|

市場調查報告書

商品編碼

1939710

資料中心基礎設施管理(DCIM):市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031)Data Center Infrastructure Management (DCIM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

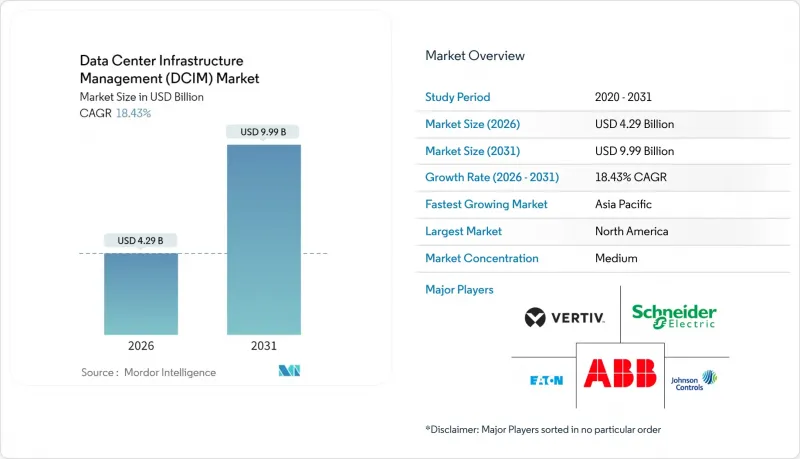

2025 年資料中心基礎設施管理 (DCIM) 市場價值為 36.2 億美元,預計到 2031 年將達到 99.9 億美元,高於 2026 年的 42.9 億美元。

預測期(2026-2031 年)的複合年成長率預計為 18.43%。

人工智慧驅動的熱負荷、歐盟強制性能源使用揭露以及全球範圍內單園區容量超過500兆瓦的超大規模計劃浪潮,共同推動了資料中心產業的成長。服務提供者正日益採用預測分析技術,以滿足網路保險的遙測要求,並將合規性轉化為可衡量的節能效果。由於資料中心營運商長期面臨設施工程師短缺的問題,與託管資料中心基礎設施管理 (DCIM) 相關的服務正經歷最快的成長。競爭的焦點在於能夠最佳化機架級冷卻、電力和資產利用率的整合式軟硬體組合。投資人正將資金籌措與檢驗的ESG 指標掛鉤,並將 DCIM 認證的能源效率作為新建設和維修的差異化優勢。

全球資料中心基礎設施管理 (DCIM) 市場趨勢與洞察

加速淨零排放和強制性能源資訊揭露

歐盟能源效率指令要求所有超過500kW的資料中心在2024年9月前揭露其電力使用效率(PUE)、碳使用效率(CUE)和水使用效率(WUE),這使得資料中心基礎設施管理(DCIM)從可選的最佳化軟體轉變為強制性的合規基礎。已實施即時DCIM的營運商報告稱,透過動態容量預測,節能高達18%,證明了監管投資的實際回報。跨國公司目前正在所有設施中採用相同的DCIM架構,以簡化永續性報告流程並避免區域性審核。隨著投資者要求統一的ESG資訊揭露,這項需求正在歐洲以外地區擴展。由於該指令也涵蓋了約佔歐盟電力消耗量3%的設施,因此效率的逐步提升將減輕全部區域電網的負擔。

超大規模叢集擴展至超過 500MW 規模

像指南針 Data Centers在密西西比州投資100億美元的園區級計劃這樣的大型投資項目,需要一個資料中心基礎設施管理(DCIM)平台來協調模組化電源和冷卻系統中的數千個機架。傳統的建築管理系統無法在千兆瓦級規模下提供機架級遙測或故障預測警報。與預製電源模組(例如與西門子簽訂的多年供應協議中的模組)的整合,可以加強DCIM軟體與電力基礎設施之間的連接。隨著資本密集度的增加,營運商優先考慮即時了解氣流和容量,以降低營運成本。超過500兆瓦的規模意味著必須將DCIM置於計劃可行性研究的核心位置。

持續OT-IT整合與傳統BMS重疊的複雜性

傳統建築管理系統通常依賴專有通訊協定,無法與現代資料中心基礎設施管理 (DCIM) API 互通。因此,營運商被迫部署冗餘的感測器和儀表板,導致資本支出和營運成本雙雙上升,卻無法建立統一的資產帳簿。客製化中間件計劃需要重新編碼才能升級,這會將部署週期延長數月,並增加生命週期成本。在多供應商環境中,每個機械設備供應商都可能將其功能鎖定在封閉式的工具鏈中,阻礙整體能源最佳化。

細分市場分析

預計業務收益將以22.99%的複合年成長率(CAGR)成長,因為58%的營運商表示難以招募合格的設施工程師。資產管理部署正從企劃為基礎的實施模式轉向包含持續最佳化服務的訂閱模式。託管服務也承擔了人工智慧叢集液冷迴路調校的複雜性。儘管解決方案在2025年仍佔資料中心基礎設施管理市場的65.55%,但基本契約的興起預示著以服務為中心的未來。企業傾向於透過外包感測器校準、韌體管理和合規性報告來控制人事費用。

隨著邊緣節點的擴展,對網路和連線管理能力的需求也隨之成長。同時,電源和冷卻管理在超大規模資料中心仍然至關重要,供應商正在提供加速器來整合傳統的建築管理系統 (BMS),從而為客戶提供統一的管理介面。這種演變凸顯了從一次性軟體授權轉向基於專業支援的經常性收入模式的策略轉變。

預計超大型資料中心(150MW 以上的園區)將以 21.74% 的複合年成長率成長,取代主導傳統雲端運算浪潮的大型資料中心。由於 GPU 互連的優勢遠大於延遲帶來的損失,營運商正在將 AI 訓練叢集集中化。超大型園區實現了規模經濟,允許多個機房共用液冷迴路,從而將冷卻設備的 PUE 值降低到 1.1 以下。隨著感測器數量達到數百萬,編配複雜性不斷增加,預計該領域的資料中心基礎設施管理 (DCIM) 市場規模將迅速擴張。

向超大型園區的轉型也將推動模組化電源撬裝設備和預製機房單元的創新,這些設備將部署經過工廠測試的資料中心基礎設施管理 (DCIM) 整合功能。小規模企業設施仍將繼續承擔對延遲敏感的工作負載,但預算限制將限制先進數位雙胞胎模組的採用。

資料中心基礎設施管理 (DCIM) 市場報告按資料中心規模(小規模、中型、其他)、部署類型(本地部署、託管)、元件(解決方案、服務)、最終用戶產業(IT 和電信、銀行、金融、保險 (BFSI)、其他)以及地區(北美、歐洲、其他)對產業進行分類。市場預測以美元計價。

區域分析

北美地區預計到2025年將佔全球收入的41.92%,這主要得益於超大規模資料中心的建設和人工智慧培訓中心的早期應用。當地業者正透過採用液冷數位雙胞胎,並將機架密度提升至50kW及以上,增加資料中心基礎設施管理(DCIM)方面的支出。聯邦和州政府的節能獎勵進一步強化了即時監控的商業價值。

預計到2031年,亞太地區的年複合成長率將達到34.12%,其中中國的目標是到2027年建成1,250億美元的資料中心經濟,而印度則在其「數位印度」計畫的推動下加速發展。日本面臨著全球最高的資料中心建置成本之一,這促使人們對自動化資料中心基礎設施管理(DCIM)越來越感興趣,以最大限度地提高每平方公尺的容量。新加坡和澳洲作為區域樞紐,提供跨境雲端服務,這些服務必須滿足各種不同的合規要求。

受能源效率指令的推動,歐洲市場持續穩定成長,營運商競相將資料中心基礎設施管理 (DCIM) 整合到現有設施維修和新建設中,以滿足 2024 年 9 月的報告截止日期。隨著區域雲端服務供應商將基礎設施在地化以降低延遲,中東和南美市場的需求也不斷成長。非洲仍處於發展中,但行動網際網路使用量的成長預計將推動輕量級 DCIM 的普及。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 加速實現淨零排放和強制揭露能源使用情況

- 叢集規模超過 500MW 的超大規模擴展

- 面向 5G/物聯網的邊緣和微型資料中心的激增

- 人工智慧/機器學習驅動的熱負荷需要即時CFD整合DCIM

- 基於資料中心基礎設施管理(DCIM)的風險遙測技術已成為網路保險保單的強制性要求。

- 評估經DCIM檢驗的效率指標的ESG關聯融資

- 市場限制

- 持續存在的OT-IT整合複雜性與傳統BMS重疊問題

- 關於雲端託管資料中心基礎設施管理平台的資料主權問題

- 缺乏精通資料中心整合管理(DCIM)的設施工程師

- AI機架密度提升速度超越了感測器網路維修

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 對宏觀經濟趨勢的市場評估

- 定價分析

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 資產和容量管理

- 電源和冷卻管理

- 網路和連線管理

- 服務

- 諮詢和系統整合

- 管理和支援服務

- 解決方案

- 按資料中心規模

- 小規模

- 中號

- 大規模

- 巨大的

- 百萬

- 透過部署模式

- 本地部署

- 搭配

- 零售

- 批發/超大規模託管

- 雲端/資料中心基礎設施管理即服務

- 按最終用戶行業分類

- 資訊科技和電信

- BFSI

- 醫療保健和生命科學

- 政府/國防

- 製造業和工業

- 零售與電子商務

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 新加坡

- 澳洲

- 馬來西亞

- 亞太其他地區

- 南美洲

- 巴西

- 智利

- 阿根廷

- 南美洲其他地區

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Schneider Electric SE

- Vertiv Group Corp.

- ABB Ltd

- Eaton Corporation plc

- Johnson Controls International plc

- IBM Corporation

- Siemens AG

- CommScope(Nlyte and iTRACS)

- Sunbird Software

- FNT GmbH

- Device42

- Panduit Corp.

- Cisco Systems Inc.

- Huawei Technologies Co. Ltd

- Raritan Inc.(Legrand)

- Siemens Smart Infrastructure

- EkkoSense Ltd

- RFcode Inc.

- Modius Inc.

- OpenDCIM(open-source)

第7章 市場機會與未來展望

The Data Center Infrastructure Management market was valued at USD 3.62 billion in 2025 and estimated to grow from USD 4.29 billion in 2026 to reach USD 9.99 billion by 2031, at a CAGR of 18.43% during the forecast period (2026-2031).

Growth is propelled by AI-driven thermal loads, mandatory energy-use disclosure rules in the European Union, and a global wave of hyperscale projects that now top 500 MW per campus. Providers increasingly embed predictive analytics to meet cyber-insurance telemetry requirements and to convert regulatory compliance into measurable energy savings. Services linked to managed DCIM operations are accelerating fastest because data-center operators face persistent shortages of facility engineers. Competitive activity centres on integrated hardware-software portfolios that optimise cooling, power, and asset utilisation at rack level. Investors are tying financing costs to verifiable ESG metrics, turning DCIM-verified efficiency into a differentiator for new builds and retrofits.

Global Data Center Infrastructure Management (DCIM) Market Trends and Insights

Accelerated Pursuit of Net-Zero and Mandatory Energy-Use Disclosure

The EU Energy Efficiency Directive requires all data centers above 500 kW to disclose Power Usage Effectiveness, Carbon Usage Effectiveness, and Water Usage Effectiveness by September 2024, repositioning DCIM from optional optimisation software to mandatory compliance infrastructure. Operators that deployed real-time DCIM report 18% energy savings through dynamic capacity forecasting, demonstrating tangible returns on regulatory spending. Multinationals now standardise identical DCIM stacks in every facility to streamline sustainability reporting and to avoid region-specific audits. Demand is spreading beyond Europe because investors demand harmonised ESG disclosures. The directive also covers centres consuming nearly 3% of EU electricity, so incremental efficiency gains translate into region-wide grid relief.

Hyperscale Build-Outs Exceeding 500 MW Clusters

Campus-scale investments such as Compass Datacenters' USD 10 billion Mississippi project require DCIM platforms that coordinate thousands of racks across modular power and cooling skids. Traditional building-management systems cannot deliver rack-level telemetry or predictive failure alerts at gigawatt scale. Integration with prefabricated power modules, exemplified by Siemens' multi-year supply agreement, tightens the link between DCIM software and electrical infrastructure. Operators prioritise real-time visualisation of airflow and capacity to shave operating expenses as capital intensity rises. The shift to 500 MW-plus footprints thus anchors DCIM at the heart of project feasibility studies.

Persistent OT-IT Integration Complexity and Legacy BMS Overlap

Legacy building-management systems often rely on proprietary protocols that do not interoperate with modern DCIM APIs. Operators then duplicate sensors and dashboards, inflating both capex and opex while still lacking a unified asset inventory. Custom middleware projects add months to deployment schedules and raise lifecycle costs because upgrades must be recoded. In multi-vendor estates, each mechanical contractor may lock functionality inside closed toolchains, hampering holistic energy optimisation.

Other drivers and restraints analyzed in the detailed report include:

- Edge and Micro-Data-Center Proliferation for 5G/IoT

- AI/ML-Driven Thermal Loads Demanding Real-Time CFD-Coupled DCIM

- Data-Sovereignty Worries About Cloud-Hosted DCIM Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services revenue is projected to climb at 22.99% CAGR because 58% of operators report difficulty hiring qualified facility engineers. Asset-management rollouts now shift from project-based implementations to subscription frameworks that bundle continuous optimisation. Managed services also absorb the complexity of tuning liquid-cooling loops that accompany AI clusters. Though Solutions held 65.55% of Data Center Infrastructure Management market share in 2025, the rise of outcome-based contracts points to a service-centric future. Enterprises prefer to cap labour overheads by outsourcing sensor calibration, firmware management, and compliance reporting.

Demand for Network and Connectivity Management functions also increases as edge nodes expand, while Power and Cooling Management stays critical for hyperscale sites. Vendors package integration accelerators that bridge legacy BMS so clients see a single pane of glass. The evolution underscores a strategic pivot from one-off software licences toward recurring revenue backed by expert support.

Mega facilities, defined as campuses above 150 MW, are expected to post a 21.74% CAGR, displacing Massive facilities that dominated earlier cloud waves. Operators centralise AI training clusters because GPU interconnect benefits outweigh latency penalties. Mega campuses unlock economies of scale, allowing liquid cooling loops to be shared across several halls and driving cooling plant efficiency below 1.1 PUE. The Data Center Infrastructure Management market size for this segment will expand rapidly as orchestration complexity multiplies with sensor counts running into millions.

The migration toward mega-scale campuses also seeds innovation in modular power skids and prefabricated hall segments that arrive with factory-tested DCIM integrations. Smaller enterprise facilities retain a role for latency-sensitive workloads, but budget constraints limit adoption of advanced digital-twin modules.

Data Center Infrastructure Management (DCIM) Market Report Segments the Industry Into Data Center Size(Small and Medium, and More), Deployment Type (On -Premise, Colocation), Component(solutions, Services), End-User Industry(IT and Telecom, BFSI and More) and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 41.92% of 2025 revenue thanks to hyperscale builds and early adoption of AI training centres. Operators there deploy liquid cooling and digital twins to push rack densities past 50 kW, amplifying DCIM spending. Federal and state energy-efficiency incentives further reinforce the business case for real-time monitoring.

Asia-Pacific is forecast to grow at 34.12% CAGR through 2031 as China targets a USD 125 billion data-center economy by 2027 and India accelerates under the Digital India initiative. Japan faces the world's highest construction costs, driving interest in automated DCIM to extract maximum capacity from every square metre. Singapore and Australia act as regional hubs, supplying cross-border cloud services that must meet diverse compliance mandates.

Europe maintains steady expansion on the back of the Energy Efficiency Directive. Operators race to meet September 2024 reporting deadlines, integrating DCIM into both brownfield retrofits and new builds. Middle Eastern and South American markets show rising demand as regional cloud providers localise infrastructure to cut latency. Africa remains nascent but is expected to adopt lightweight DCIM as mobile-internet use increases.

- Schneider Electric SE

- Vertiv Group Corp.

- ABB Ltd

- Eaton Corporation plc

- Johnson Controls International plc

- IBM Corporation

- Siemens AG

- CommScope (Nlyte and iTRACS)

- Sunbird Software

- FNT GmbH

- Device42

- Panduit Corp.

- Cisco Systems Inc.

- Huawei Technologies Co. Ltd

- Raritan Inc. (Legrand)

- Siemens Smart Infrastructure

- EkkoSense Ltd

- RFcode Inc.

- Modius Inc.

- OpenDCIM (open-source)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated pursuit of net-zero and mandatory energy-use disclosure

- 4.2.2 Hyperscale build-outs exceeding 500 MW clusters

- 4.2.3 Edge and micro-data-center proliferation for 5G/IoT

- 4.2.4 AI/ML-driven thermal loads demanding real-time CFD-coupled DCIM

- 4.2.5 Cyber-insurance policies now requiring DCIM-based risk telemetry

- 4.2.6 ESG-linked financing that scores DCIM-verified efficiency metrics

- 4.3 Market Restraints

- 4.3.1 Persistent OT-IT integration complexity and legacy BMS overlap

- 4.3.2 Data-sovereignty worries about cloud-hosted DCIM platforms

- 4.3.3 Shortage of DCIM-literate facility engineers

- 4.3.4 Rising AI rack densities outpacing sensor network retrofits

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macro Economic Trends on the Market

- 4.9 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Asset and Capacity Management

- 5.1.1.2 Power and Cooling Management

- 5.1.1.3 Network and Connectivity Management

- 5.1.2 Services

- 5.1.2.1 Consulting and Integration

- 5.1.2.2 Managed and Support Services

- 5.1.1 Solutions

- 5.2 By Data-Center Size

- 5.2.1 Small

- 5.2.2 Medium

- 5.2.3 Large

- 5.2.4 Massive

- 5.2.5 Mega

- 5.3 By Deployment Mode

- 5.3.1 On-premise

- 5.3.2 Colocation

- 5.3.2.1 Retail Colo

- 5.3.2.2 Wholesale / Hyperscale Colo

- 5.3.3 Cloud / DCIM-as-a-Service

- 5.4 By End-User Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Life-Sciences

- 5.4.4 Government and Defence

- 5.4.5 Manufacturing and Industrial

- 5.4.6 Retail and E-commerce

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Singapore

- 5.5.3.5 Australia

- 5.5.3.6 Malaysia

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Chile

- 5.5.4.3 Argentina

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirate

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Schneider Electric SE

- 6.4.2 Vertiv Group Corp.

- 6.4.3 ABB Ltd

- 6.4.4 Eaton Corporation plc

- 6.4.5 Johnson Controls International plc

- 6.4.6 IBM Corporation

- 6.4.7 Siemens AG

- 6.4.8 CommScope (Nlyte and iTRACS)

- 6.4.9 Sunbird Software

- 6.4.10 FNT GmbH

- 6.4.11 Device42

- 6.4.12 Panduit Corp.

- 6.4.13 Cisco Systems Inc.

- 6.4.14 Huawei Technologies Co. Ltd

- 6.4.15 Raritan Inc. (Legrand)

- 6.4.16 Siemens Smart Infrastructure

- 6.4.17 EkkoSense Ltd

- 6.4.18 RFcode Inc.

- 6.4.19 Modius Inc.

- 6.4.20 OpenDCIM (open-source)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026-2030年全球資料中心IT基礎設施市場

2026-2030年全球資料中心IT基礎設施市場 2026年全球資料中心(DCIM)服務市場報告

2026年全球資料中心(DCIM)服務市場報告 資料中心基礎設施市場:按組件、資料中心類型、產業和地區分類

資料中心基礎設施市場:按組件、資料中心類型、產業和地區分類 全球資料中心IT基礎設施市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球資料中心IT基礎設施市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 全球資料中心基礎設施管理 (DCIM) 市場預測至 2034 年:按元件、功能、部署類型、資料中心類型、應用程式、最終用戶和地區分類全球資料中心電氣基礎設施服務市場預測(至2034年),依電氣系統類型、等級分類、電力容量、資料中心類別、最終使用者和地區分類全球資料中心電氣設備試運行市場:預測(至 2034 年)—按試運行類型、試運行級別、電氣系統、資料中心類型、服務供應商類型、最終用戶和地區進行分析全球超大規模資料中心擴建市場:預測(至 2034 年)-按元件、資料中心類型、部署方式、IT 架構、最終使用者和區域進行分析

全球資料中心基礎設施管理 (DCIM) 市場預測至 2034 年:按元件、功能、部署類型、資料中心類型、應用程式、最終用戶和地區分類全球資料中心電氣基礎設施服務市場預測(至2034年),依電氣系統類型、等級分類、電力容量、資料中心類別、最終使用者和地區分類全球資料中心電氣設備試運行市場:預測(至 2034 年)—按試運行類型、試運行級別、電氣系統、資料中心類型、服務供應商類型、最終用戶和地區進行分析全球超大規模資料中心擴建市場:預測(至 2034 年)-按元件、資料中心類型、部署方式、IT 架構、最終使用者和區域進行分析 整合資料中心基礎設施市場 - 全球產業規模、佔有率、趨勢、機會及預測(按部署方式、組件、設施、地區和競爭格局分類),2021-2031年

整合資料中心基礎設施市場 - 全球產業規模、佔有率、趨勢、機會及預測(按部署方式、組件、設施、地區和競爭格局分類),2021-2031年 資料中心基礎設施市場規模、佔有率和成長分析(按產品、組件、資料中心、部署方式、企業規模、應用和地區分類)—產業預測,2026-2033年

資料中心基礎設施市場規模、佔有率和成長分析(按產品、組件、資料中心、部署方式、企業規模、應用和地區分類)—產業預測,2026-2033年