|

市場調查報告書

商品編碼

1940572

美國汽車售後市場零件:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)United States Aftermarket Automotive Parts And Components - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

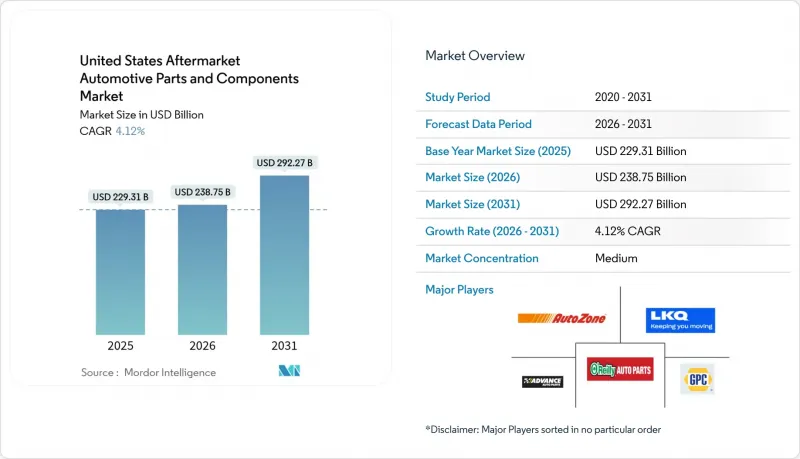

美國汽車售後零件市場預計將從 2025 年的 2,293.1 億美元成長到 2026 年的 2,387.5 億美元,到 2031 年達到 2,922.7 億美元,2026 年至 2031 年的複合年成長率為 4.12%。

推動這一擴張的因素包括車輛平均車齡延長、輕型卡車銷售強勁以及電子商務的快速發展。新車價格上漲、維修權法律的擴大以及疫情後駕駛量的復甦刺激了替換需求,而新興的電動改裝套件則開闢了一個高階專業細分市場。儘管不同零件類別的競爭情況各不相同,但那些將全通路分銷與電子技術專長相結合的供應商正在為持續成長奠定基礎。從美國環保署(EPA)的排放氣體標準到各州的電動車強制令,管理方案既是推動因素也是推動因素,它們透過不斷變化的合規要求重塑著汽車售後零件市場。

美國汽車售後市場零件及組件市場趨勢與洞察

大型SUV和皮卡車的普及帶動了易耗零件收入的成長。

輕型卡車在汽車市場佔據主導地位,預計到2027年將佔據新車銷售的相當大佔有率。與傳統乘用車相比,這些重型車輛的售後市場支出更高,這反映了它們獨特的性能和需求。由於需要牽引和承載重物,構成這些卡車的部件——懸吊、煞車系統和傳動系統部件——必須承受更大的負荷。

越野旅行、拖車和戶外探險等生活方式趨勢正在推動車輛性能升級的需求。愛好者們正在尋找升高套件、重型減震器和更大尺寸的輪胎,以改善駕駛體驗並應對崎嶇地形。皮卡車專用配件市場規模已高達每年160億美元,製造商也為這些多功能車輛提供專門的產品線。

輕型卡車車主往往熱衷於改裝,升級改造的平均交易金額通常超過標準零件更換的費用。這種趨勢不僅提升了卡車的美觀性和功能性,也提高了汽車售後市場零件產業的利潤率,展現出一個蓬勃發展、潛力無限的市場。

電子商務的滲透加速了長尾SKU的供應。

如今,絕大多數汽車售後市場交易都發生在充滿活力的數位管道中,其速度遠遠超過美國整體零售電商的滲透率。這一顯著轉變使得網路商店商店能夠展示專業化的SKU,而無需承擔傳統實體批發商的庫存成本。因此,全國各地都能輕鬆找到老式車款的稀有零件,滿足了愛好者和收藏家的需求。直接出貨和即時庫存數據縮短了DIY愛好者和小規模維修廠的前置作業時間,並將市場力量重新分配給了精通數位技術的供應商。然而,仿冒品仍然是一個嚴重的風險,聯邦執法行動凸顯了品牌保護計畫的重要性。那些將強大的認證技術與方便用戶使用介面相結合的公司正在不斷擴大其在數位售後市場的佔有率。

ADAS降低了對碰撞部件的需求

自動緊急煞車和車道維持系統正在降低事故率,從而減少了對保險桿、擋泥板和車燈的需求。事故頻率的下降在新型豪華車中最為顯著,這些車輛的ADAS普及率最高,進一步壓縮了對外部零件的需求。然而,由於需要進行感測器校準和更長的工時,配備ADAS的車輛維修費用更高,抵消了部分需求下降的影響。損壞的攝影機和雷達模組的更換推動了專用電子產品細分市場的成長。碰撞維修中心正在提陞技能並投資先進的掃描工具,這使得提供原廠級感測器和校準夾具的零件供應商受益。

細分市場分析

截至2025年,乘用車將占美國汽車售後市場零件總收入的52.74%,這主要得益於其龐大的保有量。然而,商用輕型卡車預計將以7.05%的複合年成長率成長,隨著小包裹遞送和服務車隊行駛里程的不斷增加,其對汽車售後市場零件規模的貢獻也將更大。嚴苛的使用週期以及對運轉率的嚴格要求,導致煞車系統總成、傳動系統接頭和冷卻零件的更換頻率不斷提高。車隊營運商優先選擇能夠保證快速交付和高效保固流程的供應商,這迫使零件製造商轉向倉庫級庫存和預測性供應系統。

中型和重型卡車由於銷量低、零件成本高且運作損失巨大,因此創造了相對較大的經濟價值。美國環保署 (EPA) 2027 年排放氣體法規正在推動購車前的活動以及售後市場對選擇性催化還原 (SCR) 和顆粒過濾器 (DPF) 的改裝,從而暫時提振了對重型車輛的需求。預測中新分類的巴士和長途客車市場為大批量溫度控管和懸吊產品的專業供應商提供了更多機會。雖然乘用車市場仍然很重要,但隨著家庭在混合辦公時代質疑是否需要多輛車,其銷售成長已趨於平穩。同時,車隊車輛的成長似乎與物流業的擴張密切相關。

到2025年,引擎零件將占美國汽車售後市場零件市場的31.45%,這反映出內燃機(ICE)的持續主導地位。同時,高級駕駛輔助系統(ADAS)感測器預計將以7.52%的複合年成長率成長,標誌著價值正從機械轉向電子。相機模組、雷達單元和控制ECU經常在輕微碰撞中發生故障,或受到環境污染物的影響,從而形成利潤豐厚的更換週期。大陸集團計劃在2024年推出700個新的引擎管理SKU,這反映了該供應商在擴展其電子產品組合的同時,保護其機械基礎的雙管齊下的策略。

在懸吊、煞車和輪胎領域,大型SUV和皮卡的流行趨勢持續推動需求成長。隨著駕駛員對更高連接性和空中升級功能的需求不斷成長,電氣和資訊娛樂細分市場也在擴張,售後硬體和軟體服務之間的界線也變得模糊。車身和外觀零件的市場格局更為複雜:ADAS(高級駕駛輔助系統)降低了事故發生率,而個人化客製化文化和區域氣候變遷造成的損害則支撐著潛在的需求。隨著獨立維修店越來越有能力維修複雜的軟體驅動型車輛系統,工具、診斷設備和車間耗材的需求也不斷成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 現役老舊輕型車輛數量眾多,推動了車輛更換需求。

- 大型SUV和皮卡車的普及推動了易損件收入的成長。

- 電子商務的普及加速了長尾SKU的上市。

- 電動改裝套件開闢了高利潤的專業領域。

- 《維修權法案》擴大了獨立售後市場的進入範圍

- 疫情里程恢復推動服務頻率提升

- 市場限制

- 電動車的活動部件比一般汽車少30-40%。

- ADAS的引入降低了對碰撞部件的需求。

- OE服務即軟體訂閱模式將蠶食硬體銷售。

- 跨境電商湧入的仿冒品侵蝕品牌佔有率

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方和消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按車輛類型

- 搭乘用車

- 輕型商用車(1-3 類)

- 中型和大型卡車(4-8級)

- 巴士和長途客車(新)

- 依組件類型

- 引擎零件(濾清器、墊片、活塞)

- 變速箱/傳動系統

- 電氣和電子設備(感測器、交流發電機、ADAS)

- 懸吊和煞車

- 車身及外觀(保險桿、照明)

- 胎

- 室內用品和配件

- 潤滑劑和潤滑劑

- 其他(座椅、椅套等)

- 按銷售管道

- 線上

- 離線

- 依推進類型

- 內燃機車輛

- 混合動力電動車(HEV)

- 電池電動車(BEV)

- 插電式混合動力電動車(PHEV)

- 燃料電池電動車(FCEV)

- 透過服務管道

- DIY

- DIFM獨立維修店

- 車隊/商業服務供應商

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Magna International Inc.

- Continental AG

- ZF Friedrichshafen AG

- DENSO Corporation

- Robert Bosch GmbH

- Lear Corporation

- Flex-N-Gate Corporation

- Panasonic Automotive Systems Co. of America

- Aisin World Corp. of America

- American Axle & Manufacturing

- Yazaki North America

- Adient PLC

- Faurecia SE

- Aptiv PLC

- LKQ Corporation

- Advance Auto Parts Inc.

- O'Reilly Automotive Inc.

- AutoZone Inc.

- Genuine Parts Co.(NAPA)

- Tenneco Inc.

- Dana Incorporated

- BorgWarner Inc.

- Goodyear Tire & Rubber Co.

第7章 市場機會與未來展望

The United States aftermarket automotive parts and components market is expected to grow from USD 229.31 billion in 2025 to USD 238.75 billion in 2026 and is forecast to reach USD 292.27 billion by 2031 at 4.12% CAGR over 2026-2031.

A longer average vehicle age, strong light-truck sales, and rapid e-commerce uptake underpin this expansion. Elevated new-vehicle prices, wider right-to-repair statutes, and post-pandemic driving recovery stimulate replacement demand, while emerging electrified retrofit kits carve out premium specialty niches. Competitive intensity varies by component category, yet suppliers that pair omnichannel distribution with electronics expertise are positioning for durable growth. Regulatory initiatives, from EPA emissions rules to state EV mandates, act as simultaneous headwinds and tailwinds, reshaping the aftermarket automotive parts market through shifting compliance requirements.

United States Aftermarket Automotive Parts And Components Market Trends and Insights

Shift to Larger SUVs and Pickups Raises Wear-Part Revenues

Light trucks are poised to take the automotive market by storm, likely capturing a substantial share of new-vehicle sales by 2027. Each of these robust vehicles commands a higher aftermarket expenditure compared to traditional passenger cars, reflecting their unique demands and capabilities. The components that comprise these trucks, suspension, braking, and drivetrain parts, must endure considerably greater stress due to the hefty loads they tow and carry.

As lifestyle trends like overlanding, trailering, and outdoor adventures gain popularity, the appetite for performance-enhancing upgrades swells. Enthusiasts are seeking out lift kits, heavy-duty shocks, and oversized tires to elevate their driving experiences and tackle rugged terrains. The market for specialty equipment tailored to pickups has already surpassed an impressive USD 16 billion annually, prompting manufacturers to roll out dedicated product lines for these versatile vehicles.

Light-truck owners are often passionate about customization, leading to an average transaction value for upgrades that frequently eclipses that of standard replacements. This trend not only enhances the aesthetics and functionality of their trucks but also elevates profit margins across the aftermarket automotive parts sector, signaling a thriving market with boundless potential.

E-Commerce Penetration Accelerates Long-Tail SKU Availability

The vast majority of aftermarket transactions now traverse the dynamic landscape of digital channels, far surpassing the overall adoption of retail e-commerce across the United States. This remarkable shift allows online storefronts to showcase specialized SKUs without the burdensome costs of inventory that traditional brick-and-mortar wholesalers encounter. As a result, they can effortlessly provide nationwide access to hard-to-find parts for vintage models, catering to enthusiasts and collectors alike. Drop-shipment logistics and real-time inventory data reduce lead times for DIYers and small garages, redistributing market power toward digitally savvy suppliers. Yet counterfeit inflow remains an acute risk; federal enforcement actions underscore the importance of brand-protection programs . Firms that combine robust authentication technology with user-friendly interfaces are capturing a disproportionate share of the expanding digital aftermarket.

ADAS Lowers Collision-Part Volumes

Automatic emergency braking and lane-keeping systems are cutting crash rates, trimming demand for bumpers, fenders, and lamps. Collision frequency declines most among late-model premium vehicles, where ADAS penetration is highest, compressing volumes for cosmetic body parts. Offsetting this decline, repairs on ADAS-equipped vehicles command higher invoice values due to mandatory sensor calibration and longer labor hours. Replacement of damaged cameras or radar modules fosters growth in specialized electronics sub-segments. Collision-repair centers are upskilling and investing in advanced scan tools, benefiting parts suppliers that offer OE-grade sensors and calibration fixtures.

Other drivers and restraints analyzed in the detailed report include:

- Electrified Retrofit Kits Open High-Margin Specialty Niches

- Post-Pandemic Rebound in Vehicle Miles Traveled Lifts Service Frequency

- OEM "Service-as-Software" Subscriptions Cannibalize Hardware Sales

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars accounted for 52.74% of the United States Aftermarket Automotive Parts and Components Market overall revenue in 2025, anchored through an expansive installed base. Nevertheless, commercial light trucks are projected to post a 7.05% CAGR, elevating their contribution to the aftermarket automotive parts market size as parcel delivery and service fleets log higher daily mileage. Combining intensive duty cycles and stringent uptime requirements lifts replacement frequency for brake assemblies, driveline joints, and cooling components. Fleet operators' procurement practices favor suppliers that guarantee rapid availability and streamlined warranty processes, nudging parts makers toward depot-level inventory and predictive fulfillment systems.

Medium and heavy trucks yield outsized monetary value, while smaller in volume, because individual components carry higher price tags and downtime penalties. EPA 2027 emissions rules motivate prebuy activity and aftermarket retrofits of selective catalytic reduction and particulate filters, temporarily boosting heavy-duty demand. Buses and coaches, newly segmented in the forecast, open ancillary potential for specialist providers of high-capacity thermal-management and suspension products. Passenger-car segments remain relevant but confront a plateauing unit base as households question the need for multiple vehicles in the era of hybrid work, whereas fleet vehicles appear locked into growth trajectories tied to logistics expansion.

Engine components retained 31.45% of the United States Aftermarket Automotive Parts and Components Market in 2025, mirroring the still-dominant ICE parc. Yet ADAS sensors are forecast for a 7.52% CAGR, signaling the pivot from mechanical to electronic value. Camera modules, radar units, and control ECUs often fail in minor collisions or succumb to environmental contaminants, creating high-margin replacement cycles. Continental's 2024 launch of 700 new engine-management SKUs illustrates suppliers' dual strategy of defending mechanical strongholds while scaling electronics portfolios.

Suspension, brake, and tire categories see ongoing lift from the trend toward heavier SUVs and pickups. Electrical and infotainment sub-segments increase as drivers seek connectivity upgrades and over-the-air functionality, blurring the line between aftermarket hardware and software services. Body and exterior parts face mixed fortunes: ADAS reduces collision frequency, yet personalization culture and regional climate damage sustain baseline demand. Tools, diagnostics, and shop consumables are expanding as independent garages gear up to service complex, software-driven vehicle systems.

The United States Aftermarket Automotive Parts and Components Market is Segmented by Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Component Type (Engine Components, Transmission and Driveline, and More), Sales Channel (Online and Offline), Propulsion Type (ICE Vehicles, and More), and by Service Channel (DIY, DIFM Independent Garages, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Magna International Inc.

- Continental AG

- ZF Friedrichshafen AG

- DENSO Corporation

- Robert Bosch GmbH

- Lear Corporation

- Flex-N-Gate Corporation

- Panasonic Automotive Systems Co. of America

- Aisin World Corp. of America

- American Axle & Manufacturing

- Yazaki North America

- Adient PLC

- Faurecia SE

- Aptiv PLC

- LKQ Corporation

- Advance Auto Parts Inc.

- O'Reilly Automotive Inc.

- AutoZone Inc.

- Genuine Parts Co. (NAPA)

- Tenneco Inc.

- Dana Incorporated

- BorgWarner Inc.

- Goodyear Tire & Rubber Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Light-Vehicle Parc Drives Replacement Demand.

- 4.2.2 Shift To Larger SUVs and Pickups Raises Wear-Part Revenues.

- 4.2.3 E-Commerce Penetration Accelerates Long-Tail SKU Availability.

- 4.2.4 Electrified Retrofit Kits Open High-Margin Specialty Niches.

- 4.2.5 Right-To-Repair Statutes Widen Independent Aftermarket Access.

- 4.2.6 Post-Pandemic Rebound In Vehicle-Miles-Traveled Lifts Service Frequency

- 4.3 Market Restraints

- 4.3.1 EVs Contain 30-40 % Fewer Moving Parts.

- 4.3.2 ADAS Lowers Collision-Part Volumes

- 4.3.3 OE Service-As-Software Subscriptions Cannibalize Hardware Sales.

- 4.3.4 Counterfeit Inflow Via Cross-Border E-Commerce Erodes Brand Share.

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Light Commercial Vehicles (Class 1-3)

- 5.1.3 Medium & Heavy Trucks (Class 4-8)

- 5.1.4 Buses & Coaches (NEW)

- 5.2 By Component Type

- 5.2.1 Engine Components (filters, gaskets, pistons)

- 5.2.2 Transmission & Driveline

- 5.2.3 Electrical & Electronics (sensors, alternators, ADAS)

- 5.2.4 Suspension & Brakes

- 5.2.5 Body & Exterior (bumpers, lighting)

- 5.2.6 Tires

- 5.2.7 Interior & Accessories

- 5.2.8 Fluids & Lubricants

- 5.2.9 Others (Seat and Covers, etc.)

- 5.3 By Sales Channel

- 5.3.1 Online

- 5.3.2 Offline

- 5.4 By Propulsion Type

- 5.4.1 Internal-Combustion Engine (ICE) Vehicles

- 5.4.2 Hybrid Electric Vehicles (HEV)

- 5.4.3 Battery Electric Vehicles (BEV)

- 5.4.4 Plug-in Hybrid Electric Vehicles (PHEV)

- 5.4.5 Fuel-Cell Electric Vehicles (FCEV)

- 5.5 By Service Channel

- 5.5.1 DIY (Do-It-Yourself)

- 5.5.2 DIFM Independent Garages

- 5.5.3 Fleet / Commercial Service Providers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Magna International Inc.

- 6.4.2 Continental AG

- 6.4.3 ZF Friedrichshafen AG

- 6.4.4 DENSO Corporation

- 6.4.5 Robert Bosch GmbH

- 6.4.6 Lear Corporation

- 6.4.7 Flex-N-Gate Corporation

- 6.4.8 Panasonic Automotive Systems Co. of America

- 6.4.9 Aisin World Corp. of America

- 6.4.10 American Axle & Manufacturing

- 6.4.11 Yazaki North America

- 6.4.12 Adient PLC

- 6.4.13 Faurecia SE

- 6.4.14 Aptiv PLC

- 6.4.15 LKQ Corporation

- 6.4.16 Advance Auto Parts Inc.

- 6.4.17 O'Reilly Automotive Inc.

- 6.4.18 AutoZone Inc.

- 6.4.19 Genuine Parts Co. (NAPA)

- 6.4.20 Tenneco Inc.

- 6.4.21 Dana Incorporated

- 6.4.22 BorgWarner Inc.

- 6.4.23 Goodyear Tire & Rubber Co.

7 Market Opportunities & Future Outlook

2026年全球中行程懸吊套件市場報告

2026年全球中行程懸吊套件市場報告 機車售後市場零件及耗材市場分析及預測(至2035年):按類型、產品、服務、技術、零件、應用、材料類型、最終用戶、安裝類型及解決方案分類全球汽車售後零件市場:機會與策略展望(至2035年)

機車售後市場零件及耗材市場分析及預測(至2035年):按類型、產品、服務、技術、零件、應用、材料類型、最終用戶、安裝類型及解決方案分類全球汽車售後零件市場:機會與策略展望(至2035年) 汽車售後零件市場:按產品類型、車輛類型、銷售管道和地區分類

汽車售後零件市場:按產品類型、車輛類型、銷售管道和地區分類 日本汽車售後市場配件市場規模、佔有率、趨勢及預測(按產品類型、車輛類型、銷售管道、最終用戶和地區分類,2026-2034年)日本汽車零件售後市場規模、佔有率、趨勢和預測:按類型、應用和地區分類,2026-2034年

日本汽車售後市場配件市場規模、佔有率、趨勢及預測(按產品類型、車輛類型、銷售管道、最終用戶和地區分類,2026-2034年)日本汽車零件售後市場規模、佔有率、趨勢和預測:按類型、應用和地區分類,2026-2034年 2024-2028年全球汽車售後零件市場

2024-2028年全球汽車售後零件市場