|

市場調查報告書

商品編碼

1939644

車載資訊服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Telematics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

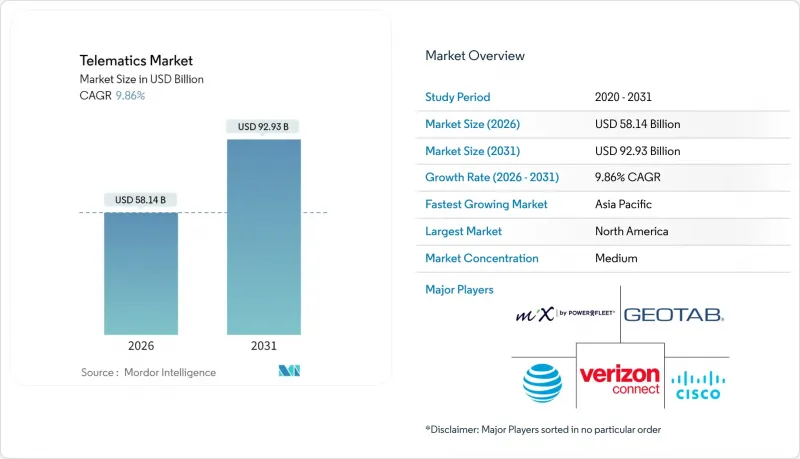

2025 年,車載資訊服務市場價值 529.3 億美元,預計到 2031 年將達到 929.3 億美元,而 2026 年為 581.4 億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 9.86%。

監管要求,特別是歐洲的eCall和印度的AIS 140,正迫使汽車製造商和車隊營運商在工廠層面就將互聯功能整合到車輛中,從而加速了原始設備製造商(OEM)的需求。預計到2030年,每輛車的半導體數量將加倍,這將推高硬體成本,但同時也將支援豐富的資料流,進而推動進階分析。利用即時駕駛數據的基於使用量的保險計劃正在北美和歐洲迅速發展,進一步增強了聯網汽車的商業價值。 5G和邊緣運算的快速普及正在將車載資訊服務從簡單的車輛追蹤轉變為預測性維護和車聯網(V2X)。根據聯合國歐洲經濟委員會(UNECE)WP.29和ISO/SAE 21434標準,網路安全合規成本的不斷攀升給小型供應商帶來了壓力,但也為資金雄厚的公司提供了競爭優勢。

全球車載資訊服務市場趨勢與洞察

擴大的OEM嵌入式連線義務

為了遵守新的資料共用法規,例如將於2025年生效的歐盟《資料法案》,汽車製造商正將車載資訊系統直接整合到車輛電子設備中。該法案要求製造商向第三方服務供應商開放車輛資料。 Geotab與沃爾沃汽車的合作使其OEM整合範圍擴展至157個品牌,這顯示嵌入式連接技術的快速普及。分析師估計,互聯服務預計將為每輛車帶來1,600美元的收入,這促使汽車製造商將數據視為新的收入來源。像WirelessCar這樣的專業供應商現在提供工具包,幫助OEM廠商落實數據法規,並加快了採用速度。日益嚴格的法規正在推動工廠出貨時裝載單元的標準化,並縮小售後市場規模,從而整合車載資訊系統市場。

自2025年起,基於使用量的保險普及率將大幅提升。

保險公司正利用即時駕駛數據,從基於人口統計的定價模式轉向行為模式的定價模式。 Intuit 將 Zendrive 的分析功能整合到其 Credit Karma 應用中,計劃到 2025 年向 600 萬會員發送 400 萬份保單報價,這表明該技術已被廣泛接受。起亞汽車和 LexisNexis 在歐盟 27 國推出了駕駛員評分共用服務,簡化了客戶註冊流程,同時確保符合 GDPR 法規。安全駕駛員可獲得高達 30% 的保費折扣,這不僅刺激了消費者需求,還有助於保險公司降低賠付率。 Cambridge Mobile Telematics 增加了燃油消耗評級,顯示保險公司現在除了獎勵安全駕駛外,也獎勵環保節能駕駛。這些發展正在加強數據驅動的承保業務,並加速遠端資訊處理市場的成長。

網路安全應對成本不斷上升

聯合國歐洲經濟委員會 (UNECE) WP.29 要求汽車製造商在車輛整個生命週期內運行經認證的網路安全管理系統。合規要求持續監控、事件報告和安全更新管道,這會增加工程成本並延長開發週期。 ISO/SAE 21434 增加了生命週期風險管理程序,而美國目前禁止從某些國家採購聯網汽車零件,並強制要求進行供應鏈審核。哈曼等供應商提供諮詢服務,幫助原始設備製造商 (OEM) 獲得認證,這表明合規正在從一項工程任務轉變為支出。小型供應商可能難以承擔這些成本,這可能會減緩新進入遠端資訊處理市場的企業的速度。

細分市場分析

到2025年,售後市場解決方案將佔據車載資訊服務市場56.30%的佔有率,這反映了其在售後市場和混合車隊中的歷史地位。到2031年,OEM系統將以11.62%的複合年成長率快速成長,這標誌著市場正朝著工廠互聯的方向發展,從而實現更清晰的數據流和無縫的保固整合。車載資訊服務市場受益於這種雙管道結構,因為新車出廠時就已整合,而老舊車輛仍需加裝設備。

儘管售後市場緊急呼叫(eCall)的監管標準化將使第三方供應商保持競爭力,但諸如歐盟資料法等原始設備製造商(OEM)資料共用規則更有利於嵌入式通路。隨著汽車製造商將聯網汽車訂閱服務商業化,下游價值獲取將會增加,從而降低售後市場的利潤率。因此,供應商正在加強其分析能力和多車隊管理能力,以維持其在車載資訊服務市場的地位。

至2025年,嵌入式單元將佔車載資訊服務市場規模的47.80%,年複合成長率(CAGR)高達12.94%,成為成長最快的細分市場。這項轉變主要受多種因素驅動,例如預測性維護、電動車電池管理以及監管資料共用義務等,這些因素需要深度整合到車輛中。基於智慧型手機的解決方案也能為對成本敏感的車隊提供價值,但它們在效能和資料精度方面不如嵌入式架構。

車隊營運商更傾向於使用嵌入式硬體進行關鍵任務分析,例如智慧充電演算法,該演算法可將電動車隊的能源成本降低 55%。隨著 5G 模組的標準化,嵌入式解決方案將成為 V2X 和高精度定位等高階應用的主流選擇,從而鞏固其在車載資訊服務市場的戰略地位。

區域分析

預計到2025年,歐洲將以31.95%的市場佔有率引領遠端資訊處理市場,這主要得益於強制性的eCall指令、GDPR的保護以及預計到2028年將達到2760萬套車隊管理設備的安裝基礎。歐盟將於2025年生效的資料保護法預計將強制要求資料共用,從而在保障隱私保護的同時,催生新一輪的第三方服務浪潮。為了滿足更嚴格的整合和合規要求,供應商正在為其連接套件建立品牌,例如大陸集團的「Aumovio」。

亞太地區是成長最快的地區,預計到2031年將維持12.26%的複合年成長率。印度的AIS 140強制令以及政府10億盧比(約1200萬美元)的地理空間投資將擴大基礎地圖基礎設施。中國新的駕駛輔助安全法規也提高了整車製造商的互聯互通標準。快速的都市化和龐大的商用車保有量正在創造需求,促使全球供應商與當地企業建立夥伴關係,並擴大全部區域的遠端資訊處理市場規模。

北美市場雖已成熟,但仍在持續成長,這主要得益於政府車隊的大規模應用,包括電子記錄設備(ELD)的強制實施以及美國總務管理局與Geotab簽訂的部署40萬輛政府車輛的合約。預計到2028年,美洲地區的車隊管理車輛數量將達到4,300萬輛。限制某些外國製造零件的供應鏈安全法規可能會增加硬體成本,但也可能促進國內半導體投資,為遠端資訊處理市場帶來長期的供應穩定性。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 擴大OEM嵌入式連接性要求

- 預計從2025年起,基於使用量的保險(UBI)的採用率將大幅成長。

- 政府電子呼叫和AIS 140法規

- 支援 5G/Edge 的空中下載 (OTA) 分析

- 車隊電氣化需要即時電池分析

- 旅遊即服務 (MaaS) 平台的興起

- 市場限制

- 網路安全回應成本不斷增加

- TCU*硬體價格在初始部署階段波動性較大

- 多司法管轄區資料主權障礙

- 現有商用車隊的慣性

- 產業價值鏈分析

- 監管環境

- 技術展望

- ポーターの五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按頻道

- 原始設備製造商 (OEM)

- 售後市場

- 透過解決方案

- 嵌入式

- スマートフォンベース

- 可攜式/プラグイン

- 提供形態別

- 硬體

- サービス- エントリーレベル

- サービス- ミッドティア

- 高階服務

- 按車輛類型

- 搭乘用車

- 小型商用車(LCV)

- 大型商用車(HCV)

- 透過使用

- 車隊管理

- 保険テレマティクス

- 予知保全および診断

- ナビゲーションおよびインフォテインメント

- 汽車共享和訂閱服務

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞洲地區

- 中東

- 以色列

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 北美洲

第6章 競合情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Verizon Communications Inc.(Verizon Connect)

- Geotab Inc.

- Trimble Inc.

- TomTom NV

- MiX Telematics Ltd

- ATandT Inc.

- Cisco Systems Inc.

- LG Electronics Inc.

- Continental AG

- Robert Bosch GmbH

- ZF Friedrichshafen AG

- Harman International Industries Inc.

- Valeo SA

- Inseego Corp.(Ctrack)

- Microlise Group PLC

- Aplicom Oy

- Huawei Technologies Co. Ltd.

- Sierra Wireless Inc.

- Octo Telematics SpA

- CalAmp Corp.

第7章 市場機會與未來展望

The telematics market was valued at USD 52.93 billion in 2025 and estimated to grow from USD 58.14 billion in 2026 to reach USD 92.93 billion by 2031, at a CAGR of 9.86% during the forecast period (2026-2031).

Regulatory mandates, especially eCall in Europe and AIS 140 in India, are compelling automakers and fleets to embed connectivity at the factory level, which accelerates OEM demand. Semiconductor content per vehicle is set to double by 2030, raising hardware costs yet enabling richer data streams that underpin advanced analytics. Usage-based insurance programs, powered by real-time driving data, are expanding quickly across North America and Europe, reinforcing the business case for connected cars. Rapid adoption of 5G and edge computing is transforming telematics from simple tracking to predictive maintenance and vehicle-to-everything communication. Rising cybersecurity compliance costs under UNECE WP.29 and ISO/SAE 21434 are pressuring smaller vendors but giving well-capitalized players a competitive edge.

Global Telematics Market Trends and Insights

Expanding OEM-embedded connectivity mandates

Automakers are integrating telematics directly into vehicle electronics to meet new data-sharing rules such as the EU Data Act, which applies from 2025 and obliges manufacturers to open vehicle data to third-party service providers. Geotab's collaboration with Volvo Cars lifts its OEM integrations to more than 157 brands, proving that embedded connectivity is scaling quickly. Analysts estimate connected services could yield USD 1,600 revenue per car, incentivizing automakers to treat data as a profit center. Specialized vendors like WirelessCar now offer compliance toolkits that help OEMs operationalize the Data Act, accelerating rollout timelines. As regulations tighten, factory-fitted units are becoming standard, shrinking the addressable aftermarket and reshaping the telematics market.

Usage-based insurance adoption surging post-2025

Insurance carriers are shifting from demographic to behaviour-based pricing, fuelled by real-time driving data. Intuit embedded Zendrive analytics into the Credit Karma app, sending 4 million policy offers to its 6 million members in 2025, which demonstrates mainstream scale. Kia and LexisNexis rolled out driver-score sharing in 27 EU countries, simplifying customer enrolment while preserving GDPR compliance. Safe drivers can secure premium cuts of up to 30%, boosting consumer demand and improving loss ratios for insurers. Cambridge Mobile Telematics added fuel consumption scoring, proving that insurers now value eco-efficient driving as well as safety. These advances reinforce data-centric underwriting and amplify the telematics market's growth.

Escalating cybersecurity compliance cost

UNECE WP.29 obliges automakers to operate certified Cyber Security Management Systems across the vehicle lifecycle. Compliance demands continuous monitoring, incident reporting and secure update channels, which raises engineering costs and lengthens development cycles. ISO/SAE 21434 adds lifecycle risk-management steps, while the U.S. now blocks connected-vehicle components sourced from certain countries, forcing supply-chain audits. Vendors like HARMAN have built consulting practices to help OEMs navigate certification, showing that compliance is transforming from an engineering task to a line-item expense. Smaller suppliers may struggle to shoulder these costs, slowing new-entrant momentum within the telematics market.

Other drivers and restraints analyzed in the detailed report include:

- Government eCall and AIS 140 regulations

- 5G/edge-enabled over-the-air analytics

- High upfront TCU hardware price volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Aftermarket solutions held 56.30% of the telematics market share in 2025, reflecting their historical role in retrofits and mixed fleets. OEM systems are scaling faster at an 11.62% CAGR to 2031, signalling a pivot toward factory-installed connectivity that delivers cleaner data streams and seamless warranty integration. The telematics market benefits from this dual-channel structure because older vehicles still need retrofit devices, while new cars roll off the line connected.

Regulatory standardization of aftermarket eCall ensures that third-party providers remain relevant, yet OEM data-sharing rules like the EU Data Act favour embedded channels. As automakers commercialize connected-car subscriptions, they capture more downstream value, narrowing the aftermarket's margin pool. Providers are thus emphasizing analytics and cross-fleet compatibility to preserve their position in the telematics market.

Embedded units accounted for 47.80% of the telematics market size in 2025 and exhibit the highest growth at a 12.94% CAGR. The shift is propelled by predictive maintenance, battery management in EVs, and regulatory data-sharing obligations that all require deep vehicle integration. Smartphone-based offerings remain viable in cost-sensitive fleets, but performance and data fidelity lag behind embedded architectures.

Fleet operators prefer embedded hardware for mission-critical analytics such as smart charging algorithms that cut energy expenses by 55% in electric fleets. As 5G modules become standard, embedded solutions will dominate advanced applications like V2X and high-accuracy positioning, cementing their strategic weight in the telematics market.

The Telematics Market Report is Segmented by Channel (OEM, and Aftermarket), Solution (Embedded, Smartphone-Based, Portable/Plug-in), Offering Type (Hardware, Services - Entry-Level, Services - Mid-Tier, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Application (Fleet Management, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe led the telematics market with a 31.95% share in 2025, underpinned by mandatory eCall, GDPR protections, and an installed base of 27.6 million fleet management units projected by 2028. The EU Data Act, effective in 2025, compels data sharing and is expected to stimulate a new wave of third-party services while maintaining privacy safeguards. Suppliers are branding connectivity suites, such as Continental's Aumovio, to meet tighter integration and compliance demands.

Asia-Pacific is the fastest-growing region, forecast at a 12.26% CAGR through 2031. India's AIS 140 mandate and the government's geospatial investment of INR 100 crore (USD 12 million) will broaden foundational mapping infrastructure. China's new driver-assistance safety rules also raise the bar for OEM connectivity. Rapid urbanization and large commercial fleets create volume, pulling global vendors into local partnerships and expanding the telematics market size across the region.

North America maintains a mature but still growing base, helped by ELD mandates and sizeable government-fleet deployments such as the US General Services Administration's 400,000-vehicle contract with Geotab. Fleet management units in the Americas are projected to reach 43 million by 2028. Supply-chain security rules limiting certain foreign components could elevate hardware costs yet may also spur domestic chip investments that stabilize long-term supply for the telematics market.

- Verizon Communications Inc. (Verizon Connect)

- Geotab Inc.

- Trimble Inc.

- TomTom N.V.

- MiX Telematics Ltd

- ATandT Inc.

- Cisco Systems Inc.

- LG Electronics Inc.

- Continental AG

- Robert Bosch GmbH

- ZF Friedrichshafen AG

- Harman International Industries Inc.

- Valeo SA

- Inseego Corp. (Ctrack)

- Microlise Group PLC

- Aplicom Oy

- Huawei Technologies Co. Ltd.

- Sierra Wireless Inc.

- Octo Telematics S.p.A.

- CalAmp Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding OEM-embedded connectivity mandates

- 4.2.2 Usage-based insurance (UBI) adoption surging post-2025

- 4.2.3 Government eCall and AIS 140 regulations

- 4.2.4 5G/edge-enabled over-the-air (OTA) analytics

- 4.2.5 Fleet electrification demands real-time battery analytics

- 4.2.6 Rise of mobility-as-a-service (MaaS) platforms

- 4.3 Market Restraints

- 4.3.1 Escalating cybersecurity compliance cost

- 4.3.2 High upfront TCU* hardware price volatility

- 4.3.3 Multi-jurisdictional data-sovereignty hurdles

- 4.3.4 Inertia in legacy commercial fleets

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Channel

- 5.1.1 Original-Equipment Manufacturer (OEM)

- 5.1.2 Aftermarket

- 5.2 By Solution

- 5.2.1 Embedded

- 5.2.2 Smartphone-based

- 5.2.3 Portable/Plug-in

- 5.3 By Offering Type

- 5.3.1 Hardware

- 5.3.2 Services - Entry-level

- 5.3.3 Services - Mid-tier

- 5.3.4 Services - High-end

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles (LCV)

- 5.4.3 Heavy Commercial Vehicles (HCV)

- 5.5 By Application

- 5.5.1 Fleet Management

- 5.5.2 Insurance Telematics

- 5.5.3 Predictive Maintenance and Diagnostics

- 5.5.4 Navigation and Infotainment

- 5.5.5 Car-sharing and Subscription Services

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia

- 5.6.4 Middle East

- 5.6.4.1 Israel

- 5.6.4.2 Saudi Arabia

- 5.6.4.3 United Arab Emirates

- 5.6.4.4 Turkey

- 5.6.4.5 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Egypt

- 5.6.5.3 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Verizon Communications Inc. (Verizon Connect)

- 6.4.2 Geotab Inc.

- 6.4.3 Trimble Inc.

- 6.4.4 TomTom N.V.

- 6.4.5 MiX Telematics Ltd

- 6.4.6 ATandT Inc.

- 6.4.7 Cisco Systems Inc.

- 6.4.8 LG Electronics Inc.

- 6.4.9 Continental AG

- 6.4.10 Robert Bosch GmbH

- 6.4.11 ZF Friedrichshafen AG

- 6.4.12 Harman International Industries Inc.

- 6.4.13 Valeo SA

- 6.4.14 Inseego Corp. (Ctrack)

- 6.4.15 Microlise Group PLC

- 6.4.16 Aplicom Oy

- 6.4.17 Huawei Technologies Co. Ltd.

- 6.4.18 Sierra Wireless Inc.

- 6.4.19 Octo Telematics S.p.A.

- 6.4.20 CalAmp Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

全球及中國乘用車T型盒市場(2026年)

全球及中國乘用車T型盒市場(2026年) 車隊遠端資訊處理系統市場:按部署類型、通訊技術、組件類型、車輛類型、應用和最終用戶產業分類-2026-2032年全球市場預測

車隊遠端資訊處理系統市場:按部署類型、通訊技術、組件類型、車輛類型、應用和最終用戶產業分類-2026-2032年全球市場預測 2026年全球車載資訊服務市場報告車用通訊系統售後服務資訊處理市場:按組件類型、連接類型、部署模式、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測

2026年全球車載資訊服務市場報告車用通訊系統售後服務資訊處理市場:按組件類型、連接類型、部署模式、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測 2026-2034年全球車用通訊系統市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球車用通訊系統市場規模、佔有率、趨勢和成長分析報告 賽車遙測市場:按組件、應用、國家和地區分類-全球產業分析、市場規模、市場佔有率及2025年至2032年預測

賽車遙測市場:按組件、應用、國家和地區分類-全球產業分析、市場規模、市場佔有率及2025年至2032年預測 全球保險遠距資訊處理市場,2025-2029年

全球保險遠距資訊處理市場,2025-2029年 共享出行遠端資訊處理市場 - 全球產業規模、佔有率、趨勢、機會及預測(按服務類型、車輛類型、產品/服務、技術、地區和競爭格局分類,2021-2031)輕型商用車遠端資訊處理市場-全球產業規模、佔有率、趨勢、機會、預測:按解決方案類型、應用、最終用戶、地區和競爭對手分類,2021-2031年車載資訊系統備用電池市場(按電池化學成分、車輛類型、應用、最終用戶和分銷管道分類)-2026-2032年全球預測

共享出行遠端資訊處理市場 - 全球產業規模、佔有率、趨勢、機會及預測(按服務類型、車輛類型、產品/服務、技術、地區和競爭格局分類,2021-2031)輕型商用車遠端資訊處理市場-全球產業規模、佔有率、趨勢、機會、預測:按解決方案類型、應用、最終用戶、地區和競爭對手分類,2021-2031年車載資訊系統備用電池市場(按電池化學成分、車輛類型、應用、最終用戶和分銷管道分類)-2026-2032年全球預測