|

市場調查報告書

商品編碼

1939607

化妝品包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Cosmetic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

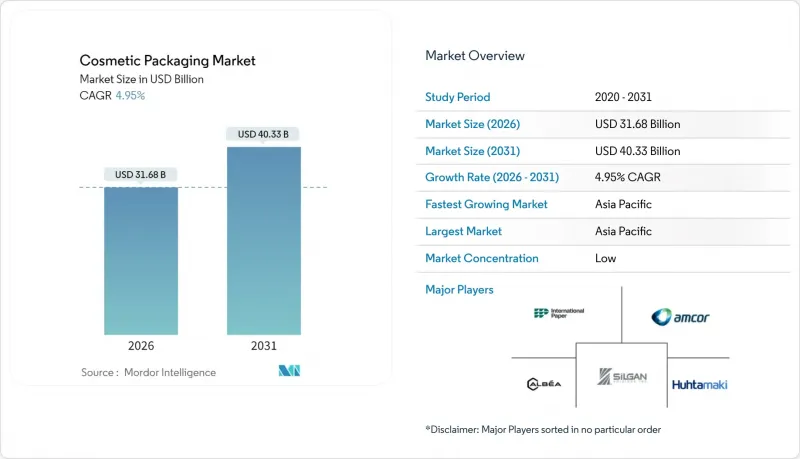

2025年化妝品包裝市場價值為301.9億美元,預計到2031年將達到403.3億美元,而2026年為316.8億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 4.95%。

這項進展反映了各大品牌對歐盟《包裝及包裝廢棄物法規》的正面回應。該法規將於2025年2月生效,強制要求包裝可回收並遵守生產者延伸責任制。由於地緣政治緊張局勢以及中國和歐洲的減產,聚對苯二甲酸乙二醇酯(PET)成本不斷上漲,各大品牌正加速使用再生材料和輕量化設計。亞太地區依然是成長引擎,這得益於成熟的消費習慣和強大的電商物流體系。面膜在中國的成功以及韓國和日本的優質化,都反映了該地區的影響力。包裝材料的選擇持續兩極化,塑膠仍保持其成本優勢,而玻璃則因其在奢侈品、可重複填充產品和循環經濟中的吸引力而日益普及。同時,諸如安姆科以84.3億美元收購貝瑞世界等併購交易,將規模優勢與研發能力結合,加速了永續包裝的普及。

全球化妝品包裝市場趨勢與洞察

高階輕奢美容產品消費量不斷成長

奢華元素正逐漸融入主流管道,觸感豐富的表面處理、厚實的玻璃瓶身和裝飾性瓶蓋等元素正在塑造品牌故事。歐萊雅的「2025世界補充裝日」活動在五年內使其可補充裝產品數量成長了17倍,同時又不影響其高階定位。雅詩蘭黛旗下產品組合中已有71%的原料來自永續來源,顯示環保承諾與奢華可以並存。這促使供應商優先考慮為高階配方產品提供高透明度玻璃和單一材質的泵頭。這項機會也延伸至補充裝套裝,從而促進相關產品的促銷並提高利潤率。奢侈品牌對環境績效的關注正在提升化妝品包裝市場各個細分市場的標準。

轉向適合電子商務的輕量級格式

抗衝擊性和輕量化是線上銷售的關鍵因素。可扁平運輸、減少緩衝和運輸成本的軟包裝袋正以7.67%的複合年成長率快速成長。 KISS Cosmetics對其48萬平方英尺的工廠進行了自動化改造,引進了智慧揀選車和A型架分發系統。事實證明,統一輕便的包裝有利於降低物流成本。預計到2032年,包裝機器人投資將達到75億美元,凸顯了自動化在促進多SKU分銷方面的重要角色。那些將最佳化重點放在配送網路而非零售貨架上的品牌,正在實現更短的周期和更低的排放,從而使全球化妝品包裝市場更能抵禦物流波動的影響。

全球再生樹脂價格波動加劇

2024年,受反傾銷法規導致的供應緊張影響,歐洲PET價格維持在每噸1130歐元至1170歐元之間,迫使加工商在現貨市場競標。 2025年初,由於原物料成本上漲,聚乙烯和聚丙烯的價格也分別上漲了每磅5美分和4美分。承諾使用50%再生材料的品牌正在承受利潤率下降的影響,或透過垂直整合(例如自建清洗廠)進行對沖。由於高品質食品級消費後再生樹脂(PCR)價格溢價較高,供應風險可能會限制設計自由度,並延緩化妝品包裝市場對原生樹脂的替代過程。

細分市場分析

由於塑膠具有成本效益高、透明度好以及與生產線速度相容等優點,預計到2025年,塑膠將佔化妝品包裝市場64.02%的佔有率。聚對苯二甲酸乙二醇酯(PET)在個人護理瓶領域佔據主導地位,聚丙烯(PP)用於製造泵桿和瓶蓋,低密度聚乙烯(LDPE)則用於製造軟管。然而,隨著奢侈品牌追求輕巧、耐刮擦和可無限可再生的特性,預計到2031年,玻璃包裝將以8.32%的複合年成長率快速成長。這種對高階包裝的轉向將使玻璃化妝品包裝獲得兩位數的收入佔有率,即使包裝總量低於塑膠。諸如雅詩蘭黛與Strategic Materials的合作等玻璃回收項目正在提高玻璃屑性能和清涼的質感使其在商店上脫穎而出。纖維板擴大用於運輸容器和禮品套裝中,滿足了電子商務的緩衝需求,同時又不會增加塑膠稅的風險。

第二代材料正在模糊不同類別之間的界線。曾經用於軟管的多層PET-鋁複合材料正逐漸被單一材料的EVOH阻隔PET所取代,同時保持與回收製程的兼容性。聚乳酸等生物基樹脂正在限量版標籤中進行試點,但它們在耐熱性和填充線上的摩擦性方面面臨挑戰,限制了其規模化應用。能夠解決這些挑戰的供應商正在贏得先發製人的契約,這反映了當前化妝品包裝市場中,永續性正在影響供應商選擇標準的趨勢。同時,可回收玻璃瓶專案以及配套的填充站,正是優質可靠性和低環境影響相結合,進一步推動玻璃瓶進入主流產品線的絕佳例證。

到2025年,瓶罐包裝將佔總銷售額的44.12%,這主要得益於其快速填充和消費者對其的熟悉度。寬口瓶仍然是乳霜的首選包裝,而窄口寶特瓶則在洗髮精和卸妝水中佔據主導地位。然而,袋裝和立式袋的銷售持續成長,複合年成長率高達7.41%,它們不僅能減輕單次使用重量,防曬油運輸過程中破損。合理的包裝技術使品牌能夠將每月包裝數量從一瓶減少到每袋五袋,從而降低運輸過程中的排放強度。軟管和棒狀包裝迎合了攜帶式防曬霜、固態精華和潤色膏等產品的需求,同時也符合旅行裝的規格要求和對完全防漏性能的期望。可折疊紙盒仍然是高階包裝的首選,用於盛裝玻璃瓶和精華液管瓶,並透過觸感柔軟的表面和燙金工藝來講述品牌故事。

運輸包裝箱也在不斷發展。紙板製造商利用演算法減少填充物,而Packsize機器則可根據即時訂單尺寸切割紙板。消費者的開箱體驗正成為全通路差異化的關鍵因素,帶有QR碼即可啟動數位會員獎勵。軟包裝上的阻隔塗層正在向二氧化矽和氧化鋁轉變,既能保持產品風味,又能降低氧氣滲透性。這在不影響可回收性的前提下,拓展了軟包裝材料的市場,並重新定義了不再僅依賴硬質包裝的「大眾高階」美學。

化妝品包裝市場按材料類型(塑膠、玻璃、金屬、紙/紙板)、產品類型(瓶/罐、管/棒、折疊紙盒、運輸瓦楞紙箱等)、分配方式(泵、滴管/移液管、噴霧/噴霧等)、化妝品類型(護髮、彩妝品、護膚等)和地區進行細分。市場規模和預測以美元計價。

區域分析

預計到2025年,亞太地區將佔全球化妝品包裝市場收入的42.55%,並在2031年之前以7.18%的複合年成長率成長,這主要得益於可支配收入的成長、韓妝的興起以及移動商務的高滲透率。面膜在中國的爆紅表明,當地對一次性且精緻的包裝有著強勁的需求,這使得該地區成為簡約實用包裝袋的熱門市場。日本和韓國正將無氣墊粉底和纖細旋轉膏等設計元素輸出到全球,這為區域內的加工商帶來了先發優勢。

北美市場保持強勁成長勢頭,這主要得益於高階護膚品的流行和電子商務的快速發展。專賣店正在擴大試驗推行填充站,這為玻璃墨盒供應商帶來了新的服務合約。自動化程度的提高加速了機器人相容紙板包裝和無底紙標籤的普及。各州推出的塑膠減量法規正在推動轉向輕量化、單一材料的解決方案,從而促進了對再生PET和纖維替代品的投資。儘管化妝品包裝市場趨於成熟,但這些趨勢仍支撐著該市場蓬勃發展。

歐洲正在建立具有全球影響力的法規結構。法國實施的《塑膠包裝法規》(PPWR)以及不斷提高的環保費用,正在製定明確的包裝回收標準,並加速對可拆卸設計的投資。法國和義大利的奢侈香水叢集主導著玻璃材料的創新,包括用於提高耐刮擦性的先進熱端塗層。同時,中東歐正在擴大瓶型成型產能,以支持本土品牌和出口生產。全球各區域正攜手合作,共同影響材料策略和技術轉移的步伐,並將化妝品包裝市場的需求促進因素連結起來。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 高階和陳年美容產品的消費量不斷增加

- 過渡到更輕量級的格式,以適應電子商務

- 奢侈品通路中可重複填充/可重複使用配送系統的興起

- 具有防偽功能的智慧包裝

- 品牌對符合碳標籤標準的包裝的需求

- 第三方物流(3PL)履約中機器人輔助二次包裝的快速普及

- 市場限制

- 全球再生樹脂價格波動加劇

- 一次性塑膠製品的監管上限

- 新型生物基材料與填充線的不相容性

- 掩埋容量減少導致生產者責任成本上升

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依材料類型

- 塑膠

- 聚對苯二甲酸乙二醇酯(PET)

- 聚丙烯(PP)

- 聚乙烯(PE)

- 其他塑膠

- 玻璃

- 金屬

- 紙和紙板

- 塑膠

- 依產品類型

- 瓶子和罐子

- 管子和棍子

- 可折疊瓦楞紙箱

- 紙板運輸箱

- 軟性小袋和包裝袋

- 其他產品類型

- 透過管理機制

- 泵浦類型

- 滴管/移液器

- 噴霧/霧

- 棒狀/旋轉式

- 罐子/湯匙

- 依化妝品類型

- 護膚

- 臉部保養

- 身體保養

- 護髮

- 彩妝品

- 香水及香氛

- 其他化妝品類型

- 護膚

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲地區

- 中東

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Albea SA

- AptarGroup Inc.

- Amcor Group GmbH

- Silgan Holdings Inc.

- DS Smith PLC

- Graham Packaging LP

- Quadpack Industries SA

- Libo Cosmetics Co. Ltd

- Gerresheimer AG

- Ball Corporation

- Verescence France SA

- SKS Bottle & Packaging Inc.

- Altium Packaging

- Cosmopak Ltd

- Raepak Ltd

- Rieke Corporation

- Essel Propack Ltd

- Huhtamaki Oyj

- Alpla Werke Alwin Lehner GmbH

- RPC M&H Plastics

- HCP Packaging Co. Ltd

第7章 市場機會與未來展望

The cosmetic packaging market was valued at USD 30.19 billion in 2025 and estimated to grow from USD 31.68 billion in 2026 to reach USD 40.33 billion by 2031, at a CAGR of 4.95% during the forecast period (2026-2031).

The advance mirrors brand responses to the European Union's Packaging and Packaging Waste Regulation, effective February 2025, which obliges recyclability and extended producer responsibility compliance. Brands counter rising polyethylene terephthalate costs driven by geopolitical tension and production cuts in China and Europe by accelerating recycled-content usage and lightweight designs. Asia-Pacific remains the growth engine, propelled by sophisticated consumer routines and strong e-commerce logistics; Chinese facial sheet-mask success and premiumization across South Korea and Japan typify the region's influence. Material choice continues to bifurcate: plastics retain cost leadership while glass advances on luxury, refillable, and circular-economy appeal. Meanwhile, corporate consolidation highlighted by Amcor's USD 8.43 billion merger with Berry Global bundles scale and R&D to quicken sustainable-packaging rollouts.

Global Cosmetic Packaging Market Trends and Insights

Growing Consumption of Premium and Masstige Beauty Products

Luxury cues have migrated into mainstream channels as tactile finishes, heavy-wall glass, and ornate closures shape brand storytelling. L'Oreal's 2025 World Refill Day push lifted refillable options seventeen-fold in five years without diluting premium positioning. Estee Lauder already supplies 71% of its portfolio in sustainable formats, confirming that environmental progress and upscale image can co-exist. Suppliers thus prioritise high-clarity glass and mono-material pumps that tolerate prestige formulations. The opportunity extends to refill kits that guarantee adjacency sales and invite higher margins. Luxury's embrace of environmental performance raises the bar for all tiers of the cosmetic packaging market.

Shift Toward E-commerce-Friendly Lightweight Formats

Online sales make damage resistance and dimensional-weight savings decisive. Flexible pouches grow at 7.67% CAGR because they ship flat, cut void fill, and slash freight spend. KISS Cosmetics automated its 480,000 ft2 facility with intelligent cart-picking and A-Frame dispensing, demonstrating fulfilment economics that favour uniform, lighter packs. Packaging-robot investments are projected to reach USD 7.5 billion by 2032, underlining automation's role in smoothing multi-SKU flows. Brands that optimise for courier networks rather than retail shelves secure faster cycle times and lower emissions, fortifying the global cosmetic packaging market against logistics volatility.

Escalating Global Recycled-Resin Price Volatility

European PET hovered at EUR 1,130-1,170 per t in 2024 as anti-dumping rules tightened supply, forcing converters into spot-market bidding wars. Polyethylene and polypropylene followed with five-cent and four-cent per-lb upticks in early 2025 as feedstock costs rose. Brands with 50%-recycled-content pledges thus absorb margin shocks or hedge via vertical integration, such as on-site washing plants. Because high-quality food-grade PCR commands premiums, availability risk constrains design freedom and may slow substitutions away from virgin resin in the cosmetic packaging market.

Other drivers and restraints analyzed in the detailed report include:

- Rise of Refillable/Reusable Delivery Systems in Prestige Channels

- Rapid Adoption of Robot-Ready Secondary Packs in 3-PL Fulfilment

- Regulatory Caps on Single-Use Plastic

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastics held a 64.02% cosmetic packaging market share in 2025 thanks to cost efficiency, clarity, and line-speed compatibility. Polyethylene terephthalate leads for personal-care bottles, polypropylene secures pump stems and closures, while low-density polyethylene shapes flexible tubes. Yet glass races ahead at 8.32% CAGR to 2031 because prestige brands crave heft, scratch resistance, and infinite recyclability. The premium shift lifts the cosmetic packaging market size for glass to meaningful double-digit revenue slices even as total pack count stays lower than plastic. Glass-recycling initiatives such as Estee Lauder's work with Strategic Materials Inc.improve cullet quality and furnace yields, soothing environmental criticisms. Metallised aluminium and steel remain niche for fragrances and gifting editions where barrier performance and tactile coolness drive shelf impact. Fibre-based board escalates in transit shippers and gift sets, answering e-commerce cushioning needs without raising plastic tax exposure.

Second-generation materials blur lines between categories. Multi-layer PET-aluminium laminates once seen in tubes migrate toward mono-material EVOH-barrier PET that retains recycling stream compatibility. Bio-sourced resins such as polylactic acid win trial runs for limited-edition labels but still battle heat resistance and filling-line friction, limiting scale. Suppliers addressing these hurdles gain early-mover contracts, reflecting how sustainability performance now shapes vendor selection criteria across the cosmetic packaging market. Meanwhile, returnable glass programs aligned with refill stations exemplify how premium credentials fuse with low-impact ambitions to pull glass farther into mainstream assortments.

Bottles and jars delivered 44.12% revenue in 2025, supported by high filling speeds and shopper familiarity. Wide-mouth jars continue to anchor face creams, while narrow-neck PET bottles dominate shampoos and micellar waters. However, sachets and stand-up pouches compound at a brisk 7.41% CAGR, cutting grams per dose and resisting breakage during courier drops. Right-size technology lets brands switch from one bottle-per-month to five flat sachets per envelope, lowering freight-emissions intensity. Tubes and sticks address on-the-go sunscreen, solid serum, and colour-balm trends, meshing with travel-size regulation and zero-leak expectations. Folding cartons remain favoured in luxury presentations, housing glass flacons or booster vials while conveying brand narratives through soft-touch varnish and foil embossing.

Transit boxes evolve too. Corrugated suppliers deploy algorithmic box-making to trim void fill, supported by Packsize machines that cut board in line with real-time order dimensions. Consumer unboxing gains differentiate omnichannel experiences, prompting QR-printed inserts that trigger digital loyalty rewards. Flexible-pack barrier coatings upgrade to silicon oxide or aluminium oxide, securing fragrance retention and reducing oxygen transmission without disqualifying recyclability. Such advances swell the cosmetic packaging market size credited to flexible formats and re-define mass-premium aesthetics away from solely rigid containers.

Cosmetic Packaging Market is Segmented by Material Type (Plastic, Glass, Metal, Paper and Paperboard), Product Type (Bottles and Jars, Tubes and Sticks, Folding Cartons, Corrugated Transit Boxes, and More), Dispensing Mechanism (Pump-Based, Dropper / Pipette, Spray / Mist, and More), Cosmetic Type (Hair Care, Color Cosmetics, Skin Care, and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific owned 42.55% of cosmetic packaging market revenue in 2025 and will grow at a 7.18% CAGR to 2031, lifted by rising disposable income, advanced K-beauty regimens, and high mobile-commerce penetration. Sheet-mask dominance in China illustrates local appetite for single-use but sophisticated pack forms, making the region a hotbed for minimalist yet functional pouches. Japan and South Korea export design cues globally, such as airless cushion compacts and slim twist balms, giving regional converters first-mover advantages.

North America holds firm value through premium skincare adoption and rapid e-commerce. Refill station pilots appear in beauty specialty retailers, rewarding glass cartridge suppliers with new service contracts. Automation readiness drives widespread acceptance of robot-friendly corrugate and linerless labels. State-level plastic-reduction bills add urgency to lightweight mono-material shifts, redirecting investment towards recycled-content PET and fibre substitution. These moves keep the cosmetic packaging market buoyant despite mature category penetration.

Europe shapes regulatory frameworks that ripple worldwide. Enforcement of the PPWR and escalating eco-contribution fees in France imposes clear packaging recyclability thresholds, accelerating investment in design for disassembly. Luxury fragrance clusters in France and Italy champion glass innovation, including advanced hot-end coating for scratch reduction. Meanwhile, Central and Eastern Europe attract bottle moulding capacity expansions to serve both local brands and export production. Collectively, global regions influence material strategies and technology transfer rates, interlocking demand drivers for the cosmetic packaging market.

- Albea SA

- AptarGroup Inc.

- Amcor Group GmbH

- Silgan Holdings Inc.

- DS Smith PLC

- Graham Packaging LP

- Quadpack Industries SA

- Libo Cosmetics Co. Ltd

- Gerresheimer AG

- Ball Corporation

- Verescence France SA

- SKS Bottle & Packaging Inc.

- Altium Packaging

- Cosmopak Ltd

- Raepak Ltd

- Rieke Corporation

- Essel Propack Ltd

- Huhtamaki Oyj

- Alpla Werke Alwin Lehner GmbH

- RPC M&H Plastics

- HCP Packaging Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing consumption of premium and masstige beauty products

- 4.2.2 Shift toward e-commerce-friendly lightweight formats

- 4.2.3 Rise of refillable / reusable delivery systems in prestige channels

- 4.2.4 Authentication-enabled smart packaging to curb counterfeits

- 4.2.5 Brand demand for carbon-label-ready packs

- 4.2.6 Rapid adoption of robot-ready secondary packs in 3-PL fulfilment

- 4.3 Market Restraints

- 4.3.1 Escalating global recycled-resin price volatility

- 4.3.2 Regulatory caps on single-use plastics

- 4.3.3 Filling-line incompatibility of novel bio-materials

- 4.3.4 Shrinking landfill capacity driving extended-producer-responsibility fees

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Plastics

- 5.1.1.1 Polyethylene Terephthalate (PET)

- 5.1.1.2 polypropylene (PP)

- 5.1.1.3 Polyethylene (PE)

- 5.1.1.4 Other Plastics

- 5.1.2 Glass

- 5.1.3 Metal

- 5.1.4 Paper and Paperboard

- 5.1.1 Plastics

- 5.2 By Product Type

- 5.2.1 Bottles and Jars

- 5.2.2 Tubes and Sticks

- 5.2.3 Folding Cartons

- 5.2.4 Corrugated Transit Boxes

- 5.2.5 Flexible Sachets and Pouches

- 5.2.6 Other Product Type

- 5.3 By Dispensing Mechanism

- 5.3.1 Pump-based

- 5.3.2 Dropper / Pipette

- 5.3.3 Spray / Mist

- 5.3.4 Stick / Twist-up

- 5.3.5 Jar / Scoop

- 5.4 By Cosmetic Type

- 5.4.1 Skin Care

- 5.4.1.1 Facial Care

- 5.4.1.2 Body Care

- 5.4.2 Hair Care

- 5.4.3 Color Cosmetics

- 5.4.4 Perfumes and Fragrances

- 5.4.5 Other Cosmetics Type

- 5.4.1 Skin Care

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacifc

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Nigeria

- 5.5.4.2.3 Kenya

- 5.5.4.2.4 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Albea SA

- 6.4.2 AptarGroup Inc.

- 6.4.3 Amcor Group GmbH

- 6.4.4 Silgan Holdings Inc.

- 6.4.5 DS Smith PLC

- 6.4.6 Graham Packaging LP

- 6.4.7 Quadpack Industries SA

- 6.4.8 Libo Cosmetics Co. Ltd

- 6.4.9 Gerresheimer AG

- 6.4.10 Ball Corporation

- 6.4.11 Verescence France SA

- 6.4.12 SKS Bottle & Packaging Inc.

- 6.4.13 Altium Packaging

- 6.4.14 Cosmopak Ltd

- 6.4.15 Raepak Ltd

- 6.4.16 Rieke Corporation

- 6.4.17 Essel Propack Ltd

- 6.4.18 Huhtamaki Oyj

- 6.4.19 Alpla Werke Alwin Lehner GmbH

- 6.4.20 RPC M&H Plastics

- 6.4.21 HCP Packaging Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球真空瓶市場報告

2026年全球真空瓶市場報告 化妝品包裝市場預測至2034年—按材料、包裝類型、功能、永續性、應用、最終用戶和地區分類的全球分析

化妝品包裝市場預測至2034年—按材料、包裝類型、功能、永續性、應用、最終用戶和地區分類的全球分析 化妝品和盥洗用品容器市場:2026-2032年全球市場預測(按容器類型、材質、封蓋類型、容量、分銷管道和應用分類)

化妝品和盥洗用品容器市場:2026-2032年全球市場預測(按容器類型、材質、封蓋類型、容量、分銷管道和應用分類) 化妝品包裝市場規模、佔有率和成長分析:按材料類型、包裝類型、化妝品類型和地區分類-2026-2033年產業預測

化妝品包裝市場規模、佔有率和成長分析:按材料類型、包裝類型、化妝品類型和地區分類-2026-2033年產業預測 化妝品包裝市場分析及預測(至2035年):依類型、產品類型、材料類型、技術、應用、最終用戶、功能及製程分類

化妝品包裝市場分析及預測(至2035年):依類型、產品類型、材料類型、技術、應用、最終用戶、功能及製程分類 化妝品包裝市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年全球化妝品包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球護膚包裝市場規模、佔有率、趨勢及成長分析報告(2026-2034年)

化妝品包裝市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年全球化妝品包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球護膚包裝市場規模、佔有率、趨勢及成長分析報告(2026-2034年) 日本化妝品包裝市場規模、佔有率、趨勢及預測(依材料類型、產品類型、化妝品類型及地區分類),2026-2034年2026年全球化妝品包裝市場報告

日本化妝品包裝市場規模、佔有率、趨勢及預測(依材料類型、產品類型、化妝品類型及地區分類),2026-2034年2026年全球化妝品包裝市場報告