|

市場調查報告書

商品編碼

1939740

美國物業管理:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)US Property Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

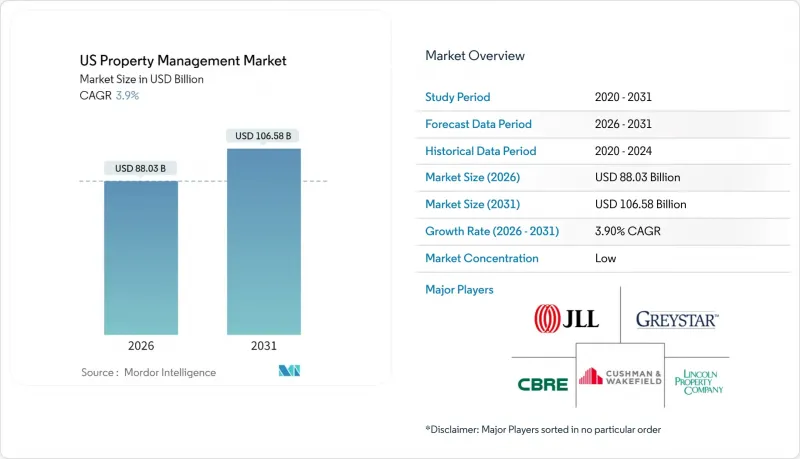

預計到 2025 年,美國物業管理服務市場價值將達到 847.3 億美元,到 2031 年將達到 1,065.8 億美元,高於 2026 年的 880.3 億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 3.9%。

強勁的租賃需求、機構投資者對單戶和多用戶住宅住宅資產的持有以及高階辦公大樓租賃活動的復甦支撐了市場成長。根據聯準會的一項調查,27%的美國成年人租房子住宅,這支撐著大規模的租戶群體,需要專業的物業管理服務。機構投資人正利用其規模優勢推動專業化管理,而環境、社會和管治(ESG)法規的實施也加速了對合規服務的需求。科技的應用,特別是能夠自動化租賃、維護和居住者互動的人工智慧工具,進一步提高了效率和租戶留存率。全國性公司正擴大收購技術型專業公司,以擴大其服務範圍和地理涵蓋範圍,從而加劇了市場競爭。

美國物業管理市場趨勢與洞察

擴大我們的獨棟住宅租賃 (SFR) 組合

機構對獨棟住宅的所有權模式已從2010年代初期的大量收購法拍房,發展到2024年成熟的「建後出租」模式。根據美國政府審核局(GAO)的研究,截至2015年,機構擁有的獨棟住宅數量已達17萬至30萬套。如今,隨著基金加速收購,機構的大規模擴大。例如,American Homes 4 Rent在2024年管理61,336套住宅,創造了17.29億美元的租金收入。這種規模的擴張導致對標準化租賃協議、維護和合規流程的需求增加,而這些服務通常由個人房東提供。因此,專業的住宅管理服務提供者和綜合房地產投資信託基金(REIT)平台在美國物業管理服務市場中獲得了定價權和穩定的收入來源。

A級商業不動產需求增加

隨著越來越多的公司尋求高價值辦公空間以支持混合辦公模式,高階辦公物業正重新吸引租戶的目光。世邦魏理仕(CBRE)預測,到2024年,租金收入將成長18%,其中紐約的辦公大樓租賃市場將飆升28%。頂級辦公室的業主正透過引入禮賓團隊、智慧建築平台和精心策劃的租戶體驗來提升其供應的差異化優勢。這些附加價值服務通常需要大規模的管理預算,使專業公司能夠收取更高的費用。績效標竿管理和配套設施升級也為能源管理和辦公室諮詢等服務創造了交叉銷售機會。因此,專注於美國A級物業組合的物業管理公司正在實現持續的收入成長。

利率上升導致交易放緩

自2023年底以來,不斷攀升的借貸成本導致房地產銷售和新開發項目停滯不前。據世邦魏理仕(CBRE)稱,儘管現有投資組合保持相對穩定,但投資量已大幅下降。交易量的減少意味著物業管理公司(其收入主要來自物業入駐費和施工管理費)的房產收購和新開發項目減少。依賴交易量的中小型企業正面臨短期收入壓力。然而,持續的管理合約將緩解這種影響,使美國整體物業管理服務市場得以繼續擴張,儘管增速放緩,直至利率恢復正常。

細分市場分析

預計到2025年,住宅房地產將佔總收入的49.35%,成為美國物業管理服務市場中佔有率最大的部分。機構型單戶住宅租賃物業和多用戶住宅住宅組合可提供可預測的租金收入,而配套設施齊全的社區則可透過停車、倉儲空間、智慧家庭訂閱等方式產生額外收入。商業房地產預計將以4.82%的複合年成長率成長,隨著A級辦公室和體驗式零售租賃需求的復甦,住宅房地產與物業管理服務之間的差距將逐漸縮小。

住宅市場受惠於房地產投資信託基金(REITs)的集中持股,例如Invitation Homes在2024年投資了4.252億美元用於物業維修。規模的擴大轉化為供應商定價的改善、技術的普及和反應速度的提升,這印證了專業管理是機構投資者的必備條件。商業不動產的成長則得益於企業向更高品質物業的搬遷以及傳統建築中融入的新型靈活辦公空間模式。隨著電子商務公司尋求更靠近消費者的位置,並依賴專業的維護和通訊協定,工業和物流資產也展現出更大的成長潛力。這些趨勢共同推動了美國物業管理服務市場的均衡成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- A級商業不動產需求增加

- 擴大我們的獨棟住宅租賃 (SFR) 組合

- 退休基金和主權財富基金擴大將投資外包給機構投資者

- 採用基於人工智慧的租賃管理和服務技術

- 美國老舊的住宅存量需要專業的維護。

- ESG與綠色租賃合規壓力

- 市場限制

- 利率波動導致交易放緩

- 州和市的租金管制法

- 由於技術純熟勞工短缺,營運成本(OPEX)增加

- 業主轉向自助式房地產科技平台

- 價值/供應鏈分析

- 監管狀況(住房和城市發展部、聯邦住房金融局、州租賃法)

- 技術展望(物聯網感測器、人工智慧租賃機器人、SaaS 管理套件)

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 業主和租戶的議價能力

- 供應商/分包商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章 市場規模及成長預測(價值,單位:十億美元)

- 按屬性類型

- 商業的

- 住宅

- 工業與物流

- 機構/混合用途

- 按服務類型

- 行銷與租賃管理

- 房地產估值和實質審查

- 租戶及居住者服務(租賃合約等)

- 維護、維修和設施管理

- 租賃管理及合規

- 其他服務(合規、法律服務、續約程序等)

- 按地區

- 東北

- 中西部

- 東南

- 西

- 西南

第6章 競爭情勢

- 市場集中度

- 策略性舉措和資金籌措活動

- 市佔率分析

- 公司簡介

- Greystar Real Estate Partners

- CBRE Group, Inc.

- Lincoln Property Company

- Jones Lang LaSalle(JLL)

- Cushman & Wakefield plc

- Pinnacle Property Management Services

- Equity Residential

- AvalonBay Communities, Inc.

- Invitation Homes Inc.

- FPI Management

- RPM Living

- FirstService Residential

- UDR, Inc.

- Aimco

- WinnCompanies

- Brookfield Properties US

- Colliers International US

- CoStar Group, Inc.

- Cushman & Wakefield Asset Services

- Knightvest Capital Management

第7章 市場機會與未來展望

The US Property Management Services Market was valued at USD 84.73 billion in 2025 and estimated to grow from USD 88.03 billion in 2026 to reach USD 106.58 billion by 2031, at a CAGR of 3.9% during the forecast period (2026-2031).

Growth rests on resilient rental demand, institutional ownership of both single-family and multifamily assets, and renewed leasing activity in premium office buildings. Federal Reserve surveys show 27% of U.S. adults rent their homes, underpinning a large tenant base that requires professional oversight. Institutional investors use scale to drive professional management, while environmental, social, and governance (ESG) regulations accelerate demand for compliance-oriented services. Technology adoption, especially artificial-intelligence tools that automate leasing, maintenance, and resident engagement, further supports efficiency and tenant retention. Competitive intensity is rising as national firms buy tech-enabled specialists to widen service breadth and geographic reach.

US Property Management Market Trends and Insights

Expansion of Single-Family Rental (SFR) Portfolios

Institutional ownership of single-family homes grew from bulk foreclosure purchases in the early 2010s to sophisticated build-for-rent programs by 2024. The GAO traced holdings of 170,000-300,000 homes by 2015, with larger footprints today as funds accelerate acquisitions. American Homes 4 Rent, for example, managed 61,336 homes and generated USD 1.729 billion rental revenue in 2024. Scale drives demand for standardized leasing, maintenance, and compliance processes that individual landlords rarely provide. Consequently, residential specialists and integrated REIT platforms gain pricing power and recurring revenue inside the US property management services market.

Rising Demand from Class-A Commercial Real Estate

Premium office assets are regaining tenant attention as employers seek high-amenity space to support hybrid work models. CBRE recorded 18% leasing revenue growth in 2024, including a 28% jump in office leasing in New York. Owners of trophy buildings deploy concierge teams, smart-building platforms, and curated tenant experiences to differentiate supply. These value-added services typically require large management budgets, allowing professional firms to command higher fees. Performance benchmarking and amenity upgrades also create cross-selling potential for energy management and workplace consulting. The result is durable revenue growth for managers focused on Class-A portfolios within the US property management services market.

Interest-Rate-Driven Transaction Slowdown

Elevated borrowing costs since late 2023 have caused a pause in property sales and ground-up development. CBRE noted that investment volume fell sharply even as existing portfolios remained relatively stable. Less trading means fewer property takeovers and new-build assignments for managers who earn onboarding and construction-management fees. Smaller firms that rely on deal flow face near-term revenue stress. Nonetheless, recurring management contracts cushion the impact, allowing the broader US property management services market to continue expanding, albeit at a slower clip until rates normalize.

Other drivers and restraints analyzed in the detailed report include:

- Aging U.S. Housing Stock Needs Professional Maintenance

- Growing Institutional Outsourcing by Pension/SWF Investors

- State & City Rent-Control Legislation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Residential properties accounted for 49.35% of 2025 revenue, making them the largest slice of the US property management services market share. Institutional single-family rentals and multifamily portfolios deliver predictable, recurring fees based on rent rolls, while amenity-rich communities drive ancillary income from parking, storage, and smart-home subscriptions. Commercial properties are projected to register a 4.82% CAGR and will narrow the gap as leasing rebounds in Class-A offices and experiential retail.

The residential segment benefits from concentrated holdings by REITs such as Invitation Homes, which invested USD 425.2 million in property upgrades in 2024. Scale improves vendor pricing, technology adoption, and response times, reinforcing professional management as table stakes for institutional owners. Commercial growth is fueled by corporate flight to quality and new flexible-workspace models integrated into traditional buildings. Industrial and logistics assets add further upside as e-commerce firms seek proximity to consumers and rely on specialized maintenance and security protocols. Together, these dynamics sustain balanced momentum in the US property management services market.

The US Property Management Services Market Report is Segmented by Property Type (Commercial, Residential, Industrial & Logistics, and More), by Service Type (Marketing & Leasing, Property Evaluation & Due Diligence, Tenant & Resident Services, Maintenance & Facility Management, and More), and by Geography (Northeast, Midwest, Southeast, West and Southwest). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Greystar Real Estate Partners

- CBRE Group, Inc.

- Lincoln Property Company

- Jones Lang LaSalle (JLL)

- Cushman & Wakefield plc

- Pinnacle Property Management Services

- Equity Residential

- AvalonBay Communities, Inc.

- Invitation Homes Inc.

- FPI Management

- RPM Living

- FirstService Residential

- UDR, Inc.

- Aimco

- WinnCompanies

- Brookfield Properties U.S.

- Colliers International U.S.

- CoStar Group, Inc.

- Cushman & Wakefield Asset Services

- Knightvest Capital Management

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand from Class-A commercial real estate

- 4.2.2 Expansion of single-family rental (SFR) portfolios

- 4.2.3 Growing institutional outsourcing by pension/SWF investors

- 4.2.4 Adoption of AI-enabled leasing & service tech

- 4.2.5 Aging U.S. housing stock needs professional maintenance

- 4.2.6 ESG & green-lease compliance pressure

- 4.3 Market Restraints

- 4.3.1 Interest-rate-driven transaction slowdown

- 4.3.2 State & city rent-control legislation

- 4.3.3 Skilled trade-labor shortages raising OPEX

- 4.3.4 Owners' shift to DIY prop-tech platforms

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape (HUD, FHFA, State landlord-tenant laws)

- 4.6 Technological Outlook (IoT sensors, AI leasing bots, SaaS PM suites)

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Owners/Tenants

- 4.7.3 Bargaining Power of Suppliers/Sub-contractors

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry Intensity

5 Market Size & Growth Forecasts(Value, In USD Billion)

- 5.1 By Property Type

- 5.1.1 Commercial

- 5.1.2 Residential

- 5.1.3 Industrial & Logistics

- 5.1.4 Institutional & Mixed-Use

- 5.2 By Service Type

- 5.2.1 Marketing & Leasing

- 5.2.2 Property Evaluation & Due Diligence

- 5.2.3 Tenant & Resident Services (Renting, Leasing, etc.)

- 5.2.4 Maintenance, Repair & Facility Management

- 5.2.5 Lease Administration & Compliance

- 5.2.6 Other Services (Compliance, Legal Services, Renewals, etc.)

- 5.3 By Geography

- 5.3.1 Northeast

- 5.3.2 Midwest

- 5.3.3 Southeast

- 5.3.4 West

- 5.3.5 Southwest

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves & Funding Activities

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Greystar Real Estate Partners

- 6.4.2 CBRE Group, Inc.

- 6.4.3 Lincoln Property Company

- 6.4.4 Jones Lang LaSalle (JLL)

- 6.4.5 Cushman & Wakefield plc

- 6.4.6 Pinnacle Property Management Services

- 6.4.7 Equity Residential

- 6.4.8 AvalonBay Communities, Inc.

- 6.4.9 Invitation Homes Inc.

- 6.4.10 FPI Management

- 6.4.11 RPM Living

- 6.4.12 FirstService Residential

- 6.4.13 UDR, Inc.

- 6.4.14 Aimco

- 6.4.15 WinnCompanies

- 6.4.16 Brookfield Properties U.S.

- 6.4.17 Colliers International U.S.

- 6.4.18 CoStar Group, Inc.

- 6.4.19 Cushman & Wakefield Asset Services

- 6.4.20 Knightvest Capital Management

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

2026-2030年全球房地產管理市場

2026-2030年全球房地產管理市場 2026年全球房地產管理市場報告2026年全球物業管理服務市場報告

2026年全球房地產管理市場報告2026年全球物業管理服務市場報告 住宅物業管理市場:2026-2032年全球預測(依服務內容、所有權類型、合約期限及實施方法分類)2026年全球商業房地產管理市場報告

住宅物業管理市場:2026-2032年全球預測(依服務內容、所有權類型、合約期限及實施方法分類)2026年全球商業房地產管理市場報告 物業管理市場規模、佔有率和成長分析(按組成部分、地點、物業類型、最終用戶和地區分類)—產業預測(2026-2033 年)

物業管理市場規模、佔有率和成長分析(按組成部分、地點、物業類型、最終用戶和地區分類)—產業預測(2026-2033 年) 物業管理市場-全球產業規模、佔有率、趨勢、機會和預測,按組件、部署方式、最終用戶、應用、地區和競爭格局分類,2020-2030 年預測住宅物業管理軟體市場 - 全球產業規模、佔有率、趨勢、機會和預測,按部署、按最終用戶、按地區、按競爭進行細分,2020-2030 年預測

物業管理市場-全球產業規模、佔有率、趨勢、機會和預測,按組件、部署方式、最終用戶、應用、地區和競爭格局分類,2020-2030 年預測住宅物業管理軟體市場 - 全球產業規模、佔有率、趨勢、機會和預測,按部署、按最終用戶、按地區、按競爭進行細分,2020-2030 年預測 物業管理市場、規模、趨勢和行業分析報告:依產品、地理、物業類型、最終用戶和地區 - 市場預測(2025-2034年)

物業管理市場、規模、趨勢和行業分析報告:依產品、地理、物業類型、最終用戶和地區 - 市場預測(2025-2034年) 全球房地產管理市場:按產品、地理位置、房地產類型、最終用戶、地區分類 - 到 2030 年的預測

全球房地產管理市場:按產品、地理位置、房地產類型、最終用戶、地區分類 - 到 2030 年的預測