|

市場調查報告書

商品編碼

1939632

會計軟體:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Accounting Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

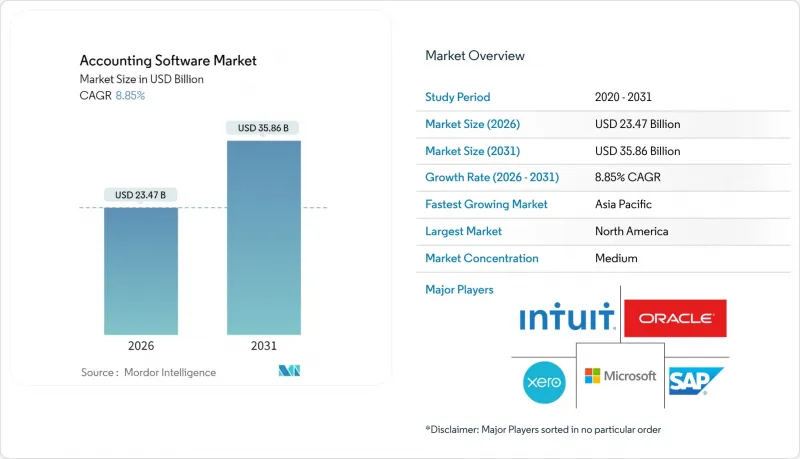

2025年會計軟體市值為215.6億美元,預計2031年將達到358.6億美元,高於2026年的234.7億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 8.85%。

雲端優先策略、即時監管報告要求以及嵌入式人工智慧功能正在不斷重塑競爭優勢,預計到2024年,雲端採用將佔營收的67.43%。供應商正在擴展行動端、以API為中心的套件,這些套件整合了銀行、資金管理和費用管理功能,使企業能夠縮短每月結算週期並獲得營運資本洞察。同時,財務部門人才短缺正在加速軟體的採用,因為自動化正在取代重複性的記帳工作。最後,新的ESG審核追蹤要求迫使企業對舊有系統進行現代化改造,以便轉向能夠產生不可更改的環境和社會揭露資訊的解決方案。

全球會計軟體市場趨勢與洞察

採用雲端優先的金融堆疊

企業正逐步放棄本地部署,轉而採用雲端架構,實現會計、財務和營運數據的即時同步,從而降低基礎設施成本並提高現金流透明度。這種轉變也實現了與金融科技(支付、費用卡、短期流動性管理)的無縫整合,而這些在傳統系統中是無法實現的。

簿記工作流程的超自動化

機器學習驅動的資料提取和機器人流程自動化技術如今能夠以98%的準確率完成交易分類、銀行對帳和發票處理,使會計事務所能夠在不相應增加員工人數的情況下承接更多客戶。這種生產力的提升降低了中小企業的整體擁有成本,並緩解了整個行業的人才短缺問題。

資料主權和隱私監管

GDPR等法規強制要求本地資料存儲,迫使供應商維護跨區域雲,並推高部署預算。企業往往不願意遷移敏感帳本,除非合約條款能夠保證加密、存取控制和本地儲存選項,這導致計劃進度延誤。

細分市場分析

到2025年,雲端解決方案的營收將成長68.08%,年複合成長率(CAGR)為10.15%,這意味著本地部署的市場佔有率將持續下降。按需收費模式無需資本支出,並具備自動更新功能,從而增強了安全性。與銀行和薪資核算服務提供者的無縫API整合將進一步推動雲端解決方案的普及。依賴傳統ERP系統的大型企業仍然傾向於採用混合策略來處理對延遲敏感的工作流程,但他們也嘗試透過雲端子公司來縮短財務結算週期。擴展的資料居住選項和區域資料中心佈局將緩解傳統的合規性問題,預計未來十年內,雲端在會計軟體市場的佔有率將接近飽和。

本地部署平台在高度監管的行業中仍佔有一席之地,這些行業往往需要離線處理,或者系統因客製化而受到嚴格限制。然而,維護成本和大型主機工程師的短缺迫使財務長們不得不撥出預算用於現代化改造。供應商抓住這一機遇,提供遷移工具包,將傳統帳簿資料映射到多租戶架構,從而將過渡期縮短至短短幾週。因此,即使整個會計軟體產業整體擴張,與本地部署相關的會計軟體市場規模預計仍將萎縮。

大型企業將採用多幣種、多實體全球合併會計套件,預計2025年,其營收佔比將達到54.10%。同時,中小企業將以10.85%的複合年成長率成為成長最快的企業,因為直覺的雲端模組和人工智慧驅動的數據收集減少了對專職IT人員的需求。訂閱模式會根據交易量調整費用,即使在早期成長階段也能維持價格合理。

隨著強制性電子帳單政策推動數位化,亞太和拉丁美洲的創業生態系統將進一步刺激中小企業的需求。供應商透過提供包含聊天機器人功能的入門方案來降低採用門檻,從而將手動使用電子表格的用戶轉化為用戶用戶。因此,中小企業的會計軟體市場佔有率將穩定成長,並逐漸縮小與傳統大型企業在會計軟體應用上的差距。

會計軟體市場按部署類型(本地部署、雲端部署)、組織規模(大型企業、中小企業)、最終用戶行業(銀行、金融服務和保險、製造業、零售和電子商務、專業服務、IT和電信、醫療保健)、應用(薪資管理、帳單和出貨單、其他)以及地區進行細分。市場預測以美元(USD)計價。

區域分析

到2025年,北美將佔全球收入的38.35%,這主要得益於其較高的雲端採用率、成熟的支付基礎設施以及充足的技術預算。美國企業在員工人均財務應用方面的支出高於全球平均水平,從而促進了供應商的快速創新和夥伴關係關係的形成。加拿大也呈現類似的趨勢,這得益於其統一的稅收框架,該框架簡化了跨境應用。

在歐洲,GDPR一般資料保護規則和永續發展報告義務正在推動平台更新,而多語言介面和歐洲電子帳單標準(例如Peppol)則推動了產品在地化。然而,與亞太地區相比,歐洲較慢的決策週期限制了其成長。

亞太地區以10.45%的複合年成長率成為成長最快的地區,這主要得益於印度和印尼強制推行電子帳單,以及日本對電子帳簿儲存的非正式規定。中小企業正在跨越桌面軟體階段,直接採用行動優先的雲端套件,這些套件整合了本地電子錢包和QR碼支付功能。全球供應商對本地資料中心的投資正在緩解資料主權的擔憂,並創造公共部門採購機會。

在拉丁美洲,巴西和墨西哥的發展勢頭強勁。這兩個國家多年來一直實行即時發票支付,企業正在將自動化應用擴展到稅務申報之外,並轉向整合ERP和財務系統的雲端平台。中東和非洲地區在經濟多元化和不斷擴展的金融科技生態系統的推動下正經歷穩步成長,但網路連接和人才短缺限制了技術的普及速度。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 市場促進因素

- 雲端優先金融系統實施

- 簿記工作流程的超自動化

- 人工智慧驅動的異常檢測和合規性

- 對行動優先結帳體驗的需求

- 利用開放銀行平台實現即時應收帳款及應付帳款融資

- 基於ESG的審核追蹤驅動軟體更新

- 市場限制

- 資料主權和隱私監管

- 舊有系統切換成本

- 具備人工智慧能力的會計人員短缺

- 跨境電子帳單指令分散

- 價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 產業生態系分析

- 主要用例和案例研究

- 宏觀經濟趨勢評估

- 投資分析

第5章 市場規模與成長預測

- 依部署類型

- 本地部署

- 基於雲端的(SaaS)

- 按組織規模

- 主要企業

- 中小企業

- 按最終用戶行業分類

- BFSI

- 製造業

- 零售與電子商務

- 專業服務

- 資訊科技和電信

- 衛生保健

- 透過使用

- 薪資管理

- 帳單和發票

- 費用管理

- 稅務管理

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 新加坡

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Intuit Inc.

- The Sage Group plc

- SAP SE

- Oracle Corporation(subsidiary:NetSuite Inc.)

- Microsoft Corporation

- Xero Limited

- Infor, Inc.(aka Infor Global Solutions, Inc.)

- Epicor Software Corporation

- Unit4 NV(parent Unit4 Holding BV)

- Zoho Corporation Private Limited

- MYOB Group Pty Ltd

- 2ndSite Inc.(doing business as FreshBooks)

- Wave Financial Inc.

- KashFlow Software Limited

- FreeAgent Holdings plc(operating entity:FreeAgent Central Ltd)

- Patriot Software Company, LLC

- Odoo SA

- Saasu Pty Ltd

- Red Wing Software, Inc.

- Reckon Limited

第7章 市場機會與未來展望

The accounting software market was valued at USD 21.56 billion in 2025 and estimated to grow from USD 23.47 billion in 2026 to reach USD 35.86 billion by 2031, at a CAGR of 8.85% during the forecast period (2026-2031).

Cloud-first strategies, real-time regulatory reporting mandates and embedded artificial-intelligence features continue to redefine competitive advantage, with cloud deployments already anchoring 67.43% of revenue in 2024. Vendors are expanding mobile, API-centric suites that integrate banking, treasury and spend-management functions, helping enterprises compress monthly close cycles and unlock working-capital insights. At the same time, talent shortages inside finance departments accelerate software adoption because automation substitutes repetitive bookkeeping labor. Finally, emerging ESG audit-trail requirements force organizations to refresh legacy systems in favor of solutions that generate immutable environmental and social disclosures.

Global Accounting Software Market Trends and Insights

Cloud-First Finance-Stack Adoption

Organizations are abandoning on-premise installations in favor of cloud architectures that synchronize accounting, treasury and operational data in real time, cutting infrastructure costs and improving cash-flow visibility. The shift also unlocks seamless fintech integrations-payments, expense cards and short-term liquidity-once unattainable on legacy systems.

Hyper-Automation of Bookkeeping Workflows

Machine-learning extraction and robotic process automation now classify transactions, reconcile banks and process invoices with 98% accuracy, allowing accounting firms to absorb more clients without proportional head-count increases. The resulting productivity gains lower total ownership costs for small businesses and offset the industry-wide talent deficit.

Data-Sovereignty and Privacy Regulations

Rules such as GDPR compel local data residency, forcing vendors to maintain multi-region clouds and inflating implementation budgets. Enterprises hesitate to migrate sensitive ledgers until contractual clauses guarantee encryption, access controls and in-country storage options, delaying project timelines .

Other drivers and restraints analyzed in the detailed report include:

- AI-Led Anomaly Detection and Compliance

- Mobile-First Accounting Experience Demand

- Scarcity of AI-Ready Accounting Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud solutions generated 68.08% revenue in 2025, and their 10.15% CAGR signals that the on-premise share will continue to erode. The model's pay-as-you-grow pricing eliminates capital expenditure and embeds automatic updates that strengthen security posture. Seamless API connectivity with banks and payroll providers further cements adoption. Large enterprises wedded to legacy ERPs still favor hybrid strategies for latency-sensitive workflows, yet even they pilot cloud subsidiaries to reduce close cycles. Growing data-residency options and regional datacenters mitigate prior compliance objections, suggesting that the cloud slice of the accounting software market will near saturation by decade-end.

On-premise platforms retain niche relevance in highly regulated sectors where offline processing is mandatory or where bespoke customizations lock systems in place. However, maintenance overhead and scarce mainframe skills push CFOs to earmark modernization budgets. Vendors exploit this transition by offering migration toolkits that map historical ledgers into multi-tenant architectures, shortening cut-over periods to weeks. As a result, the accounting software market size tied to on-premise deployments is projected to contract despite overall industry expansion.

Large organizations captured 54.10% of 2025 revenue by deploying global-consolidation suites capable of multi-currency and multi-entity reporting. Yet SMEs drive the fastest 10.85% CAGR because intuitive cloud modules and AI-driven data capture reduce the need for dedicated IT staff. Subscription tiers align costs with transaction volume, ensuring affordability even during early growth stages.

Entrepreneurial ecosystems in Asia-Pacific and Latin America further catalyze SME demand as mandatory e-invoicing forces digital upgrades. Vendors releasing starter packages with embedded chatbot support lower adoption barriers and convert manual spreadsheet users into subscribers. Consequently, the accounting software market share commanded by SMEs will steadily rise, narrowing the historic gap with enterprise deployments.

Accounting Software Market is Segmented by Deployment Type (On-Premise, and Cloud-Based), Organization Size (Large Enterprises, and Small and Medium Enterprises (SMEs)), End-User Industry (BFSI, Manufacturing, Retail and E-Commerce, Professional Services, IT and Telecom, and Healthcare), Application (Payroll Management, Billing and Invoicing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 38.35% revenue in 2025 on the back of high cloud readiness, mature payments rails and well-funded technology budgets. United States enterprises allocate larger per-employee spend on finance applications compared with global averages, spurring rapid vendor innovation and partnering ecosystems. Canada mirrors this trend, supported by harmonized taxation frameworks that simplify cross-border deployment.

Europe follows, where GDPR compliance and sustainability-reporting mandates stimulate platform refreshes. Multi-lingual interfaces and European e-invoicing standards such as Peppol drive product localization. However, slower decision cycles temper growth relative to Asia-Pacific.

Asia-Pacific charts the fastest 10.45% CAGR, propelled by India's and Indonesia's compulsory e-invoicing rollouts and by Japan's soft-mandate for electronic preservation of ledgers. SMEs leapfrog desktop software, adopting mobile-first cloud suites that integrate domestic e-wallets and QR code payments. Local datacenter investments by global vendors mitigate data-sovereignty hesitance and unlock public-sector procurements.

Latin America sees momentum in Brazil and Mexico, where real-time invoice clearance has existed for years, leading businesses to extend automation beyond tax reporting to full ERP-finance clouds. Middle East and Africa post steady gains aligned to economic diversification drives and expanding fintech ecosystems, though connectivity and talent shortages moderate adoption pace.

- Intuit Inc.

- The Sage Group plc

- SAP SE

- Oracle Corporation (subsidiary: NetSuite Inc.)

- Microsoft Corporation

- Xero Limited

- Infor, Inc. (a.k.a. Infor Global Solutions, Inc.)

- Epicor Software Corporation

- Unit4 N.V. (parent Unit4 Holding B.V.)

- Zoho Corporation Private Limited

- MYOB Group Pty Ltd

- 2ndSite Inc. (doing business as FreshBooks)

- Wave Financial Inc.

- KashFlow Software Limited

- FreeAgent Holdings plc (operating entity: FreeAgent Central Ltd)

- Patriot Software Company, LLC

- Odoo SA

- Saasu Pty Ltd

- Red Wing Software, Inc.

- Reckon Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-first finance-stack adoption

- 4.2.2 Hyper-automation of book-keeping workflows

- 4.2.3 AI-led anomaly detection and compliance

- 4.2.4 Mobile-first accounting experience demand

- 4.2.5 Real-time A/R-A/P financing via open-banking rails

- 4.2.6 ESG-grade audit trails driving software refresh

- 4.3 Market Restraints

- 4.3.1 Data-sovereignty and privacy regulations

- 4.3.2 Legacy-system switching costs

- 4.3.3 Scarcity of AI-ready accounting talent

- 4.3.4 Fragmented e-invoicing mandates across borders

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Industry Ecosystem Analysis

- 4.9 Key Use Cases and Case Studies

- 4.10 Assessment of Macroeconomic Trends

- 4.11 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 On-premise

- 5.1.2 Cloud-based (SaaS)

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises (SMEs)

- 5.3 By End-user Industry

- 5.3.1 BFSI

- 5.3.2 Manufacturing

- 5.3.3 Retail and E-commerce

- 5.3.4 Professional Services

- 5.3.5 IT and Telecom

- 5.3.6 Healthcare

- 5.4 By Application

- 5.4.1 Payroll Management

- 5.4.2 Billing and Invoicing

- 5.4.3 Expense Tracking

- 5.4.4 Tax Management

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Colombia

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Netherlands

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 Singapore

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Intuit Inc.

- 6.4.2 The Sage Group plc

- 6.4.3 SAP SE

- 6.4.4 Oracle Corporation (subsidiary: NetSuite Inc.)

- 6.4.5 Microsoft Corporation

- 6.4.6 Xero Limited

- 6.4.7 Infor, Inc. (a.k.a. Infor Global Solutions, Inc.)

- 6.4.8 Epicor Software Corporation

- 6.4.9 Unit4 N.V. (parent Unit4 Holding B.V.)

- 6.4.10 Zoho Corporation Private Limited

- 6.4.11 MYOB Group Pty Ltd

- 6.4.12 2ndSite Inc. (doing business as FreshBooks)

- 6.4.13 Wave Financial Inc.

- 6.4.14 KashFlow Software Limited

- 6.4.15 FreeAgent Holdings plc (operating entity: FreeAgent Central Ltd)

- 6.4.16 Patriot Software Company, LLC

- 6.4.17 Odoo SA

- 6.4.18 Saasu Pty Ltd

- 6.4.19 Red Wing Software, Inc.

- 6.4.20 Reckon Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

會計軟體市場:2026-2032年全球市場預測(依軟體、定價模式、應用程式、部署類型、企業規模、最終用戶和產業分類)

會計軟體市場:2026-2032年全球市場預測(依軟體、定價模式、應用程式、部署類型、企業規模、最終用戶和產業分類) 2026-2030年全球商業會計軟體市場

2026-2030年全球商業會計軟體市場 薪資稅合規自動化:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)薪資和人力資源合規軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

薪資稅合規自動化:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)薪資和人力資源合規軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 2026年全球稅務和會計軟體市場報告

2026年全球稅務和會計軟體市場報告 人力資源和薪資管理軟體市場:按部署類型、行業和地區分類

人力資源和薪資管理軟體市場:按部署類型、行業和地區分類 全球基金會計軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球會計軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034)2026年全球線上記帳與會計軟體市場報告2026年全球商業會計軟體市場報告

全球基金會計軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球會計軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034)2026年全球線上記帳與會計軟體市場報告2026年全球商業會計軟體市場報告