|

市場調查報告書

商品編碼

1939629

超吸收性聚合物(SAP):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Super Absorbent Polymers (SAP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

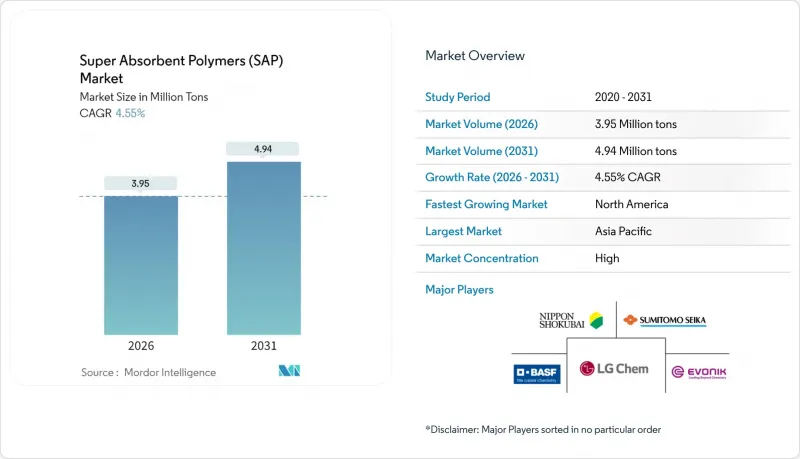

預計到 2026 年,超吸收性聚合物 (SAP) 市場規模將達到 395 萬噸,較 2025 年的 378 萬噸持續成長。

預計到 2031 年將達到 494 萬噸,2026 年至 2031 年的複合年成長率為 4.55%。

這一穩定成長主要得益於嬰兒尿布需求的不斷成長、高吸水性成人失禁墊的快速普及以及工業和農業領域應用範圍的擴大。歐洲更嚴格的生物基化學品法規,加上中國和印度人均尿布消費量的成長,正推動產品系列為高階高性能等級。製造商不斷升級工廠,提高能源效率並實現垂直整合,以降低丙烯酸價格波動。同時,面向消費者的訂閱模式和電商主導的低溫運輸包裝開闢了高利潤的細分市場,抵消了標準衛生用品銷售帶來的利潤壓力。對纖維素和澱粉基替代品的投資增加表明,永續性正在推動超吸收性聚合物(SAP)市場的品牌價值和製程創新。

全球超吸收性聚合物(SAP)市場趨勢與洞察

中國和印度人均尿布支出增加

在中國,受鼓勵多胞胎生育政策和可支配收入成長的推動,預計自2022年起,都市區家庭尿布平均支出將增加15%。在印度,二、三線城市分銷網路的擴張提高了尿布的滲透率,使高階尿布產品更受首次購買者的歡迎。採用高吸收性超強聚合物(SAP)並減少凝膠結塊的優質產品正在加速超強吸收性聚合物市場的銷售和價值成長。當地加工商正透過簽訂長期承購協議來加強供應保障,以確保產品品質並降低運輸風險。

高吸水性成人尿墊迅速流行

日本、韓國、德國和義大利等國的人口老化推動了成人失禁用品的需求,而社會接納宣傳活動也有助於減少人們對失禁的歧視。新產品將吸水性聚合物(SAP)含量提高了高達40%,使其更輕薄,更接近普通內褲,從而鼓勵白天使用。訂閱式電商通路正在蓬勃發展,提供包含隱私配送、防漏保護和便於行動的SKU等組合產品。製造商正積極回應,研發差異化的核殼顆粒結構,以增強負重下的吸收能力,進而打造一個利潤豐厚的細分市場。

原物料價格波動

丙烯酸佔生產成本的70%之多,季波動幅度高達25%,為採購預算帶來不確定性。長虹高分子投資16億美元建設的丙烷制丙烯酸工廠計劃於2026年竣工,預計將降低可變成本曲線,並打破現有西方供應商之間的價格模式。隨著企業董事會將原料安全放在首位,對生物基路線和垂直整合的興趣日益濃厚。

細分市場分析

到2025年,丙烯酸類產品將佔據超吸收性聚合物市場71.30%的佔有率,這主要歸功於其在嬰兒尿布領域久經考驗的可靠性。為了提高安全性,高階品牌擴大指定使用低遊離單體含量的高純度丙烯酸類超吸收性聚合物(SAP)。同時,聚丙烯醯胺類產品預計將繼續以6.18%的複合年成長率成長,這主要得益於其在乾旱農業應用和工業密封領域優異的保水性能。就超吸收性聚合物(SAP)市場規模而言,預計2026年至2031年間,聚丙烯醯胺的產量將增加12萬噸,從而取代丙烯酸類產品佔據市場佔有率。

產品開發人員正在探索結合丙烯酸和多醣骨架的混合網路,以平衡成本和分解性。日本觸媒株式會社的生質能基超吸水性聚合物(SAP)產品線(獲得清真認證,產自印尼)就是這種跨化學創新的典範。目前,投資重點正轉向生質能採購物流、雜質管理以及可擴展的連續反應器設計,以確保聚合物結構的穩定性。

到2025年,凝膠聚合將維持59.20%的收入佔有率,其反應釜生產線經過最佳化,可實現高通量和均勻的交聯密度。能源回收循環和連續單體循環正在推動成本競爭力的提升。溶液聚合將以4.72%的複合年成長率成長,因為它能夠生產小批量特種級產品,精確控制分子量分佈,並降低能耗,符合永續性目標。

懸浮聚合和反相懸浮聚合製程在需要特殊顆粒形態的細分領域仍然佔據一席之地,例如用於醫療流體管理的核殼微球。製程工程師正致力於精確控制交聯劑的進料量並在線連續光譜技術來調整負載下的吸收性能,這進一步加劇了超吸收性聚合物(SAP)市場的供應細分化。

超吸收性聚合物 (SAP) 市場按產品類型(聚丙烯醯胺、丙烯酸基、其他)、聚合工藝(溶液聚合、其他)、應用(嬰兒尿布、成人失禁用品等)、終端用戶行業(個人護理和衛生用品製造商、農業投入品供應商等)和地區(亞太地區、北美、歐洲等)進行細分。

區域分析

到2025年,亞太地區將佔據超吸收性聚合物(SAP)市場41.40%的佔有率,這主要得益於中國丙烯酸-SAP一體化產業叢集的推動,該集群最大限度地減少了原料物流環節。政府激勵措施,尤其是在江蘇和山東兩省,正在支持產能瓶頸的消除和出口導向擴張。由於一次性尿布的日益普及,印度將為市場成長做出貢獻,而日本則在特種和生質能基SAP領域保持著技術領先地位。

預計北美將達到最高成長率,到2031年複合年成長率將達到5.18% 。成長要素包括高階一次性尿布產品種類的增加、高吸水性超強(SAP)成人失禁護理產品在老齡化嬰兒潮一代中的流行,以及水力壓裂防水層和低溫運輸墊等特殊工業應用。一個由州立大學領導的研究聯盟正在主導一個纖維素和蛋白質基網路,使企業永續性舉措與監管趨勢保持一致。該地區園藝業也開始率先實用化大麻基吸水性超強聚合物,這有助於在超強吸水性聚合物(SAP)市場建立循環經濟。

歐洲嚴格的政策環境正在加速生物基產品和包裝可回收性的普及。德國在產量方面主導地位,而北歐國家的消費者對可堆肥尿布芯材的偏好日益成長。不斷上漲的合規成本促使聚合物供應商和廢棄物管理公司之間建立合作關係,閉合迴路回收方案也正在試行。歐盟標準對出口配方的影響日益增強,並迫使全球生產商統一產品安全性和標籤標準。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 中國和印度人均尿布支出增加

- SAP成人尿墊在亞洲和歐洲迅速普及

- 歐盟向生物基SAP過渡(由一次性塑膠指令推動)

- 電子商務主導了對吸水包裝墊(低溫運輸)需求的快速成長。

- 在農業領域不斷拓展應用

- 市場限制

- 原物料價格波動

- 嬰兒尿布中殘留單體的安全隱患

- 高成本生產

- 生產成本概覽

- 價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭加劇

第5章 市場規模與成長預測

- 依產品類型

- 聚丙烯醯胺

- 丙烯酸基

- 其他

- 透過聚合過程

- 溶液聚合

- 懸浮聚合/反相懸浮聚合

- 凝膠聚合

- 透過使用

- 嬰兒尿布

- 成人失禁護理產品

- 女性用衛生用品

- 農業支持

- 其他用途

- 按最終用戶行業分類

- 個人護理和衛生用品製造商

- 農業投入品供應商

- 醫療保健提供者

- 其他終端用戶產業(電信和電力電纜製造商、食品和藥品低溫運輸物流)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 埃及

- 奈及利亞

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ADM

- BASF

- Braskem

- Chase Corp.

- Chemtex Speciality Limited

- Evonik Industries AG

- Formosa Plastics Group

- LG Chem

- NIPPON SHOKUBAI CO., LTD.

- SANYO CHEMICAL INDUSTRIES, LTD.

- SAP SE

- Satellite Chemical

- SNF

- SONGWON

- SUMITOMO SEIKA CHEMICALS CO.,LTD.

- TOYO BOEKI Co.,Ltd.

- Wanhua

- Yixing Danson Technology

第7章 市場機會與未來展望

The Super Absorbent Polymers Market size in 2026 is estimated at 3.95 Million tons, growing from 2025 value of 3.78 Million tons with 2031 projections showing 4.94 Million tons, growing at 4.55% CAGR over 2026-2031.

Enlarging demand in baby diapers, rapid uptake of high-SAP adult incontinence pads, and a widening set of industrial and agricultural applications are the core forces behind this steady expansion. Tightening European regulations that reward bio-based chemistries, together with higher per-capita diaper spend in China and India, are reshaping product portfolios toward premium, high-performance grades. Manufacturers continue to upgrade plants for energy efficiency and vertical integration to buffer acrylic acid price swings. At the same time, direct-to-consumer subscription models and e-commerce-driven cold-chain packaging unlock high-margin niches that compensate for margin pressure in standard hygiene volumes. Rising investment in cellulosic and starch-derived alternatives signals that sustainability now drives both brand value and process innovation in the super absorbent polymers market.

Global Super Absorbent Polymers (SAP) Market Trends and Insights

Rising Per-Capita Diaper Spend in China and India

Urban households in China lifted their average diaper outlay by 15% since 2022, aided by policy changes that support larger families and rising disposable income. In India, distribution build-out in tier-2 and tier-3 cities raised penetration, bringing advanced diaper formats within reach of first-time buyers. Premium SKUs contain higher-capacity SAP grades and reduced gel blocking, accelerating unit consumption and value growth across the super absorbent polymers market. Local converters increasingly lock supply via long-term offtake deals to secure quality and mitigate freight risks.

Rapid Adoption of High-SAP Adult Incontinence Pads

Demographic aging in Japan, South Korea, Germany, and Italy has elevated adult incontinence prevalence, while social acceptance campaigns reduce stigma. New pads integrate up to 40% more SAP, enabling thinner profiles that resemble regular underwear and encourage daytime use. Subscription e-commerce channels are growing, bundling discrete delivery, leakage guarantees, and mobility-specific SKUs. Producers respond with differentiated core-shell particle morphologies that boost absorption under load, creating a high-margin sub-segment within the super absorbent polymers market.

Volatile Raw Material Prices

Acrylic acid constitutes up to 70% of production cost, and quarterly swings as wide as 25% destabilize procurement budgets. Changhong Polymer's USD 1.6 billion propane-to-acrylic-acid plant, due in 2026, could lower variable cost curves and unsettle pricing parity among established Western suppliers. Interest in bio-routes and vertical integration rises as boards prioritize feedstock security.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Bio-Based SAP in EU Driven by Packaging Rules

- Expanding Agricultural Applications

- Safety Concerns Over Residual Monomers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The acrylic fraction represented 71.30% of the super absorbent polymers market share in 2025, anchored by its proven reliability in baby diapers. To bolster safety perception, premium brands specify higher-purity acrylic SAPs with lower free monomer levels. In parallel, polyacrylamide grades are expanding at a 6.18% CAGR, propelled by their superior water retention in arid agriculture and industrial sealing. Within the super absorbent polymers market size context, polyacrylamide volumes are forecast to add 120 kilotons between 2026 and 2031, capturing incremental share from acrylic grades.

Product developers pursue hybrid networks that mix acrylic and polysaccharide backbones to marry cost and degradability. Nippon Shokubai's biomass-derived SAP line, certified Halal and produced in Indonesia, exemplifies such cross-chemistry innovation. Investment emphasis now tilts toward biomass sourcing logistics, impurity control, and scalable continuous reactor designs that ensure consistent polymer architecture.

Gel polymerization kept a 59.20% revenue share in 2025, with its reactor trains optimized for high throughput and uniform cross-link density. Energy recovery loops and continuous monomer recycling drive incremental cost competitiveness. Solution polymerization grows at 4.72% CAGR because it enables small-lot, specialty grades with tight molecular weight distribution and reduced energy load, aligning with sustainability targets.

Suspension and inverse-suspension routes persist in niche roles that require unique particle morphologies, such as core-shell microspheres for medical fluid management. Process engineers focus on precise cross-linker feed control and in-line spectroscopy to tune absorption under load, further segmenting supply within the super absorbent polymers market.

The Super Absorbent Polymer (SAP) Market Segments the Industry by Product Type (Polyacrylamide, Acrylic Acid Based, and Others), Polymerization Process (Solution Polymerization, and More), Application (Baby Diapers, Adult Incontinence Products, and More), End-User Industry (Personal Care and Hygiene Manufacturers, Agriculture Input Suppliers, and More), and Geography (Asia-Pacific, North America, Europe, and More).

Geography Analysis

Asia-Pacific held 41.40% of the super absorbent polymers market in 2025, powered by China's integrated acrylic acid-SAP clusters that minimize feedstock logistics. Government incentives, notably in Jiangsu and Shandong, support capacity debottlenecking and export-oriented expansions. India contributes volume growth through broader diaper penetration, while Japan retains a technology leadership niche in specialty and biomass-derived grades.

North America is projected to post the fastest 5.18% CAGR through 2031. Growth arises from premium diaper SKUs, high-SAP adult incontinence adoption among aging baby boomers, and specialized industrial uses such as fracking water blockers and cold-chain pads. Research consortia with land-grant universities pioneer cellulosic and protein-based networks, aligning corporate sustainability pledges with regulatory trends. The region also records early field use of hemp-based SAP in horticulture, reinforcing circular economy narratives within the superabsorbent polymers market.

Europe's stringent policy climate accelerates bio-based uptake and packaging recyclability. Germany leads production volume, whereas Nordic countries drive consumer preference for compostable diaper cores. Compliance costs spur alliances between polymer suppliers and waste-management firms to pilot closed-loop recovery schemes. EU standards increasingly influence export formulations, compelling global producers to harmonize product safety and labeling.

- ADM

- BASF

- Braskem

- Chase Corp.

- Chemtex Speciality Limited

- Evonik Industries AG

- Formosa Plastics Group

- LG Chem

- NIPPON SHOKUBAI CO., LTD.

- SANYO CHEMICAL INDUSTRIES, LTD.

- SAP SE

- Satellite Chemical

- SNF

- SONGWON

- SUMITOMO SEIKA CHEMICALS CO.,LTD.

- TOYO BOEKI Co.,Ltd.

- Wanhua

- Yixing Danson Technology

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Per-Capita Diaper Spend in China and India

- 4.2.2 Rapid Adoption of High-SAP Adult Incontinence Pads Asia and Europe

- 4.2.3 Shift to Bio-based SAP in EU Driven by Single-Use Plastics Directive

- 4.2.4 E-Commerce-Led Demand Spike for Absorbent Packaging Pads (Cold Chain)

- 4.2.5 Expanding Agricultural Applications

- 4.3 Market Restraints

- 4.3.1 Volatile Raw Material Prices

- 4.3.2 Safety Concerns Over Residual Monomers in Infant Diapers

- 4.3.3 High Production Cost

- 4.4 Production Cost Overview

- 4.5 Value Supply-Chain Analysis

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Polyacrylamide

- 5.1.2 Acrylic Acid Based

- 5.1.3 Others

- 5.2 By Polymerization Process

- 5.2.1 Solution Polymerization

- 5.2.2 Suspension/Inverse-Suspension Polymerization

- 5.2.3 Gel Polymerization

- 5.3 By Application

- 5.3.1 Baby Diapers

- 5.3.2 Adult Incontinence Products

- 5.3.3 Feminine Hygiene

- 5.3.4 Agriculture Support

- 5.3.5 Other Application

- 5.4 By End-User Industry

- 5.4.1 Personal Care and Hygiene Manufacturers

- 5.4.2 Agriculture Input Suppliers

- 5.4.3 Healthcare Providers

- 5.4.4 Other End-use Industries (Telecom and Power Cable Makers and Food and Pharmaceutical Cold-Chain Logistics)

- 5.5 Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordics

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Egypt

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ADM

- 6.4.2 BASF

- 6.4.3 Braskem

- 6.4.4 Chase Corp.

- 6.4.5 Chemtex Speciality Limited

- 6.4.6 Evonik Industries AG

- 6.4.7 Formosa Plastics Group

- 6.4.8 LG Chem

- 6.4.9 NIPPON SHOKUBAI CO., LTD.

- 6.4.10 SANYO CHEMICAL INDUSTRIES, LTD.

- 6.4.11 SAP SE

- 6.4.12 Satellite Chemical

- 6.4.13 SNF

- 6.4.14 SONGWON

- 6.4.15 SUMITOMO SEIKA CHEMICALS CO.,LTD.

- 6.4.16 TOYO BOEKI Co.,Ltd.

- 6.4.17 Wanhua

- 6.4.18 Yixing Danson Technology

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Commercial Scale-up of 100% Bio-Based SAP

2026-2030年全球超吸收性聚合物市場

2026-2030年全球超吸收性聚合物市場 超吸收性聚合物(SAP)市場規模、佔有率、趨勢和預測:按類型、應用、製造方法和地區分類,2026-2034年

超吸收性聚合物(SAP)市場規模、佔有率、趨勢和預測:按類型、應用、製造方法和地區分類,2026-2034年 超吸收性聚合物市場:2026-2032年全球市場預測(依產品、產品類型、形態、應用及銷售管道)

超吸收性聚合物市場:2026-2032年全球市場預測(依產品、產品類型、形態、應用及銷售管道) 超吸收性材料市場規模、佔有率和成長分析:按材料類型、製造流程、應用、產品形式、分銷管道和地區分類-2026-2033年產業預測

超吸收性材料市場規模、佔有率和成長分析:按材料類型、製造流程、應用、產品形式、分銷管道和地區分類-2026-2033年產業預測 超吸收性聚合物市場:按類型、應用和地區分類

超吸收性聚合物市場:按類型、應用和地區分類 超吸收性聚合物技術市場分析及預測(至2035年):按類型、產品、應用、最終用戶、技術、形態、材料類型、功能和製程分類

超吸收性聚合物技術市場分析及預測(至2035年):按類型、產品、應用、最終用戶、技術、形態、材料類型、功能和製程分類 全球超吸收性聚合物市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球超吸收性聚合物市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球超吸收性聚合物市場報告

2026年全球超吸收性聚合物市場報告 可吸收聚合物市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、區域和競爭格局分類,2021-2031年全球超吸收性聚合物市場:市場規模、佔有率、成長率、產業分析、類型、應用和地區因素及未來預測(2026-2034)

可吸收聚合物市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、區域和競爭格局分類,2021-2031年全球超吸收性聚合物市場:市場規模、佔有率、成長率、產業分析、類型、應用和地區因素及未來預測(2026-2034)