|

市場調查報告書

商品編碼

1939634

智慧水錶:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Smart Water Meter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

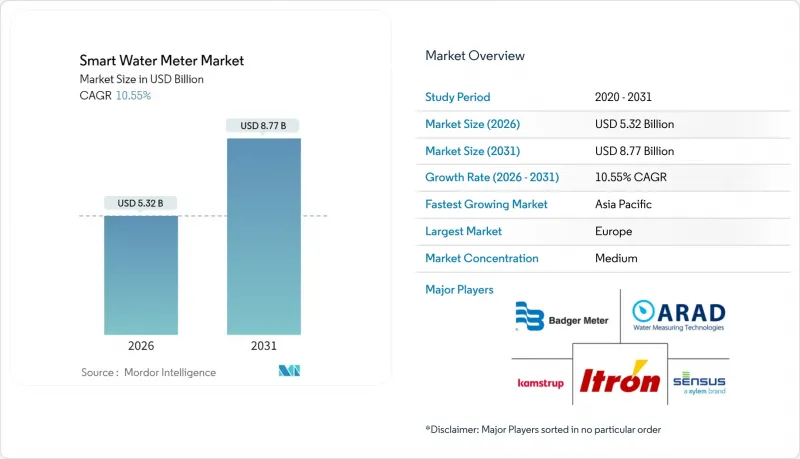

2025年智慧水錶市場價值為48.1億美元,預計到2031年將達到87.7億美元,高於2026年的53.2億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 10.55%。

公共產業正持續從機械式水錶過渡到連網設備,以實現即時監測、自動收費和數據驅動的洩漏檢測。節水監管要求、老舊配水設備更換壓力日益增大以及物聯網 (IoT) 平台的擴展,共同推動了各公共產業(TCO)。諸如按需付費模式等資金籌措方式的拓展,以及獎勵檢驗的洩漏減少的績效導向法規,將進一步增強已開發市場和新興市場的需求。

全球智慧水錶市場趨勢與洞察

支持性的政府法規

強制性部署計劃和節水標準正推動公共產業轉型為符合合規和報告要求的先進計量解決方案。歐盟飲用水指令要求端到端監測,促使德國和法國要求新建建築和大型維修安裝智慧水錶。加州的永久性用水法規要求提供詳細數據以進行執法,並將高級計量基礎設施(AMI)的部署作為合格資金籌措的先決條件。供水事業透過記錄減少漏損和提高客戶參與的績效,獲得成本回收機制,從而降低投資風險並支持在其轄區內推廣。供應商受益於大量訂單帶來的更低單位成本,而政策制定者則可以利用透明的績效指標來追蹤節水進度。無論是在市政、區域或國家層面,相關法規都確保了智慧水錶市場廣泛應用所需的長期確定性。

提高用水效率的必要性

在缺水地區,供水事業部署智慧水錶,以識別高耗水模式,並透過提供每小時數據來支援用戶改變用水行為,從而提升用戶的自主用水能力。使用連續遙測技術的工業設施透過洩漏識別和製程最佳化,實現了20%至30%的用水量減少。農業試點計畫將土壤濕度感測與基於天氣的灌溉計畫結合,實現了高達28%的節水效果,展現了智慧水錶在跨產業的效用。由於水的生產和抽水是重要的營運成本,效率的提升也轉化為能源的節約。透過分析應用程式進行需求預測,供水事業可以平滑用水高峰,並推遲產能擴張。當供水事業將節水與收入脫鉤結合時,效率的提升就能轉化為穩定的財務業績,進而推動智慧水錶市場的發展。

高昂的初始成本和網路安全風險

一套完整的智慧水錶(AMI)部署方案,每個終端的成本可能在200至400美元之間,這對資本預算有限的公共產業來說是一個挑戰。費率調整核准可能需要數年時間,從而延誤計劃啟動。網路安全措施、加密、入侵偵測和24小時監控會使計劃總成本增加15%至25%。小規模的系統,尤其是在開發中國家,如果沒有優惠融資,往往會延後投資。備受矚目的網路安全事件會加劇監管審查,進一步推高合規成本。在資金籌措機製成熟和安全框架標準化之前,這些因素將抑制智慧水錶市場的整體成長。

細分市場分析

到2025年,自動抄表(AMR)系統將佔據智慧水錶市場57.10%的佔有率,這反映了其強大的基礎和經濟高效的單向資料傳輸特性。許多公共產業在現代化改造初期就採用AMR系統,因為它無需大規模的網路建設,並且可以透過移動抄表顯著降低人事費用。雖然與AMR相關的智慧水錶市場規模仍然可觀,但隨著第二代部署優先採用雙向架構,其成長速度正在放緩。

隨著供水事業對即時漏水警報、遠端斷水和分時收費系統的需求日益成長,到2031年,高級計量基礎設施(AMI)的複合年成長率將達到11.55%。蜂窩網路、NB-IoT和LoRaWAN模組成本的下降消除了AMI普及的關鍵障礙。服務供應商將水錶、分析工具和軟體訂閱捆綁銷售,從而將資本成本分攤到營運預算中。數據豐富的AMI平台有助於與節水計畫的整合,加速區域普及,並推動智慧水錶市場的發展。

到2025年,住宅智慧水錶市場規模將佔智慧水錶市場的58.00%,這主要得益於歐洲和北美住宅新房屋強制安裝智慧水錶。消費者可以透過用水入口網站將節水目標與實際節省的費用連結起來,並保持定期更新。

商業建築領域採用智慧水錶的速度最快,複合年成長率高達 11.85%,這主要得益於整合水、能源和暖通空調數據的設施管理軟體的普及。高層建築業主透過營運成本的節約和綠建築認證來證明其投資的合理性。零售連鎖店和酒店集團正在利用分析技術進行跨站點對比分析,以發現隱藏的洩漏並最佳化灌溉系統。企業用戶採用率的提高,以及永續發展報告架構的完善,正在推動智慧水錶市場的整體成長。

這份智慧水錶市場報告按技術(自動抄表/高級計量基礎設施)、應用(住宅等)、水錶類型(機械/渦輪、超音波、電磁)、通訊技術(射頻、LoRaWAN/其他LPWAN等)、組件(硬體、軟體/分析、服務)、部署類型(新安裝、維修/更換)和地區對市場進行分析。

區域分析

預計到2025年,歐洲將以36.10%的收入佔有率引領智慧水錶市場,這得益於歐盟指令強制要求追蹤水損和實現透明計費。各國制定的實施藍圖確保了穩定的競標機會,而長期供應商架構則簡化了採購流程。此外,公共產業正利用旨在增強氣候適應能力的復甦基金,加速採用高級計量基礎設施(AMI),以支持全部區域的穩定用水需求。

亞太地區預計將成為成長最快的地區,到2031年複合年成長率將達到12.05%。中國正在大規模智慧城市示範計畫中,將計量功能融入其區域數位雙胞胎;印度的「飲用水生命線計畫」(Jal Jeevan Mission)則在資金籌措農村地區的智慧互聯,包括智慧設備。印尼和越南等東南亞國家的快速都市化正在推動傳統資產的升級改造,以避免因技術過時而造成的沉沒成本。政府補貼、多邊融資和公私合營等多種因素的共同作用,透過擴大安裝規模,推動了智慧水錶市場的成長。

在北美,老舊基礎設施的更新換代和各州範圍內的節水政策正在推動水務成長。加州公共產業正在部署高級計量基礎設施(AMI),以強制執行人均用水量限制,並透過遠端斷水功能增強抵禦野火的能力。加拿大各州的現代化計畫重點在於非收益水的回收利用,水務成長也呈現漸進式成長。在拉丁美洲,巴西的特許經營競標預示著巨大的發展機會。與此同時,中東和非洲的公共產業正在使用智慧水錶來應對水資源短缺和防止盜水,但部署進度因資金籌措和通訊網路的準備情況而異。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 支持性的政府法規

- 需要提高用水效率。

- 減少無收益水損失

- 智慧城市與物聯網平台整合

- 按節省金額付費的融資模式

- 乾旱引發的節水措施

- 市場限制

- 高昂的初始成本和網路安全風險

- 系統整合複雜性

- 公共產業數據分析人才短缺

- 超音波設備的電池壽命有限

- 產業價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 智慧電錶投資收益(ROI) 分析

- 通訊協定基準比較

- LoRaWAN 安裝步驟和用例

- 公共產業數位化帶來的益處

- 影響市場的宏觀經濟因素

第5章 市場規模與成長預測

- 透過技術

- 自動抄表(AMR)

- 進階計量基礎設施(AMI)

- 透過使用

- 住宅

- 商業

- 產業

- 農業

- 按計量類型

- 機械/渦輪機

- 超音波

- 電磁學

- 透過通訊技術

- 射頻(專有射頻技術)

- LoRaWAN/其他低功耗廣域網

- 蜂窩通訊(NB-IoT/LTE-M)

- 有線(M-Bus/乙太網路)

- 按組件

- 硬體

- 軟體和分析

- 服務

- 透過部署

- 新推出

- 維修/更換

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 新加坡

- 澳洲

- 亞太其他地區

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Arad Ltd.

- Badger Meter Inc.

- Itron Inc.

- Sensus USA Inc.(Xylem Inc.)

- Kamstrup A/S

- Diehl Stiftung and Co. KG

- Zenner International GmbH and Co. KG

- Landis+Gyr Group AG

- Honeywell International Inc.

- Neptune Technology Group Inc.(Roper)

- Aclara Technologies LLC(Hubbell)

- Apator SA

- Axioma Metering

- B Meters Srl

- Datamatic Inc.

- Maddalena SpA

- Suntront Tech Co., Ltd.

- Mueller Systems LLC

- Waviot

- Watertech SpA(Arad)

- Jiangxi Sanchuan Water Meter Co. Ltd.

- Ningbo Water Meter Co. Ltd.

- BETAR Company

- Integra Metering AG

- IESLab Electronic Co. Ltd.

第7章 市場機會與未來展望

The Smart Water Meter market was valued at USD 4.81 billion in 2025 and estimated to grow from USD 5.32 billion in 2026 to reach USD 8.77 billion by 2031, at a CAGR of 10.55% during the forecast period (2026-2031).

Utilities continue to migrate from mechanical meters to connected devices that enable real-time monitoring, automated billing, and data-driven leak detection. Regulatory mandates for conservation, mounting pressure to replace aging distribution assets, and the expansion of Internet of Things platforms combine to accelerate adoption across utility classes. Vendor competition centers on integrating analytics and two-way communications while maintaining a favorable total cost of ownership. Expanding financing options, such as pay-as-you-save models, and performance-based regulation that rewards verified water-loss reduction, further strengthen demand pipelines in developed and emerging economies.

Global Smart Water Meter Market Trends and Insights

Supportive Government Regulations

Mandatory deployment timelines and water-efficiency standards push utilities toward advanced metering solutions that satisfy compliance and reporting needs. The EU Drinking Water Directive requires end-to-end monitoring, prompting Germany and France to stipulate smart meters in all new constructions and major renovations. California's permanent water-use rules demand granular data for enforcement, making AMI rollouts a prerequisite for funding eligibility. Utilities gain cost recovery mechanisms when they document water-loss cuts and customer engagement improvements, which lowers investment risk and supports full-territory deployments. Vendors benefit from volume orders that reduce per-unit costs, while policymakers secure transparent performance metrics to track conservation progress. Across municipal, regional, and national levels, regulation underwrites the long-term certainty needed for widespread Smart Water Meter market adoption.

Need to Improve Water-Use Efficiency

Utilities in water-scarce regions adopt connected meters to identify high-consumption patterns and empower customers with hourly data that supports behavioral changes. Industrial facilities using continuous telemetry report 20-30% consumption cuts after pinpointing leaks and optimizing processes. Agricultural pilots that combine soil-moisture sensing with weather-based scheduling record up to 28% savings, demonstrating cross-sector utility. Efficiency gains also yield energy savings because water production and pumping constitute large operational expenses. Analytics applications forecast demand, allowing utilities to flatten peaks and defer capacity expansion. As utilities tie conservation to revenue decoupling, efficiency gains translate into stable financial performance and propel the Smart Water Meter market forward.

High Upfront Costs and Cybersecurity Risks

Full AMI rollouts cost USD 200-400 per endpoint, challenging utilities with tight capital budgets. Rate-case approvals can stretch over several years, delaying project start dates. Cybersecurity countermeasures, encryption, intrusion detection, and 24-hour monitoring raise the total project expense by an additional 15-25%. Smaller systems, especially in developing economies, often defer investments without concessional finance. High-profile cyber incidents intensify regulatory scrutiny, further elevating compliance costs. These factors collectively weigh on Smart Water Meter market growth until financing mechanisms mature and security frameworks standardize.

Other drivers and restraints analyzed in the detailed report include:

- Reducing Non-Revenue Water Losses

- Smart-City and IoT Platform Integration

- Systems-Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automatic Meter Reading systems accounted for 57.10% of Smart Water Meter market share in 2025, reflecting their entrenched base and cost-efficient one-way data transmission. Many utilities adopt AMR during early modernization phases because drive-by collection sharply reduces manual labor without extensive network build-out. The Smart Water Meter market size attached to AMR remains large, yet its growth moderates as second-generation rollouts favor two-way architectures.

Advanced Metering Infrastructure records an 11.55% CAGR to 2031 as utilities seek real-time leak alerts, remote disconnect, and time-variant pricing schemes. Cellular, NB-IoT, and LoRaWAN modules drop in cost, erasing a key barrier to AMI adoption. Service providers package meters, analytics, and software subscriptions, distributing capital costs over operating budgets. Data-rich AMI platforms integrate easily with conservation programs, accelerating regional penetration and widening the Smart Water Meter market.

Residential deployments formed 58.00% of the Smart Water Meter market size in 2025 after multiple European and North American mandates required smart meters for new housing. Consumers benefit from usage portals that connect conservation goals to tangible savings, sustaining stable replacement cycles.

Commercial buildings show the fastest uptake at a 11.85% CAGR, propelled by facility-management software that pairs water, energy, and HVAC data. High-rise real-estate owners justify investment through lower operating expenses and green-building certifications. Retail chains and hospitality groups apply analytics to benchmark sites, uncover concealed leaks, and optimize irrigation. As sustainability reporting frameworks tighten, enterprise users expand deployments, bolstering overall Smart Water Meter market growth.

The Smart Water Meter Market Report is Segmented by Technology (Automatic Meter Reading & Advanced Metering Infrastructure), Application (Residential, and More), Meter Type (Mechanical/Turbine, Ultrasonic, and Electromagnetic), Communication Technology (Radio-Frequency, LoRaWAN/Other LPWAN, and More), Component (Hardware, Software and Analytics, and Services), Deployment (New Installations and Retrofit/Replacement), and Geography.

Geography Analysis

Europe dominated the Smart Water Meter market with 36.10% revenue share in 2025, anchored by EU directives that compel water-loss tracking and transparent billing. National implementation roadmaps guarantee steady tender pipelines, and long-term vendor frameworks streamline procurement. Utilities also tap recovery funds targeting climate resilience, accelerating district-wide AMI deployments that underpin stable regional demand.

Asia-Pacific registers the fastest expansion, clocking a 12.05% CAGR to 2031. China's extensive smart-city pilots embed metering within neighborhood digital twins, while India's Jal Jeevan Mission finances rural connections that include smart endpoints. Southeast Asian economies such as Indonesia and Vietnam upgrade legacy assets concurrently with rapid urbanization, avoiding sunk costs tied to older technologies. Government grants, multilateral loans, and public-private partnerships combine to scale installations and enlarge the Smart Water Meter market.

North America benefits from aging infrastructure replacement and statewide conservation mandates. California utilities deploy AMI to enforce per-capita usage limits and to support wildfire resilience through remote shut-off capabilities. Canada advances province-level modernization programs focusing on non-revenue water recovery, adding incremental growth. Latin America's concession tenders in Brazil signal sizable upcoming opportunities, while Middle East and Africa utilities leverage smart meters to address scarcity and reduce theft, though deployment progress varies by funding availability and communication-network readiness.

- Arad Ltd.

- Badger Meter Inc.

- Itron Inc.

- Sensus USA Inc. (Xylem Inc.)

- Kamstrup A/S

- Diehl Stiftung and Co. KG

- Zenner International GmbH and Co. KG

- Landis+Gyr Group AG

- Honeywell International Inc.

- Neptune Technology Group Inc. (Roper)

- Aclara Technologies LLC (Hubbell)

- Apator SA

- Axioma Metering

- B Meters Srl

- Datamatic Inc.

- Maddalena S.p.A.

- Suntront Tech Co., Ltd.

- Mueller Systems LLC

- Waviot

- Watertech S.p.A. (Arad)

- Jiangxi Sanchuan Water Meter Co. Ltd.

- Ningbo Water Meter Co. Ltd.

- BETAR Company

- Integra Metering AG

- IESLab Electronic Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Supportive government regulations

- 4.2.2 Need to improve water-use efficiency

- 4.2.3 Reducing non-revenue water (NRW) losses

- 4.2.4 Smart-city and IoT platform integration

- 4.2.5 Pay-as-you-save financing models

- 4.2.6 Drought-driven conservation mandates

- 4.3 Market Restraints

- 4.3.1 High upfront costs and cybersecurity risks

- 4.3.2 Systems-integration complexity

- 4.3.3 Shortage of utility data-analytics talent

- 4.3.4 Battery-life limits in ultrasonic units

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 ROI Analysis for Smart Meters

- 4.9 Protocol Benchmarking and Comparison

- 4.10 LoRaWAN Implementation Steps and Use-cases

- 4.11 Utility Digitalisation Benefits

- 4.12 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Technology

- 5.1.1 Automatic Meter Reading (AMR)

- 5.1.2 Advanced Metering Infrastructure (AMI)

- 5.2 By Application

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.2.4 Agricultural

- 5.3 By Meter Type

- 5.3.1 Mechanical / Turbine

- 5.3.2 Ultrasonic

- 5.3.3 Electromagnetic

- 5.4 By Communication Technology

- 5.4.1 Radio-frequency (Proprietary RF)

- 5.4.2 LoRaWAN / Other LPWAN

- 5.4.3 Cellular (NB-IoT/LTE-M)

- 5.4.4 Wired (M-Bus/Ethernet)

- 5.5 By Component

- 5.5.1 Hardware

- 5.5.2 Software and Analytics

- 5.5.3 Services

- 5.6 By Deployment

- 5.6.1 New Installations

- 5.6.2 Retrofit / Replacement

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Chile

- 5.7.2.4 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Malaysia

- 5.7.4.6 Singapore

- 5.7.4.7 Australia

- 5.7.4.8 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 United Arab Emirates

- 5.7.5.1.2 Saudi Arabia

- 5.7.5.1.3 Turkey

- 5.7.5.1.4 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Nigeria

- 5.7.5.2.3 Rest of Africa

- 5.7.5.1 Middle East

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Arad Ltd.

- 6.4.2 Badger Meter Inc.

- 6.4.3 Itron Inc.

- 6.4.4 Sensus USA Inc. (Xylem Inc.)

- 6.4.5 Kamstrup A/S

- 6.4.6 Diehl Stiftung and Co. KG

- 6.4.7 Zenner International GmbH and Co. KG

- 6.4.8 Landis+Gyr Group AG

- 6.4.9 Honeywell International Inc.

- 6.4.10 Neptune Technology Group Inc. (Roper)

- 6.4.11 Aclara Technologies LLC (Hubbell)

- 6.4.12 Apator SA

- 6.4.13 Axioma Metering

- 6.4.14 B Meters Srl

- 6.4.15 Datamatic Inc.

- 6.4.16 Maddalena S.p.A.

- 6.4.17 Suntront Tech Co., Ltd.

- 6.4.18 Mueller Systems LLC

- 6.4.19 Waviot

- 6.4.20 Watertech S.p.A. (Arad)

- 6.4.21 Jiangxi Sanchuan Water Meter Co. Ltd.

- 6.4.22 Ningbo Water Meter Co. Ltd.

- 6.4.23 BETAR Company

- 6.4.24 Integra Metering AG

- 6.4.25 IESLab Electronic Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

全球漏水檢測系統市場預測至2034年-按類型、檢測方法、應用和地區分類的分析

全球漏水檢測系統市場預測至2034年-按類型、檢測方法、應用和地區分類的分析 2026年全球變化檢測分析市場報告

2026年全球變化檢測分析市場報告 全球漏水檢測系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球漏水檢測系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 日本智慧水錶市場報告:按產品類型、水錶類型、配置類型、組件、應用和地區分類(2026-2034年)全球智慧水務市場:預測至2032年-按組件、部署方式、解決方案、最終用戶和地區進行分析

日本智慧水錶市場報告:按產品類型、水錶類型、配置類型、組件、應用和地區分類(2026-2034年)全球智慧水務市場:預測至2032年-按組件、部署方式、解決方案、最終用戶和地區進行分析 全球漏水檢測系統市場

全球漏水檢測系統市場 漏水檢測系統市場-全球產業規模、佔有率、趨勢、機會和預測(按組件、技術、最終用戶、地區和競爭細分,2020-2030 年)

漏水檢測系統市場-全球產業規模、佔有率、趨勢、機會和預測(按組件、技術、最終用戶、地區和競爭細分,2020-2030 年) 全球智慧水錶市場:市場規模、市場佔有率、趨勢分析(按技術、儀表類型、應用和地區)、展望和未來預測(2025-2032 年)

全球智慧水錶市場:市場規模、市場佔有率、趨勢分析(按技術、儀表類型、應用和地區)、展望和未來預測(2025-2032 年) 智慧水錶市場規模、佔有率、趨勢分析報告:按水錶類型、技術、應用、地區、細分市場預測,2025-2030 年全球智慧水錶市場:市場規模(按類型、組件、應用和地區分類)、未來預測

智慧水錶市場規模、佔有率、趨勢分析報告:按水錶類型、技術、應用、地區、細分市場預測,2025-2030 年全球智慧水錶市場:市場規模(按類型、組件、應用和地區分類)、未來預測