|

市場調查報告書

商品編碼

1939100

亞太地區醫藥包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Asia Pacific Pharmaceutical Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

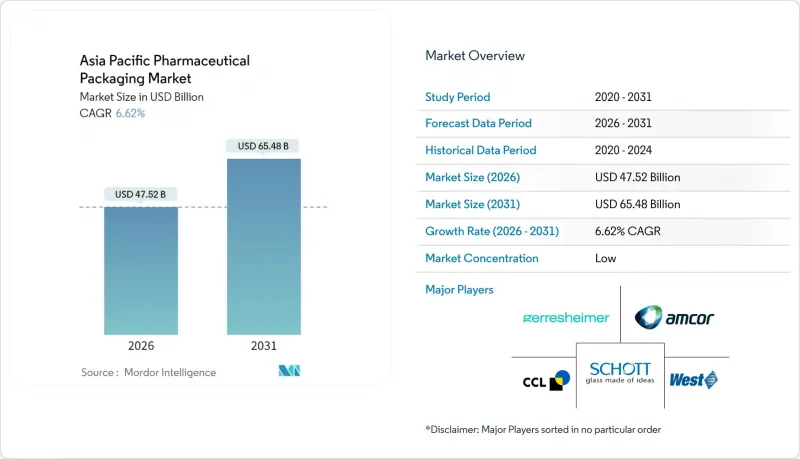

亞太地區藥品包裝市場在 2025 年的價值為 445.7 億美元,預計到 2031 年將達到 654.8 億美元,而 2026 年為 475.2 億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 6.62%。

這一穩步成長反映了該地區從低成本生產中心向高價值生物製藥、複雜灌裝密封服務和序列化包裝生產線的全球中心轉型。隨著中國實施電子代碼序列化,以及印度擴大藥品認證和檢驗應用(DAVA)的覆蓋範圍,需求不斷成長,推動供應鏈各環節向可追溯、防篡改包裝形式轉變。材料創新也在加速發展,加工商正從一般塑膠轉向能夠承受細胞和基因療法低溫物流的環烯烴和生質塑膠。同時,製藥品牌所有者正在採用單劑量包裝和整合數位標識符,亞太地區藥品包裝市場正處於以永續性和合規性為重點的多年投資週期中。

亞太地區醫藥包裝市場趨勢與洞察

不斷成長的生物製藥產品線需要可靠的初級包裝

2024年,生物製劑佔肖特製藥生物製藥銷售額的34%,推動總銷售額達10.5億美元。這標誌著其包裝結構向預滅菌硼硼矽酸玻璃容器轉變,從而最大限度地降低污染風險。 Stevanato集團也呈現類似的趨勢,2024會計年度銷售額達到12.1億美元,其中38%來自即用型管瓶和藥筒。 2024年9月,Schotta與Gerresheimer共同創立了「即用型包裝聯盟」(Alliance for RTU),旨在推動亞太地區藥品包裝市場即用型容器規格的標準化。如今,契約製造生產商在競標階段就明確要求使用無熱原管瓶和預組裝瓶蓋,從而縮短疫苗和單株抗體上市的驗證時間。隨著生物製藥產品線的成熟,對高價值容器的需求正在超越頂級製造地,這促使區域玻璃製造商對熔爐進行改造,以實現更嚴格的尺寸公差和可見的無顆粒生產。

將灌裝和表面處理工程外包給亞洲的趨勢正在推動合約包裝量的成長。

Lotus Pharmaceutical 獲得 FDA、EMA 和 PMDA 認證的網路在 2025 會計年度上半年實現了創紀錄的收入,凸顯了印度吸收從西方工廠轉移過來的複雜灌裝和表面處理工程的能力。新加坡和韓國在生物製藥專業技術方面競爭,而中國經濟高效的滅菌設施則縮短了季節性疫苗的生產前置作業時間。因此,亞太地區的藥品包裝市場對嵌套注射器、雙腔藥筒和序列化二級包裝盒的需求量正在增加。技術轉移協議擴大將包裝合格測試與藥品生產相結合,使本地加工商從單純的商品供應商轉變為解決方案合作夥伴。這種趨勢正在加速符合 ISO 標準的無塵室基礎設施的普及,並對標籤、測試和聚合服務產生連鎖反應。

樹脂和氧化鋁價格的波動對加工商的利潤率帶來壓力。

Winpack發布的2024年公佈財報顯示,尼龍和鋁箔價格較上月下降9%至13%。這標誌著價格從先前的飆升中回落,凸顯了包裝材料生產商面臨的商品價格快速波動問題。包裝製造商正將財務資源投入到避險策略和靈活的定價條款中,而規模較小的公司則缺乏足夠的信貸額度來應對價格飆升。庫存控制更加嚴格,如果供應商限制配額,生產線停產的風險也會增加。成本吸收能力的不平衡使一體化跨國公司佔據優勢,導致亞太地區醫藥包裝市場的競爭格局向那些透過談判獲得年度原料合約的大型企業傾斜。

細分市場分析

到2025年,塑膠仍將佔據亞太地區醫藥包裝市場46.78%的主導地位,這主要得益於主要製藥製造群附近成熟的擠出和射出成型能力。然而,該細分市場的中個位數成長率與先進材料8.22%的複合年成長率形成鮮明對比,預示著市場正在向環烯烴、生物基聚合物和特種玻璃轉型,這些材料具有更優異的耐低溫儲存和耐高活性藥物性能。隨著生物製藥研發管線的擴展及Annex 1無塵室標準的加強,環烯烴共聚物可望推動亞太地區醫藥包裝市場規模達到兩位數成長。

三井化學的APEL™環烯烴創新技術已證明其能夠在滿足防潮要求的同時保持與伽馬射線滅菌的兼容性,從而得以廣泛應用於預填充式注射器筒體。玻璃製造商也在對其I型硼矽酸玻璃熔爐維修,以充分利用不斷成長的注射劑填充和封裝市場,同時避免傳統管瓶的分層風險。從永續性的角度來看,薄膜加工商正在試驗PLA-奈米纖維素複合材料,該材料預計將在滿足《藥品法典》規定的可萃取物限量的同時,確保可堆肥性。區域監管機構透過發布指南,優先考慮可回收性和碳足跡揭露,並將環境指標納入材料選擇清單,從而支持這項轉型。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 不斷成長的生物製藥產品線需要可靠的初級包裝

- 灌裝和表面處理工程加速外包至亞洲,推動了合約包裝業務量的成長。

- 政府批量採購計畫傾向於採用成本效益高的泡殼包裝形式。

- 序列化法規(中國的E-Code、印度的Dava)促進了可追溯包裝的實施。

- 低劑量、高活性口服固體製劑(OSD)的激增將推動阻隔性PTP箔片的應用(被低估了)。

- 溫度敏感型細胞和基因療法的成長將創造對耐冷凍保存管瓶的需求(被低估了)。

- 市場限制

- 樹脂和氧化鋁價格的波動對加工商的利潤率帶來壓力。

- 日本和韓國都採取了嚴格的PVC淘汰政策。

- 由於港口堵塞和低溫運輸瓶頸導致出口貨物延誤(未充分報告)

- 區域內藥用級硼矽酸玻璃管供不應求(未充分通報)

- 產業價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 產業夥伴關係與合作

第5章 市場規模與成長預測

- 材料

- 塑膠

- 紙和紙板

- 玻璃

- 鋁箔

- 其他材質(生質塑膠、環狀烯烴)

- 按類型

- 安瓿

- 泡殼包裝

- 塑膠瓶

- 注射器

- 管瓶

- 點滴

- 棒狀包裝

- 小袋和小袋

- 瓶蓋和封裝

- 透過藥物輸送方法

- 口服

- 注射

- 肺

- 經皮/經皮吸收型

- 其他給藥途徑

- 按國家/地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Amcor plc

- Gerresheimer AG

- Schott AG

- West Pharmaceutical Services Inc

- CCL Industries Inc

- NIPRO Corporation

- Wihuri Group

- Klockner Pentaplast Group

- Catalent Pharma Solutions Inc

- Berry Global Group Inc

- SGD Pharma

- AptarGroup Inc

- Stevanato Group

- Huhtamaki Oyj

- Daikyo Seiko Ltd

- Shandong Pharmaceutical Glass Co

- Tekni-Plex Inc

- Alpla Werke

- Chongqing Zhengchuan Glass

- Essel Propack Ltd

第7章 市場機會與未來展望

The Asia Pacific pharmaceutical packaging market was valued at USD 44.57 billion in 2025 and estimated to grow from USD 47.52 billion in 2026 to reach USD 65.48 billion by 2031, at a CAGR of 6.62% during the forecast period (2026-2031).

This steady climb reflects the region's transition from a low-cost production base into a global center for high-value biologics, complex fill-finish services, and serialization-ready packaging lines. Demand intensifies as China enforces e-code serialization and India scales its Drug Authentication and Verification Application, pushing every tier of the supply chain toward traceable, tamper-evident formats. Material innovation also quickens: converters move from commodity plastics toward cyclic olefins and bioplastics that withstand deep-cold logistics for cell-and-gene therapies. In parallel, pharmaceutical brand owners favor single-dose formats and integrated digital identifiers, locking the Asia Pacific pharmaceutical packaging market into a multi-year investment cycle focused on sustainability and compliance.

Asia Pacific Pharmaceutical Packaging Market Trends and Insights

Rising Biologics Pipeline Demanding High-Integrity Primary Packaging

Biologics represented 34% of SCHOTT Pharma's biopharmaceutical revenue in 2024, lifting total sales to USD 1.05 billion and signaling a structural pivot toward pre-sterilized borosilicate formats that minimize contamination risk.Stevanato Group echoed this trend, generating USD 1.21 billion in fiscal 2024 with 38% of revenue from ready-to-use vials and cartridges. The two firms, together with Gerresheimer, formed the Alliance for RTU in September 2024 to standardize ready-to-use container formats across the Asia Pacific pharmaceutical packaging market. Contract manufacturers now specify depyrogenated vials and pre-assembled closures at bid stage, compressing validation timelines for vaccine and monoclonal antibody launches. As biologics pipelines mature, high-value container demand expands beyond top-tier sites, encouraging regional glass makers to retrofit furnaces for tighter dimensional tolerances and visible-particle-free output.

Accelerated Fill-Finish Outsourcing to Asia Driving Contract Packaging Volumes

Lotus Pharmaceutical's FDA-, EMA- and PMDA-certified network earned a record first-half 2025 revenue, reinforcing India's ability to absorb complex fill-finish work relocated from Western plants. Singapore and South Korea compete on biologics expertise, while cost-efficient sterilization suites in China shorten lead times for seasonal vaccine production. The Asia Pacific pharmaceutical packaging market consequently records higher throughput for nested syringes, dual-chamber cartridges, and serialized secondary cartons. Technology transfer contracts increasingly bundle packaging qualification with drug-product manufacture, elevating local converters into solution partners rather than commodity suppliers. This momentum accelerates adoption of ISO -compliant clean-room infrastructure and creates a ripple effect on labelling, inspection, and aggregation services.

Volatile Resin and Alumina Prices Squeezing Converter Margins

Winpak's 2024 earnings call revealed a 9-13% quarter-over-quarter drop in nylon and aluminum foil prices after earlier spikes, underscoring the commodity whiplash confronting converters. Packaging producers devote treasury resources to hedging strategies and flexible pricing clauses, yet smaller firms lack the credit lines to buffer sudden surges. Inventory runs leaner, raising the risk of line stoppages when suppliers ration allocations. Uneven cost absorption places integrated multinationals at an advantage, tilting competitive balance within the Asia Pacific pharmaceutical packaging market toward scale players that negotiate annual raw-material contracts.

Other drivers and restraints analyzed in the detailed report include:

- Government Bulk-Procurement Schemes Favouring Cost-Efficient Blister Formats

- Serialization Regulations Boosting Track-and-Trace Packaging

- Stringent PVC Phase-Out Policies in Japan and South Korea

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastic maintained a commanding 46.78% share of the Asia Pacific pharmaceutical packaging market in 2025 thanks to established extrusion and injection-molding capacity close to major drug-manufacturing clusters. Yet the segment's mid-single-digit growth contrasts with the 8.22% CAGR logged by advanced materials, underscoring a pivot toward cyclic olefins, bio-based polymers, and specialty glass that better withstand cryogenic storage and high-potency drugs. The Asia Pacific pharmaceutical packaging market size attributable to cyclic-olefin copolymers is projected to climb in double digits as biologics pipelines deepen and Annex 1 clean-room standards tighten.

Mitsui Chemicals' APEL(TM) demonstrates how cyclic-olefin innovation satisfies moisture-barrier demands while remaining compatible with gamma sterilization, enabling wider adoption in pre-filled syringe barrels. Glass producers also renovate furnaces for Type I borosilicate, aiming to capture injectable fill-finish growth without the delamination risks of legacy vials. On the sustainability front, film converters experiment with PLA-nanocellulose blends that promise compostability yet meet extractables limits required by pharmacopeias. Regional regulators support this shift by issuing guidance prioritizing recyclability and carbon-footprint disclosure, embedding environmental metrics into material-selection checklists.

The Asia Pacific Pharmaceutical Packaging Market Report is Segmented by Material (Plastic, Paper and Paperboard, Glass, Aluminum Foil, Other Advanced Materials), Type (Ampoules, Blister Packs, Plastic Bottles, Syringes, Vials, IV Fluids, Stick Packs, Pouches and Sachets, Caps and Closures), Drug Delivery Mode (Oral, Injectable, Pulmonary, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amcor plc

- Gerresheimer AG

- Schott AG

- West Pharmaceutical Services Inc

- CCL Industries Inc

- NIPRO Corporation

- Wihuri Group

- Klockner Pentaplast Group

- Catalent Pharma Solutions Inc

- Berry Global Group Inc

- SGD Pharma

- AptarGroup Inc

- Stevanato Group

- Huhtamaki Oyj

- Daikyo Seiko Ltd

- Shandong Pharmaceutical Glass Co

- Tekni-Plex Inc

- Alpla Werke

- Chongqing Zhengchuan Glass

- Essel Propack Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Biologics Pipeline Demanding High-Integrity Primary Packaging

- 4.2.2 Accelerated Fill-Finish Outsourcing to Asia Driving Contract Packaging Volumes

- 4.2.3 Government Bulk-Procurement Schemes Favouring Cost-Efficient Blister Formats

- 4.2.4 Serialization Regulations (China E-Codes, India Dava) Boosting Track-and-Trace Packaging

- 4.2.5 Surge in Low-Dose, High-Potency OSD Drugs Spurring Adoption of High-Barrier PTP Foils (Under-Reported)

- 4.2.6 Growth of Temperature-Sensitive Cell-and-Gene Therapies Creating Demand for Cryo-Compatible Vials (Under-Reported)

- 4.3 Market Restraints

- 4.3.1 Volatile Resin and Alumina Prices Squeezing Converter Margins

- 4.3.2 Stringent PVC Phase-Out Policies In Japan and South Korea

- 4.3.3 Port Congestion and Cold-Chain Bottlenecks Slowing Export Shipments (Under-Reported)

- 4.3.4 Limited Regional Supply of Pharma-Grade Borosilicate Tubing (Under-Reported)

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Supplier

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Industry Partnerships and Collaborations

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Plastic

- 5.1.2 Paper and Paperboard

- 5.1.3 Glass

- 5.1.4 Aluminum Foil

- 5.1.5 Other Materials (Bioplastics, Cyclic Olefins)

- 5.2 By Type

- 5.2.1 Ampoules

- 5.2.2 Blister Packs

- 5.2.3 Plastic Bottles

- 5.2.4 Syringes

- 5.2.5 Vials

- 5.2.6 IV Fluids

- 5.2.7 Stick Packs

- 5.2.8 Pouches and Sachets

- 5.2.9 Caps and Closures

- 5.3 By Drug Delivery Mode

- 5.3.1 Oral

- 5.3.2 Injectable

- 5.3.3 Pulmonary

- 5.3.4 Topical and Transdermal

- 5.3.5 Other Modes

- 5.4 By Country

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Australia

- 5.4.6 Rest of Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Amcor plc

- 6.4.2 Gerresheimer AG

- 6.4.3 Schott AG

- 6.4.4 West Pharmaceutical Services Inc

- 6.4.5 CCL Industries Inc

- 6.4.6 NIPRO Corporation

- 6.4.7 Wihuri Group

- 6.4.8 Klockner Pentaplast Group

- 6.4.9 Catalent Pharma Solutions Inc

- 6.4.10 Berry Global Group Inc

- 6.4.11 SGD Pharma

- 6.4.12 AptarGroup Inc

- 6.4.13 Stevanato Group

- 6.4.14 Huhtamaki Oyj

- 6.4.15 Daikyo Seiko Ltd

- 6.4.16 Shandong Pharmaceutical Glass Co

- 6.4.17 Tekni-Plex Inc

- 6.4.18 Alpla Werke

- 6.4.19 Chongqing Zhengchuan Glass

- 6.4.20 Essel Propack Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

全球藥品包裝袋檢測系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球藥品包裝袋檢測系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 醫藥瓶裝盒機市場:按應用、最終用戶、機器類型、包裝材料和包裝速度分類 - 全球預測 2026-2032

醫藥瓶裝盒機市場:按應用、最終用戶、機器類型、包裝材料和包裝速度分類 - 全球預測 2026-2032 2026年全球藥品單劑量包裝市場報告

2026年全球藥品單劑量包裝市場報告 容器密封完整性測試市場分析及預測(至2035年):類型、產品、服務、技術、應用、材質類型、設備、製程、最終用戶、設施醫藥包裝市場分析及預測(至2035年):依類型、產品類型、材質、技術、應用、組件、最終用戶、功能、製程及解決方案分類全球疫苗包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

容器密封完整性測試市場分析及預測(至2035年):類型、產品、服務、技術、應用、材質類型、設備、製程、最終用戶、設施醫藥包裝市場分析及預測(至2035年):依類型、產品類型、材質、技術、應用、組件、最終用戶、功能、製程及解決方案分類全球疫苗包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 日本生物製藥包裝市場規模、佔有率、趨勢及預測(依材料、包裝類型、應用及地區分類),2026-2034年2026年全球微型離心管盒市場報告2026年全球益生菌包裝市場報告2026年全球藥品包裝檢測設備市場報告

日本生物製藥包裝市場規模、佔有率、趨勢及預測(依材料、包裝類型、應用及地區分類),2026-2034年2026年全球微型離心管盒市場報告2026年全球益生菌包裝市場報告2026年全球藥品包裝檢測設備市場報告