|

市場調查報告書

商品編碼

1939657

窗膜:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Window Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

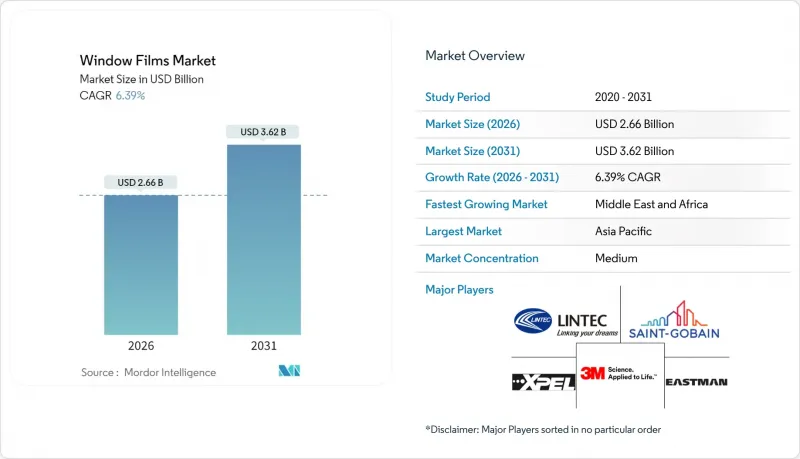

預計到 2026 年,窗膜市值將達到 26.6 億美元,高於 2025 年的 25 億美元。

預計到 2031 年將達到 36.2 億美元,2026 年至 2031 年的複合年成長率為 6.39%。

市場需求正從基本的太陽能控制轉向兼具能源管理、安全性和互聯性等優勢的多功能薄膜,推動了汽車、建築和特種應用領域的應用。淨零排放建築的強制性要求正在加速維修活動,而不斷成長的電動車保有量和快速的玻璃更換週期也支撐了汽車行業的需求。供應商正在推出奈米陶瓷和低輻射結構,這些結構既符合嚴格的節能標準,又不會影響5G駕駛輔助系統所需的無線電波滲透性。亞太地區仍然是生產和消費中心,但中東和非洲地區正在崛起成為成長最快的地區,沙烏地阿拉伯和阿拉伯聯合大公國的大型計劃正在採用電塗裝玻璃。儘管面臨來自電致變色智慧玻璃和低成本通用薄膜日益成長的競爭壓力,但主要現有企業仍透過創新和區域產能擴張來鞏固其市場地位,因此市場集中度仍保持在中等水平。

全球窗膜市場趨勢與洞察

安全防護膜的需求不斷成長

人們對活躍威脅場景的日益關注推動了24密耳厚安全層壓膜的應用,這種薄膜能夠在強行闖入或爆炸中有效阻擋玻璃碎片。承包商擴大指定使用多層胺甲酸乙酯結構,這種結構比傳統的聚酯產品具有更優異的抗撕裂性和邊緣抓力。設施管理人員讚賞這種產品能夠同時提供防入侵和紫外線防護功能,從而在單一產品中同時解決安全和節能方面的挑戰。颶風易發地區的保險折扣也進一步促進了維修活動。隨著相關人員尋求經濟高效的外部加固方案,這項技術正從高風險的政府設施擴展到學校、零售連鎖店和綜合用途大樓。製造商正在積極響應這一趨勢,推出符合ANSI Z97.1和EN 12600衝擊測試標準的安全薄膜,進一步鞏固了其在全球建築規範中的重要性。

淨零排放指令促進節能隔熱膜的應用

歐盟建築能源性能指令和加州第24號法規對玻璃的熱傳導係數(U值)和太陽能熱增益係數進行了規定,鼓勵業主對現有窗戶維修,而不是進行高成本的更換。高性能太陽能控制薄膜可以即時提升能源性能證書,幫助房地產投資組合實現其2030年脫碳目標。奈米陶瓷配方在降低紅外線透射率的同時保留自然光,使其成為以健康為導向的室內設計中的關鍵元素。智慧光致變色薄膜的研究原型表明,當與低輻射(Low-E)雙層玻璃結合使用時,預計將年度能源消耗降低高達35%。卷對捲製造技術使其價格與電致變色玻璃相當,有望使這種薄膜成為數百萬尋求提高能源效率的建築的主流維修解決方案。

技術安裝難題和保固問題

先進的多層薄膜需要完美的表面處理、濕度控制和精準的刮塗技術。施工人員技術水平的差異會導致氣泡、邊緣翹起和光學霧化,從而引發保固糾紛,尤其是在對價格敏感的新興市場。行業協會已發布視覺品質標準,但執行力度仍參差不齊。製造商的回應是提供更多認證課程和預裁套件,但這推高了分銷成本,並限制了客製化解決方案。在汽車售後市場,複雜的曲面增加了施工難度,延長了施工時間,一旦出現缺陷,就會引發消費者不滿。

細分市場分析

到2025年,隔熱和防紫外線薄膜將佔窗膜市場40.89%的佔有率,鞏固其作為領先的維修方案的地位,可即時降低熱量吸收並提升居住者舒適度。由於人們越來越意識到其在家具、藝術品和汽車內裝方面的防褪色性能,銷售業績強勁。高階奈米陶瓷產品因其色彩還原度高且在惡劣氣候條件下也具有良好的耐久性,推高了平均售價。結合頻譜選擇性塗層和裝飾圖案的混合型產品正在市場上湧現,滿足了零售商在不犧牲性能的前提下對品牌差異化的需求。供應商正在推廣非金屬化層壓結構,以避免對連網建築和車輛造成無線電干擾。

受淨零排放政策目標和中緯度地區供暖度日數增加的推動,隔熱/低輻射(Low-E)產品預計將在2031年之前以7.26%的複合年成長率快速成長。多層濺鍍層壓結構可減少傳導和輻射損失,使單層玻璃窗的性能指標接近雙層玻璃,而更換成本卻遠低於雙層玻璃。在溫帶地區,該產品的投資回收期不到三年,促使設施管理人員在維修B級辦公大樓時廣泛採用。雖然隨著建築規範的日益嚴格,隔熱/低輻射(Low-E)窗膜市場預計將快速成長,但由於製造流程複雜和安裝要求高,其應用仍然主要局限於專業管道。裝飾性、隱私和安全等細分市場繼續滿足酒店、醫療保健和關鍵基礎設施等行業的特殊需求。

區域分析

亞太地區將引領市場,到2025年將佔全球收入的45.84%,主要得益於中國在建築占地面積和汽車生產方面的雙重優勢。日本和韓國雄心勃勃的建築節能法規正在推動高階低輻射(Low-E)和智慧薄膜的安裝,而印度和東南亞國協由於快速的都市化,在較低的基數上實現了兩位數的成長。本地價值鏈提供了具有競爭力的成本優勢,大型跨國公司在中國和新加坡擴大大規模生產能力便是最好的證明。區域分銷商正在將薄膜與遮陽裝置和建築自動化感測器結合,以凸顯建築幕牆的整體價值提案。

預計到2031年,中東和非洲地區的複合年成長率將達到6.83%,成為成長最快的地區,這主要得益於沙烏地阿拉伯「2030願景」計劃的推動。這些項目必須承受極端的太陽輻射,同時也要符合LEED或Estidama綠建築標準。利雅德和杜拜的開發商正在指定使用高選擇性薄膜來控制空調成本,同時保持現代建築標誌性的大面積玻璃建築幕牆。技術純熟勞工短缺和建築材料需求旺盛可能會限制施工能力,因此供應商正在實施加速培訓計劃,以培訓安裝人員並對大型企劃的分包商進行資格預審。

北美和歐洲是成熟市場,其成長依賴於建築規範驅動的維修以及對高階市場的滲透。儘管宏觀經濟波動,但需求依然強勁,這主要得益於歐盟強制要求到2030年維修至少16%的商業建築存量。美國各州的深度節能維修獎勵提供了穩定的專案來源,而企業脫碳承諾也持續推動市場發展。南美洲的普及速度較為緩慢,經濟週期和貨幣波動抑制了投資,但聖保羅和聖地牙哥等都市區已採用更高的玻璃標準,這為中等性能薄膜創造了機會。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 安全防護膜的需求不斷成長

- 淨零排放指令推動節能隔熱的發展

- 加速汽車售後市場的玻璃更換週期

- 資料中心外牆維修迅速增加,旨在阻擋紅外線

- 購買抗颶風薄膜可享保險折扣

- 市場限制

- 安裝過程中的技術和保固問題

- 與電致變色智慧玻璃的競爭

- 限制溶劑型黏合劑的VOC排放法規

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按類型

- 隔熱和紫外線阻隔膜

- 裝飾膜

- 安全保障影片

- 防窺膜

- 隔熱/低輻射薄膜

- 其他

- 按最終用戶行業分類

- 車

- 建築/施工

- 海洋

- 航太

- 其他

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 土耳其

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 奈及利亞

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率/排名分析

- 公司簡介

- 3M

- Armolan Greece

- Avery Dennison Corporation

- Eastman Chemical Company

- Erickson International, LLC

- Garware Hi-Tech Films.

- HYOSUNG CHEMICAL

- Johnson Window Films Inc.

- Lintec Corporation

- Madico

- Nexfil

- Rayno Window Film

- Saint-Gobain

- TORAY INDUSTRIES INC.

- WINTECH CO., LTD.

- XPEL

第7章 市場機會與未來展望

Window Films market size in 2026 is estimated at USD 2.66 billion, growing from 2025 value of USD 2.50 billion with 2031 projections showing USD 3.62 billion, growing at 6.39% CAGR over 2026-2031.

Strong demand pivots from basic solar control toward multi-functional films that combine energy management, safety, and connectivity benefits, increasingly specified in automotive, building, and specialty applications. Net-zero building mandates accelerate retrofit activity, while an expanding electric-vehicle (EV) fleet and rapid glazing replacement cycles keep automotive volumes buoyant. Suppliers are introducing nanoceramic and low-emissivity constructions that meet stringent energy-code requirements without compromising the radio-wave transparency required for 5G-enabled driver-assistance systems. Asia-Pacific remains the production and consumption hub, yet Middle-East and Africa emerges as the fastest-growing geography as mega-projects in Saudi Arabia and the UAE embrace high-performance glazing. Market concentration stays moderate because leading incumbents defend their positions through innovation and regional capacity expansion, even as electrochromic smart glass and low-cost commodity films intensify competitive pressure.

Global Window Films Market Trends and Insights

Growing demand for safety and security films

Heightened awareness of active-threat scenarios drives wider adoption of 24-mil security laminates that retain glass fragments during forced entry or blast events. Installers are increasingly specifying multi-layer urethane constructions that surpass legacy polyester products in terms of tear resistance and edge-grip performance. Facility managers value the ability to combine intrusion mitigation with UV filtration, allowing a single product to address both safety and energy challenges. Insurance premium rebates in hurricane-prone regions further stimulate retrofit activity. The technology is migrating from high-risk government sites into schools, retail chains, and mixed-use towers as stakeholders seek cost-effective envelope hardening. Manufacturers answer the trend with security films certified under ANSI Z97.1 and EN 12600 impact protocols, reinforcing their relevance in global building codes.

Net-zero mandates driving energy-saving solar-control films

The EU Energy Performance of Buildings Directive and California's Title 24 cap glazing U-factor and solar heat-gain coefficients, pushing owners to upgrade existing windows rather than pursue costly replacements. High-performance solar-control films demonstrate immediate Energy Performance Certificate uplifts, enabling property portfolios to meet 2030 decarbonization targets. Nanoceramic formulations cut infrared transmittance while preserving daylight, an important factor in wellness-oriented interior design. Research prototypes of smart photochromic films indicate potential annual energy-use reductions of up to 35% when paired with low-E double glazing. Roll-to-roll manufacturing keeps price points competitive against electrochromic glass, positioning films as the mainstream retrofit path for millions of buildings needing efficiency gains.

Technical and warranty issues during installation

Advanced multi-layer films require pristine surface preparation, controlled humidity, and precise squeegee techniques. Variations in installer skill create bubbles, edge lift, and optical haze that trigger warranty disputes, particularly in price-sensitive emerging markets. Trade associations publish visual-quality standards, yet enforcement remains uneven. Manufacturers answer with expanded certification courses and pre-cut kits, but these initiatives raise channel costs and limit bespoke solutions. In the automotive aftermarket, compound curves amplify complexity, prolonging installation time and inviting consumer dissatisfaction when defects appear.

Other drivers and restraints analyzed in the detailed report include:

- Rapid glazing replacement cycle in automotive aftermarket

- Insurance-premium rebates for hurricane-resistant films

- VOC-emission regulations limiting solvent-based adhesives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solar-control and UV-blocking constructions retained a 40.89% slice of the window films market in 2025, confirming their status as the go-to retrofit option for instant heat-gain reduction and occupant comfort. Strong sales track widespread awareness of fading protection in furniture, artworks, and automotive interiors. Premium nanoceramic variants command higher average selling prices thanks to neutral color rendition and longevity in harsh climates. The market now witnesses hybrid products that fuse spectrally selective coatings with decorative patterns, appealing to retail storefronts seeking brand differentiation without sacrificing performance. Suppliers promote metallized-free stacks to avert radio interference in connected buildings and vehicles.

Insulating/low-E products post the fastest 7.26% CAGR through 2031, buoyed by net-zero policy targets and rising heating-degree-day counts in mid-latitude regions. Their multi-layer sputtered stacks cut conducted and radiative losses, allowing single-pane windows to approach double-pane performance metrics at a fraction of replacement cost. Demonstrated payback periods of three years or less in temperate zones catalyze adoption among facility managers retrofitting Class-B office stock. The window films market size for insulating/low-E solutions is projected to surge as building codes tighten, yet production complexity and higher installation skill requirements still confine uptake to professional channels. Decorative, privacy and safety niches continue serving specialized demand pockets in hospitality, healthcare and critical-infrastructure verticals.

The Window Films Market Report is Segmented by Type (Solar-Control and UV-Blocking Films, Decorative Films, Safety and Security Films, Privacy Films, Insulating/Low-E Films, Others), End-User Industry (Automotive, Building and Construction, Marine, Aerospace, Others), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led with 45.84% of 2025 global revenue, thanks to China's dual dominance in construction floor space and vehicle production. Ambitious building-energy regulations in Japan and South Korea propel premium low-E and smart-film installations, while India and ASEAN nations show double-digit growth off lower bases as urbanization surges. Local supply chains grant competitive cost positions, evidenced by large-scale capacity additions in China and Singapore announced by major multinationals. Regional distributors bundle films with shading devices and building-automation sensors, highlighting holistic facade value propositions.

Middle-East and Africa records the highest 6.83% CAGR through 2031, underpinned by Saudi Vision 2030 giga-projects that must endure extreme solar loads and meet LEED or Estidama green-building criteria. Developers in Riyadh and Dubai specify high-selectivity films to curb HVAC bills while preserving expansive glass facades emblematic of contemporary architecture. Skilled-labor shortages and competing construction material demand occasionally constrain installation capacity, prompting suppliers to train applicators under accelerated programs and pre-qualify subcontractors for mega-project packages.

North America and Europe constitute mature arenas where growth relies on code-driven retrofits and premium segment penetration. The EU's mandate to refurbish the worst-performing 16% of commercial stock by 2030 keeps demand resilient despite macroeconomic swings. U.S. state-level incentives for deep-energy retrofits feed a steady pipeline, and corporate decarbonization pledges extend momentum. South America follows with moderate uptake as economic cycles and currency volatility temper investment, yet urban centers such as Sao Paulo and Santiago adopt higher glazing standards that open opportunities for mid-tier performance films.

- 3M

- Armolan Greece

- Avery Dennison Corporation

- Eastman Chemical Company

- Erickson International, LLC

- Garware Hi-Tech Films.

- HYOSUNG CHEMICAL

- Johnson Window Films Inc.

- Lintec Corporation

- Madico

- Nexfil

- Rayno Window Film

- Saint-Gobain

- TORAY INDUSTRIES INC.

- WINTECH CO., LTD.

- XPEL

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for safety and security films

- 4.2.2 Net-zero mandates driving energy-saving solar-control films

- 4.2.3 Rapid glazing replacement cycle in automotive aftermarket

- 4.2.4 Surge in data-centre facade retrofits for Infrared rejection

- 4.2.5 Insurance-premium rebates for hurricane-resistant films

- 4.3 Market Restraints

- 4.3.1 Technical and warranty issues during installation

- 4.3.2 Competition from electro-chromic smart glass

- 4.3.3 VOC-emission regulations limiting solvent-based adhesives

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Solar-control and UV-blocking Films

- 5.1.2 Decorative Films

- 5.1.3 Safety and Security Films

- 5.1.4 Privacy Films

- 5.1.5 Insulating/Low-E Films

- 5.1.6 Others

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.2 Building and Construction

- 5.2.3 Marine

- 5.2.4 Aerospace

- 5.2.5 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Nordic Countries

- 5.3.3.7 Russia

- 5.3.3.8 Turkey

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Nigeria

- 5.3.5.6 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share**/Ranking Analysis

- 6.4 Company Profiles (includes Global overview, Market overview, Core segments, Financials, Strategic info, Market share, Products and Services, Recent developments)

- 6.4.1 3M

- 6.4.2 Armolan Greece

- 6.4.3 Avery Dennison Corporation

- 6.4.4 Eastman Chemical Company

- 6.4.5 Erickson International, LLC

- 6.4.6 Garware Hi-Tech Films.

- 6.4.7 HYOSUNG CHEMICAL

- 6.4.8 Johnson Window Films Inc.

- 6.4.9 Lintec Corporation

- 6.4.10 Madico

- 6.4.11 Nexfil

- 6.4.12 Rayno Window Film

- 6.4.13 Saint-Gobain

- 6.4.14 TORAY INDUSTRIES INC.

- 6.4.15 WINTECH CO., LTD.

- 6.4.16 XPEL

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

窗膜市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年

窗膜市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年 窗膜市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年

窗膜市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年 窗膜市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場分類的預測(2026-2033 年)

窗膜市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場分類的預測(2026-2033 年) 建築窗膜市場規模、佔有率、成長及全球市場分析:按類型、應用和地區分類,並提供2026-2034年的洞察與預測

建築窗膜市場規模、佔有率、成長及全球市場分析:按類型、應用和地區分類,並提供2026-2034年的洞察與預測 全球節能窗膜市場(按薄膜類型、應用和分銷管道分類)預測(2026-2032年)

全球節能窗膜市場(按薄膜類型、應用和分銷管道分類)預測(2026-2032年) 2026年全球建築窗膜市場報告2026年全球窗膜市場報告

2026年全球建築窗膜市場報告2026年全球窗膜市場報告 全球窗膜市場,2026-2030年過渡性窗膜市場按技術、應用、終端用戶產業和分銷管道分類-2026-2032年全球預測全球窗膜市場:市場規模、市場佔有率、成長率、產業分析、按類型、應用和地區劃分的分析以及未來預測(2026-2034)

全球窗膜市場,2026-2030年過渡性窗膜市場按技術、應用、終端用戶產業和分銷管道分類-2026-2032年全球預測全球窗膜市場:市場規模、市場佔有率、成長率、產業分析、按類型、應用和地區劃分的分析以及未來預測(2026-2034)