|

市場調查報告書

商品編碼

1939733

英國包裝業:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)United Kingdom Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

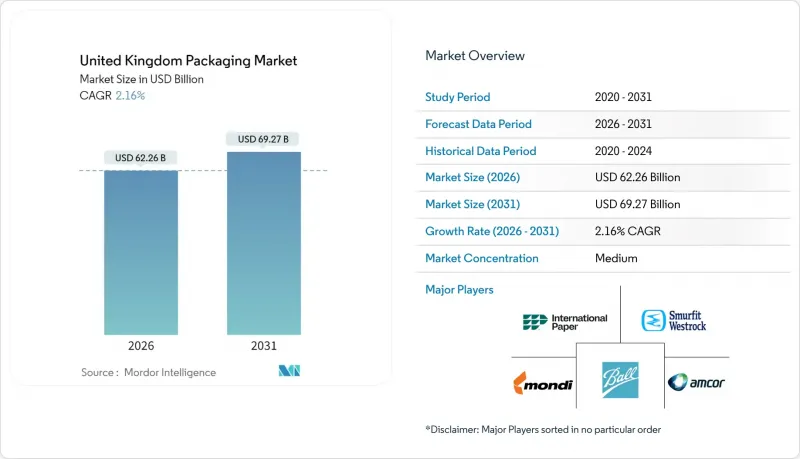

英國包裝市場預計到 2026 年價值將達到 622.6 億美元,高於 2025 年的 609.4 億美元。

預計到 2031 年將達到 692.7 億美元,2026 年至 2031 年的複合年成長率為 2.16%。

目前的市場動能反映了一個日益成熟且不斷演變的格局,其形成受到英國脫歐後邊境規則、更嚴格的環境法規、電子商務加速發展以及成本上漲。邊境目標營運模式(BTOM)下的結構調整增加了合規工作量和交付前置作業時間,促使生產商在在地採購並實現海關文件的自動化。同時,英國塑膠包裝稅的擴大和生產者延伸責任制的全面實施,提高了人們對可回收性的關注,推動了紙張、單一材料塑膠和生物基薄膜的快速替代。線上零售額佔國內銷售額的31.3%,提升了軟包裝的市場佔有率,而增值印刷能力則使品牌能夠以更具成本效益的方式瞄準細分客戶群。產業整合仍在持續,其中最引人注目的是國際紙業以75.4億美元收購DS Smith,此舉不僅打造了該地區最大的瓦楞紙包裝供應商,也加劇了反壟斷審查。

英國包裝市場趨勢與洞察

電子商務的擴張推動了對瓦楞紙包裝和軟包裝袋的需求。

到2024年,線上零售額將佔國內總銷售額的31.3%,瓦楞紙箱和軟包裝袋的出貨量增加了23%。 Getil等電商平台推廣了兼具防篡改和隔熱功能的單件包裝。亞馬遜的自動化包裝線減少了15%的包裝材料用量,提高了出貨效率,並樹立了新的效率標竿。 HelloFresh的訂閱模式增加了對可回收隔熱材料的需求,而電商賣家也擴大選擇尺寸合適的郵寄袋以降低體積重量收費。這些趨勢都支撐著瓦楞紙箱和軟包裝在英國包裝市場的持續擴張。

英國塑膠稅轉向可再生和生物基材料

2024年塑膠包裝稅的擴大將對再生材料含量低於30%的聚合物徵收每噸200英鎊(263美元)的課稅,這將推動再生材料含量提高35%。聯合利華在英國的個人保健產品線中已實現了50%的再生塑膠使用率,雀巢也承諾在2025年實現完全可回收解決方案。原生樹脂與再生材料之間的價格差距已擴大至18%,這有利於垂直整合的回收企業。大型加工商的平均監管成本已達230萬英鎊(302萬美元),推動了對水洗薄片產能和化學回收試點計畫的資金投入。這些永續發展要求正在加速英國包裝市場材料組合的重組。

樹脂和造紙原物料價格飆升

預計到2024年,聚乙烯樹脂價格將上漲22%,而由於能源成本上升和供應受限,再生紙價格也將上漲18%。蒙迪英國業務的利潤率下降了340個基點,導致下游價格上漲,需求彈性降低。加工商將安全庫存水準提高了25%至30%,以確保供應的連續性,但倉儲成本給營運資金帶來了壓力。高能耗擠出生產線在價格高峰期減產,凸顯了英國包裝市場短期內面臨的拖累。

細分市場分析

到2025年,塑膠將佔英國包裝市場佔有率的48.02%,這主要得益於其在食品、飲料和個人護理行業的廣泛應用。過去十年,硬質寶特瓶的輕量化設計已使材料重量減少了25%,而消費後回收樹脂的整合也提高了再生材料的可靠性。然而,稅收閾值的收緊以及零售商的無塑膠承諾正推動成長重點轉向紙質基材。受電子商務對瓦楞紙板需求成長的推動,紙質基材將呈現最快的成長速度,到2031年複合年成長率將達到4.62%。隨著單一材料設計簡化家庭垃圾收集,英國包裝紙質基材市場規模預計將持續擴大。

由於玻璃和金屬具有無限可回收性和良好的品質感,它們在高階飲品領域重新佔據一席之地,分別推動了3.2%和4.1%的年成長率。隨著精釀啤酒廠利用鋁罐的輕盈和快速冷卻特性,並透過提高產量來抵消不斷上漲的原料成本,飲料罐的需求激增。同時,可生物分解的聚合物薄膜也已滲透到一些特殊用途領域,在這些領域,可堆肥性決定了其價格溢價。這些變化表明,儘管塑膠的主導地位略有下降,但其仍然佔據主導地位,因為永續性標準正在影響英國包裝市場的材料選擇。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 由於電子商務的擴張,對瓦楞紙板和軟包裝郵件的需求增加。

- 英國塑膠稅與向可再生和生物基材料的轉型

- 千禧世代和旅遊需求優質化和對豪華包裝的需求。

- 快速消費品自有品牌在折扣通路的擴張需要經濟高效的包裝。

- 暗廚房的興起和快速零售的擴張催生了對單件包裝的需求。

- 採用數位印刷技術進行小批量生產,使小型企業品牌能夠客製化產品。

- 市場限制

- 樹脂和造紙原料價格波動劇烈

- 英國對一次性塑膠製品的監管更加嚴格,以及生產者延伸責任制(EPR)的成本

- 英國脫歐後供應鏈中斷對進口包裝組件的影響

- 製造業和物流業勞動力短缺推高了營運成本。

- 產業價值鏈分析

- 技術展望

- 監管環境

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 宏觀經濟因素的影響

第5章 市場規模與成長預測

- 按包裝類型

- 塑膠包裝

- 按類型

- 硬質塑膠包裝

- 依材料類型

- 聚乙烯(PE)

- 聚丙烯(PP)

- 聚對苯二甲酸乙二醇酯(PET)

- 聚氯乙烯(PVC)

- 聚苯乙烯(PS)和發泡聚苯乙烯(EPS)

- 其他材料類型

- 依產品類型

- 瓶子和罐子

- 瓶蓋和封裝

- 托盤和容器

- 其他產品類型

- 按最終用途行業分類

- 食物

- 飲料

- 製藥

- 化妝品和個人護理

- 工業的

- 其他終端用戶產業

- 依材料類型

- 軟塑膠包裝

- 依材料類型

- 聚乙烯(PE)

- 雙軸延伸聚丙烯(BOPP)

- 流延聚丙烯(CPP)

- 其他材料類型

- 依產品類型

- 麻袋

- 薄膜和包裝

- 其他產品類型

- 按最終用途行業分類

- 食物

- 飲料

- 製藥

- 化妝品和個人護理

- 工業的

- 其他終端用戶產業

- 依材料類型

- 硬質塑膠包裝

- 依產品類型

- 瓶子和罐子

- 麻袋

- 散裝產品

- 其他產品類型

- 按最終用途行業分類

- 食物

- 飲料

- 化妝品和個人護理

- 製藥

- 工業的

- 其他終端用戶產業

- 按類型

- 紙包裝

- 依產品類型

- 折疊紙箱

- 瓦楞紙箱

- 液態紙板

- 其他產品類型

- 按最終用途行業分類

- 食物

- 飲料

- 電子商務

- 其他終端用戶產業

- 依產品類型

- 容器玻璃

- 按顏色

- 綠色的

- 琥珀色

- 燧石

- 其他顏色

- 按最終用途行業分類

- 食物

- 飲料

- 酒精飲料

- 不含酒精的飲料

- 個人護理和化妝品

- 藥品(不含管瓶和安瓿瓶)

- 香水

- 按顏色

- 金屬罐和容器

- 依材料類型

- 鋼材

- 鋁

- 依產品類型

- 能

- 鼓和桶

- 瓶蓋和封裝

- 其他產品類型

- 按最終用途行業分類

- 食物

- 飲料

- 化學品/石油

- 工業的

- 油漆和塗料

- 其他終端用戶產業

- 依材料類型

- 塑膠包裝

- 按包裝類型

- 靈活的

- 難的

- 按最終用途行業分類

- 食物

- 飲料

- 製藥和醫療保健

- 個人護理和化妝品

- 工業的

- 電子商務

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- International Paper Company

- Smurfit WestRock

- Amcor plc

- Mondi plc

- Ball Corporation

- Crown Holdings Inc.

- Sealed Air Corporation

- Sonoco Products Company

- Graphic Packaging International LLC

- Greif Inc.

- Silgan Holdings Inc.

- AptarGroup Inc.

- Huhtamaki Oyj

- Tetra Pak International SA

- CAN-PACK UK Ltd.

- Ardagh Group SA

- RPC Group Ltd.

- Klckner Pentaplast Ltd.

- Coveris Holdings SA

第7章 市場機會與未來展望

United Kingdom packaging market size in 2026 is estimated at USD 62.26 billion, growing from 2025 value of USD 60.94 billion with 2031 projections showing USD 69.27 billion, growing at 2.16% CAGR over 2026-2031.

Current momentum reflects a mature yet steadily evolving landscape shaped by post-Brexit border rules, tighter environmental mandates, e-commerce acceleration and pronounced cost inflation. Structural adjustments under the Border Target Operating Model raised compliance workloads and stretched lead times, prompting producers to localize inputs and automate customs documentation. Parallel expansion of the United Kingdom Plastic Packaging Tax and full roll-out of Extended Producer Responsibility sharpened the focus on recyclability, driving rapid substitution toward paper, mono-material plastics and bio-based films. Flexible formats gained share as online retail reached 31.3% of national sales, and value-added printing capabilities helped brands target niche audiences cost-effectively. Consolidation continued, highlighted by International Paper's USD 7.54 billion acquisition of DS Smith, which created the region's largest corrugated supplier but intensified antitrust scrutiny.

United Kingdom Packaging Market Trends and Insights

Rising E-commerce Driven Demand for Corrugated and Flexible Mailers

Online retail sales surged to 31.3% of national turnover in 2024, lifting shipment volumes for corrugated boxes and flexible mailers by 23%. Quick-commerce operators such as Getir stimulated single-portion packaging that combines tamper evidence with thermal integrity. Amazon's automated packing lines cut packaging material intensity 15% and accelerated outbound throughput, setting new efficiency benchmarks. Subscription models from HelloFresh amplified demand for returnable insulation, while marketplace sellers gravitated toward right-sized mailers that curb dimensional-weight charges. These developments support continued expansion of corrugated and flexible formats within the United Kingdom packaging market.

Shift Toward Recyclable and Biobased Materials Due to United Kingdom Plastic Tax

The Plastic Packaging Tax extension in 2024 imposed a GBP 200 (USD 263) per-tonne levy on polymers lacking 30% recycled content, encouraging a 35% jump in reclaimed feedstock adoption. Unilever achieved 50% recycled plastic in United Kingdom personal-care lines, while Nestle pledged fully recyclable solutions by 2025. Rising virgin resin differentials 18% above recycled inputs favor vertically integrated recyclers. Average compliance outlays reached GBP 2.3 million (USD 3.02 million) for large converters, prompting capital flows into wash-flake capacity and chemical recycling pilots. Sustainability requirements therefore accelerate material portfolio realignment across the United Kingdom packaging market.

High Raw-Material Price Volatility for Resins and Paper

Polyethylene resin prices jumped 22% in 2024, while recycled paper climbed 18% on energy cost spikes and supply constraints. Mondi's United Kingdom operations reported 340-basis-point margin erosion, triggering downstream price hikes that tempered demand elasticity. Converters raised safety-stock thresholds 25-30% to secure continuity, yet carrying costs strained working capital. Energy-intensive extrusion lines curtailed output during peak tariff windows, underscoring volatility as a short-term drag on the United Kingdom packaging market.

Other drivers and restraints analyzed in the detailed report include:

- Premiumization and Luxury Packaging Demand from Millennials and Tourism

- Growing FMCG Private Label Expansion in Discount Channels Requiring Cost-Efficient Packaging

- Strict United Kingdom Regulations on Single-Use Plastics and Extended Producer Responsibility Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastic accounted for 48.02% of the United Kingdom packaging market share in 2025, underpinned by its versatility across food, beverage and personal-care categories. Rigid PET bottle light-weighting shaved 25% material mass over the decade while integration of post-consumer resin boosted recycled content credibility. Yet tightening tax thresholds and retailer zero-plastic pledges pivot growth toward paper, which delivers the fastest 4.62% CAGR through 2031 on expanding e-commerce corrugated volumes. The United Kingdom packaging market size for paper substrates will continue to widen as mono-material designs simplify curbside recycling.

Glass and metal regained relevance in premium drinks due to infinite recyclability and high perceived quality, contributing 3.2% and 4.1% respective annual growth. Beverage can volumes surged as craft breweries exploited aluminum's light weight and rapid chilling properties, offsetting higher input costs via volume efficiencies. Meanwhile, bio-polymer films entered specialty applications where compostability commands price premiums. These shifts indicate that plastic's leadership persists but erodes marginally as sustainability criteria increasingly influence material selection within the United Kingdom packaging market.

The United Kingdom Packaging Market Report is Segmented by Packaging Type (Plastic, Paper, Container Glass, Metal Cans), Packaging Format (Flexible, Rigid), End-Use Industry (Food, Beverage, Pharmaceuticals, Personal Care, Industrial, E-Commerce). Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- International Paper Company

- Smurfit WestRock

- Amcor plc

- Mondi plc

- Ball Corporation

- Crown Holdings Inc.

- Sealed Air Corporation

- Sonoco Products Company

- Graphic Packaging International LLC

- Greif Inc.

- Silgan Holdings Inc.

- AptarGroup Inc.

- Huhtamaki Oyj

- Tetra Pak International SA

- CAN-PACK UK Ltd.

- Ardagh Group S.A.

- RPC Group Ltd.

- Klckner Pentaplast Ltd.

- Coveris Holdings S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising e Commerce driven demand for corrugated and flexible mailers

- 4.2.2 Shift towards recyclable and biobased materials due to United Kingdom Plastic Tax

- 4.2.3 Premiumization and luxury packaging demand from millennials and tourism

- 4.2.4 Growing FMCG private label expansion in discount channels requiring cost-efficient packaging

- 4.2.5 Growth of dark kitchens and quick commerce creating single-portion packaging needs

- 4.2.6 Adoption of digital printing for short runs enabling customization for SME brands

- 4.3 Market Restraints

- 4.3.1 High raw-material price volatility for resins and paper

- 4.3.2 Strict United Kingdom regulations on single-use plastics and Extended Producer Responsibility costs

- 4.3.3 Supply-chain disruptions post-Brexit impacting imported packaging components

- 4.3.4 Labor shortages in manufacturing and logistics escalating operational costs

- 4.4 Industry Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Packaging Type

- 5.1.1 Plastic Packaging

- 5.1.1.1 By Type

- 5.1.1.1.1 Rigid Plastic Packaging

- 5.1.1.1.1.1 By Material Type

- 5.1.1.1.1.1.1 Polyethylene (PE)

- 5.1.1.1.1.1.2 Polypropylene (PP)

- 5.1.1.1.1.1.3 Polyethylene Terephthalate (PET)

- 5.1.1.1.1.1.4 Polyvinyl Chloride (PVC)

- 5.1.1.1.1.1.5 Polystyrene (PS) and Expanded Polystyrene (EPS)

- 5.1.1.1.1.1.6 Other Material Types

- 5.1.1.1.1.2 By Product Type

- 5.1.1.1.1.2.1 Bottles and Jars

- 5.1.1.1.1.2.2 Caps and Closures

- 5.1.1.1.1.2.3 Trays and Containers

- 5.1.1.1.1.2.4 Other Product Types

- 5.1.1.1.1.3 By End-use Industry

- 5.1.1.1.1.3.1 Food

- 5.1.1.1.1.3.2 Beverage

- 5.1.1.1.1.3.3 Pharmaceutical

- 5.1.1.1.1.3.4 Cosmetics and Personal Care

- 5.1.1.1.1.3.5 Industrial

- 5.1.1.1.1.3.6 Other End-use Industry

- 5.1.1.1.1.1 By Material Type

- 5.1.1.1.2 Flexible Plastic Packaging

- 5.1.1.1.2.1 By Material Type

- 5.1.1.1.2.1.1 Polyethylene (PE)

- 5.1.1.1.2.1.2 Biaxially Oriented Polypropylene (BOPP)

- 5.1.1.1.2.1.3 Cast Polypropylene (CPP)

- 5.1.1.1.2.1.4 Other Material Types

- 5.1.1.1.2.2 By Product Type

- 5.1.1.1.2.2.1 Pouches and Bags

- 5.1.1.1.2.2.2 Films and Wraps

- 5.1.1.1.2.2.3 Other Product Types

- 5.1.1.1.2.3 By End-use Industry

- 5.1.1.1.2.3.1 Food

- 5.1.1.1.2.3.2 Beverage

- 5.1.1.1.2.3.3 Pharmaceutical

- 5.1.1.1.2.3.4 Cosmetics and Personal Care

- 5.1.1.1.2.3.5 Industrial

- 5.1.1.1.2.3.6 Other End-use Industry

- 5.1.1.1.2.1 By Material Type

- 5.1.1.1.1 Rigid Plastic Packaging

- 5.1.1.2 By Product Type

- 5.1.1.2.1 Bottles and Jars

- 5.1.1.2.2 Pouches and Bags

- 5.1.1.2.3 Bulk-Grade Products

- 5.1.1.2.4 Other Product Types

- 5.1.1.3 By End-use Industry

- 5.1.1.3.1 Food

- 5.1.1.3.2 Beverages

- 5.1.1.3.3 Cosmetics and Personal Care

- 5.1.1.3.4 Pharamceuticals

- 5.1.1.3.5 Industrial

- 5.1.1.3.6 Other End-use Industry

- 5.1.1.1 By Type

- 5.1.2 Paper Packaging

- 5.1.2.1 By Product Type

- 5.1.2.1.1 Folding Carton

- 5.1.2.1.2 Corrugated Boxes

- 5.1.2.1.3 Liquid Paperboard

- 5.1.2.1.4 Other Product Type

- 5.1.2.2 By End-use Industry

- 5.1.2.2.1 Food

- 5.1.2.2.2 Beverages

- 5.1.2.2.3 E-commerce

- 5.1.2.2.4 Other End-use Industry

- 5.1.2.1 By Product Type

- 5.1.3 Container Glass

- 5.1.3.1 By Color

- 5.1.3.1.1 Green

- 5.1.3.1.2 Amber

- 5.1.3.1.3 Flint

- 5.1.3.1.4 Other Colors

- 5.1.3.2 By End-use Industry

- 5.1.3.2.1 Food

- 5.1.3.2.2 Beverage

- 5.1.3.2.2.1 Alcoholic

- 5.1.3.2.2.2 Non-Alcoholic

- 5.1.3.2.3 Personal Care and Cosmetics

- 5.1.3.2.4 Pharmaceuticals (excluding Vials and Ampoules)

- 5.1.3.2.5 Perfumery

- 5.1.3.1 By Color

- 5.1.4 Metal Cans and Containers

- 5.1.4.1 By Material Type

- 5.1.4.1.1 Steel

- 5.1.4.1.2 Aluminum

- 5.1.4.2 By Product Type

- 5.1.4.2.1 Cans

- 5.1.4.2.2 Drums and Barrels

- 5.1.4.2.3 Caps and Closures

- 5.1.4.2.4 Other Product Type

- 5.1.4.3 By End-use Industry

- 5.1.4.3.1 Food

- 5.1.4.3.2 Beverage

- 5.1.4.3.3 Chemicals and Petroleum

- 5.1.4.3.4 Industrial

- 5.1.4.3.5 Paints and coatings

- 5.1.4.3.6 Other End-use Industry

- 5.1.4.1 By Material Type

- 5.1.1 Plastic Packaging

- 5.2 By Packaging Format

- 5.2.1 Flexible

- 5.2.2 Rigid

- 5.3 By End-use Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceuticals and Healthcare

- 5.3.4 Personal Care and Cosmetics

- 5.3.5 Industrial

- 5.3.6 E-commerce

- 5.3.7 Other End-use Industry

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level overview, Market level overview, Core segments, Financials as available, Strategic information, Market rank/share for key companies, Products and Services, and Recent developments)

- 6.4.1 International Paper Company

- 6.4.2 Smurfit WestRock

- 6.4.3 Amcor plc

- 6.4.4 Mondi plc

- 6.4.5 Ball Corporation

- 6.4.6 Crown Holdings Inc.

- 6.4.7 Sealed Air Corporation

- 6.4.8 Sonoco Products Company

- 6.4.9 Graphic Packaging International LLC

- 6.4.10 Greif Inc.

- 6.4.11 Silgan Holdings Inc.

- 6.4.12 AptarGroup Inc.

- 6.4.13 Huhtamaki Oyj

- 6.4.14 Tetra Pak International SA

- 6.4.15 CAN-PACK UK Ltd.

- 6.4.16 Ardagh Group S.A.

- 6.4.17 RPC Group Ltd.

- 6.4.18 Klckner Pentaplast Ltd.

- 6.4.19 Coveris Holdings S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

濕度控制包裝市場預測至2034年-按產品類型、材料、包裝形式、通路、最終用戶和地區分類的全球分析

濕度控制包裝市場預測至2034年-按產品類型、材料、包裝形式、通路、最終用戶和地區分類的全球分析 感官包裝市場:依技術、材料、感測器類型、包裝形式和應用分類-2026-2032年全球市場預測

感官包裝市場:依技術、材料、感測器類型、包裝形式和應用分類-2026-2032年全球市場預測 2026年全球包裝與標籤服務市場報告氣泡膜市場:2026-2032年全球市場預測(依材料、厚度、應用、最終用戶及通路分類)復古包裝市場:按材料、類型、最終用途、印刷技術和通路-2026-2032年全球預測紙質復古包裝市場:依材料、包裝類型、銷售管道、最終用戶、應用程式分類,全球預測(2026-2032)多功能零件市場按產品類型、價格範圍、應用、垂直產業和分銷管道分類,全球預測(2026-2032年)紙塑包裝器材市場:依機器類型、材料、操作類型和應用分類,全球預測(2026-2032年)

2026年全球包裝與標籤服務市場報告氣泡膜市場:2026-2032年全球市場預測(依材料、厚度、應用、最終用戶及通路分類)復古包裝市場:按材料、類型、最終用途、印刷技術和通路-2026-2032年全球預測紙質復古包裝市場:依材料、包裝類型、銷售管道、最終用戶、應用程式分類,全球預測(2026-2032)多功能零件市場按產品類型、價格範圍、應用、垂直產業和分銷管道分類,全球預測(2026-2032年)紙塑包裝器材市場:依機器類型、材料、操作類型和應用分類,全球預測(2026-2032年) 航太級包裝市場規模、佔有率、成長、產業分析,依材料、應用及區域預測 (~2034年)全球電子順磁共振波譜儀市場(按產品類型、頻率、工作模式、組件、應用和最終用戶分類)預測(2026-2032年)

航太級包裝市場規模、佔有率、成長、產業分析,依材料、應用及區域預測 (~2034年)全球電子順磁共振波譜儀市場(按產品類型、頻率、工作模式、組件、應用和最終用戶分類)預測(2026-2032年)