|

市場調查報告書

商品編碼

1939599

熱塑性聚氨酯(TPU):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Thermoplastic Polyurethane (TPU) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

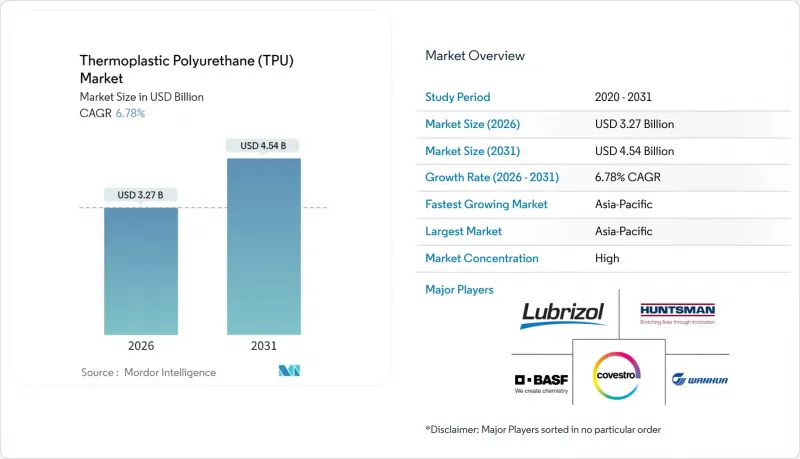

熱塑性聚氨酯市場預計將從 2025 年的 30.6 億美元成長到 2026 年的 32.7 億美元,預計到 2031 年將達到 45.4 億美元,2026 年至 2031 年的複合年成長率為 6.78%。

這一成長主要得益於鞋類、汽車、醫療設備和積層製造(3D列印)等行業需求的不斷成長。加工商正在尋找兼具彈性、耐磨性和易加工性的材料。聚酯類材料因其優異的機械性能和成本平衡而佔據主導地位。同時,生物基原料和閉合迴路設計的運用正幫助品牌滿足永續性的要求。輕量化電動車的日益普及、穿戴式健康監測設備的廣泛應用以及軟性太陽能組件中TPU膜的日益普及,進一步擴大了熱塑性聚氨酯市場的潛在基本客群。從區域來看,亞太地區憑藉其一體化的供應鏈和大規模的下游生產能力,成為最具競爭力的地區,而北美製造商則在法規遵循和特殊應用創新方面處於主導。

全球熱塑性聚氨酯(TPU)市場趨勢與洞察

穿戴式醫療設備

連續血糖監測儀、智慧型心臟貼片和新一代導管的快速普及推動了醫用級TPU的需求。這些設備需要觸感柔軟、具有長期皮膚相容性和耐彎曲性。為了滿足亞洲醫療技術製造商的在地化供應需求,Avient公司在其通過ISO 13485認證的蘇州工廠將NEUSoft TPU的產能提高了三倍。隨後,Lubrizol和Polyhose公司在泰米爾納德邦建立了一家管材製造廠,將神經血管產品的產能提高了五倍。此類垂直整合的投資透過縮短前置作業時間和確保材料等級通過嚴格的生物相容性測試,進一步加速了熱塑性聚氨酯市場的發展。

3D列印耗材和粉末

積層製造技術正在革新原型製作流程,使功能性零件能夠模擬最終用途的性能。BASF的 Ultrasint TPU01運作粉末層熔融平台,實現了 80% 的粉末回收率和 88-90 的邵氏 A 硬度。這賦予了材料優異的能量回彈性能,使其適用於晶格中底和汽車吸震管道。製程穩定性降低了廢棄物,而回收粉末的使用降低了單一部件的成本,從而鼓勵一級供應商將 TPU 整合到大規模生產線中。這提高了設計自由度,加速了迭代開發,並促進了熱塑性聚氨酯市場的廣泛應用。

1,4-BDO原物料價格波動

聚酯和聚醚型熱塑性聚氨酯(TPU)的軟段化學結構中均含有1,4-丁二醇。供應中斷和對兩用物項監管的日益嚴格審查推高了交易價格,並使庫存計劃變得複雜。化學品經銷商報告稱,與受限物質相關的文書工作會延誤清關,並在需求激增期間延長前置作業時間。儘管生產商透過多種籌資策略和期貨合約來對沖風險,但他們仍然面臨利潤率壓縮,這限制了熱塑性聚氨酯市場的產能擴張計劃。

細分市場分析

預計到2025年,聚酯基TPU將佔總銷售額的39.35%,複合年成長率達7.73%,成為熱塑性聚氨酯市場中規模最大且成長最快的細分市場。其優異的耐油耐脂性能使其在液壓軟管、電線塗層和汽車動力帶等領域具有顯著優勢。BASF的Elastollan B CF系列產品可將成型週期縮短25%,並將硬度範圍從邵氏A25擴展至邵氏D70。這使得生產兼具透明度和低溫衝擊強度的零件成為可能,從而提高了二次加工商的生產效率和經濟效益。

聚醚基熱塑性聚氨酯(TPU)在對耐水解性要求極高的應用領域,例如氣動管道和戶外電纜,仍然保持著良好的市場需求。聚己內酯基TPU在生物可吸收支架領域取得了一些進展。靜電紡絲奈米纖維透過模擬細胞外基質並支持藥物控釋,正在拓展臨床研究的管道。化學結構的多樣性確保熱塑性聚氨酯市場能滿足各行業廣泛的性能要求。

區域分析

預計到2025年,亞太地區將佔全球收入的57.40%,並在2031年之前維持7.55%的年均成長率。中國垂直整合的供應鏈集中了原料採購、配製和加工環節,降低了服務交付成本。 Avient在蘇州的投資實現了導管級TPU的本地化生產,有助於縮短區域醫療設備製造商的前置作業時間。同時,路博潤在印度的導管製造計劃將使其區域產能擴大五倍,進而增強心血管器械OEM廠商的供應保障。

北美位居第二,這主要得益於高性能運動用品、醫療拋棄式產品和特殊薄膜領域的高應用率。對二異氰酸酯監管的日益嚴格提高了市場准入門檻,同時也推動了低遊離異氰酸酯預聚物和生物基碳材料的創新。此外,對積層製造的投資也促進了該地區材料的差異化發展,從而支持熱塑性聚氨酯市場細分領域的成長。

歐洲正充分利用主導地位。各大品牌優先考慮可再生碳原料和透明的廢棄物處理方案,加速了對生質能平衡型TPU的需求。德國和法國的汽車零件製造商正在整合TPU密封件以滿足歐盟的排放氣體目標,而義大利時尚品牌則在高階配件領域採用無溶劑TPU合成皮革。

儘管南美洲和中東及非洲地區仍在發展中,但它們具有重要的戰略意義。巴西的製鞋叢集正在增加對可再生TPU顆粒的需求,而阿拉伯聯合大公國的建築商則指定使用能夠抵禦沙漠紫外線的TPU屋頂防水卷材。由於當地產能有限,跨國製造商正在建立分銷中心和技術服務中心,以打入新興的熱塑性聚氨酯市場。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 穿戴式醫療設備推動了對醫用級TPU的需求。

- 3D列印耗材和粉末加速原型製作技術的普及

- 生物基鞋類計畫推動消費

- 柔軟性太陽能和建築膜材料從PVC到TPU的過渡

- 在工業應用的使用日益增多

- 市場限制

- 1,4-丁二醇原料價格的波動推高了聚酯/醚基TPU的價格。

- 加強對異氰酸酯暴露的監管

- 汽車應用中耐熱TPEE/TPV替代的風險

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依產品類型

- 聚酯TPU

- 聚醚基熱塑性聚氨酯(TPU)

- 聚己內酯基熱塑性聚氨酯(TPU)

- 透過使用

- 擠出成型產品

- 射出成型產品

- 黏合劑

- 其他用途

- 按最終用途行業分類

- 鞋類

- 車

- 醫療保健

- 電氣和電子設備

- 建造

- 重工業

- 其他終端用戶產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 策略趨勢

- 市佔率分析

- 公司簡介

- BASF

- Avient Corporation

- Coim Group

- Covestro AG

- Dongsung

- Epaflex Polyurethanes SpA

- Hexpol AB

- Huntsman International LLC

- Miracll Chemicals Co. Ltd

- Mitsui Chemicals Inc.

- Novotex Italiana SpA

- Sumei Chemical Co. Ltd

- Suzhou Austen New Mstar Technology Ltd

- Taiwan PU Corporation

- The Lubrizol Corporation

- Tosoh Corporation

- Trinseo

- Wanhua Chemical Group Co. Ltd

第7章 市場機會與未來展望

The Thermoplastic Polyurethane market is expected to grow from USD 3.06 billion in 2025 to USD 3.27 billion in 2026 and is forecast to reach USD 4.54 billion by 2031 at 6.78% CAGR over 2026-2031.

Expanding demand across footwear, automotive, medical devices, and additive manufacturing anchors this growth as converters seek materials that combine elasticity, abrasion resistance, and ease of processing. Polyester grades hold sway because they balance mechanical performance with cost, while bio-based content and closed-loop designs help brands meet sustainability mandates. Rising lightweighting in electric vehicles, strong adoption in wearable health monitors, and increased use of TPU membranes in flexible solar modules further widen the addressable base of the thermoplastic polyurethane market. Regional competitive intensity is highest in Asia-Pacific due to integrated supply chains and sizable downstream capacity, yet North American producers set the pace on regulatory compliance and specialty innovation.

Global Thermoplastic Polyurethane (TPU) Market Trends and Insights

Wearable medical devices

Surging adoption of continuous glucose monitors, smart cardiac patches and next-generation catheters is intensifying the pull for medical-grade TPU. These devices require soft touch, long-term skin compatibility and kink resistance. Avient tripled capacity for its NEUSoft TPU in Suzhou under ISO 13485 certification to localize supply for Asian health-tech manufacturers . Lubrizol and Polyhose followed with a Tamil Nadu tubing plant that scales neurovascular products five-fold . Such vertical investments shorten lead times and lock in material grades that can pass stringent biocompatibility testing, adding momentum to the thermoplastic polyurethane market.

3D-printing filaments & powders

Additive manufacturing reshapes prototype cycles by enabling functional parts that mimic end-use performance. BASF's Ultrasint TPU01 runs on powder-bed fusion platforms with 80% powder recyclability and 88-90 Shore A hardness, delivering energy return suited to lattice midsoles and impact-absorbing automotive ducts. Process stability lowers scrap while recycled powder cuts cost per part, encouraging tier-1 suppliers to integrate TPU into serial production. The resulting design freedom accelerates iteration and supports broader adoption across the thermoplastic polyurethane market.

1,4-BDO feedstock volatility

Polyester and polyether TPU rely on 1,4-butanediol for soft-segment chemistry. Supply disruptions and dual-use regulatory scrutiny raise transaction prices and complicate inventory planning. Chemical distributors report that controlled-substance documentation slows customs clearance, extending lead times during demand spikes. Producers hedge with multi-sourcing strategies and forward contracts but still face margin compression that restrains capacity expansion plans in the thermoplastic polyurethane market.

Other drivers and restraints analyzed in the detailed report include:

- Bio-based mono-material footwear

- PVC-to-TPU shift in membranes

- Tightening isocyanate regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyester TPU generated 39.35% of 2025 revenue and is projected to grow at 7.73% CAGR, establishing it as both the largest and fastest segment within the thermoplastic polyurethane market. Robust oil and grease resistance underpins its dominance in hydraulic hoses, wire coatings and dynamic automotive belts. BASF's Elastollan B CF series trims cycle times by 25% and widens hardness coverage from 25 Shore A to 70 Shore D, enabling parts that combine clarity with low-temperature impact strength. The resulting productivity gains improve economic viability for secondary converters.

Polyether TPU sustains demand where hydrolysis resistance is paramount, such as pneumatic tubes and outdoor cables. Polycaprolactone TPU, though smaller, advances in bio-resorbable scaffolds. Electrospun nanofibers mimic extracellular matrices and support controlled drug release, expanding clinical research pipelines. Diversified chemistry assures that the thermoplastic polyurethane market can address divergent performance specifications across industries.

The Thermoplastic Polyurethane Market Report Segments the Industry by Product Type (Polyester TPU, Polyether TPU, Polycaprolactone TPU), Application (Extruded Products, Injection Molded Products, and More), End-User Industry (Footwear, Automotive, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific controlled 57.40% of global revenue in 2025 and is set to compound at 7.55% annually to 2031. China's vertically integrated supply chain secures raw materials, compounding and conversion under one roof, thereby compressing cost to serve. Avient's Suzhou investment localises catheter-grade TPU production, cutting lead times for regional device makers. Concurrently, Lubrizol's Indian tubing project lifts regional capacity five-fold and enhances supply resilience for cardiovascular OEMs.

North America ranks second owing to high adoption in performance sports, medical disposables and specialty films. Regulatory tightening on diisocyanates elevates barriers to entry yet spurs innovation in low-free-isocyanate prepolymers and bio-based carbon routes. Investments in additive manufacturing also advance regional material differentiation, supporting niche growth inside the thermoplastic polyurethane market.

Europe leverages its leadership in circular economy frameworks. Brands favour renewable carbon feedstocks and transparent end-of-life schemes, accelerating demand for biomass-balanced TPU grades. Automotive suppliers in Germany and France integrate TPU seal profiles to meet EU fleet emission targets, while Italian fashion houses adopt solvent-free TPU synthetic leather for luxury accessories.

South America and the Middle East & Africa remain nascent but strategic. Brazilian footwear clusters consume increasing volumes of recyclable TPU pellets, while United Arab Emirates contractors specify TPU roofing membranes to withstand desert UV exposure. Local production remains limited, encouraging multinational producers to establish distribution hubs and technical service centers to penetrate these emerging nodes of the thermoplastic polyurethane market.

- BASF

- Avient Corporation

- Coim Group

- Covestro AG

- Dongsung

- Epaflex Polyurethanes SpA

- Hexpol AB

- Huntsman International LLC

- Miracll Chemicals Co. Ltd

- Mitsui Chemicals Inc.

- Novotex Italiana SpA

- Sumei Chemical Co. Ltd

- Suzhou Austen New Mstar Technology Ltd

- Taiwan PU Corporation

- The Lubrizol Corporation

- Tosoh Corporation

- Trinseo

- Wanhua Chemical Group Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Wearable Medical Devices Driving Medical-Grade TPU Demand

- 4.2.2 3D-Printing Filaments & Powders Accelerating Prototyping Adoption

- 4.2.3 Bio-Based Mono-Material Footwear Programs Boosting Consumption

- 4.2.4 PVC-to-TPU Shift in Flexible Solar & Architectural Membranes

- 4.2.5 Rising Usage in Industrial Applications

- 4.3 Market Restraints

- 4.3.1 1,4-BDO Feedstock Volatility Inflating Polyester/Ether TPU Prices

- 4.3.2 Tightening Isocyanate-Exposure Regulations

- 4.3.3 Displacement Risk from High-Heat TPEE & TPV in Automotive Application

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Polyester TPU

- 5.1.2 Polyether TPU

- 5.1.3 Polycaprolactone TPU

- 5.2 By Application

- 5.2.1 Extruded Products

- 5.2.2 Injection Molded Products

- 5.2.3 Adhesives

- 5.2.4 Other Applications

- 5.3 By End-Use Industry

- 5.3.1 Footwear

- 5.3.2 Automotive

- 5.3.3 Medical

- 5.3.4 Electrical & Electronics

- 5.3.5 Construction

- 5.3.6 Heavy Engineering

- 5.3.7 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordics

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Chile

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 Asia Pacific

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global & Market Overview, Core Segments, Financials, Strategy, Rank/Share, Products, Recent Developments)

- 6.3.1 BASF

- 6.3.2 Avient Corporation

- 6.3.3 Coim Group

- 6.3.4 Covestro AG

- 6.3.5 Dongsung

- 6.3.6 Epaflex Polyurethanes SpA

- 6.3.7 Hexpol AB

- 6.3.8 Huntsman International LLC

- 6.3.9 Miracll Chemicals Co. Ltd

- 6.3.10 Mitsui Chemicals Inc.

- 6.3.11 Novotex Italiana SpA

- 6.3.12 Sumei Chemical Co. Ltd

- 6.3.13 Suzhou Austen New Mstar Technology Ltd

- 6.3.14 Taiwan PU Corporation

- 6.3.15 The Lubrizol Corporation

- 6.3.16 Tosoh Corporation

- 6.3.17 Trinseo

- 6.3.18 Wanhua Chemical Group Co. Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

- 7.2 Shifting Focus Toward the Development of Bio-based Products

熱塑性聚氨酯市場:按類型、製造方法、加工方法、應用和分銷管道分類-2026-2032年全球市場預測

熱塑性聚氨酯市場:按類型、製造方法、加工方法、應用和分銷管道分類-2026-2032年全球市場預測 熱塑性聚氨酯(TPU)市場預測至2034年-按原料、類型、加工方法、應用和地區分類的全球分析

熱塑性聚氨酯(TPU)市場預測至2034年-按原料、類型、加工方法、應用和地區分類的全球分析 全球熱塑性聚氨酯市場

全球熱塑性聚氨酯市場 熱塑性聚氨酯(TPU)市場規模、佔有率、趨勢和預測:按類型、原料、應用、最終用途行業和地區分類,2026-2034年

熱塑性聚氨酯(TPU)市場規模、佔有率、趨勢和預測:按類型、原料、應用、最終用途行業和地區分類,2026-2034年 熱塑性聚氨酯(TPU)市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年TPU軟管和管材市場材料類型、增強結構、壓力等級和最終用途行業分類,全球預測,2026-2032年TPU軟管市場按材料類型、應用和分銷管道分類,全球預測(2026-2032年)全球多潤滑熱塑性聚氨酯管材市場(按管流明數、產品類型、應用和最終用途產業分類)預測(2026-2032年)

熱塑性聚氨酯(TPU)市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年TPU軟管和管材市場材料類型、增強結構、壓力等級和最終用途行業分類,全球預測,2026-2032年TPU軟管市場按材料類型、應用和分銷管道分類,全球預測(2026-2032年)全球多潤滑熱塑性聚氨酯管材市場(按管流明數、產品類型、應用和最終用途產業分類)預測(2026-2032年) 熱塑性聚氨酯(TPU)市場分析與預測(至2035年):類型、產品類型、應用、技術、形態、材料類型、最終用戶、功能、工藝

熱塑性聚氨酯(TPU)市場分析與預測(至2035年):類型、產品類型、應用、技術、形態、材料類型、最終用戶、功能、工藝 熱塑性聚氨酯市場規模、佔有率和趨勢分析報告:按類型、應用、地區和細分市場預測(2026-2033 年)

熱塑性聚氨酯市場規模、佔有率和趨勢分析報告:按類型、應用、地區和細分市場預測(2026-2033 年)