|

市場調查報告書

商品編碼

1939698

測試、檢驗和認證 (TIC):市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031)Testing, Inspection, And Certification - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

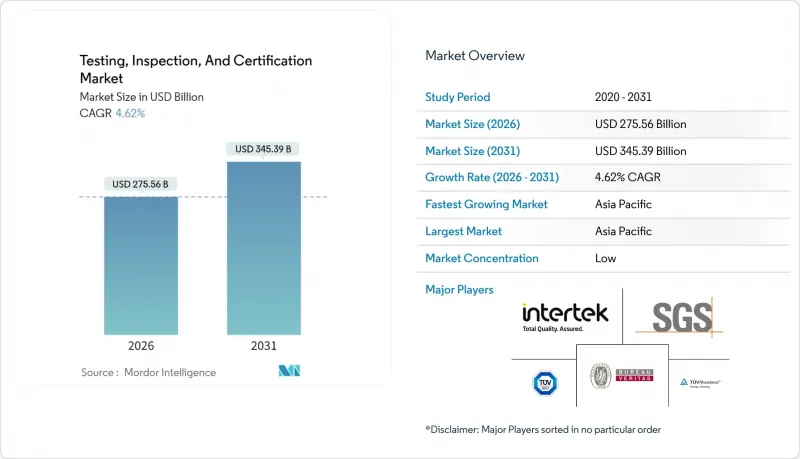

The testing inspection certification market is expected to grow from USD 263.40 billion in 2025 to USD 275.56 billion in 2026 and is forecast to reach USD 345.39 billion by 2031 at 4.62% CAGR over 2026-2031.

Escalating regulatory scrutiny, rising product-safety expectations, and digital transformation are strengthening demand for independent assurance services across consumer goods, electronics, energy storage, and automotive value chains. Mandatory ESG and carbon-footprint verification requirements, tighter cybersecurity rules for connected products, and the complexity of globalized supply networks are compelling firms to rely on accredited third parties. Strategic consolidation combined with AI-enabled inspection technologies is allowing market leaders to widen service scope and improve efficiency. At the same time, cost pressures and talent shortages in niche domains such as battery and 5G testing are forcing providers to invest in automation and workforce development to protect margins.

Global Testing, Inspection, And Certification Market Trends and Insights

Mandatory ESG / Carbon-Footprint Verification Accelerates Export Compliance

Global decarbonization policies are repositioning carbon-footprint certification from a voluntary gesture to a prerequisite for cross-border trade. The EU Carbon Border Adjustment Mechanism requires ISO 14067 product carbon-footprint verification and is encouraging exporters worldwide to secure accredited assurance. SGS has leveraged three decades of sustainability expertise to launch expanded verification programs, while Bureau Veritas has rolled out organization-level ESG certification suites. Integrated digital platforms, such as SGS's data-validation partnership with Worldly, couple continuous supply-chain emissions tracking with independent verification, aligning with regulators' preference for auditable, real-time evidence.

AI-Enabled Remote Monitoring Transforms Service Delivery Models

Artificial intelligence tools are automating repetitive visual checks, predicting equipment failures, and enabling continuous quality monitoring without on-site presence. Digital twins recreate physical assets virtually, permitting inspectors to identify anomalies and validate performance parameters in near real time. Major TIC providers report up to 50% cuts in field visits after adopting AI-supported image analytics and sensor fusion. Savings in travel time and faster feedback loops allow reallocation of skilled technicians to higher-value tasks while reducing customer downtime. Growing acceptance of remotely issued certificates by regulatory bodies in North America and Europe is accelerating the large-scale deployment of these platforms.

Margin Squeeze from Price Competition Pressures Traditional Models

Thousands of small laboratories compete in commoditized testing niches, eroding pricing power for routine chemical, materials, and consumer-product assays. Larger providers are responding by migrating toward subscription-based continuous-monitoring offers and data-rich ESG verification, aiming to shift customer conversations away from unit pricing toward value creation. However, building digital platforms, integrating IoT sensors, and training staff in data analytics entail substantial capital outlays that disproportionately burden mid-tier firms. The resulting cost-to-serve gap risks widening the divide between global leaders and regional specialists.

Other drivers and restraints analyzed in the detailed report include:

- Cyber-Physical Security Certification Drives IoT Testing Demand

- Global Supply-Chain Complexity Intensifies Third-Party Assurance

- Talent Shortages in Specialized Domains Constrain Growth

- Increase in Lead Times Due to Complex Global Supply Chains

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Testing accounted for 61.25% of the 2025 testing inspection certification market share, underlining its foundational role in product development and compliance cycles. Stringent automotive cybersecurity rules and complex 5G radio frequency characteristics are driving laboratories to invest in millimeter-wave chambers and over-the-air systems. The testing, inspection certification market size for battery evaluations is also expanding as UL Solutions extends laboratories near major EV production clusters to support thermal-runaway and vibration protocols.

Certification services, although smaller, are forecast to record the fastest 4.88% CAGR. New programs such as the Cyber Trust Mark require ISO/IEC 17065-accredited bodies to authorize cybersecurity labels, creating additional revenue streams for firms with the right accreditations. ESG standards linked to carbon-footprint verification further amplify demand, making certification a strategic priority for providers seeking margin-resilient growth. Inspection sits between the two segments, benefiting from supply-chain verification mandates yet facing substitution pressure from AI-enabled remote visual tools.

Outsourced services dominated the 2025 testing, inspection certification market, capturing a 74.65% share as manufacturers relied on third-party expertise to navigate proliferating standards. Independent labs offer scale advantages in capital-intensive domains such as electromagnetic compatibility and high-energy battery abuse testing, while their global footprint helps multinational clients harmonize compliance processes. The trend is strongest in consumer electronics, where rapid model refresh cycles favor external labs that maintain state-of-the-art facilities.

In-house programs remain essential for life-science, utility, and defense entities that insist on data confidentiality and operational control, but their market share is gradually eroding. Hybrid approaches are emerging: automotive OEMs retain design-validation benches yet outsource type-approval testing to accredited bodies for global market entry, illustrating how internal oversight and external certification can coexist to optimize resources.

The Testing, Inspection, and Certification Market Report is Segmented by Service Type (Testing, Inspection, and Certification), Sourcing Type (In-House, and Outsourced), Industry Vertical (Consumer Goods and Retail, ICT and Telecom, and More), Mode of Service Delivery (On-Site, Off-site/Laboratory, and Remote/Digital), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific remains the fulcrum of demand with a 47.05% share in 2025 and is expected to grow at a rapid rate of 5.28% during the forecast period. The region is mainly driven by expanding manufacturing footprints in China, India, Vietnam, and Indonesia, and by progressively stringent domestic standards across electronics, automotive, and renewables. International TIC groups have ramped up laboratory investments near EV battery gigafactories in the region to meet escalating local certification requirements. Rising middle-income consumption is also raising awareness of product-safety labels, accelerating market penetration for third-party assurance providers.

North America holds the second-largest slice of the testing, inspection certification market, supported by robust aerospace, medical-device, and advanced electronics sectors. The Cyber Trust Mark shows regulatory willingness to pioneer voluntary cybersecurity labeling, stimulating lab accreditation in wireless, cryptography, and over-the-air testing. Food safety continues to underpin steady inspection volumes as importers seek Qualified Importer Certification to unlock expedited FDA clearance.

Europe benefits from a dense regulatory framework that integrates ESG, cybersecurity, and automotive functional-safety directives. The continent's leadership in circular-economy measures, such as the EU Deforestation Regulation and CBAM, pushes exporters worldwide to obtain verified sustainability certificates. UNECE's R155 and R156 rules for automotive cybersecurity and software update management have spawned new homologation programs, prompting TIC providers to establish specialized tracks for threat analysis, penetration testing, and secure update validation.

- SGS SA

- Bureau Veritas SA

- Intertek Group plc

- TUV SUD AG

- TUV Rheinland AG

- TUV NORD GROUP

- DEKRA SE

- UL Solutions Inc.

- DNV AS

- Applus Servicios Tecnologicos S.A.

- Eurofins Scientific SE

- ALS Limited

- Kiwa N.V.

- Lloyd's Register Group Limited

- RINA S.p.A.

- Element Materials Technology Group

- Centre Testing International Group Co. Ltd.

- SAI Global Pty Ltd

- MISTRAS Group Inc.

- NSF International

- BSI Group (The British Standards Institution)

- Cotecna Inspection SA

- SOCOTEC Group SA

- FLOCERT GmbH

- Perry Johnson Registrars Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing regulatory compliance and product-safety mandates

- 4.2.2 Expansion of global supply chains demanding third-party assurance

- 4.2.3 Surge in consumer electronics and IoT product launches

- 4.2.4 AI-enabled remote and continuous monitoring platforms

- 4.2.5 Mandatory ESG / carbon-footprint verification in export markets

- 4.2.6 Cyber-physical security certification for connected products

- 4.3 Market Restraints

- 4.3.1 Margin squeeze from price competition

- 4.3.2 Trade frictions and divergent national standards

- 4.3.3 OEM self-certification via digital twins

- 4.3.4 Talent shortages in niche test domains (battery, 5G, biotech)

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Testing

- 5.1.2 Inspection

- 5.1.3 Certification

- 5.2 By Sourcing Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.3 By Industry Vertical

- 5.3.1 Consumer Goods and Retail

- 5.3.2 ICT and Telecom

- 5.3.3 Automotive and Transportation

- 5.3.4 Aerospace and Defense

- 5.3.5 Oil, Gas and Petrochemicals

- 5.3.6 Energy and Utilities

- 5.3.7 Industrial Manufacturing and Machinery

- 5.3.8 Chemicals and Materials

- 5.3.9 Construction and Infrastructure

- 5.3.10 Life Sciences and Healthcare

- 5.3.11 Food, Agriculture and Beverage

- 5.3.12 Others (Environment, Sustainability, etc.)

- 5.4 By Mode of Service Delivery

- 5.4.1 On-site

- 5.4.2 Off-site/Laboratory

- 5.4.3 Remote / Digital

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 South-East Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SGS SA

- 6.4.2 Bureau Veritas SA

- 6.4.3 Intertek Group plc

- 6.4.4 TUV SUD AG

- 6.4.5 TUV Rheinland AG

- 6.4.6 TUV NORD GROUP

- 6.4.7 DEKRA SE

- 6.4.8 UL Solutions Inc.

- 6.4.9 DNV AS

- 6.4.10 Applus Servicios Tecnologicos S.A.

- 6.4.11 Eurofins Scientific SE

- 6.4.12 ALS Limited

- 6.4.13 Kiwa N.V.

- 6.4.14 Lloyd's Register Group Limited

- 6.4.15 RINA S.p.A.

- 6.4.16 Element Materials Technology Group

- 6.4.17 Centre Testing International Group Co. Ltd.

- 6.4.18 SAI Global Pty Ltd

- 6.4.19 MISTRAS Group Inc.

- 6.4.20 NSF International

- 6.4.21 BSI Group (The British Standards Institution)

- 6.4.22 Cotecna Inspection SA

- 6.4.23 SOCOTEC Group SA

- 6.4.24 FLOCERT GmbH

- 6.4.25 Perry Johnson Registrars Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

自主測試與檢驗系統市場預測至2034年:按組件、測試類型、組織規模、部署模式、最終用戶和地區分類的全球分析

自主測試與檢驗系統市場預測至2034年:按組件、測試類型、組織規模、部署模式、最終用戶和地區分類的全球分析 2026年全球測試、檢驗和認證市場報告

2026年全球測試、檢驗和認證市場報告 全球測試、檢驗和認證 (TIC) 市場:按服務類型、來源和應用分類 - 預測(至 2031 年)

全球測試、檢驗和認證 (TIC) 市場:按服務類型、來源和應用分類 - 預測(至 2031 年) 測試與試運行市場報告:按服務類型、試運行類型、採購方式、最終用戶行業和地區分類(2026-2034 年)

測試與試運行市場報告:按服務類型、試運行類型、採購方式、最終用戶行業和地區分類(2026-2034 年) 熱交換器檢測服務市場規模、佔有率和成長分析:按檢測技術、應用和地區分類-2026-2033年產業預測2026年全球醫療設備測試、檢驗及認證市場報告

熱交換器檢測服務市場規模、佔有率和成長分析:按檢測技術、應用和地區分類-2026-2033年產業預測2026年全球醫療設備測試、檢驗及認證市場報告 測試、檢驗及認證服務市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、最終使用者、流程、部署模式及設備分類

測試、檢驗及認證服務市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、最終使用者、流程、部署模式及設備分類 食品檢測設備市場:依產品(X光系統、金屬探測器、檢重秤、視覺系統)、食品類別(肉類、乳製品、烘焙產品、水果和蔬菜、飲料)及產業劃分-全球預測至2036年日本測試試運行市場規模、佔有率、趨勢及預測(按服務類型、試運行類型、採購類型、最終用途領域和地區分類),2026-2034年

食品檢測設備市場:依產品(X光系統、金屬探測器、檢重秤、視覺系統)、食品類別(肉類、乳製品、烘焙產品、水果和蔬菜、飲料)及產業劃分-全球預測至2036年日本測試試運行市場規模、佔有率、趨勢及預測(按服務類型、試運行類型、採購類型、最終用途領域和地區分類),2026-2034年 OFTEC 測試服務市場:按服務類型、設備類型、測試模式和最終用戶分類,全球預測,2026-2032 年

OFTEC 測試服務市場:按服務類型、設備類型、測試模式和最終用戶分類,全球預測,2026-2032 年