|

市場調查報告書

商品編碼

1939669

語音辨識:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Voice Recognition - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

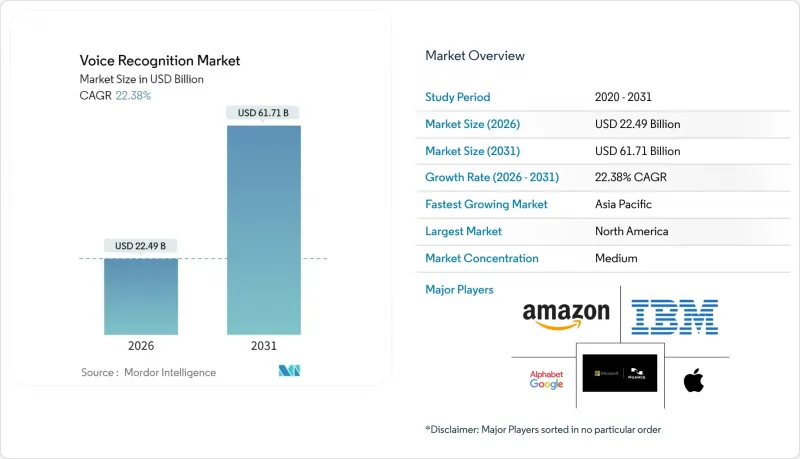

2025年全球語音辨識市場價值為183.9億美元,預計2031年將達到617.1億美元,而2026年為224.9億美元。

預測期(2026-2031 年)的複合年成長率預計為 22.38%。

市場擴張反映了三大因素的共同作用:邊緣人工智慧 (AI) 晶片組的快速普及、監管機構對緊急通訊網路現代化施加的壓力,以及企業轉向語音生物識別技術進行客戶身份驗證。目前,以軟體為中心的架構佔據主導地位,70.7% 的市場佔有率集中在軟體開發工具包 (SDK) 和應用程式介面 (API) 平台。同時,到 2024 年,62.1% 的部署將雲端部署。從區域來看,亞洲將在 2024 年佔據榜首,市佔率達到 32.5%,這主要得益於對多語言介面的需求以及強大的晶片製造生態系統。雖然語音辨識技術仍是主導技術平台,市佔率高達 81.2%,但設備端處理將實現 25% 的複合年成長率,這標誌著從純雲設計到混合或完全本地推理引擎的決定性轉變。

全球語音辨識市場趨勢與洞察

亞洲邊緣設備語音AI晶片激增

Chipintelli發表14款離線AI語音晶片,以及聯發科推出MR Breeze ASR 25型號,都顯示企業正在加速投資研發針對區域語言最佳化的專用晶片。在地化技術能夠降低延遲,解決與雲端串流相關的隱私問題,並鞏固傳統上依賴北美超大規模資料中心業者的國內供應鏈。亞洲半導體公司正利用這一優勢,透過向設備OEM廠商提供可處理印尼、越南和印度等市場語碼切換的承包語音協定棧,來鞏固該地區在邊緣推理創新領域的領先地位。

北美地區加強對語音911和緊急呼叫系統的監管

美國聯邦通訊委員會 (FCC) 的新規要求美國通訊業者使用基於 IP 的對話啟動協定(SIP) 路由 911 緊急呼叫,在 165 公尺半徑範圍內以 90% 的可靠性降低誤路由,並支援即時文字和視訊。專注於緊急服務的語音辨識供應商預計將實現收入成長,因為國家和區域層面的合規期限將在未來 6-12 個月內設定。這項強制性規定樹立了一個模板,很可能也會影響歐洲的公共網路,從而擴大對語音分析的潛在需求。語音分析技術能夠利用轉錄音訊和元資料來豐富事件資料。

口音和方言識別方面的挑戰阻礙了其在非洲的廣泛應用。

93種非洲口音的測試表明,醫療實體識別錯誤率仍需提高25%至34%。 NaijaVoices的1800小時資料集將Whisper模型的字詞辨識錯誤率降低了75.86%,但建構文化豐富的語料庫的成本和複雜性阻礙了其商業部署。 Intron Health的160萬美元種子輪融資顯示投資者已意識到這個問題,同時也凸顯了在地化模型訓練的高額資金需求。

細分市場分析

預計到2025年,雲端服務將佔全球收入的61.60%,隨著企業優先考慮快速部署、持續模型更新和廣泛的語言支持,這一比例預計還將繼續成長。金融機構和醫療保健提供者擴大選擇混合架構,將原始資料保留在本地,同時在雲端共用模型訓練結果。這種方法在合規性和集中式學習帶來的表現提升之間取得了平衡。因此,本地部署對於滿足企業自主資料需求仍然至關重要,這將推動該領域在2031年之前保持兩位數的持續成長。

對高可用性語音終端日益成長的需求正促使超大規模資料中心業者提供承包API,從而降低中型企業的整體擁有成本 (TCO),並降低獨立開發者的准入門檻。這正在擴大語音辨識市場的應用範圍,使其從消費性設備擴展到流程自動化、物流和現場服務工作流程等領域。預計到2031年,雲端語音辨識市場規模將接近385億美元,這反映了新增工作負載和現有部署的成長。

到2025年,軟體平台將佔全球支出的70.05%,這一關鍵差異推動了產業從專有硬體向模組化、開發者友善工具的轉型。 RESTful API和預先建構語言模型的普及,使得許多應用場景不再需要客製化晶片。服務領域雖然規模較小,但正以23.20%的複合年成長率快速成長,因為企業擴大將網域最佳化、語音辨識和安全合規等工作外包給專業供應商。

硬體在邊緣延遲、離線可用性和聲波束成形至關重要的領域(例如汽車資訊娛樂和工業頭戴式顯示器)仍然佔有一席之地,但許多新進入者正在透過使用平台即服務 (PaaS) 解決方案來繞過硬體,這表明橫向軟體提供商和垂直整合的硬體專家之間的差距正在擴大。

語音辨識市場依部署類型(雲端/本地部署)、組件(軟體/SDK、硬體、服務)、技術(語音辨識、語音生物識別、邊緣語音AI)、裝置類型(智慧型手機、智慧音箱、車載設備、穿戴式裝置、POS機)、應用程式(身分驗證、語音搜尋等)、終端用戶市場預測以美元以金額為準。

區域分析

到2025年,亞洲將佔全球收入的32.10%,這反映了該地區的半導體製造能力和語言多樣性。各國國內政策都在支持人工智慧的應用,例如日本資助東南亞語言模式的舉措。北美仍然是這項技術的早期採用者,但由於積極的本地化和低成本設備,其市場佔有率已被亞洲蠶食。歐洲則在汽車和銀行、金融服務及保險(BFSI)產業應用日益廣泛,推動了其穩定成長。

中東地區以22.60%的複合年成長率領跑,這主要得益於海灣國家智慧城市規劃,這些規劃將對話式自助服務終端融入了市民服務基礎設施。南美洲的成長率也達到了15%左右,這主要得益於語音搜尋在電子商務和銀行身分驗證領域的廣泛應用。非洲的成長相對滯後,因為各地口音的多樣性使得建構統一的模式變得複雜,但捐助者資助的語言計劃和通訊基礎設施升級有望從2027年起釋放市場需求潛力。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 亞洲邊緣設備語音AI晶片激增

- 北美地區加強對語音911和緊急呼叫系統的監管

- 汽車製造商轉向嵌入式語音操作系統以實現駕駛座個性化

- 歐洲銀行、金融服務和保險 (BFSI) 產業採用語音生物識別取代基於知識的身份驗證

- 智慧音箱家庭中語音商務的快速普及

- 亞太新興市場對多語言語音使用者體驗的需求日益成長

- 市場限制

- 口音和方言辨識方面的差距限制了非洲地區的普及。

- 隱私法規(GDPR、印度資料保護資料保護法)限制了雲端語音資料保存。

- 標註特定領域語音語料庫的高成本

- 在吵雜的工業環境中,精度持續下降

- 價值/供應鏈分析

- 監理展望

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

第5章 市場規模與成長預測

- 透過部署

- 雲

- 本地部署

- 按組件

- 軟體/SDK

- 硬體(ASIC、DSP、麥克風陣列)

- 服務(託管服務和專業服務)

- 透過技術

- 語音辨識

- 語音認證/語音生物識別

- 嵌入式/邊緣語音人工智慧

- 依設備類型

- 智慧型手機和平板電腦

- 智慧音箱和顯示器

- 汽車資訊娛樂和遠端資訊處理

- 穿戴式裝置(全無線耳機、智慧型手錶、AR/VR)

- 商用自助服務終端和POS機

- 透過使用

- 身份驗證和安全

- 語音搜尋和語音指令

- 轉錄和字幕

- 虛擬助理和聊天機器人

- 醫療文件

- 終端用戶產業

- 車

- 銀行和金融服務

- 溝通

- 醫療保健提供者

- 政府和國防部

- 家用電子電器

- 零售與電子商務

- 工業和製造業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 澳洲

- 紐西蘭

- 亞太其他地區

- 中東和非洲

- 中東

- GCC

- 土耳其

- 以色列

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Apple Inc.

- Alphabet Inc.(Google LLC)

- Amazon.com Inc.

- Nuance Communications Inc.(Microsoft)

- IBM Corporation

- Baidu Inc.

- Samsung Electronics Co. Ltd.

- SoundHound AI Inc.

- iFLYTEK Co. Ltd.

- Sensory Inc.

- Cerence Inc.

- Verint Systems Inc.

- NICE Ltd.

- ElevenLabs

- Auraya Systems Pty Ltd.

- Intron Health

- PlayAI

- Mobvoi Information Technology Co. Ltd.

- Deepgram Inc.

- AssemblyAI Inc.

- Speechmatics Ltd.

第7章 市場機會與未來展望

The global voice recognition market was valued at USD 18.39 billion in 2025 and estimated to grow from USD 22.49 billion in 2026 to reach USD 61.71 billion by 2031, at a CAGR of 22.38% during the forecast period (2026-2031).

Market expansion reflects three concurrent forces: the rapid roll-out of edge artificial intelligence (AI) chipsets, regulatory pressure for modernising emergency communications networks, and enterprise migration to voice biometrics for customer authentication. Software-centric architectures now dominate because 70.7% of market value sits in software development kits and application-programming-interface platforms, while cloud deployment accounts for 62.1% of implementations in 2024. Regionally, Asia led with 32.5% market share in 2024 on the back of multilingual interface demand and strong chip manufacturing ecosystems; speech recognition technology remained the principal technology pillar with 81.2% share, yet embedded on-device processing delivered the fastest 25% CAGR, showing a decisive shift from cloud-only designs to hybrid or fully local inference engines.

Global Voice Recognition Market Trends and Insights

Explosion of Voice-AI Chips in Edge Devices across Asia

The release of 14 offline AI speech chips by Chipintelli and MediaTek's MR Breeze ASR 25 model signal escalating investment in specialised silicon optimised for regional languages. Localisation delivers lower latency, resolves privacy concerns tied to cloud streaming, and entrenches domestic supply chains that historically depended on North American hyperscalers. Asian semiconductor firms leverage this advantage to offer device OEMs turnkey voice stacks that handle code-switching in markets such as Indonesia, Vietnam, and India, reinforcing the region's leadership in edge inference innovation.

Regulatory Push for Voice-Enabled 911 and Emergency Dispatch Upgrades in North America

New FCC rules obligate US carriers to route 911 calls via IP-based Session Initiation Protocol, cut misrouting below a 165-meter radius at 90% confidence, and support real-time text and video. Voice recognition vendors positioned around emergency services gain a predictable revenue ramp because compliance deadlines fall within a 6-12-month horizon for nationwide and regional operators. The mandate creates a template likely to influence European public safety networks, expanding total addressable demand for voice analytics that enrich incident data with transcribed speech and metadata.

Accent and Dialect Recognition Gaps Limiting Adoption in Africa

Tests across 93 African accents showed medical entity error rates that still required 25-34% refinement via accent-specific fine-tuning. NaijaVoices' 1,800-hour dataset cut word-error rates for Whisper models by 75.86%, but the cost and complexity of curating culturally rich corpora slow commercial roll-outs. Intron Health's USD 1.6 million seed round underlines investor recognition of the problem, yet it also highlights the capital demands of localised model training.

Other drivers and restraints analyzed in the detailed report include:

- Automotive OEM Shift to Embedded Voice OS for Cockpit Personalisation

- BFSI Adoption of Voice Biometrics to Replace Knowledge-Based Authentication in Europe

- Privacy Regulations (GDPR, India DPDP) Restricting Cloud Voice-Data Retention

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud delivery generated 61.60% of global revenue in 2025, and that share is projected to widen as enterprises prioritise rapid rollout, continuous model updates, and broad language coverage. Financial institutions and healthcare providers increasingly select hybrid architectures that keep raw recordings on premises but pool model-training insights in the cloud. The approach balances compliance with the performance gains of aggregated learning. On-premise deployments therefore remain relevant for sovereign-data mandates, explaining why the segment still posts double-digit growth through 2031.

Demand for high-availability voice endpoints has pushed hyperscalers to expose turnkey APIs. Consequently, total cost of ownership falls for mid-sized enterprises, and barriers to entry lower for independent developers. The result is a wider application funnel for voice recognition market adoption, extending beyond consumer devices into process automation, logistics, and field-service workflows. The voice recognition market size for cloud implementations is set to approach USD 38.5 billion by 2031, reflecting both new workloads and expansion of existing deployments.

Software platforms captured 70.05% of global spend in 2025, a decisive margin that underpins the industry's pivot from proprietary hardware to modular, developer-friendly tooling. The availability of RESTful APIs and pre-built language models removes the need for bespoke silicon in many use cases. Services, although representing a smaller base, rise at 23.20% CAGR as enterprises engage specialist vendors for domain tuning, accent adaptation, and security compliance.

Hardware maintains relevance where edge latency, offline availability, or acoustic beam-forming matter, such as in automotive infotainment or industrial head-mounted displays. Yet most new entrants bypass hardware by consuming platform-as-a-service offerings, illustrating an expanding gap between horizontally oriented software providers and vertically integrated hardware specialists.

Voice Recognition Market is Segmented by Deployment (Cloud, On-Premise), Component (Software/SDK, Hardware, Services), Technology (Speech Recognition, Voice Biometrics, Edge Voice AI), Device Type (Smartphones, Smart Speakers, Automotive, Wearables, POS), Application (Authentication, Voice Search, and More), End-User Vertical (Automotive, BFSI, and Morel), and by Geography. Market Forecasts in Value (USD).

Geography Analysis

Asia generated 32.10% of 2025 turnover, reflecting the region's semiconductor capacity and linguistic diversity. Domestic policy supports AI acceleration; Japan's initiative to fund Southeast Asian language models is one example. North America remains technology's early-adopter hub but ceded share to Asia because of aggressive localisation and lower device costs. Europe grew steadily, influenced by automotive and BFSI thematic adoption.

The Middle East exhibits the quickest 22.60% CAGR as Gulf smart-city programmes embed conversational kiosks in citizen-services infrastructure. South America records mid-teens growth from e-commerce voice search and banking authentication. Africa faces a lag because accent diversity complicates universal models; however, donor-funded language projects and telecom upgrades may unlock latent demand from 2027 onward.

- Apple Inc.

- Alphabet Inc. (Google LLC)

- Amazon.com Inc.

- Nuance Communications Inc. (Microsoft)

- IBM Corporation

- Baidu Inc.

- Samsung Electronics Co. Ltd.

- SoundHound AI Inc.

- iFLYTEK Co. Ltd.

- Sensory Inc.

- Cerence Inc.

- Verint Systems Inc.

- NICE Ltd.

- ElevenLabs

- Auraya Systems Pty Ltd.

- Intron Health

- PlayAI

- Mobvoi Information Technology Co. Ltd.

- Deepgram Inc.

- AssemblyAI Inc.

- Speechmatics Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosion of Voice-AI Chips in Edge Devices across Asia

- 4.2.2 Regulatory Push for Voice-Enabled 911 and Emergency Dispatch Upgrades in North America

- 4.2.3 Automotive OEM Shift to Embedded Voice OS for Cockpit Personalisation

- 4.2.4 BFSI Adoption of Voice Biometrics to Replace Knowledge-Based Authentication in Europe

- 4.2.5 Rapid Proliferation of Voice Commerce in Smart-Speaker Centric Households

- 4.2.6 Growth of Multilingual Voice UX Demand in Emerging APAC Markets

- 4.3 Market Restraints

- 4.3.1 Accent and Dialect Recognition Gaps Limiting Adoption in Africa

- 4.3.2 Privacy Regulations (GDPR, India DPDP) Restricting Cloud Voice Data Retention

- 4.3.3 High Cost of Annotated Domain-Specific Speech Corpora

- 4.3.4 Persistent Accuracy Lags in Noisy Industrial Environments

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 Cloud

- 5.1.2 On-premise

- 5.2 By Component

- 5.2.1 Software/SDK

- 5.2.2 Hardware (ASIC, DSP, Microphone Arrays)

- 5.2.3 Services (Managed and Professional)

- 5.3 By Technology

- 5.3.1 Speech Recognition

- 5.3.2 Speaker/Voice Biometrics

- 5.3.3 Embedded/Edge Voice AI

- 5.4 By Device Type

- 5.4.1 Smartphones and Tablets

- 5.4.2 Smart Speakers and Displays

- 5.4.3 Automotive Infotainment and Telematics

- 5.4.4 Wearables (TWS, Smart-watch, AR/VR)

- 5.4.5 Commercial Kiosks and POS

- 5.5 By Application

- 5.5.1 Authentication and Security

- 5.5.2 Voice Search and Command

- 5.5.3 Transcription and Captioning

- 5.5.4 Virtual Assistants and Chatbots

- 5.5.5 Medical Documentation

- 5.6 By End-user Vertical

- 5.6.1 Automotive

- 5.6.2 Banking and Financial Services

- 5.6.3 Telecommunications

- 5.6.4 Healthcare Providers

- 5.6.5 Government and Defence

- 5.6.6 Consumer Electronics

- 5.6.7 Retail and E-commerce

- 5.6.8 Industrial and Manufacturing

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 United Kingdom

- 5.7.3.2 Germany

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Rest of Europe

- 5.7.4 Asia Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South Korea

- 5.7.4.5 ASEAN

- 5.7.4.6 Australia

- 5.7.4.7 New Zealand

- 5.7.4.8 Rest of Asia Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 GCC

- 5.7.5.1.2 Turkey

- 5.7.5.1.3 Israel

- 5.7.5.1.4 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Nigeria

- 5.7.5.2.3 Egypt

- 5.7.5.2.4 Rest of Africa

- 5.7.5.1 Middle East

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)}

- 6.4.1 Apple Inc.

- 6.4.2 Alphabet Inc. (Google LLC)

- 6.4.3 Amazon.com Inc.

- 6.4.4 Nuance Communications Inc. (Microsoft)

- 6.4.5 IBM Corporation

- 6.4.6 Baidu Inc.

- 6.4.7 Samsung Electronics Co. Ltd.

- 6.4.8 SoundHound AI Inc.

- 6.4.9 iFLYTEK Co. Ltd.

- 6.4.10 Sensory Inc.

- 6.4.11 Cerence Inc.

- 6.4.12 Verint Systems Inc.

- 6.4.13 NICE Ltd.

- 6.4.14 ElevenLabs

- 6.4.15 Auraya Systems Pty Ltd.

- 6.4.16 Intron Health

- 6.4.17 PlayAI

- 6.4.18 Mobvoi Information Technology Co. Ltd.

- 6.4.19 Deepgram Inc.

- 6.4.20 AssemblyAI Inc.

- 6.4.21 Speechmatics Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

人工智慧語音辨識晶片市場報告:趨勢、預測與競爭分析(至2035年)

人工智慧語音辨識晶片市場報告:趨勢、預測與競爭分析(至2035年) 語音辨識市場:依技術、組件、部署模式、應用程式和最終用戶類型分類-2026-2032年全球市場預測語音軟體演算法市場:按服務、演算法類型和部署方式分類-2026-2032年全球市場預測

語音辨識市場:依技術、組件、部署模式、應用程式和最終用戶類型分類-2026-2032年全球市場預測語音軟體演算法市場:按服務、演算法類型和部署方式分類-2026-2032年全球市場預測 語音辨識市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、設備、部署、最終用戶、解決方案

語音辨識市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、設備、部署、最終用戶、解決方案 2026年全球語音技術市場報告2026年全球語音支付軟體市場報告2026年全球語音辨識市場報告2026年全球語音辨識與語音辨識市場報告2026年全球行動語音辨識軟體市場報告

2026年全球語音技術市場報告2026年全球語音支付軟體市場報告2026年全球語音辨識市場報告2026年全球語音辨識與語音辨識市場報告2026年全球行動語音辨識軟體市場報告 全球語音辨識(SR/VR)市場規模、佔有率、趨勢和成長分析報告:2026-2034年

全球語音辨識(SR/VR)市場規模、佔有率、趨勢和成長分析報告:2026-2034年