|

市場調查報告書

商品編碼

1940591

蜂蠟:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Beeswax - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

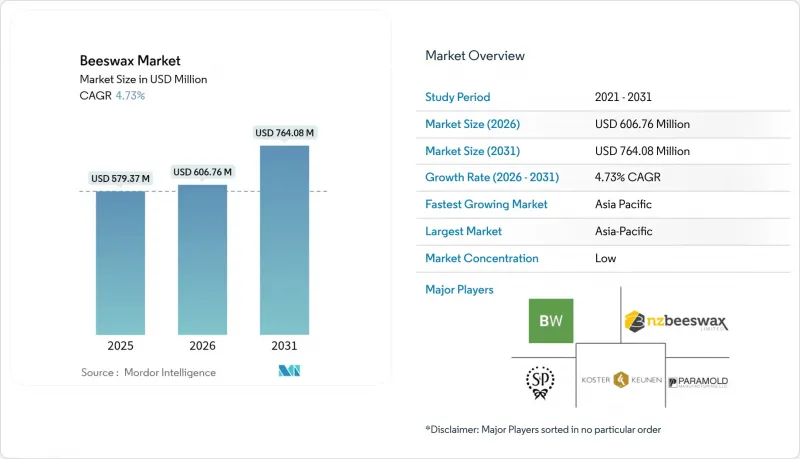

2025年全球蜂蠟市場價值為5.7937億美元,預計到2031年將達到7.6408億美元,高於2026年的6.0676億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 4.73%。

市場擴張的主要驅動力是蜂蠟在化妝品配方、藥品和天然食品塗層等領域的應用日益廣泛,這主要是由於製造商積極響應不斷變化的成分透明度監管要求。亞太地區在蜂蠟的生產和消費方面均保持主導地位,其中印度貢獻巨大,年產量達100萬公斤。同時,成熟市場透過提供符合嚴格品質標準(包括殘留限量和產品真實性)的認證蜂蠟產品,獲得了更高的收益。雖然合成蠟替代品已經出現,並具有品質穩定、污染風險低等優勢,但天然蜂蠟憑藉其監管優勢和廣泛的消費者認可度,尤其是在高價值產品應用領域,仍然保持著強勁的市場地位。

全球蜂蠟市場趨勢及展望

化妝品和個人護理產品對天然/有機成分的需求日益成長

化妝品行業向天然成分的根本性轉變,使蜂蠟作為一種乳化劑和質地改良劑,尤其是在唇部護理和防護屏障配方中,佔據了高階地位。為了回應市場需求,各大化工企業正在加強其天然成分產品組合,例如路博潤公司推出的Carbopols Biosens和BASF公司推出的玉米衍生成膜劑Verdescens Maize。蜂蠟憑藉其全面的功能性,兼具乳化能力、成膜性能以及經證實對金黃色葡萄球菌和白色念珠菌的抗菌功效,從而展現出巨大的價值。這些特性直接滿足了配方師對成分整合日益成長的需求,同時也支持了潔淨標示概念。監管方面的優勢也進一步鞏固了蜂蠟的市場地位,由於其已獲得美國FDA的GRAS認證(21 CFR 184.1973)和歐盟食品添加劑核准(E-901),因此可以無縫應用於化妝品和食品接觸領域。

護膚和化妝品領域的清潔美容和透明度趨勢

消費者對個人保健產品成分透明度的日益關注和需求顯著提升了蜂蠟的市場地位。作為一種天然成分,蜂蠟擁有完善的安全性記錄和數百年的傳統應用歷史,完美契合了當前消費者的偏好。日益興起的「清潔美容」運動強調可生物分解和無毒配方,促使製造商逐漸拋棄石油基替代品,蜂蠟的使用量也顯著增加。隨著監管機構為應對日益嚴重的環境問題(尤其是微塑膠問題)而對合成聚合物實施更嚴格的管控,這項轉變正在加速。化妝品級蜂蠟(每盎司2美元)和蠟燭級蜂蠟(每盎司1.25美元)之間出現了明顯的價格差距,這反映了化妝品應用對品質和純度的嚴格要求。現代法規結構正在不斷發展,要求全面披露成分資訊並提供永續性證明,這為蜂蠟等成熟的天然成分創造了有利的環境。同時,新的合成替代品則面臨著漫長而高成本的安全檢驗流程。

受環境和天氣因素影響,原料供應出現波動

氣候變遷導致的蜂群損失正對全球蜂蠟供應鏈產生重大影響。拉丁美洲的綜合研究揭示了令人震驚的蜂群年死亡率,墨西哥高達16.2%,哥倫比亞則高達47.7%。包括自然棲息地持續喪失、季節性開花模式紊亂以及極端天氣事件頻繁在內的多重環境挑戰,正顯著降低蜂群的生產力和蜂蠟產量。蜂蠟的生產過程特別敏感,工蜂在關鍵的12-18天蜂蠟分泌期內需要精確的環境條件。全球蜂群面臨的最主要生物威脅仍然是蜜蜂跳蚤(瓦蟎)的侵擾,嚴重的蟲害會顯著降低蜂群的存活率和蜂蠟的累積。這種供應的不確定性導致市場對穩定、高品質的蜂蠟需求旺盛,迫使價格敏感的生產商轉向合成替代品。儘管監管機構日益關注供應鏈的透明度和韌性,但與蜂蜜市場相比,蜂蠟產業仍然缺乏全面的品質標準。

細分市場分析

受消費者對天然和可生物分解成分需求不斷成長的推動,天然蜂蠟預計到2025年將繼續佔據市場主導地位,市場佔有率將達到84.65%。此外,天然蜂蠟已獲得包括食品、化妝品和製藥等多個行業的監管部門批准,進一步鞏固了其市場核准。在這些產業中,產品安全性和天然來源至關重要。

合成蠟市場正以5.70%的複合年成長率強勁成長,這主要得益於其穩定的供應能力以及對敏感應用無污染的特性。費托合成蠟,尤其是沙索公司產品系列中的佼佼者,在石蠟、微晶蠟和合成硬蠟等多種類型中均展現出優異的熱穩定性和可調熔點。這些產品廣泛應用於從化妝品到工業塗料等各個行業。合成蠟市場不受農業和氣候變遷因素的影響,從而避免了天然蜂蠟市場面臨的供應鏈不確定性。合成蠟生產商能夠精確控制成分,確保產品不含農藥殘留,這使其在對純度要求極高的醫藥和食品接觸應用中尤為重要。

區域分析

亞太地區目前佔全球蜂蠟市場最大佔有率,預計2025年將達到37.84%。這一主導地位主要歸功於印度,它是世界上最大的蜂蠟生產國,每年產量達2,460萬公斤。中國已成為一個重要的消費市場,但準確的產量數據仍難以取得。日本對進口的依賴程度很高,蜂蜜自給率僅6%,而且該國需要大量進口蜂蠟用於各種工業用途。

該地區的年複合成長率高達5.24%,遠超其他所有區域市場。韓國380萬公斤的大規模產能支撐了這一加速成長,鞏固了其作為世界第五大蜂蠟生產國的地位。然而,近期美國對韓國美容產品出口徵收的關稅壓力,改變了含蜂蠟化妝品配方的需求格局,這可能會影響未來的成長率。

北美和歐洲市場仍然成熟,法規結構完善,消費者也願意為天然成分支付溢價。雖然美國市場對蜂箱進口和牲畜飼料用途有所限制,但可以透過美國動植物衛生檢驗局(APHIS)核准的精煉蜂蠟出口途徑出口到歐盟。歐洲市場著重永續性和污染監測,並制定了具體的進口通訊協定,例如英國的第三類物質標準。在南美洲,阿根廷(500萬公斤)和巴西(180萬公斤)是主要的生產國,但面臨高達16.2%至47.7%的蜂群損失率。非洲擁有悠久的養蜂傳統,但技術和市場進入的限制使其產量未能充分發揮潛力,僅佔全球蜂蠟產量的不到25%。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 化妝品和個人護理產品對天然和有機成分的需求日益成長

- 護膚和化妝品領域的清潔美容和透明度趨勢

- 在製藥領域,尤其是在軟膏和藥膏中的應用日益廣泛

- 不含致敏物質、無毒的食品添加物和塗層的需求

- 手工製品和傳統工藝品的受歡迎程度。

- 蜂蠟精煉加工的技術進步

- 市場限制

- 受環境和天氣條件影響,原料供應出現波動。

- 全球食品和藥品成分監管日益收緊

- 農產品中農藥污染及殘留風險

- 養蜂業對勞動力和專業知識要求很高

- 供應鏈分析

- 監理展望

- 波特五力模型

- 新進入者的威脅

- 買方和消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依產品類型

- 自然的

- 合成

- 按形式

- 堵塞

- 顆粒/片劑

- 片狀/珠狀

- 透過使用

- 化妝品

- 製藥

- 其他用途

- 按地區

- 北美洲

- 美國

- 墨西哥

- 北美其他地區

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 澳洲

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市場排名分析

- 公司簡介

- Koster Keunen Inc.

- Strahl & Pitsch Inc.

- British Wax Refining Co. Ltd.

- New Zealand Beeswax Ltd.

- Paramold Manufacturing LLC

- AADRA International

- Melland Ecogreen Technology Co., Ltd.

- Alfa Chemistry

- Beeswax Products Company LLC

- Beeswax-Store.com

- Roger A. Reed Inc.

- Poth Hille & Co. Ltd.

- Seidler Chemical Company

- Frank B. Ross Co. Inc.

- Taiwan San-Ei Oil Co., Ltd.

- Qian Xiao Beeswax Co., Ltd.

- Hase Petroleum Wax Co.

- Bioscope Sdn Bhd

- Tekwax Ltd.

- Thorne Corporation

第7章 市場機會與未來展望

The global beeswax market was valued at USD 579.37 million in 2025 and estimated to grow from USD 606.76 million in 2026 to reach USD 764.08 million by 2031, at a CAGR of 4.73% during the forecast period (2026-2031).

The market expansion is primarily driven by the increased adoption of beeswax in cosmetics formulations, pharmaceutical products, and natural food coatings, as manufacturers respond to evolving regulatory requirements for ingredient transparency. The Asia-Pacific region maintains its position as the dominant force in both production and consumption, with India's substantial contribution of one million kilograms per year. Meanwhile, established markets generate higher revenues through certified beeswax grades that satisfy stringent quality standards for residue limits and product authenticity. Although synthetic wax alternatives are emerging with benefits such as quality consistency and reduced contamination risks, natural beeswax continues to hold a strong market position due to its favorable regulatory status and widespread consumer acceptance, particularly in high-value product applications.

Global Beeswax Market Trends and Insights

Rising Demand for Natural/Organic Ingredients in Cosmetics and Personal Care

The cosmetics industry's fundamental transformation toward natural ingredients has elevated beeswax to a premium status as an emulsifier and texture enhancer, particularly benefiting lip care and protective barrier formulations. In response to market demands, major chemical suppliers have strengthened their natural ingredient portfolios, evidenced by Lubrizol's introduction of Carbopol BioSense and BASF's launch of Verdessense Maize as corn-derived film-formers. Beeswax brings significant value through its comprehensive functional properties, combining emulsification capabilities, film formation characteristics, and proven antimicrobial effectiveness against Staphylococcus aureus and Candida albicans. These attributes directly address formulators' growing requirements for ingredient consolidation while supporting clean-label initiatives. The regulatory framework further reinforces beeswax's market position, with FDA GRAS status (21 CFR 184.1973) and EU food additive approval (E-901) enabling manufacturers to incorporate it seamlessly across both cosmetics and food-contact applications.

Clean Beauty and Transparency Trends in Skincare/Cosmetics

The increasing consumer awareness and demand for ingredient transparency in personal care products has significantly enhanced beeswax's position in the market. As a natural component with well-documented safety records and centuries of traditional use, beeswax aligns perfectly with current consumer preferences. The clean beauty movement, which prioritizes biodegradable and non-toxic formulations, has created a substantial shift toward beeswax as manufacturers move away from petroleum-based alternatives. This transition has gained momentum as regulatory bodies implement stricter controls on synthetic polymers, particularly due to growing environmental concerns about microplastics. The market demonstrates clear price differentiation between cosmetic-grade beeswax, which commands USD 2.00 per ounce, and candle-grade beeswax at USD 1.25 per ounce, reflecting the stringent quality standards and purity requirements for cosmetic applications. Modern regulatory frameworks have evolved to mandate comprehensive ingredient disclosure and sustainability documentation, creating a favorable environment for established natural ingredients like beeswax, while new synthetic alternatives face lengthy and costly safety validation processes.

Fluctuations in Raw Material Supply Due to Environment/Weather

Climate-driven colony losses significantly impact the global beeswax supply chain, as evidenced by comprehensive studies from Latin America that reveal concerning annual colony mortality rates ranging from 16.2% in Mexico to 47.7% in Colombia. Multiple environmental challenges, including the ongoing loss of natural habitats, disruptions in seasonal flowering patterns, and the increasing frequency of extreme weather events, have substantially reduced both colony productivity and wax production capabilities. The process of wax production is particularly sensitive, as worker bees require precise environmental conditions during their critical 12-18 day wax-secretion phase. The Varroa destructor mite infestation continues to pose the most significant biological threat to colonies worldwide, with severe infestations dramatically decreasing both colony survival rates and wax accumulation. These supply uncertainties have created a market environment where premium prices are commanded for consistent, high-quality beeswax, consequently pushing manufacturers in price-sensitive industries toward synthetic alternatives. While regulatory bodies have increased their focus on supply chain transparency and resilience, the industry still lacks comprehensive quality standards compared to the well-established specifications in the honey market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Use in Pharmaceuticals, Especially for Ointments and Salves

- Demand for Allergen-Free, Non-Toxic Food Additives/Coating Agents

- Stringent Global Regulations on Food and Pharma Ingredients

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Natural beeswax continues to dominate the market with an 84.65% share in 2025, as consumers increasingly gravitate toward natural and biodegradable ingredients. This market leadership is further reinforced by well-established regulatory approvals across multiple industries, including food, cosmetic, and pharmaceutical applications, where product safety and natural origin remain paramount considerations.

The synthetic wax segment demonstrates robust growth with a CAGR of 5.70%, primarily due to its ability to deliver consistent supply and contamination-free properties for sensitive applications. Fischer-Tropsch synthetic waxes, particularly notable in Sasol's product portfolio, offer enhanced thermal stability and adjustable melting points across paraffin, microcrystalline, and synthetic hard wax varieties. These products serve diverse industries from cosmetics to industrial coatings. The synthetic segment's independence from agricultural and climatic variables addresses the supply chain uncertainties that affect natural beeswax markets. Manufacturers of synthetic waxes can maintain precise composition control and ensure products free from pesticide residues, making them particularly valuable for pharmaceutical and food-contact applications where stringent purity standards must be met.

The Beewax Market Report is Segmented by Product Type (Natural, and Synthetic), Form (Blocks, Pellets / Pastilles, and Sheets / Beads), Application (Cosmetics, Pharmaceuticals, and Other Applications), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

The Asia-Pacific region currently commands the largest share of the global beeswax market, accounting for 37.84% in 2025. This dominance is primarily attributed to India's position as the world's largest producer, contributing 24.6 million kg annually to the global supply. China has emerged as a significant consumption market, although precise production figures remain unavailable. Japan's heavy reliance on imports, reflected in its mere 6% self-sufficiency in honey production, indicates substantial beeswax import requirements for various industrial applications.

The region's growth trajectory stands at an impressive 5.24% CAGR, outpacing all other geographical segments. This accelerated growth is supported by South Korea's substantial production capacity of 3.8 million kg, positioning it as the fifth-largest global producer. However, recent tariff pressures on Korean beauty exports to the US market have introduced new dynamics in the demand patterns for beeswax-containing cosmetic formulations, potentially influencing future growth rates.

In other regions, North America and Europe maintain their positions as mature markets, characterized by well-established regulatory frameworks and consumer willingness to pay premium prices for natural ingredients. The US market benefits from APHIS-approved refined beeswax export pathways to the EU, despite facing limitations on honeycomb imports and livestock feeding applications. European markets emphasize sustainability and contamination monitoring, with specific import protocols such as the UK's Category 3 material standards. South America contributes significantly through Argentina (5.0 million kg) and Brazil (1.8 million kg), though facing challenges from high colony loss rates ranging from 16.2% to 47.7%. Africa's production remains below its potential, contributing less than 25% of global beeswax output despite its rich beekeeping heritage, primarily due to technological and market access limitations.

- Koster Keunen Inc.

- Strahl & Pitsch Inc.

- British Wax Refining Co. Ltd.

- New Zealand Beeswax Ltd.

- Paramold Manufacturing LLC

- AADRA International

- Melland Ecogreen Technology Co., Ltd.

- Alfa Chemistry

- Beeswax Products Company LLC

- Beeswax-Store.com

- Roger A. Reed Inc.

- Poth Hille & Co. Ltd.

- Seidler Chemical Company

- Frank B. Ross Co. Inc.

- Taiwan San-Ei Oil Co., Ltd.

- Qian Xiao Beeswax Co., Ltd.

- Hase Petroleum Wax Co.

- Bioscope Sdn Bhd

- Tekwax Ltd.

- Thorne Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for natural/organic ingredients in cosmetics and personal care

- 4.2.2 Clean beauty and transparency trends in skincare/cosmetics

- 4.2.3 Growing use in pharmaceuticals, especially for ointments and salves

- 4.2.4 Demand for allergen-free, non-toxic food additives/coating agents

- 4.2.5 Popularity of artisanal, hand-made, and heritage crafts.

- 4.2.6 Technological advancements in beeswax purification/processing

- 4.3 Market Restraints

- 4.3.1 Fluctuations in raw material supply due to environment/weather

- 4.3.2 Stringent global regulations on food and pharma ingredients

- 4.3.3 Pesticide contamination and residue risks in output

- 4.3.4 High labor and expertise requirements in beekeeping

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Natural

- 5.1.2 Synthetic

- 5.2 By Form

- 5.2.1 Blocks

- 5.2.2 Pellets / Pastilles

- 5.2.3 Sheets / Beads

- 5.3 By Application

- 5.3.1 Cosmetics

- 5.3.2 Pharmaceuticals

- 5.3.3 Other Applications

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Mexico

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 Italy

- 5.4.2.4 France

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Australia

- 5.4.3.4 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Koster Keunen Inc.

- 6.4.2 Strahl & Pitsch Inc.

- 6.4.3 British Wax Refining Co. Ltd.

- 6.4.4 New Zealand Beeswax Ltd.

- 6.4.5 Paramold Manufacturing LLC

- 6.4.6 AADRA International

- 6.4.7 Melland Ecogreen Technology Co., Ltd.

- 6.4.8 Alfa Chemistry

- 6.4.9 Beeswax Products Company LLC

- 6.4.10 Beeswax-Store.com

- 6.4.11 Roger A. Reed Inc.

- 6.4.12 Poth Hille & Co. Ltd.

- 6.4.13 Seidler Chemical Company

- 6.4.14 Frank B. Ross Co. Inc.

- 6.4.15 Taiwan San-Ei Oil Co., Ltd.

- 6.4.16 Qian Xiao Beeswax Co., Ltd.

- 6.4.17 Hase Petroleum Wax Co.

- 6.4.18 Bioscope Sdn Bhd

- 6.4.19 Tekwax Ltd.

- 6.4.20 Thorne Corporation