|

市場調查報告書

商品編碼

1940614

重晶石:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Barite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

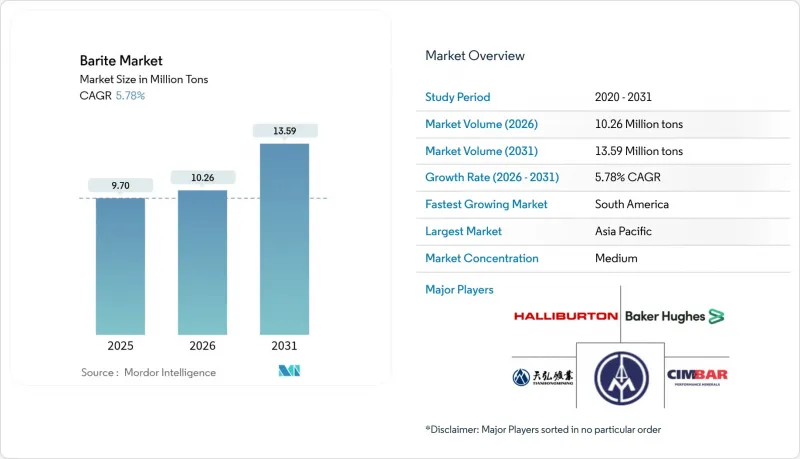

預計重晶石市場將從 2025 年的 970 萬噸成長到 2026 年的 1,026 萬噸,到 2031 年將達到 1,359 萬噸,2026 年至 2031 年的複合年成長率為 5.78%。

油田服務供應商的強勁採購支撐了需求,他們消耗了約80%的鑽井量,而超深水和高壓井的新海上鑽井計劃也推動了需求成長。包括中國和印度在內的主要產油國收緊出口限制,加強了價格紀律,並促使鑽井承包商對沖庫存。醫療影像、塗料和聚合物複合等細分領域需求的快速成長進一步增強了成長韌性,這些領域在石油鑽井活動放緩時會吸收高品質的硫酸鋇。此外,工程鑽井液的持續進步,從細分散高比重鑽井液到混合型水基鑽井液,正促使採購轉向高附加價值規格,從而推高每噸的實際價格。因此,競爭程度取決於能否獲得大型穩定的礦床和下游複合技術,而大型垂直一體化的油田服務公司對分散的礦商擁有強大的議價能力。

全球重晶石市場趨勢與洞察

拉丁美洲深水、高壓、高溫鑽井熱潮

巴西、墨西哥和圭亞那的超深水計劃需要能夠承受2500公尺水深和超過200 度C井底溫度的鑽井液。由於需要更高的泥漿比重來控制地層壓力,這些井消耗的重晶石比標準陸上計劃更多。 SLB為伍德賽德公司Trion油田提供的18口井專案體現了這種需求,並預示著重晶石的懸浮穩定性將轉向細粒重晶石(10微米或更小)。巴西的鹽層下叢集和阿根廷的瓦卡穆爾塔頁岩正在吸引基礎設施建設資金,並擴大區域高等級礦石的倉儲和破碎能力。政府為實現關鍵礦產供應鏈本地化而獎勵進一步增強了需求前景。這些因素共同作用,使拉丁美洲成為全球重晶石市場的中期成長區域,並支撐了高比重品位重晶石的溢價。

北美傳統型油氣資源的崛起

儘管鑽機數量保持穩定,頁岩油氣業者仍在不斷延長井身長度並提高壓裂段密度,以增加單井的加重劑消耗量。隨著主要油田的枯竭,開採活動正轉向二線油田。這些油田的壓力窗口更高,需要更高重力的泥漿。哈里伯頓的BaraHib和貝克休斯的PERFORMAX水基系統已證明,通過將重晶石含量提高15-20%,即可在保持與油基泥漿相當的性能的同時,達到與油基泥漿相當的重力水平。儘管資本支出受到限制,Liberty Energy公司2025年第二季的完井收入達到10.42億美元,顯示其頁岩油氣相關業務的規模仍然龐大。為此,供應鏈正在西德克薩斯和落基山脈地區增設鐵路連接的轉運碼頭,以縮短前置作業時間,並在市場上建立永續的重晶石需求基準。

合成赤鐵礦漿替代品

鐵基加重劑,例如赤鐵礦和鈦鐵礦,比重可達4.95至5.10,從而在保持相近密度的前提下,降低漿料黏度。法赫德國王大學的研究表明,在油基漿料中以鈦鐵礦取代40%的重晶石,可實現零沉降,並顯著改善流變性和電穩定性。領先的服務公司正積極開展研發項目,旨在開發複雜的加重劑混合物,以應對重晶石短缺的問題。在具備本地鐵礦石加工能力的地區(尤其是加拿大和斯堪地那維亞),隨著成本競爭力的提升,重晶石的市場佔有率正在萎縮。此外,由於赤鐵礦重金屬浸出物含量低,環境監管機構也傾向於使用赤鐵礦,這可能會加速在生態敏感地區進行替代。

細分市場分析

截至2025年,層狀礦床將佔全球產量的74.65%,體現了其規模經濟和穩定的礦石品質。該領域的主導地位得益於長期合約的穩定性,尤其是中國貴州省的生產商和印度安得拉邦的礦業公司,它們為重晶石市場的物流基礎設施提供了支持。殘餘礦床雖然規模較小,但成長速度最快,年複合成長率達6.03%,因為較高的固有品位降低了選礦成本。巴基斯坦的胡茲達爾礦區(由博蘭礦業企業營運)就是一個很好的例子,它展示了規模小規模的礦場如何透過供應比重高於4.30的高等級礦石來保持競爭力,以滿足高階應用的需求。因此,地理因素決定了風險/回報的權衡:亞洲的層狀礦山滿足了大批量採礦需求,而脈狀礦床和殘餘礦床則佔據了塗料和醫療應用等利基市場。

即使是規模較大的層狀礦場也面臨品位波動,需要經過多道分選工序才能達到API 13A標準。資本預算正被分配到高密度分選迴路、磁選和光學分選等領域,從而提高了固定成本的槓桿作用。在重晶石市場,擁有規模優勢和靈活加工方案以滿足跨領域訂單需求的營運商將獲得競爭優勢。同時,摩洛哥和內華達州的脈狀礦床供應小批量、高純度應用,且受鑽探週期相關的價格波動影響較小。大規模礦床開採和專業脈狀礦床供應商的共存增強了供應韌性,並有助於維持長期需求穩定。

重晶石市場報告按礦床類型(層狀、脈狀/空腔狀、殘餘狀)、終端用途行業(石油天然氣、化學、填料、醫療診斷及其他)和地區(亞太、北美、歐洲、南美、中東和非洲)進行細分。市場預測以噸為單位。

區域分析

到2025年,亞太地區佔全球噸位的41.35%,主要得益於中國和印度的貢獻。深圳、防城和維沙卡帕特南等港口強大的海運物流網路促進了對環太平洋地區的出口。 2025年3月實施的政策主導價格上漲(每噸人民幣200元)進一步印證了該地區的價格影響力。南美洲的成長率最高,達5.98%,這主要得益於巴西鹽鹽層下投資和阿根廷頁岩氣開發在國內供應有限的情況下提振了進口需求。

北美約三分之二的需求依賴進口,主要透過鐵路貨運站向二疊紀盆地和海恩斯維爾盆地供應礦石。歐洲仍依賴進口,而更嚴格的重金屬含量分類標準促使買家優先選擇來自摩洛哥和土耳其的高品位礦石。中東和非洲地區受益於靠近大型礦區的優勢,但缺乏大規模採礦能力,因此依賴從印度和中國進口礦石。在澳大利亞,近海鑽探前景的黯淡抑制了該地區的需求,但對關鍵礦產的關注可能會推動當地高品位礦石的生產。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 拉丁美洲深水、高壓、高溫鑽井的快速成長佔主導地位

- 北美傳統型油氣資源的崛起

- 基礎設施獎勵策略在印度油田服務業中成為主流

- 高比重重晶石因能減少滑石粉用量而備受關注。

- 重晶石-聚合物複合材料在3D列印耗材中的應用正日益受到關注。

- 市場限制

- 合成赤鐵礦泥漿置換法是主流方法。

- 與石油相關的鑽探預算波動已成為主流

- 滲透性法規限制了填充材的等級

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 價格概覽

- 貿易概覽

第5章 市場規模與成長預測

- 按礦床類型

- 分層

- 靜脈和空腔填充物

- 殘留物

- 按最終用途行業分類

- 石油和天然氣

- 化學品(鋇鹽)

- 填料(油漆、塑膠、橡膠)

- 醫療/診斷

- 其他(輻射屏蔽、3D列印)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 土耳其

- 俄羅斯

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 埃及

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Andhra Pradesh Mineral Development Corporation(APMDC)

- Ashapura Group

- Baker Hughes Inc.

- Baribright Co. Ltd.

- Bracco

- Cimbar Performance Minerals

- Desku Group Inc.

- Guizhou Saboman Import & Export Co. Ltd.

- Guizhou Tianhong Mining Co.

- Halliburton Energy Services Inc.

- International Earth Products LLC

- Luhua Group

- New Riverside Ochre

- Newpark Resources Inc.

- Pulapathuri

- PVS Global Trade Private Limited

- Sachtleben Minerals GmbH & Co. KG

- Schlumberger Limited

- Shaanxi Fuhua Chemical Co., Ltd.

- The Kish Company Inc.

- Zhongrun Barium Industry Co. Ltd.

第7章 市場機會與未來展望

The Barite market is expected to grow from 9.70 million tons in 2025 to 10.26 million tons in 2026 and is forecast to reach 13.59 million tons by 2031 at 5.78% CAGR over 2026-2031.

Strong purchasing by oilfield service operators, who consume nearly 80% of all mined tonnage, anchors demand, while fresh offshore campaigns in ultra-deepwater and high-pressure wells amplify volume growth. Tight export policies from leading producers, especially China and India, have elevated price discipline and encouraged inventory hedging among drilling contractors. Growth resilience is further supported by rapid gains in medical imaging, coatings, and polymer compounding, niches that absorb premium-grade barium sulfate when crude-linked drilling activity moderates. Ongoing advances in engineered drilling fluids-ranging from micronized high-gravity grades to hybrid water-based systems-are shifting procurement toward value-added specifications that translate into higher realized prices per metric ton. Competitive dynamics, therefore, hinge on access to large, consistent ore bodies and on downstream formulation know-how, with vertically integrated oilfield service majors wielding notable bargaining power over fragmented miners.

Global Barite Market Trends and Insights

Booming Deep-Water and HPHT Drilling in Latin America

Ultra-deepwater projects in Brazil, Mexico, and Guyana now require drilling fluids that can withstand water depths of 2,500 m and bottom-hole temperatures exceeding 200 °C. Each such well consumes more barite than standard onshore programs because a higher mud weight is necessary to control formation pressures. SLB's USD 18-well package for Woodside's Trion field illustrates this intensity and showcases a shift to micronized barite below 10 µm for superior suspension stability. Brazil's pre-salt cluster and Argentina's Vaca Muerta shale simultaneously attract infrastructure capital, expanding regional warehousing and grinding capacity for high-grade ore. Government incentives to localize critical mineral supply chains further reinforce the outlook for demand. Together, these forces contribute to the mid-term growth of Latin America in the global barite market and underpin premium pricing for high-gravity grades.

Rise of Unconventional Hydrocarbons in North America

Shale operators continue to lengthen laterals and densify stage counts, actions that increase per-well weighting-agent consumption even as rig numbers remain flat. Top-tier acreage depletes, prompting activity to shift to Tier 2 locales that exhibit higher pressure windows and therefore require heavier muds. Halliburton's BaraHib and Baker Hughes' PERFORMAX water-based systems demonstrate how operators can replicate the performance of oil-based mud while increasing barite loading by 15-20% to achieve the same density. Despite disciplined capital spending, Q2 2025 completion revenue of USD 1.042 billion at Liberty Energy confirms the scale of ongoing shale work. Supply chains respond by building more rail-served transload terminals in West Texas and the Rockies to shorten lead times, thereby establishing a sustainable baseline demand in the barite market.

Synthetic Hematite Mud Substitutes

Iron-oxide weighting agents such as hematite and ilmenite reach SG values of 4.95-5.10, enabling thinner muds at equivalent densities. Academic work from King Fahd University documented zero sag when 40% barite was replaced with ilmenite in oil-based fluids, while rheology and electrical stability both improved. Service majors have responded with research and development programs aimed at composite weighting blends that hedge against barite scarcity. Cost competitiveness improves where iron-ore processing is local, notably in Canada and Scandinavia, shrinking barite's addressable share in such basins. Environmental regulators also view hematite favorably due to lower heavy-metal leachate, a factor that could accelerate substitution in ecologically sensitive regions.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure Stimulus in India's Oilfield Services

- Use of Barite-Polymer Composites in 3-D Printing Filaments

- Volatility in Crude-Linked Drilling Budgets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bedded deposits supplied 74.65% of global tonnage in 2025, reflecting economies of scale and consistent ore quality. The segment's dominance translates into secure long-cycle contracts, notably for Chinese producers in Guizhou and Indian miners in Andhra Pradesh, who together anchor the logistics backbone of the barite market. Residual deposits, although smaller, exhibit the quickest expansion at a 6.03% CAGR, as higher intrinsic grades lower beneficiation costs. Pakistan's Khuzdar vein systems, managed by Bolan Mining Enterprises, illustrate how smaller operations sustain competitiveness by targeting more than 4.30 SG ore for premium applications. Geography, therefore, shapes the risk-return calculus: Asian bedded miners cater to bulk drilling demand, whereas vein and residual sources capture niches in the coatings and medical arenas.

Despite their share supremacy, bedded mines still navigate grade variability that mandates multiple cleaning stages to meet API 13A standards. Capital budgets thus flow to densification circuits, magnetic separation, and optical sorting, lifting fixed-cost leverage. The barite market, hence, rewards operators who marry scale with flexible processing menus that accommodate cross-segment orders. Meanwhile, vein deposits in Morocco and Nevada channel smaller volumes into high-purity end-uses, insulating them from price swings tied to drilling cycles. The coexistence of large-scale bedded operations and specialized vein suppliers enhances supply resiliency and underpins long-term demand coverage.

The Barite Market Report is Segmented by Deposit Type (Bedded, Vein and Cavity Filling, and Residual), End-Use Industry (Oil and Gas, Chemical, Fillers, Medical and Diagnostics, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

The Asia-Pacific region captured 41.35% of global tonnage in 2025, driven primarily by the contributions of China and India. Robust seaborne logistics via Shenzhen, Fangcheng, and Visakhapatnam facilitate exports across the Pacific Rim. Policy-driven price hikes of CNY 200 per ton, enacted in March 2025, underscore the region's pricing influence. South America posted the fastest growth at 5.98%, as Brazil's pre-salt investments and Argentina's shale build-out drive up import demand, given the limited indigenous supply.

North America imports roughly two-thirds of its requirement, relying on rail-fed terminals to feed the Permian and Haynesville plays. Europe remains import-dependent and increasingly selective on heavy-metal content, nudging buyers toward high-purity Moroccan and Turkish ore. The Middle East and Africa benefit from proximity to super-giant oil fields but lack sizable mining capacity, prompting the import of inbound cargoes from India and China. Australia's declining offshore drilling outlook tempers regional offtake, yet its focus on critical minerals may catalyze localized high-purity production.

- Andhra Pradesh Mineral Development Corporation (APMDC)

- Ashapura Group

- Baker Hughes Inc.

- Baribright Co. Ltd.

- Bracco

- Cimbar Performance Minerals

- Desku Group Inc.

- Guizhou Saboman Import & Export Co. Ltd.

- Guizhou Tianhong Mining Co.

- Halliburton Energy Services Inc.

- International Earth Products LLC

- Luhua Group

- New Riverside Ochre

- Newpark Resources Inc.

- Pulapathuri

- PVS Global Trade Private Limited

- Sachtleben Minerals GmbH & Co. KG

- Schlumberger Limited

- Shaanxi Fuhua Chemical Co., Ltd.

- The Kish Company Inc.

- Zhongrun Barium Industry Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Booming deep-water and HPHT drilling in Latin America mainstream

- 4.2.2 Rise of unconventional hydrocarbons in North America mainstream

- 4.2.3 Infrastructure stimulus in India's oilfield services mainstream

- 4.2.4 High-gravity barite grades enabling lower mud volumes under-radar

- 4.2.5 Use of barite-polymer composites in 3-D printing filaments under-radar

- 4.3 Market Restraints

- 4.3.1 Synthetic hematite mud substitutes mainstream

- 4.3.2 Volatility in crude-linked drilling budgets mainstream

- 4.3.3 Radio-opacity regulations curbing filler grades under-radar

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Pricing Overview

- 4.7 Trade Overview

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Deposit Type

- 5.1.1 Bedded

- 5.1.2 Vein and Cavity Filling

- 5.1.3 Residual

- 5.2 By End-use Industry

- 5.2.1 Oil and Gas

- 5.2.2 Chemical (Barium Salts)

- 5.2.3 Fillers (Paints, Plastics, Rubber)

- 5.2.4 Medical and Diagnostics

- 5.2.5 Others (Radiation Shielding, 3-D Printing)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Nordic Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 South Africa

- 5.3.5.6 Nigeria

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Andhra Pradesh Mineral Development Corporation (APMDC)

- 6.4.2 Ashapura Group

- 6.4.3 Baker Hughes Inc.

- 6.4.4 Baribright Co. Ltd.

- 6.4.5 Bracco

- 6.4.6 Cimbar Performance Minerals

- 6.4.7 Desku Group Inc.

- 6.4.8 Guizhou Saboman Import & Export Co. Ltd.

- 6.4.9 Guizhou Tianhong Mining Co.

- 6.4.10 Halliburton Energy Services Inc.

- 6.4.11 International Earth Products LLC

- 6.4.12 Luhua Group

- 6.4.13 New Riverside Ochre

- 6.4.14 Newpark Resources Inc.

- 6.4.15 Pulapathuri

- 6.4.16 PVS Global Trade Private Limited

- 6.4.17 Sachtleben Minerals GmbH & Co. KG

- 6.4.18 Schlumberger Limited

- 6.4.19 Shaanxi Fuhua Chemical Co., Ltd.

- 6.4.20 The Kish Company Inc.

- 6.4.21 Zhongrun Barium Industry Co. Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

重晶石市場:依等級、顏色、用途、地區分類

重晶石市場:依等級、顏色、用途、地區分類 重晶石市場:按類型、形態、等級、分銷管道、應用和最終用戶分類-2026-2032年全球市場預測

重晶石市場:按類型、形態、等級、分銷管道、應用和最終用戶分類-2026-2032年全球市場預測 重晶石市場規模、佔有率、趨勢和預測:按等級、應用和地區分類,2026-2034年

重晶石市場規模、佔有率、趨勢和預測:按等級、應用和地區分類,2026-2034年 重晶石市場規模、佔有率、成長及全球產業分析:按類型和應用分類,區域洞察及2026-2034年預測

重晶石市場規模、佔有率、成長及全球產業分析:按類型和應用分類,區域洞察及2026-2034年預測 重晶石市場規模、佔有率和趨勢分析報告:按應用、地區和細分市場預測(2026-2033 年)2026-2034年全球重晶石市場規模、佔有率、趨勢和成長分析報告

重晶石市場規模、佔有率和趨勢分析報告:按應用、地區和細分市場預測(2026-2033 年)2026-2034年全球重晶石市場規模、佔有率、趨勢和成長分析報告 全球重晶石市場2026-2030日本重晶石市場規模、佔有率、趨勢和預測:按等級、應用和地區分類,2026-2034年

全球重晶石市場2026-2030日本重晶石市場規模、佔有率、趨勢和預測:按等級、應用和地區分類,2026-2034年 2026年全球重晶石市場報告

2026年全球重晶石市場報告 重晶石市場機會、成長要素、產業趨勢分析及2026年至2035年預測

重晶石市場機會、成長要素、產業趨勢分析及2026年至2035年預測