|

市場調查報告書

商品編碼

1939123

鈦合金:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Titanium Alloy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

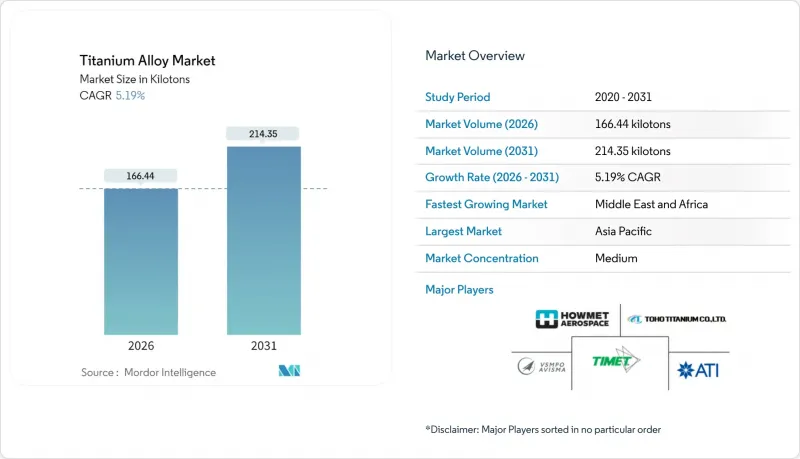

預計鈦合金市場將從 2025 年的 158.23 千噸成長到 2026 年的 166.44 千噸,到 2031 年將達到 214.35 千噸,2026 年至 2031 年的複合年成長率為 5.19%。

波音和空中巴士持續的訂單積壓、國防採購週期的復甦以及醫療植入基本客群的不斷成長支撐了市場需求。鈦合金的持續成長依賴於其優異的性能,例如高強度重量比、耐腐蝕性和生物相容性,這些優勢彌補了其在關鍵應用領域仍然較高的製造成本。生產商正透過氫輔助還原和積層製造等技術提高熔煉能力,以緩解供應瓶頸;同時,客戶也正在實現採購多元化,以降低地緣政治風險。節省成本的創新技術和日益嚴格的燃油效率飛機法規進一步鞏固了鈦合金市場的成長動能。

全球鈦合金市場趨勢與洞察

航太和國防領域對飛機的需求不斷成長

鈦合金已獲得超過15,000架民航機的訂單,在結構零件、起落架和引擎零件領域佔據穩固地位,因為減輕重量可直接轉化為燃油節省。 ATI公司2025年第一季66%的收入來自航太和國防領域,並與空中巴士公司簽署了一份為期五年、價值10億美元的供應合約。由於引擎需求激增,豪邁航空航太公司2024年第三季的商用航太銷售額成長了17%。鈦合金目前佔噴射引擎重量的15%至25%,國防項目因其隱身性和耐久性而指定使用這種合金。擺脫對俄羅斯原料的依賴,推動了與日本和中東供應商建立新的合作關係,進一步鞏固了鈦合金市場的生產格局。

軍事用陸上車輛輕量化計劃

為了在不降低防護性能的前提下提升航程和負載容量,國防負責人正在加速推進裝甲、傳動系統和懸吊部件從鋼材向鈦合金的轉換。美國國防部授予IperionX公司價值4710萬美元的契約,凸顯了美國為確保安全、低成本的鈦合金生產能力而做出的國家努力。北約統一的材料規格標準正在推動跨境需求,而實戰數據顯示,用鈦合金零件取代鋼材零件可節省15%至20%的燃料。先進的製造技術正在減少零件數量,降低部署車輛的維護負擔,從而推動鈦合金市場的長期成長。

高成本且冶金製程複雜

傳統的克羅爾法每噸鈦的能耗為11-13兆瓦時,使得鈦的價格比鋁高三到四倍,比鋼高出10-15倍。反應冶金需要惰性氣氛和專用切削液,這限制了下游加工製程的生產效率。氫輔助還原製程雖然可以降低溫度,但仍處於商業化前期階段。東京大學利用釔反應去除氧的技術具有降低成本的潛力,但實現工業規模的實用化還需要數年時間。在新製程成熟之前,高昂的轉換成本限制了鈦合金市場的發展潛力。

細分市場分析

預計到2031年,BETA合金的複合年成長率將達到6.02%,而α-BETA合金在2025年佔據了鈦合金市場佔有率的51.12%。 Ti-5553合金具有優異的鑄造性能,並具有高強度重量比,這對於機翼穿透件和起落架結構至關重要。對含鋯和鉿的高熵金屬間化合物的研究表明,其在8%塑性應變下的屈服強度可達1.5 GPa,從而拓展了高超音速應用領域的選擇。

積層製造技術的持續應用實現了近淨成形生產,可將採購到交付的比率降低高達 60%,並為渦輪葉片複雜的冷卻通道結構提供了支援。受粉末霧化技術與關鍵飛機設備認證測試之間協同效應的推動,預計到本十年末,BETA 鈦合金的市場規模將佔總市場規模的約 25%。同時,人們對適用於 500°C 以上高溫環境的 α 和近 α 合金的興趣也持續推動燃氣渦輪機和航太推進系統的需求。隨著製造商對真空電弧重熔參數的標準化,合金成分變得更加穩定,從而提高了主要航太和國防製造商的可靠性。

本鈦合金報告依微觀結構(α相及近α相、α-BETA相、BETA相)、終端用戶產業(航太、汽車及造船、化學、發電及海水淡化、醫療及人工植牙、其他終端用戶產業)及地區(亞太地區、北美地區、歐洲地區、南美地區、中東及非洲地區)進行細分。市場預測以千噸為單位。

區域分析

到2025年,亞太地區將佔鈦合金市場41.02%的佔有率,主要得益於中國60%的全球鈦合金產量。然而,該地區航太認證的延遲阻礙了其即時參與高價值噴射機計畫。印度正與印度斯坦航空有限公司(HAL)和國防研究與發展組織(DRDO)合作,擴大其國內海綿鈦的生產能力。同時,澳洲礦業公司正向下游拓展合金製造業務,力求在價值鏈上游獲得利潤。這些努力將推動鈦合金總產量穩定成長,但品質方面的挑戰依然存在。

中東和非洲地區正以5.85%的複合年成長率快速成長,並受惠於沙烏地阿拉伯460億美元的礦業策略。該戰略旨在2030年將礦業佔GDP的比重提升至750億美元,並使沙烏地阿拉伯成為鈦的中性供應國。儘管北美海綿鈦產量極低,但消費量仍居高不下。北卡羅來納州坎伯蘭縣已獲得一項價值8.67億美元的投資,用於重建國內海綿鈦產能,該產能將採用氫輔助還原法,預計運作運轉後年產量可達1萬噸。在加拿大,魁北克省一家水力發電的鈦鐵礦開採企業正在探索垂直整合到低碳海綿鈦的途徑。

在大西洋彼岸的歐洲,原始設備製造商(OEM)正努力在遵守制裁規定和維持生產之間取得平衡,並正在探討與哈薩克和日本供應商建立合資企業的可能性。歐盟關鍵材料法加快了挪威和西班牙海綿鈦計劃的核准流程。儘管南美洲仍然主要是原礦出口地區,但巴西國有開發銀行已表示有興趣為現有鈦鐵礦附近的下游合金工廠提供聯合融資。總體而言,不斷變化的供應基礎正在持續重塑鈦合金市場格局。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 航太和國防領域對飛機的需求不斷成長

- 軍事用陸上車輛輕量化計劃

- 擴大醫療和人工植牙手術

- 利用積層製造技術開發新材料等級

- 新興氫能經濟中的熱交換器需求

- 市場限制

- 高成本且冶金製程複雜

- 全球海綿生產能力受限

- 對俄羅斯原物料的地緣政治依賴

- 價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 透過微觀結構

- Alpha 和 Near Alpha

- 阿爾法貝塔

- 測試版

- 按最終用戶行業分類

- 航太

- 汽車和造船

- 化學處理

- 電力/海水淡化

- 醫療和牙科植入

- 其他終端用戶產業(例如,石油和天然氣)

- 地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率 (%)**/排名分析

- 公司簡介

- ATI

- Alleima

- AMG

- BAOTI Group Co.,Ltd.

- Corporation VSMPO-AVISMA

- CRS Holdings, LLC

- Daido Steel Co., Ltd.

- Hermith GmbH

- Howmet Aerospace

- KOBE STEEL, LTD.

- OSAKA Titanium Technologies Co.,Ltd.

- Perryman Company

- PJSC VSMPO-AVISMA Corporation

- TIMET(Precision Castparts Corp.)

- Toho Titanium Co., Ltd.

- Weber Metals(OTTO FUCHS Kommanditgesellschaft)

- Western Superconducting Technologies Co., Ltd

第7章 市場機會與未來展望

The Titanium Alloy Market is expected to grow from 158.23 kilotons in 2025 to 166.44 kilotons in 2026 and is forecast to reach 214.35 kilotons by 2031 at 5.19% CAGR over 2026-2031.

Consistent order backlogs at Boeing and Airbus, revived defense procurement cycles, and a widening medical-implant customer base anchor demand. Sustained performance hinges on titanium's high strength-to-weight ratio, corrosion resistance, and biocompatibility, traits that continue to outweigh its higher production cost in critical applications. Producers are adding melt capacity, often through hydrogen-assisted reduction or additive manufacturing, to alleviate supply bottlenecks, while customers diversify sourcing to mitigate geopolitical risk. Cost-down innovation and regulatory push for fuel-efficient aircraft further reinforce the growth narrative of the titanium alloy market.

Global Titanium Alloy Market Trends and Insights

Growing Aerospace and Defense Airframe Demand

Orders exceeding 15,000 commercial aircraft place titanium squarely in structural, landing-gear, and engine components, where weight reduction translates into fuel savings. ATI drew 66% of Q1 2025 revenue from aerospace and defense and locked in a five-year USD 1 billion supply pact with Airbus. Howmet Aerospace recorded 17% commercial-aerospace sales growth in Q3 2024 on surging engine demand. Titanium intensity now reaches 15-25% of a jet engine's weight, while defense programs specify the alloy for stealth and durability. Diversification away from Russian feedstock is driving new partnerships with Japanese and Middle Eastern suppliers, reinforcing the titanium alloy market's production realignment.

Military Ground-Vehicle Light-Weighting Programs

Defense planners increasingly swap steel for titanium in armor, drivetrains, and suspensions to boost range and payload without sacrificing protection. The U.S. Department of Defense's USD 47.1 million award to IperionX underscores a national push for secure, low-cost titanium capacity. NATO standards that harmonize material specifications amplify cross-border demand, and field data show 15-20% fuel savings when titanium components replace steel. Advanced manufacturing shortens part lists, easing maintenance burden for deployed vehicle fleets and fueling long-run momentum in the titanium alloy market.

High Production Cost and Complex Metallurgy

The legacy Kroll route burns 11-13 MWh per ton, making titanium 3-4 times pricier than aluminum and 10-15 times pricier than steel. Reactive metallurgy demands inert atmospheres and specialized cutting fluids, hampering productivity in downstream machining. Hydrogen-assisted reduction pathways promise lower temperatures but remain pre-commercial. University of Tokyo techniques for oxygen removal via yttrium reactions offer potential cost savings, yet industrial scaling is several years. Until new processes mature, elevated conversion costs cap the full potential of the titanium alloy market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Medical and Dental Implant Procedures

- Additive Manufacturing Unlocking Novel Grades

- Geopolitical Dependence on Russian Feedstock

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Beta alloys are projected to register a 6.02% CAGR through 2031, while Alpha-Beta grades retained 51.12% of the titanium alloy market share in 2025. Ti-5553 demonstrates superior castability, delivering high strength-to-weight ratios vital for wing-carry-throughs and landing-gear structures. Research into high-entropy intermetallics incorporating zirconium and hafnium achieves yield strengths of 1.5 GPa with 8% plastic strain, expanding options for hypersonic applications.

Ongoing additive-manufacturing deployments enable near-net-shape production, slashing buy-to-fly ratios by up to 60% and supporting intricate cooling-channel architectures in turbine blades. Beta alloys' titanium alloy market size is on track to close the decade at roughly 25% of overall volume, supported by synergistic gains in powder-atomization capacity and qualification tests for critical flight hardware. Parallel interest in Alpha and Near-Alpha alloys for temperatures above 500 °C preserves demand in gas turbines and space-propulsion contexts. As producers standardize vacuum-arc-remelting parameters, alloy chemistries stabilize, improving confidence among aerospace and defense primes.

The Titanium Alloy Report is Segmented by Microstructure (Alpha and Near-Alpha, Alpha-Beta, and Beta), End-User Industry (Aerospace, Automotive and Shipbuilding, Chemical Processing, Power and Desalination, Medical and Dental Implants, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Kilotons).

Geography Analysis

Asia-Pacific commanded 41.02% of the titanium alloy market in 2025, anchored by China's 60% share of global metal output. However, the region's aerospace certification gap curtails immediate penetration into high-value jet programs. India collaborates with HAL and DRDO on indigenous sponge capacity, while Australian miners explore downstream alloying to capture margin farther along the value chain. These initiatives collectively support robust volume gains, although quality hurdles remain.

The Middle East and Africa region, expanding at a 5.85% CAGR, benefits from Saudi Arabia's USD 46 billion mining strategy, which aims to lift mining GDP share to 75 billion by 2030 and position the kingdom as a neutral titanium supplier. North American consumption stays high despite minimal sponge output. Cumberland County, North Carolina, secured a USD 867 million plant to rebuild domestic capacity with hydrogen-assisted reduction that could supply 10,000 tons annually once fully operational. In Canada, Quebec's hydro-powered ilmenite operations explore vertically integrating into low-carbon sponge.

Across the Atlantic, European OEMs juggle sanction compliance and production continuity, prompting joint-venture discussions with Kazakh and Japanese suppliers; the EU's Critical Raw Materials Act expedites permitting for sponge projects in Norway and Spain. South America remains largely a raw-ore exporter, but Brazil's state development bank signals interest in co-financing downstream alloy plants near existing ilmenite mines. Overall, shifting supply footprints continue to reshape the titanium alloy market.

- ATI

- Alleima

- AMG

- BAOTI Group Co.,Ltd.

- Corporation VSMPO-AVISMA

- CRS Holdings, LLC

- Daido Steel Co., Ltd.

- Hermith GmbH

- Howmet Aerospace

- KOBE STEEL, LTD.

- OSAKA Titanium Technologies Co.,Ltd.

- Perryman Company

- PJSC VSMPO-AVISMA Corporation

- TIMET (Precision Castparts Corp.)

- Toho Titanium Co., Ltd.

- Weber Metals (OTTO FUCHS Kommanditgesellschaft)

- Western Superconducting Technologies Co., Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Aerospace and Defense Airframe Demand

- 4.2.2 Military Ground-Vehicle Light-Weighting Programs

- 4.2.3 Expansion of Medical and Dental Implant Procedures

- 4.2.4 Additive Manufacturing Unlocking Novel Grades

- 4.2.5 Heat-Exchanger Demand in Emerging Hydrogen Economy

- 4.3 Market Restraints

- 4.3.1 High Production Cost and Complex Metallurgy

- 4.3.2 Limited Global Sponge Capacity

- 4.3.3 Geopolitical Dependence on Russian Feedstock

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Microstructure

- 5.1.1 Alpha and Near-Alpha

- 5.1.2 Alpha-Beta

- 5.1.3 Beta

- 5.2 By End-User Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive and Shipbuilding

- 5.2.3 Chemical Processing

- 5.2.4 Power and Desalination

- 5.2.5 Medical and Dental Implants

- 5.2.6 Other End-user Industries (Oil and Gas, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)**/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ATI

- 6.4.2 Alleima

- 6.4.3 AMG

- 6.4.4 BAOTI Group Co.,Ltd.

- 6.4.5 Corporation VSMPO-AVISMA

- 6.4.6 CRS Holdings, LLC

- 6.4.7 Daido Steel Co., Ltd.

- 6.4.8 Hermith GmbH

- 6.4.9 Howmet Aerospace

- 6.4.10 KOBE STEEL, LTD.

- 6.4.11 OSAKA Titanium Technologies Co.,Ltd.

- 6.4.12 Perryman Company

- 6.4.13 PJSC VSMPO-AVISMA Corporation

- 6.4.14 TIMET (Precision Castparts Corp.)

- 6.4.15 Toho Titanium Co., Ltd.

- 6.4.16 Weber Metals (OTTO FUCHS Kommanditgesellschaft)

- 6.4.17 Western Superconducting Technologies Co., Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

全球鈦合金市場(至2035年):產業趨勢與預測

全球鈦合金市場(至2035年):產業趨勢與預測 工業鈦合金市場:依等級、形狀、合金類型、最終用途和應用分類-2026年至2032年全球預測

工業鈦合金市場:依等級、形狀、合金類型、最終用途和應用分類-2026年至2032年全球預測 鈦合金市場規模、佔有率、趨勢和預測:按微觀結構、終端應用產業和地區分類,2026-2034年

鈦合金市場規模、佔有率、趨勢和預測:按微觀結構、終端應用產業和地區分類,2026-2034年 Ti-6Al-4V鈦合金市場規模、佔有率和成長分析(按形態、等級、應用和地區分類)-產業預測(2026-2033年)

Ti-6Al-4V鈦合金市場規模、佔有率和成長分析(按形態、等級、應用和地區分類)-產業預測(2026-2033年) Ti-6Al-4V鈦合金的全球市場全球鈦合金市場

Ti-6Al-4V鈦合金的全球市場全球鈦合金市場 鈦合金市場 - 預測 2025-2030

鈦合金市場 - 預測 2025-2030 鈦合金配件市場報告:趨勢、預測與競爭分析(至2031年)鈦合金市場報告:趨勢、預測與競爭分析(至2031年)

鈦合金配件市場報告:趨勢、預測與競爭分析(至2031年)鈦合金市場報告:趨勢、預測與競爭分析(至2031年) 鈦合金全球市場:產業分析、規模、佔有率、成長、趨勢、預測(2024-2031)

鈦合金全球市場:產業分析、規模、佔有率、成長、趨勢、預測(2024-2031)