post-consumer resin into blister webs use advanced purification stages to preserve ISO 11607 compliance. Though glass usage declines amid freight-cost pressures, niche demand persists for moisture-sensitive biologics where glass's inertness still outweighs its weight penalty.

Second-generation plastics featuring in-process additives for easy sorting are emerging as compliance workarounds. These mono-material laminates eliminate adhesives that previously blocked recyclability, allowing converters to achieve EU's 25% recycled-content target while retaining microbial barrier performance. However, pharmaceutical license holders must reconcile these gains with U.S. Pharmacopeia guidelines, which still favor virgin polymers for high-risk parenterals. As resin suppliers roll out mass-balance certified feedstocks, brand owners can claim sustainability credits without altering pack chemistry, an interim solution expected to boost adoption through 2027.

Thermoform trays retained 28.26% share of the sterile medical packaging market in 2025, valued for rigidity and procedural efficiency. The segment's growth is flattening, while sterile bottles and containers are accelerating at a 12.18% CAGR, supported by blow-fill-seal lines that cut aseptic transfer risk. New BFS modules produce up to 170 million units per facility annually, enabling scale suitable for mass-market inhalation therapies. Pouches and bags capitalize on flexible supply-chain economics, finding traction in high-throughput IV fluid and dialysis circuits.

Vials and ampoules still underpin most injectable fills, but ready-to-use formats are cannibalizing glass depyrogenation tunnels. The Alliance for RTU-Gerresheimer, Stevanato Group, and SCHOTT Pharma-aims to standardize geometry and sterilization, smoothing fill-finish operations. Prefilled syringes exhibit 22% annual growth, fueled by patient self-administration, while autoinjector-compatible packs command premium pricing. Wraps, lids, and sterile closures remain essential adjuncts; newer elastomeric stoppers sporting fluoropolymer films mitigate drug-component interactions for proteinaceous biologics. Across formats, the sterile medical packaging market size attached to syringe systems is forecast to expand from USD 9.72 billion in 2026 to USD 16.96 billion in 2031, underscoring device convergence.

The Sterile Medical Packaging Market Report is Segmented by Material Type (Plastics, Paper and Paperboard, Glass, and More), Product Type (Thermoform Trays, Sterile Bottles and Containers, Pouches and Bags, Blister Packs and More), Application (Pharmaceutical and Biologics, Surgical and Medical Instruments and More), Sterilization Method (Chemical, Radiation, Thermal, and More), and Geography. Market Forecasts are in Value (USD).

Geography Analysis

North America generated 38.45% of the sterile medical packaging market revenue in 2025, backed by stringent regulatory oversight and deep biologics pipelines. The region's dominance is maintained through continual reinvestment: Gerresheimer's USD 108 million oxy-hybrid furnace in Lohr cuts emissions 40% and elevates melter capacity, securing glass supply for U.S. injectables. Compliance with the upcoming FDA QMSR compels domestic producers to upgrade digital documentation, supporting the adoption of cloud-hosted audit platforms. Yet resin price swings and EPA EO rules raise operating costs, encouraging near-shoring of sterilization capacity adjacent to major drug clusters.

Asia-Pacific is the fastest-advancing territory, recording an 11.42% CAGR through 2031 and poised to eclipse Europe in absolute value by 2028. China's NMPA reforms, aligning with ICH guidelines, ease export hurdles, attracting greenfield investments in Jiangsu and Zhejiang. Amcor's Selangor coating plant marks the first air-knife healthcare line in Asia, evidence of technology transfer from mature markets. India's generics hub is scaling blister and BFS capacity to support export ambitions; 67% of IPA members plan packaging upgrades by 2026. Southeast Asia-Thailand, Vietnam-offers cost-effective clean-room labor, drawing contract packagers that service regional vaccine alliances.

Europe remains an innovation stronghold, governed by Packaging Waste Regulation (EU) 2025/40 that forces 25% recycled content in plastic packs by 2030. OEMs accept higher material costs to secure eco-label advantages, evidenced by Sudpack's PharmaGuard winning a national sustainability award. Germany, Italy, and the Netherlands are scaling radiation capacity to offset EO bottlenecks. Eastern European states such as Poland are emerging as overflow sites for label printing and pouch converting, benefiting from proximity to EU pharmaceutical demand without the higher wage overhead of Western Europe.

- Amcor plc

- DuPont de Nemours Inc.

- 3M Company

- Nelipak Healthcare Packaging

- Tekni-Plex Inc.

- Oliver Healthcare Packaging

- Wipak Group

- Steripack Group

- Placon Corporation

- Sonoco Products Co.

- Billerud

- Paxxus Inc.

- Charter Next Generation

- Riverside Medical Packaging

- Technipaq Inc.

- DWK Life Sciences

- Sigma Medical Supplies

- Sterimed Holdings

- West Pharmaceutical Services

- WestRock Company

- Gerresheimer AG

- APTAR Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent infection-control regulations and standards

- 4.2.2 Rise in surgical volumes and chronic disease burden

- 4.2.3 Boom in biologics and injectables needing high-integrity packs

- 4.2.4 Rapid material innovations in high-barrier recyclable plastics and papers

- 4.2.5 Near-shoring of "sterilization-as-a-service" hubs near pharma clusters

- 4.2.6 AI-driven container-closure integrity (CCI) inspection and digital twins

- 4.3 Market Restraints

- 4.3.1 Volatile resin pricing and supply-chain shocks

- 4.3.2 Multi-jurisdiction regulatory complexity and compliance costs

- 4.3.3 Legislative push for minimum recycled content risking pack integrity

- 4.3.4 Shortage of ethylene-oxide (EtO) capacity amid emission curbs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Plastics

- 5.1.1.1 Polypropylene

- 5.1.1.2 Polyethylene

- 5.1.1.3 Polyethylene-terephthalate glycol

- 5.1.1.4 Polyvinyl Chloride

- 5.1.1.5 Polystyrene

- 5.1.1.6 Other Plastics

- 5.1.2 Paper and Paperboard

- 5.1.3 Glass

- 5.1.4 Other Material Types

- 5.1.1 Plastics

- 5.2 By Product Type

- 5.2.1 Thermoform Trays

- 5.2.2 Sterile Bottles and Containers

- 5.2.3 Pouches and Bags

- 5.2.4 Blister Packs

- 5.2.5 Vials and Ampoules

- 5.2.6 Pre-filled Syringes and Inhalers

- 5.2.7 Wraps and Lids

- 5.2.8 Sterile Closures and Stoppers

- 5.3 By Application

- 5.3.1 Pharmaceutical and Biologics

- 5.3.2 Surgical and Medical Instruments

- 5.3.3 In-Vitro Diagnostics (IVD) Kits and Reagents

- 5.3.4 Medical Implants and Disposables

- 5.3.5 Other Applications

- 5.4 By Sterilization Method

- 5.4.1 Chemical

- 5.4.2 Radiation

- 5.4.3 Thermal

- 5.4.4 Low-temperature Plasma and Ozone

- 5.4.5 Aseptic/Filtration-based

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Russia

- 5.5.2.8 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 ASEAN

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Nigeria

- 5.5.4.2.3 Egypt

- 5.5.4.2.4 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, Capacity Expansions)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 DuPont de Nemours Inc.

- 6.4.3 3M Company

- 6.4.4 Nelipak Healthcare Packaging

- 6.4.5 Tekni-Plex Inc.

- 6.4.6 Oliver Healthcare Packaging

- 6.4.7 Wipak Group

- 6.4.8 Steripack Group

- 6.4.9 Placon Corporation

- 6.4.10 Sonoco Products Co.

- 6.4.11 Billerud

- 6.4.12 Paxxus Inc.

- 6.4.13 Charter Next Generation

- 6.4.14 Riverside Medical Packaging

- 6.4.15 Technipaq Inc.

- 6.4.16 DWK Life Sciences

- 6.4.17 Sigma Medical Supplies

- 6.4.18 Sterimed Holdings

- 6.4.19 West Pharmaceutical Services

- 6.4.20 WestRock Company

- 6.4.21 Gerresheimer AG

- 6.4.22 APTAR Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-needs Assessment

無菌醫療包裝市場:2026-2032年全球市場預測(按產品類型、滅菌方法、材料、最終用戶、應用和分銷管道分類)

無菌醫療包裝市場:2026-2032年全球市場預測(按產品類型、滅菌方法、材料、最終用戶、應用和分銷管道分類) 無菌醫療包裝市場分析及預測(至2035年):依類型、材質、產品類型、應用、技術、最終用戶、製程及設備分類

無菌醫療包裝市場分析及預測(至2035年):依類型、材質、產品類型、應用、技術、最終用戶、製程及設備分類 無菌醫療包裝市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測

無菌醫療包裝市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測 2026年全球無菌醫療包裝市場報告

2026年全球無菌醫療包裝市場報告 無菌醫療包裝市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、材料、滅菌方法、應用、地區和競爭格局分類),2021-2031年醫用包裝薄膜市場(依材料類型、包裝類型、滅菌方式、應用領域和最終用戶分類)-全球預測,2026-2032年

無菌醫療包裝市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、材料、滅菌方法、應用、地區和競爭格局分類),2021-2031年醫用包裝薄膜市場(依材料類型、包裝類型、滅菌方式、應用領域和最終用戶分類)-全球預測,2026-2032年 無菌醫療包裝市場規模、佔有率和成長分析(按材料、類型、滅菌方法、應用和地區分類)—產業預測(2026-2033 年)

無菌醫療包裝市場規模、佔有率和成長分析(按材料、類型、滅菌方法、應用和地區分類)—產業預測(2026-2033 年) 醫療包裝市場規模、佔有率和成長分析(按類型、材料、應用、最終用戶和地區分類)-2026-2033年產業預測醫療包裝市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材料、包裝類型、應用、地區和競爭格局分類,2020-2030 年預測

醫療包裝市場規模、佔有率和成長分析(按類型、材料、應用、最終用戶和地區分類)-2026-2033年產業預測醫療包裝市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材料、包裝類型、應用、地區和競爭格局分類,2020-2030 年預測 全球無菌醫療包裝市場:預測(至 2032 年)—按產品類型、材料類型、滅菌方法、應用、最終用戶和地區進行分析

全球無菌醫療包裝市場:預測(至 2032 年)—按產品類型、材料類型、滅菌方法、應用、最終用戶和地區進行分析