|

市場調查報告書

商品編碼

1939598

汽車輪胎壓力監測系統(TPMS):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Automotive TPMS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

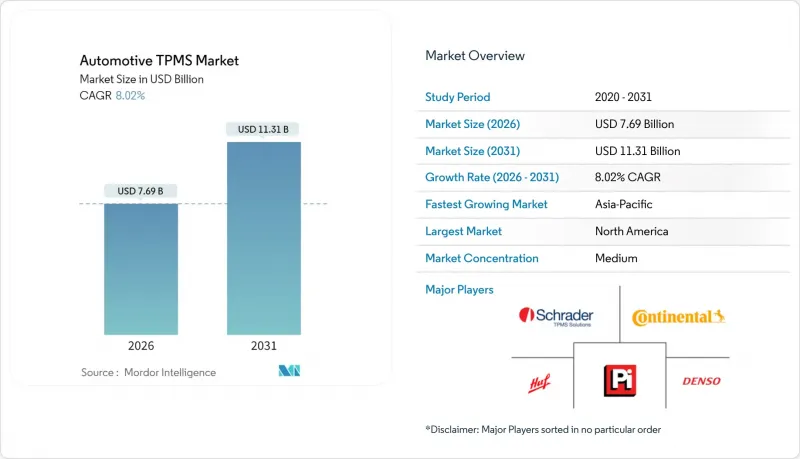

汽車輪胎壓力監測系統 (TPMS) 市場預計將從 2025 年的 71.2 億美元成長到 2026 年的 76.9 億美元,預計到 2031 年將達到 113.1 億美元,2026 年至 2031 年的複合年成長率為 8.02%。

這項成長的驅動力來自日益嚴格的安全法規、向電動動力傳動系統的轉型,以及輪胎數據與高級駕駛輔助系統和聯網汽車基礎設施的深度整合。即時輪胎健康分析正在取代傳統的僅提供胎壓警報,使汽車製造商能夠將預測性維護與空中軟體更新相結合,同時保障對重量敏感的電動車車型的續航里程。感測器、閘道器和雲端平台的整合也降低了系統成本,加速了其在摩托車和商用車車隊的應用。同時,壓電能源採集技術的創新和安全的2.4GHz連接正在重新定義感測器的自供電方式以及輪胎、閘道器和雲端之間的數據傳輸方式,為汽車輪胎壓力監測系統(TPMS)市場在多個細分領域的持續成長奠定了基礎。

全球汽車輪胎壓力監測系統(TPMS)市場趨勢及洞察

根據新的汽車安全法規,胎壓監測系統(TPMS)的安裝現已成為強制性要求。

法規的適用範圍已不再局限於乘用車。歐盟通用安全法規(將於2024年7月生效)將強制要求擴展至卡車、巴士和拖車。美國相應的法規FMVSS 138涵蓋所有重量低於10,000磅的輕型車輛,每輛車的安裝成本在48.44美元至69.89美元之間。韓國的早期應用以及印度的框架草案為新興市場提供了藍圖,確保汽車輪胎壓力監測系統(TPMS)市場在中期內保持監管需求。先前應用較為緩慢的商用車也在快速更新換代,推動了替換需求,並促進了感測器生產的規模經濟。

加強與ADAS和聯網汽車遠端資訊處理平台的整合

將胎壓監測系統 (TPMS) 的直接數據與車輛穩定性控制、自動煞車和雲端分析結合,可提升整體安全性能。 Melexis 為汽車製造商推出了業界首款支援藍牙功能的 TPMS,支援無線軟體更新,並可與行動應用程式無縫整合。在電動車領域,TPMS 數據是高級駕駛輔助系統 (ADAS) 的重要組成部分,因為最佳化的胎壓可以延長電池續航里程並減少能量回收煞車波動。隨著 2025 年車型強製配備自動緊急煞車系統,輪胎狀況預計將成為決策演算法中更關鍵的輸入參數。

入門級產品中感測器和校準高成本

對於價格敏感的A級轎車和通勤自行車而言,12-15美元的額外硬體成本加上經銷商的校準費用阻礙了其全面普及。大陸集團的多重通訊協定可編程感測器雖然減少了維修廠的庫存單位數量,但獨立維修人員仍需要掃描工具和培訓,以避免保固問題。電池續航力的限制也進一步阻礙了預算有限的車主採用這項技術,因為他們覺得更換燈泡很麻煩。

細分市場分析

到2025年,直接式架構將佔據汽車輪胎壓力監測系統(TPMS)市場62.35%的佔有率,預計到2031年將以8.01%的複合年成長率成長,這主要得益於其能夠提供符合聯合國R141精度標準的即時壓力和溫度數據。間接式解決方案利用ABS車輪速度訊號,為車隊改造提供了經濟高效的方案,但無法提供ADAS感測器融合所需的高解析度資料流。隨著汽車製造商向集中式網域控制器轉型,直接式TPMS節點可以輕鬆整合到CAN-FD和汽車乙太網路骨幹網路中,從而簡化診斷和空中韌體更新。

除了硬體之外,軟體分析平台還能將原始輪胎資料轉化為可操作的維護週期、預測性胎面磨損警報和動態負載平衡提示。車隊管理入口網站整合了胎壓監測系統 (TPMS) 控制面板,使維修經理能夠在路邊爆胎之前及早發現微小洩漏。這種預測價值正推動汽車胎壓監測系統 (TPMS) 市場從零件到服務的模式轉型,即使晶片成本下降,也能維持較高的定價。

到2025年,MEMS電容元件將佔據汽車輪胎壓力監測系統(TPMS)51.05%的市場佔有率,這主要得益於前端製造技術的日趨成熟以及原始設備製造商(OEM)的廣泛檢驗。然而,壓電能源採集正迅速普及,預計年複合成長率(CAGR)將達到8.11%,這主要歸功於供應商將鋯鈦酸鉛條整合到TPMS中,該鉛條能夠將汽車胎體形變轉化為有效電荷。佩魯賈大學的概念驗證原型在2MPa的徑向負載下產生了768V的電壓,完全滿足了微控制器的佔空比要求,且無需紐扣電池。省去電池不僅便於報廢回收,延長了維護週期,也使得TPMS能夠應用於無輪轂摩托車等感測器安裝困難的車款上。

同時,諸如NXP FXTH87E之類的雙軸加速感應器可實現車輪自動定位,將輪胎換位時間縮短五分鐘,並支援租賃車隊的現場部署。應變計和光學感測器在小眾高性能車輛領域仍需求旺盛,因為低於0.1 psi的解析度能夠提升賽道性能,但高昂的組件成本限制了其產量。

區域分析

根據FMVSS 138標準,北美地區在2025年仍是汽車輪胎壓力監測系統(TPMS)市場收入的最大區域貢獻者,市佔率高達36.12%,這主要得益於其在輕型車輛中的高搭載率和強大的售後市場供應鏈。各州對網路安全的持續關注正促使供應商轉向符合即將到來的ISO 21434審核要求的加密BLE和UWB協定堆疊。加拿大正朝著美國標準部署方向發展,而墨西哥的OEM工廠則擴大為出口市場預裝TPMS,從而加強了德克薩斯州和新萊昂州物流中心的供應鏈集群。為了提高合規性、安全性和責任評估(CSA)評分,商務傳輸者正在大規模改裝8級牽引車,預計到2025年,該地區的改裝滲透率將達到約40%。

歐洲通用安全法規將要求從2024年中期起,所有新商用車都必須安裝胎壓監測系統(TPMS)。戴姆勒卡車和曼恩等德國汽車製造商已開始將感測器直接整合到重型卡車平台中。同時,英國售後市場經銷商報告稱,改裝廂型車的銷量較去年同期成長超過50%。該地區的脫碳目標正促使車隊營運商將TPMS與低滾動阻力輪胎配合使用,TÜV Nord的實地測試表明,這樣可以節省2-3%的燃油。 UN R141標準在歐洲的統一化進一步降低了型式認證門檻,使得從鹿特丹到華沙的拖車零件編號能夠在跨境車隊中實現標準化。

亞太地區在輪胎胎壓監測系統(TPMS)出貨量方面保持領先地位,預計到2031年將以8.19%的複合年成長率成長,超過全球平均水平。這主要得益於印度、中國和東南亞國家不斷擴大的摩托車和輕型卡車TPMS法規。中國電動車的快速成長迫使對續航里程要求較高的汽車製造商在其A級掀背車標配TPMS,比亞迪每年從當地二級供應商採購數百萬個感測器。韓國的售後感測器市場自2013年初強制實施TPMS以來已日趨成熟,而印度修訂後的汽車工業標準149(AISI)提案提案從2026年起強制M類和N類車輛安裝TPMS。越南摩托車製造商正在為售價低於1500美元的150cc車型標配直通式感測器,這表明在東協地區,由於具備大規模生產的能力,TPMS成本有快速降低的潛力。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 根據新的汽車安全法規,胎壓監測系統(TPMS)的安裝現已成為強制性要求。

- 加強與ADAS和聯網汽車遠端資訊處理平台的整合

- 低成本MEMS感測器在摩托車領域的普及

- 邁向智慧輪胎健康分析生態系統

- 電氣化帶來的重量增加和續航里程問題

- 保險公司利用遠端資訊處理技術激勵輪胎壓力合規性

- 市場限制

- 入門級感測器校準高成本

- 售後市場安裝的複雜性與維修挑戰

- 無線胎壓監測系統的網路安全漏洞

- 無氣輪胎和防爆輪胎技術的出現

- 價值/供應鏈分析

- 監管環境

- 技術展望

- ポーターの五力分析

- 供應商的議價能力

- 買方和消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模及成長預測(金額)

- 依系統類型

- 直接的

- 間接

- 混合

- センサー技術別

- MEMS静電容量式

- 應變計

- 壓電

- 其他(光學、表面聲波等)

- 透過安裝方法

- 閥桿(卡入式/夾緊式)

- バンド/リムマウント式

- 組み込みタイヤモジュール

- 按頻段

- 315 MHz

- 433 MHz

- 2.4 GHz 以上頻段及超寬頻

- 按車輛類型

- 搭乘用車

- 商用車輛

- 摩托車

- 按銷售管道

- 原廠配套

- 售後改裝

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競合情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Continental AG

- Sensata Technologies/Schrader

- Pacific Industrial Co. Ltd.

- Huf Hulsbeck & Furst

- DENSO Corporation

- ZF Friedrichshafen AG(incl. TRW)

- Valeo SA

- ALLIGATOR Ventilfabrik GmbH

- Alps Alpine Co. Ltd.

- Delphi/Aptiv plc

- Continental-Vitesco JV

- PressurePro Enterprises Inc.

- Steelmate Co. Ltd.

- Orange Electronic Co. Ltd.

- Bartec USA LLC

第7章 市場機會與未來展望

The Automotive TPMS market is expected to grow from USD 7.12 billion in 2025 to USD 7.69 billion in 2026 and is forecast to reach USD 11.31 billion by 2031 at 8.02% CAGR over 2026-2031.

The expansion stems from tightly enforced safety rules, the shift toward electrified powertrains, and deeper integration of tire data into advanced driver-assistance and connected-car stacks. Real-time tire health analytics are replacing legacy pressure-only alerts, allowing automakers to align predictive maintenance with over-the-air software capabilities while protecting driving range in weight-sensitive electric models. Consolidation of sensor, gateway, and cloud platforms is also lowering system costs, accelerating adoption in two-wheelers and commercial fleets. In parallel, innovation in piezoelectric energy harvesting and secure 2.4 GHz connectivity is redefining how sensors power themselves and how data move between tires, gateways, and the cloud, positioning the Automotive TPMS market for resilient multi-segment growth.

Global Automotive TPMS Market Trends and Insights

Mandated TPMS Fitment In New-Vehicle Safety Regulations

Regulatory expansion is widening beyond passenger cars into trucks, buses, and trailers now mandated by the EU's General Safety Regulation from July 2024. Comparable rules in the United States under FMVSS 138 keep all light vehicles under 10,000 lb within scope and have demonstrated fitment costs of USD 48.44-69.89 per unit. Early adoption in South Korea and draft frameworks in India offer blueprints for emerging markets, ensuring the Automotive TPMS market sustains regulatory pull into the medium term. Commercial fleets that previously lagged adoption are rapidly upgrading, swelling replacement volumes and driving economies of scale in sensor production.

Rising Integration With ADAS & Connected-Car Telematics Platforms

Merging direct TPMS data with vehicle stability, automated braking, and cloud analytics amplifies overall safety value. Melexis launched the first Bluetooth-enabled OEM TPMS, unlocking over-the-air software support and frictionless pairing to mobile apps. For electric vehicles, optimized tire pressure elevates battery range and mitigates regenerative-braking variability, making TPMS data indispensable within the ADAS stack. Upcoming mandates for automatic emergency braking in 2025 vehicles further embed tire status as a critical input to decision algorithms.

High Sensor & Calibration Cost In Entry-Level Segments

In price-sensitive A-segment cars and commuter bikes, the extra USD 12-15 hardware cost plus dealer calibration fees deter full compliance. Although Continental's multi-protocol programmable sensor trims SKU counts for garages, independent repairers still require scan tools and training to avoid warranty misfires. Battery life constraints further discourage low-budget owners who view valve dismounting labor as prohibitive.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation Of Low-Cost Mems Sensors For Two-Wheelers

- Shift Toward Smart-Tire Health-Analytics Ecosystems

- Wireless TPMS Cybersecurity Vulnerabilities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Direct architectures held a 62.35% Automotive TPMS market share in 2025 and are projected to log an 8.01% CAGR through 2031, underpinned by real-time pressure and temperature delivery that meets UN R141 accuracy thresholds. Indirect solutions remain a cost hedge in fleet retrofits by piggybacking ABS wheel-speed signals but cannot furnish the high-granularity data streams required for ADAS sensor fusion. As automakers transition to centralized domain controllers, direct TPMS nodes slot neatly onto CAN-FD or Automotive Ethernet backbones, streamlining diagnostics and over-the-air firmware updates.

Parallel to hardware, software analytics platforms convert raw tire data into actionable maintenance intervals, predictive tread-wear alerts, and dynamic load balancing cues. Fleet management portals integrate TPMS dashboards, giving maintenance managers early insight into slow leaks before roadside blowouts. Such predictive value elevates the Automotive TPMS market from component supply to recurring service models, supporting premium pricing even as silicon costs decline.

MEMS capacitive elements captured 51.05% of Automotive TPMS market share in 2025 due to mature front-end fabrication and wide OEM validation. However, piezoelectric harvesters are rapidly gaining traction with an 8.11% CAGR outlook as suppliers integrate lead-zirconate-titanate strips that convert carcass deflection into usable charge. Proof-of-concept prototypes from the University of Perugia generated 768 V under 2 MPa radial load, adequate for microcontroller duty cycles without coin-cell batteries. Eliminating batteries eases end-of-life recycling, lengthens maintenance intervals, and opens TPMS deployment on hub-less two-wheelers where sensor access is tight.

Meanwhile, dual-axis accelerometers such as NXP FXTH87E enable automatic wheel localization, cutting 5 minutes from tire-rotation service times and underpinning field adoption across rental fleets. Strain-gauge and optical sensors continue filling niche performance cars where sub-0.1 psi resolution adds track-day value, but their higher BOM keeps volume modest.

The Automotive TPMS Market Report is Segmented by System Type (Direct, Indirect, and Hybrid), Sensor Technology (MEMS Capacitive, Strain-Gauge, and More), Fitting Method (Valve-Stem, Band/Rim-Mounted, and Embedded-Tire Module), Frequency Band (315 MHz and More), Vehicle Type (Passenger Cars and More), Sales Channel (OEM Factory-Fit and Aftermarket Retrofit), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America, anchored by FMVSS (Federal Motor Vehicle Safety Standards) 138, remained the largest regional contributor to Automotive TPMS market revenue in 2025 with 36.12% market share, supported by light-vehicle installation rates and robust aftermarket supply chains. Ongoing emphasis on cybersecurity at the state level is steering suppliers toward encrypted BLE and UWB stacks that can satisfy upcoming ISO 21434 audits. Canadian adoption tracks U.S. standards, while Mexican OEM plants increasingly pre-install TPMS to serve export markets, reinforcing supply-chain clustering at Texas and Nuevo Leon logistics hubs. Commercial carriers pursuing Compliance, Safety, Accountability score improvements are bulk-retrofitting Class 8 tractors, lifting the regional retrofit penetration to almost two-fifths in 2025.

The General Safety Regulation in Europe mandated TPMS on all new commercial vehicles from mid-2024. German OEMs such as Daimler Truck and MAN have already embedded direct sensors on heavy-duty platforms. At the same time, British aftermarket distributors report more than half-year-on-year growth in van retrofit sales. The region's decarbonization targets encourage fleets to pair TPMS with low-rolling-resistance tires, capturing 2-3% fuel savings validated by TUV Nord field testing. Pan-European UN R141 harmonization further lowers homologation friction, allowing cross-border fleets to standardize part numbers for trailers operating from Rotterdam to Warsaw.

Asia-Pacific leads absolute shipment volume and is forecast to outpace global averages to 2031 with 8.19% CAGR as India, China, and Southeast Asian nations legislate broader two-wheeler and light-truck coverage. China's electric-vehicle surge is compelling battery-range-sensitive automakers to standardize TPMS across A-segment hatchbacks, with BYD sourcing millions of sensor annually from local tier-twos. South Korea's early 2013 mandate offers a mature aftermarket for replacement sensors, while India's Automotive Industry Standard 149 revision proposes mandatory TPMS on M and N categories from 2026. Motorcycle OEMs in Vietnam already bundle direct sensors on 150 cc models priced under USD 1,500, underscoring the rapid cost deflation achievable in high-volume ASEAN ecosystems.

- Continental AG

- Sensata Technologies / Schrader

- Pacific Industrial Co. Ltd.

- Huf Hulsbeck & Furst

- DENSO Corporation

- ZF Friedrichshafen AG (incl. TRW)

- Valeo SA

- ALLIGATOR Ventilfabrik GmbH

- Alps Alpine Co. Ltd.

- Delphi / Aptiv plc

- Continental - Vitesco JV

- PressurePro Enterprises Inc.

- Steelmate Co. Ltd.

- Orange Electronic Co. Ltd.

- Bartec USA LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandated TPMS Fitment In New-Vehicle Safety Regulations

- 4.2.2 Rising Integration With ADAS & Connected-Car Telematics Platforms

- 4.2.3 Proliferation Of Low-Cost Mems Sensors For Two-Wheelers

- 4.2.4 Shift Toward Smart-Tire Health-Analytics Ecosystems

- 4.2.5 Electrification Increasing Weight-Sensitive Range Anxiety

- 4.2.6 Insurance-Telematics Incentives For Tire-Pressure Compliance

- 4.3 Market Restraints

- 4.3.1 High Sensor & Calibration Cost In Entry-Level Segments

- 4.3.2 Aftermarket Installation Complexity & Maintenance Issues

- 4.3.3 Wireless TPMS Cybersecurity Vulnerabilities

- 4.3.4 Advent Of Airless & Run-Flat Tire Technologies

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By System Type

- 5.1.1 Direct

- 5.1.2 Indirect

- 5.1.3 Hybrid

- 5.2 By Sensor Technology

- 5.2.1 MEMS Capacitive

- 5.2.2 Strain-Gauge

- 5.2.3 Piezoelectric

- 5.2.4 Others (Optical, SAW, etc.)

- 5.3 By Fitting Method

- 5.3.1 Valve-Stem (Snap-In & Clamp-In)

- 5.3.2 Band / Rim-Mounted

- 5.3.3 Embedded-Tire Module

- 5.4 By Frequency Band

- 5.4.1 315 MHz

- 5.4.2 433 MHz

- 5.4.3 More than or equal to 2.4 GHz & UWB

- 5.5 By Vehicle Type

- 5.5.1 Passenger Cars

- 5.5.2 Commercial Vehicle

- 5.5.3 Two-Wheelers

- 5.6 By Sales Channel

- 5.6.1 OEM Factory-Fit

- 5.6.2 Aftermarket Retrofit

- 5.7 Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South Korea

- 5.7.4.5 Australia

- 5.7.4.6 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 Turkey

- 5.7.5.4 Egypt

- 5.7.5.5 South Africa

- 5.7.5.6 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Continental AG

- 6.4.2 Sensata Technologies / Schrader

- 6.4.3 Pacific Industrial Co. Ltd.

- 6.4.4 Huf Hulsbeck & Furst

- 6.4.5 DENSO Corporation

- 6.4.6 ZF Friedrichshafen AG (incl. TRW)

- 6.4.7 Valeo SA

- 6.4.8 ALLIGATOR Ventilfabrik GmbH

- 6.4.9 Alps Alpine Co. Ltd.

- 6.4.10 Delphi / Aptiv plc

- 6.4.11 Continental - Vitesco JV

- 6.4.12 PressurePro Enterprises Inc.

- 6.4.13 Steelmate Co. Ltd.

- 6.4.14 Orange Electronic Co. Ltd.

- 6.4.15 Bartec USA LLC

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

2026年全球智慧拖車輪胎壓力監測系統(TMPS)和遠端資訊處理市場報告

2026年全球智慧拖車輪胎壓力監測系統(TMPS)和遠端資訊處理市場報告 輪胎壓力監測系統市場:2026年至2032年全球市場預測(依產品類型、組件、銷售管道、最終用戶及車輛類型分類)

輪胎壓力監測系統市場:2026年至2032年全球市場預測(依產品類型、組件、銷售管道、最終用戶及車輛類型分類) 輪胎壓力監測系統市場報告:按類型、技術、車輛類型、銷售管道和地區分類(2026-2034 年)2026年全球先進胎壓監測系統市場報告2026年全球汽車輪胎壓力監測系統市場報告2026年全球高壓熔斷器監測模組市場報告輪胎壓力監測系統電池市場:按車輛類型、電池化學成分、應用和銷售管道- 全球預測 2026-2032

輪胎壓力監測系統市場報告:按類型、技術、車輛類型、銷售管道和地區分類(2026-2034 年)2026年全球先進胎壓監測系統市場報告2026年全球汽車輪胎壓力監測系統市場報告2026年全球高壓熔斷器監測模組市場報告輪胎壓力監測系統電池市場:按車輛類型、電池化學成分、應用和銷售管道- 全球預測 2026-2032 全球輪胎壓力監測系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)汽車胎壓監測系統(TPMS)服務套件市場按產品類型、車輛類型、分銷管道和最終用戶分類-全球預測,2026-2032年

全球輪胎壓力監測系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)汽車胎壓監測系統(TPMS)服務套件市場按產品類型、車輛類型、分銷管道和最終用戶分類-全球預測,2026-2032年 輪胎壓力監測系統市場 - 全球產業規模、佔有率、趨勢、機會與預測:按類型、銷售管道類型、車輛類型、地區和競爭格局分類,2021-2031年

輪胎壓力監測系統市場 - 全球產業規模、佔有率、趨勢、機會與預測:按類型、銷售管道類型、車輛類型、地區和競爭格局分類,2021-2031年