|

市場調查報告書

商品編碼

1940620

鋁製瓶蓋和封蓋:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Aluminum Caps And Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

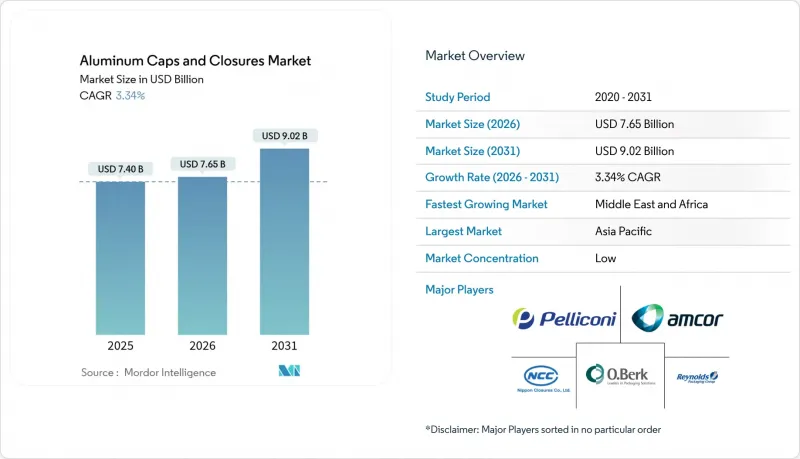

預計鋁製瓶蓋和瓶塞市場將從 2025 年的 74 億美元成長到 2026 年的 76.5 億美元,到 2031 年將達到 90.2 億美元,2026 年至 2031 年的複合年成長率為 3.34%。

由於主要飲料細分市場的滲透率已趨於成熟,需求成長並非爆發式成長,而是循序漸進。然而,高階烈酒市場需求的成長、生物製藥包裝需求的增加以及歐盟永續性法規的日益嚴格,持續開拓著盈利市場。歐洲強制性瓶蓋固定法規、中國對再生鋁的激勵措施以及北美市場向高階即飲產品的轉變,都促使品牌所有者重新設計瓶蓋,以提升其功能性和美觀性。儘管倫敦金屬交易所 (LME) 的價格波動給加工商的利潤率帶來了壓力,但對可無限循環利用材料日益成長的需求,仍然使鋁材優於軟木、鋼材和塑膠。區域成本優勢,尤其是在亞太地區,以及不斷成長的回收能力,有助於抵消原料價格波動的影響,同時繼續使高階市場免受低成本 PET 替代品的衝擊。

全球鋁製瓶蓋及瓶塞市場趨勢及洞察

北美高階即飲雞尾酒鋁瓶包裝的興起

2024年,高階即飲雞尾酒品牌紛紛推出鋁瓶,在保持可回收性的同時,將自身定位為高階產品。有些品牌的鋁瓶售價比傳統易拉罐高出40%至60%,顯示消費者非常重視包裝的觸感耐用性和再封功能。鋁的阻隔性能可以保護植物萃取物免受紫外線和氧氣的侵害,從而延長以烈酒為基底的配方的保存期限。與環保組織的合作進一步強化了永續性的形象,創造了小型鋼罐或寶特瓶無法實現的行銷優勢。這種趨勢也正在歐洲旅遊零售市場蔓延,那裡的烈酒需要既防竄改又美觀的包裝。

歐盟飲料包裝必須使用繫繩式瓶蓋(指令 2019/904)

自2024年7月起,歐盟將強制所有飲料瓶使用繫繩式瓶蓋,促使碳酸飲料和礦泉水產業重新設計瓶蓋。儘管消費者最初對塑膠繫繩式瓶蓋有所抵觸,但高階礦泉水和果汁品牌已轉向使用帶有整合式鉸鏈機構的鋁製螺旋蓋。鋁的無限可回收性和在資源回收設施中易於分離的特性,使品牌所有者能夠同時滿足繫繩式瓶蓋法規和即將實現的90%金屬回收目標。跨國公司也在非歐盟市場推行包裝標準化,以避免生產線變更的複雜性,推動了近期對高價值鋁製瓶蓋的需求。

倫敦金屬交易所(LME)鋁價波動對加工商的利潤率帶來壓力。

2025年2月,鋁錠價格達到每噸2,662美元,六個月內波動超過15%。簽訂長期固定合約的加工商面臨壓力。規模較小的生產商由於缺乏避險機制,利潤率不斷下降,成為擁有完善風險管理部門的跨國公司的理想收購目標。俄羅斯出口的不確定性、歐洲冶煉電力成本的上漲以及美國新的貨櫃關稅加劇了這種波動。為了穩定供應,大型加工商正在探索提高再生鋁含量和使用廢鋼的合金配方,這些配方符合碳減排承諾,但需要投入資金升級退火爐。

細分市場分析

螺旋蓋廣泛應用於飲料、調味品和醫藥產業,預計2025年將維持其主導地位,市佔率高達50.74%。這一佔有率意味著2025年鋁製蓋和封蓋市場規模將達到37.5億美元,體現了其可靠的密封性能。易開蓋雖然體積較小,但預計到2031年將以6.38%的複合年成長率快速成長,這主要得益於消費者對罐裝咖啡和蒸餾食品便利性的需求日益成長。連續螺紋ROPP蓋在精釀烈酒市場中佔據了重要地位,兼具防篡改功能和高階視覺吸引力。皇冠蓋在傳統啤酒包裝中仍佔據重要地位,但隨著纖細罐裝啤酒的普及,其成長速度正在放緩。卡扣蓋、按壓旋轉蓋和特殊翻蓋設計則針對食品和醫藥等對篡改敏感的應用領域,標誌著該領域正從「一刀切」的解決方案轉向針對特定應用場景的解決方案。

對模切和壓痕技術的投資,使得瓶蓋拉環更安全、更易於手指抓握,從而開闢了新的大眾市場,例如老年人營養飲品市場。瓶蓋製造商還在瓶蓋上整合雷射雕刻的QR碼,在不犧牲裝飾空間的前提下實現產品溯源。這些裝飾元素提高了單位成本,在原料成本上漲的當下,有效提升了利潤率。同時,標準的螺旋蓋形式日益趨於同質化,迫使製造商透過改進內襯化學成分來提升產品差異化,從而延長高pH值飲料的保存期限。

到2025年,飲料業將佔鋁製瓶蓋和封蓋市場(價值34.1億美元)的46.02%。該領域涵蓋礦泉水、碳酸飲料、啤酒、葡萄酒和頂級烈酒,每種產品都有其獨特的封蓋要求。高檔酒類生產商將鋁作為品牌宣傳的載體,而碳酸飲料填充商則尋求以最低成本滿足歐盟的Tether法規要求。預計製藥業的需求將以6.76%的複合年成長率成長,到2031年將創造2.84億美元的附加價值。這一成長主要得益於生物製藥新產品的推出,這些產品指定使用翻蓋式易碎密封件以確保無菌性。食品應用領域的需求保持穩定,這主要得益於高檔食用油和醬料採用金屬凸耳蓋以實現順暢的傾倒控制。個人護理品牌正在強調鋁的可回收性並取代複合材料封蓋,例如,採用可回收鋁製氣霧罐容器的高調推出的除臭劑產品就體現了這一點。

跨行業經驗正在推動創新:一家飲料罐供應商正與一家化妝品公司合作,改進其內清漆,使其與乳液相容,從而擴大其目標市場。工業化學品罐蓋雖然是一個小眾市場,但鋁的耐腐蝕性與專用內襯相結合,正使其在市場中佔據優勢。多種應用情境的通用性有助於建立均衡的產品組合,從而對沖特定產業的週期性低迷風險。

鋁製瓶蓋及封蓋市場按瓶蓋類型(螺旋蓋、皇冠蓋、按壓式/旋蓋等)、應用領域(飲料、食品、醫藥、化妝品及個人護理等)、瓶頸直徑(20毫米以下、21-30毫米等)、通路(銷售管道、間接銷售管道)和地區進行細分。市場規模和預測均以美元以金額為準。

區域分析

亞太地區受中國豐富的飲料產量和印度包裝產品市場的擴張所推動,預計到2025年將佔全球收入的40.20%。中國於2024年11月取消進口再生鋁關稅,提高了成本競爭力,使冶煉廠能夠以低於原鋁的價格供應鋁捲。日本和韓國正將技術進步引入該地區,出口瓶蓋壓平機和視覺檢測系統。東南亞的需求受到都市化和西方快餐連鎖店對防篡改瓶蓋的需求的推動,刺激了當地瓶蓋加工廠的發展。在印度,食用油包裝上強制使用QR碼追蹤,提高了包裝標準,擴大了高階旋蓋的價值佔有率,並鼓勵外資合資企業進入市場。

預計中東和非洲地區將成為成長最快的市場,到2031年複合年成長率將達到6.89%。奈及利亞和肯亞的飲料投資以及海灣地區瓶裝淡化水產能的提升支撐了市場需求。然而,循環經濟基礎設施的匱乏限制了鋁蓋子與封口裝置的市場滲透。儘管埃及在建立專門的食品級回收工廠方面取得了進展,但建立經濟永續的回收管道是實現廣泛應用的先決條件。在南非,完善的鋁冶煉基礎設施和港口連接為這個內陸國家創造了出口機會。

儘管歐洲市場已趨於成熟,但由於法規主導全球規範,它仍然至關重要。 2024年7月固定瓶蓋強制令的最後期限迫使灌裝商同時重新設計PET和鋁製容器,為瓶蓋專家帶來了工程諮詢收入。一家德國機械工程叢集開發了每分鐘可生產600個產品的連續螺紋螺旋蓋機,並整合了扭力監控功能,提高了性能標準。一家義大利設計公司為高階烈酒客製化了壓紋和變色油墨,在從軟木塞向鋁製瓶蓋永續性過渡的過程中,保持了產品的高階質感。

北美市場正在成長,這主要得益於消費者對可重複密封鋁瓶裝精釀飲料和即飲雞尾酒的需求增加。美國於2025年4月生效的關稅壁壘間接支持了瓶蓋卷材製造商,一方面鼓勵國內罐體庫存生產,另一方面由於供應緊張,促使生產商重返日本市場。墨西哥是主要的啤酒出口國,為了平衡成本和供應風險,該國同時使用鋁製和鋼製瓶蓋材料。然而,鋁製瓶蓋在歐洲高階瓶裝飲料生產線上仍然佔據一定地位。在南美洲,尤其是巴西,各公司正在投資建造配備內部瓶蓋生產模組的新型飲料罐生產線,以縮短前置作業時間。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 北美高階即飲雞尾酒鋁瓶包裝的興起

- 歐盟飲料包裝強制過渡到繫繩式瓶蓋(指令 2019/904)

- 中國擴大飲料用再生鋁產能

- 製藥業向生物製藥用翻蓋式鋁製密封過渡

- 歐洲精釀烈酒包裝從軟木塞到鋁製ROPP的過渡

- 印度電子商務洩漏測試通訊協定推動 RagCap 的普及

- 市場限制

- 倫敦金屬交易所(LME)鋁價波動對加工商利潤帶來壓力

- 品牌商在碳酸飲料中改用PET材質的瓶蓋

- 墨西哥啤酒中無錫鋼皇冠瓶塞的替代

- 中東地區對食品級回收途徑的限制

- 供應鏈分析

- 技術展望

- 監理展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 競爭對手之間的競爭

- 替代品的威脅

第5章 市場規模與成長預測

- 按帽型

- 螺帽

- 皇冠軟木塞

- 凸耳/按壓式

- 易打開端

- 滾動式防盜裝置(ROPP)

- 其他(豎中指、拆解)

- 透過使用

- 飲料

- 酒精飲料

- 不含酒精的飲料

- 食物

- 製藥

- 化妝品和個人護理

- 工業和家用化學品

- 飲料

- 頸部直徑

- 20毫米或更小

- 21-30 mm

- 31-40 mm

- 40毫米或以上

- 透過分銷管道

- 銷售管道

- 間接銷售管道

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 義大利

- 英國

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 中東

- GCC

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 肯亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Amcor plc

- Crown Holdings Inc.

- Silgan Holdings Inc.

- Guala Closures SpA

- Tecnocap Group

- Pelliconi and C. SpA

- Nippon Closures Co. Ltd

- Closure Systems International(CSI)

- Berlin Packaging LLC

- Bericap GmbH

- AptarGroup Inc.

- SKS Bottle and Packaging Inc.

- Hicap Closures Co. Ltd

- Federfin Tech SRL

- Rauh GmbH & Co.

- O.Berk Company

- The Cary Company

- Alutop SAS

- Shandong Lipeng Co. Ltd

- Idea Cap SRL

- Easy Open Lid Industry Corp.(Yiwu)

- RPC Group(PET Power)

第7章 市場機會與未來展望

The aluminium caps and closures market is expected to grow from USD 7.40 billion in 2025 to USD 7.65 billion in 2026 and is forecast to reach USD 9.02 billion by 2031 at 3.34% CAGR over 2026-2031.

Demand growth is paced, not explosive, because penetration in core beverage segments is mature; however, upgrades in premium spirits, biologics packaging, and EU sustainability rules continue to open profitable niches. Mandatory tethered-cap regulations in Europe, recycled-aluminium incentives in China, and a shift toward premium ready-to-drink offerings in North America are prompting brand owners to redesign closures with higher functional and aesthetic value. Volatility in London Metal Exchange (LME) pricing tightens converter margins, yet the push for infinitely recyclable materials still tilts preference toward aluminium over cork, steel, or plastic. Regional cost advantages particularly additional recycled capacity in Asia-Pacific are helping offset raw-material swings while keeping premium segments insulated from low-cost PET alternatives.

Global Aluminum Caps And Closures Market Trends and Insights

Rise of Premium RTD-Cocktail Aluminium Bottling in North America

Premium ready-to-drink cocktail brands introduced aluminium bottles throughout 2024 to signal upscale positioning while retaining recyclability. Several brands recorded 40-60% price premiums versus conventional cans, indicating consumers value tactile rigidity and re-close functionality. The barrier performance of aluminium protects botanical extracts from UV light and oxygen, supporting shelf life for spirit-based formulations. Brand collaborations with environmental non-profits reinforce sustainable credentials, creating a marketing halo that smaller steel or PET formats cannot match. The phenomenon is spilling into European travel-retail channels where single-serve spirits require tamper-evident yet elegant closures.

Mandatory Transition to Tethered Caps in EU Beverage Packaging (Directive 2019/904)

Since July 2024, EU beverage bottles must feature tethered closures, sparking redesign activity across carbonated soft drink and water segments.Early consumer pushback against plastic tethered systems led premium water and juice brands to adopt aluminium screw-top variants with integrated hinge mechanisms. Because aluminium is infinitely recyclable and easily detached in material-recovery facilities, brand owners meet both tethered-cap rules and forthcoming 90% metal-collection targets. Multinationals are harmonizing pack formats across non-EU markets to avoid line-change complexity, magnifying near-term demand for value-added aluminium closures.

Volatile LME Aluminium Prices Compressing Converter Margins

Aluminium ingot reached USD 2,662 per ton in February 2025, swinging more than 15% within six months and squeezing converters that sell on long-term fixed contracts. Smaller closure firms without hedging programs face eroded margins, making them attractive acquisition targets for multinationals with advanced risk-management desks. Russian export uncertainty, elevated European smelting power costs, and new US container duties all amplify volatility. To stabilize supply, leading converters raise recycled content and explore alloy recipes with higher scrap tolerance, an approach aligned with carbon-reduction pledges yet requiring capital spend on upgraded annealing furnaces.

Other drivers and restraints analyzed in the detailed report include:

- Beverage-Grade Recycled Aluminium Capacity Expansions in China

- Pharma Shift to Flip-Off Tear-Down Aluminium Seals for Biologics

- Brand-Owner Switch to PET Tethered Caps in Carbonated Soft Drinks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Screw caps retained dominance with 50.74% share in 2025 as they span beverages, condiments, and pharmaceuticals. That share equals USD 3.75 billion of the aluminium caps and closures market size in 2025, reflecting their proven sealing reliability. Easy-open ends, while smaller, are gaining fastest at a 6.38% CAGR through 2031 as consumers gravitate toward convenience features in canned coffee and ready meals. Continuous-thread ROPP variants secure traction in craft spirits because they reconcile tamper evidence with luxury visual cues. Crown corks hold relevance in traditional beer packaging, yet their growth is modest given the migration toward full-body slim cans. Lug, press-twist, and specialized flip-off designs serve tamper-sensitive food and pharma uses, illustrating the segmentation's shift from generalist to application-specific solutions.

Investment is flowing into die-cutting and scoring technologies that create safer, finger-friendly easy-open tabs, unlocking new mass channels like senior-nutrition beverages. Closure makers are also integrating laser-etched QR codes for trace-and-trace compliance without compromising decoration space. These embellishments carry higher unit economics, cushioning margins when raw-material costs rise. In contrast, standard screw-cap formats face commoditization, pressing manufacturers to differentiate through liner chemistry improvements that extend shelf life in aggressive-pH drinks.

Beverages commanded 46.02% share in 2025, equivalent to USD 3.41 billion of the aluminium caps and closures market. The segment covers still water, carbonated drinks, beer, wine, and premium spirits, each with nuanced closure needs. Premium alcohol producers elevate aluminium as a branding canvas, whereas carbonated soft-drink fillers chase lowest cost compliance to EU tethering. Pharmaceutical demand is expanding at a 6.76% CAGR, adding USD 284 million incremental value by 2031. Growth rests on biologic drug launches that specify flip-off tear-down seals to ensure sterile integrity. Food applications remain steady, propelled by gourmet oils and sauces pursuing metal lug caps for smooth pour control. Personal-care brands leverage aluminium's recyclability story to displace mixed-material lids, evidenced by high-profile deodorant launches in recyclable aluminium aerosols.

Cross-sector learning accelerates innovation: beverage can suppliers partner with personal-care companies to adapt internal varnishes for lotion compatibility, broadening addressable markets. Industrial chemical closures, though niche, benefit from aluminium's corrosion resistance when combined with specialty liners. The versatility across end-uses supports balanced portfolio exposure, hedging against cyclical dips in any one sector.

Aluminum Caps and Closures Market is Segmented by Cap Type (Screw Caps, Crown Cork, Lugs/Press Twist, and More), Application (Beverages, Food, Pharmaceutical, Cosmetics and Personal Care, and More), Neck Finish Diameter ( Less Than and Equal To 20mm, 21-30mm, and More), Distribution Channel (Direct Sales Channels, and Indirect Sales Channels) and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific anchored 40.20% of global revenue in 2025, driven by China's prolific beverage output and India's packaged-goods expansion. Cost competitiveness improved after November 2024 when China abolished tariffs on imported recycled aluminium, enabling mills to supply coil at discounts versus primary metal. Japan and South Korea added a layer of technological sophistication, exporting closure presses and vision-inspection systems regionally. Southeast Asian demand benefitted from urbanization and Western quick-service restaurant chains insisting on tamper-proof lids, stimulating local cap conversion lines. India's standards upgrade mandating QR traceability for edible-oil packs nudged value share toward premium lug caps, attracting foreign joint ventures.

The Middle East and Africa represent the fastest-growing territory, forecast at 6.89% CAGR through 2031. Beverage investments in Nigeria and Kenya, plus desalinated bottled-water capacity in the Gulf, underpin volume. However, limited circular-economy infrastructure tempers aluminium caps and closures market penetration. Egypt's move to establish a dedicated food-grade recycling mill marks progress, yet widespread adoption awaits proof of economically viable collection streams. South Africa's established aluminium smelter base and port connectivity create export opportunities into landlocked neighbors.

Europe, though mature, remains pivotal because regulation steers global specifications. The July 2024 tethered-cap deadline forced fillers to redesign PET and aluminium containers simultaneously, generating engineering consulting revenue for closure specialists. Germany's mechanical-engineering cluster pioneered continuous-thread screw-top machines capable of 600 cpm with integrated torque monitoring, raising performance benchmarks. Italy's design houses customized embossing and color-shift inks for premium spirits, preserving perceived luxury even as closures migrate from cork to aluminium for sustainability reasons.

North America's market rides consumer migration to craft beverages and ready-to-drink cocktails packaged in resealable aluminium bottles. US tariff barriers imposed in April 2025 boosted domestic can-stock production, indirectly supporting closure coil producers by tightening local supply and encouraging reshoring. Mexico, a major beer exporter, toggles between aluminium and steel closure options to balance cost and supply risk, yet aluminium retains a foothold in premium bottle lines destined for European customers. South America, led by Brazil, invests in new beverage can lines that include in-house closure modules, shortening lead times.

- Amcor plc

- Crown Holdings Inc.

- Silgan Holdings Inc.

- Guala Closures S.p.A

- Tecnocap Group

- Pelliconi and C. SpA

- Nippon Closures Co. Ltd

- Closure Systems International (CSI)

- Berlin Packaging LLC

- Bericap GmbH

- AptarGroup Inc.

- SKS Bottle and Packaging Inc.

- Hicap Closures Co. Ltd

- Federfin Tech SRL

- Rauh GmbH & Co.

- O.Berk Company

- The Cary Company

- Alutop SAS

- Shandong Lipeng Co. Ltd

- Idea Cap SRL

- Easy Open Lid Industry Corp. (Yiwu)

- RPC Group (PET Power)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise of Premium RTD-Cocktail Aluminium Bottling in North America

- 4.2.2 Mandatory Transition to Tethered Caps in EU Beverage Packaging (Directive 2019/904)

- 4.2.3 Beverage-Grade Recycled Aluminium Capacity Expansions in China

- 4.2.4 Pharma Shift to Flip-Off Tear-Down Aluminium Seals for Biologics

- 4.2.5 Craft Spirits Migration from Cork to Aluminium ROPP in Europe

- 4.2.6 E-commerce Leakage-Testing Protocols Driving Lug Cap Adoption in India

- 4.3 Market Restraints

- 4.3.1 Volatile LME Aluminium Prices Compressing Converter Margins

- 4.3.2 Brand-Owner Switch to PET Tethered Caps in Carbonated Soft Drinks

- 4.3.3 Tin-Free Steel Crown Cork Substitution in Mexican Beer

- 4.3.4 Limited Food-Grade Recycling Streams in Middle East

- 4.4 Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Cap Type

- 5.1.1 Screw Caps

- 5.1.2 Crown Cork

- 5.1.3 Lug / Press-Twist

- 5.1.4 Easy-Open End

- 5.1.5 Roll-On Pilfer Proof (ROPP)

- 5.1.6 Others (Flip-Off, Tear-Down)

- 5.2 By Application

- 5.2.1 Beverages

- 5.2.1.1 Alcoholic Beverages

- 5.2.1.2 Non-Alcoholic Beverages

- 5.2.2 Food

- 5.2.3 Pharmaceutical

- 5.2.4 Cosmetics and Personal Care

- 5.2.5 Industrial and Household Chemicals

- 5.2.1 Beverages

- 5.3 By Neck Finish Diameter

- 5.3.1 Less than and Equal to 20 mm

- 5.3.2 21-30 mm

- 5.3.3 31-40 mm

- 5.3.4 More than 40 mm

- 5.4 By Distribution Channels

- 5.4.1 Direct Sales Channels

- 5.4.2 Indirect Sales Channels

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 France

- 5.5.2.3 Italy

- 5.5.2.4 United Kingdom

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 GCC

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Kenya

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Amcor plc

- 6.4.2 Crown Holdings Inc.

- 6.4.3 Silgan Holdings Inc.

- 6.4.4 Guala Closures S.p.A

- 6.4.5 Tecnocap Group

- 6.4.6 Pelliconi and C. SpA

- 6.4.7 Nippon Closures Co. Ltd

- 6.4.8 Closure Systems International (CSI)

- 6.4.9 Berlin Packaging LLC

- 6.4.10 Bericap GmbH

- 6.4.11 AptarGroup Inc.

- 6.4.12 SKS Bottle and Packaging Inc.

- 6.4.13 Hicap Closures Co. Ltd

- 6.4.14 Federfin Tech SRL

- 6.4.15 Rauh GmbH & Co.

- 6.4.16 O.Berk Company

- 6.4.17 The Cary Company

- 6.4.18 Alutop SAS

- 6.4.19 Shandong Lipeng Co. Ltd

- 6.4.20 Idea Cap SRL

- 6.4.21 Easy Open Lid Industry Corp. (Yiwu)

- 6.4.22 RPC Group (PET Power)

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment