|

市場調查報告書

商品編碼

1939098

藍牙音箱:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Bluetooth Speaker - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

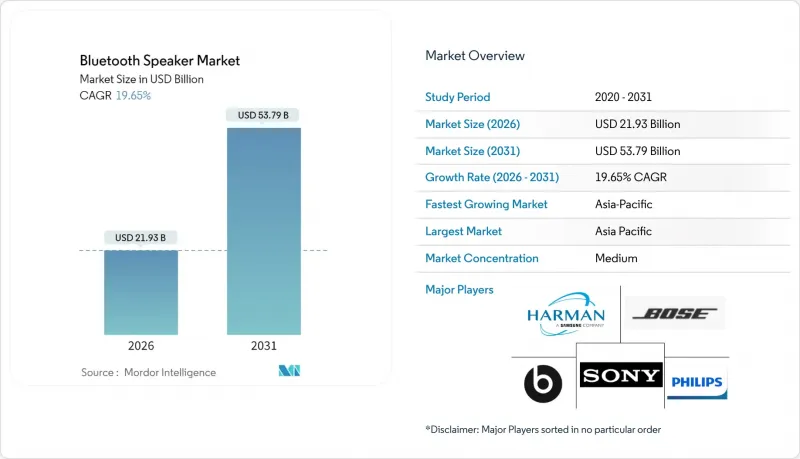

2025年藍牙音箱市場價值為183.2億美元,預計到2031年將達到537.9億美元,而2026年為219.3億美元。

預測期(2026-2031 年)的複合年成長率預計為 19.65%。

強勁的需求主要得益於智慧家庭的普及、音樂串流媒體的大眾化、電池成本的下降以及藍牙低功耗音訊的商業化,這些因素都在擴大目標用戶群的同時縮短更換週期。亞太地區憑藉其強大的製造地和快速壯大的中產階級,目前在銷量方面領先。同時,北美和歐洲由於智慧家庭的早期普及,實現了較高的平均售價。支援語音助理的型號是成長最快的品類,而僅支援藍牙的音箱仍然是最大的細分市場,它們無需Wi-Fi即可提供簡單、低延遲的體驗。競爭格局正朝著整合的方向發展,成熟品牌收購高階音響製造商以確保其專利技術和品牌價值,從而提高了普通產品廠商的進入門檻。

全球藍牙音箱市場趨勢與洞察

智慧家庭生態系統的快速普及

透過 Matter 標準實現的無縫互通性,正推動藍牙音箱從獨立的娛樂設備轉型為多功能智慧家庭中心。亞馬遜 2025 年推出的 Echo Show 系列正是這一轉變的體現,它將 Fire TV 服務、帶自動取景功能的視訊通訊以及對 Matter、Zigbee 和 Thread 的全面支援整合於一體。品牌間相容性的提升降低了轉換成本,刺激了那些希望透過語音控制音箱實現照明、暖通空調和安防控制的家庭對高級產品更換產品的需求。像 LegatoXP 這樣的中國 ODM 平台縮短了產品開發週期,使技術預算有限的中階品牌也能進入智慧家庭市場。這些因素共同加速了智慧家庭的普及,加劇了品牌競爭,並推動了對藍牙音箱的整體需求。

音樂串流服務的擴展

預計到2024年,音樂串流服務的付費用戶數量將超過7.5億,這將推動對能夠播放高解析度和空間音訊的硬體的需求。隨著LC3、LDAC和aptX Lossless等轉碼器技術的日益成熟,使用者越來越意識到傳統設備和新一代揚聲器在音質上的差異,從而刺激了更換需求。訂閱平台也鼓勵用戶選擇原生支援多人聆聽的多裝置套餐,這使得多房間揚聲器比單房間揚聲器系統更具優勢。串流媒體的循環收入模式鼓勵促銷商品搭售,折扣揚聲器可以作為吸引新用戶的手段,進一步刺激預測期內硬體的銷售成長。

假冒偽劣商品和盜版商品猖獗

未經授權的工廠大量複製熱門設計,以低劣的假冒商品充斥電商管道,給正品品牌帶來價格壓力,並損害消費者信任。仿冒品通常缺乏安全電路,增加電池起火的風險,並增加品牌透過認證技術、區塊鏈標籤和法律訴訟等手段進行保護的成本。雖然高階製造商正在實施安全全像圖和供應鏈追蹤,但小型供應商由於缺乏資金進行大規模監控,面臨收入損失和聲譽受損的風險。

細分市場分析

到2025年,桌上型和壁掛式藍牙音箱將佔據68.75%的市場佔有率,這表明消費者偏好能夠與電視和多房間平台無縫整合的主動音箱系統。此細分市場穩定的收入基礎為製造商提供了可預測的升級週期,這與智慧家庭維修計劃密切相關。同時,受都市區戶外活動和遠距辦公行動性需求的推動,可攜式音箱的複合年成長率將達到21.95%。

固定式藍牙音箱注重高音質、低音表現和語音助理控制——這些特性推高了平均售價,並促進了與串流媒體服務的捆綁銷售。同時,可攜式音箱則最佳化了堅固耐用的結構、輕巧的設計和超長的電池續航時間,吸引了新興市場的新買家。因此,這兩個細分市場正在同步發展,互不蠶食,為整個藍牙音箱市場提供了多元化的收入來源。

到2025年,住宅安裝將佔藍牙音箱市場的60.55%,維持21.85%的最快複合年成長率,這表明疫情封鎖期間形成的以家庭為中心的娛樂習慣已經根深蒂固。智慧家庭的持續升級已將更換週期縮短至四年以下,遠低於傳統高傳真音響設備的平均更換週期。

商業場所(餐廳、飯店、小規模辦公室)對高階安裝系統的需求依然重要,但面臨著冗長的採購流程和日益緊張的資金預算。隨著語音助理技術的日趨成熟,住宅音響正日益成為照明和暖通空調控制中心,將功能性與娛樂性融為一體,鞏固了主導地位。

區域分析

預計到2025年,亞太地區將佔據藍牙音箱市場31.45%的佔有率,並在2031年之前以21.15%的複合年成長率成長,這主要得益於製造業規模、年輕消費群體以及智慧型手機的快速普及。中國OEM廠商正利用其在印刷基板和電池供應鏈方面的地理接近性,縮短前置作業時間,以滿足國內對專業影音設備的需求。預計到2030年,國內市場對專業影音設備的需求將超過5.8兆元。政府對物聯網生態系統的扶持政策進一步加速了智慧音箱的普及,鞏固了主導地位。

北美地區的銷售量雖然落後於其他國家,但平均售價卻位居全球最高之列。智慧家庭的早期普及以及消費者對語音助理整合功能的付費意願,支撐了該地區高於平均的毛利率。從國家公園露營到都市區屋頂聚會,戶外休閒趨勢推動了對具備多設備連接功能的堅固耐用產品的需求。強大的品牌忠誠度使得像 Sonos 這樣的行業領導者能夠在價格競爭中保持高階銷售地位。

歐洲市場維持了穩健成長,成長速度在15%左右。嚴格的品質和網路安全標準賦予了成熟品牌優勢,而將於2024年8月生效的修訂版無線電設備指令(RED)將要求安全啟動和網路安全保護,從而有效地淘汰了那些沒有合規預算的低成本進口產品。由於消費者會根據合規性來評估產品價格,國內外製造商正將早期認證和CE標誌作為差異化因素。這將繼續推動全球藍牙音箱市場收入的成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 智慧家庭生態系統的快速普及

- 不斷擴大的音樂串流服務用戶

- 鋰離子電池平均售價(ASP)下降

- 戶外休閒與房車生活熱潮

- 隆重推出藍牙低功耗音訊和 Auracast

- 對身臨其境型課堂音訊的需求日益成長

- 市場限制

- 假冒偽劣商品和盜版商品猖獗

- 價格競爭導致利潤率下降

- 與電池起火相關的安全召回

- 歐盟收緊30瓦以上揚聲器的電磁干擾法規。

- 價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 移動性別

- 可攜式的

- 固定式/壁掛式

- 透過使用

- 住宅

- 商業的

- 透過連接技術

- 限藍牙

- 藍牙+Wi-Fi(支援多房間連線)

- 附語音助理的智慧音箱

- 透過分銷管道

- 僅限線上零售商

- 全通路電子產品量販店

- 按價格範圍

- 經濟型(50 美元以下)

- 中檔(50-199美元)

- 高級版(超過 200 美元)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 非洲

- 南非

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Sony Group Corporation

- Samsung Electronics Co., Ltd.(Harman International Industries, Inc.)

- Panasonic Holdings Corporation

- Bose Corporation

- Beats Electronics LLC(Apple Inc.)

- Koninklijke Philips NV

- LG Electronics Inc.

- Logitech International SA

- Sonos, Inc.

- Bang & Olufsen A/S

- Yamaha Corporation

- Altec Lansing LLC

- JVCKENWOOD Corporation

- Anker Innovations Technology Co., Ltd.

- Ultimate Ears(Logitech)

- Tribit Audio(Thesy Technology Co., Ltd.)

- Onkyo Home Entertainment Corporation

- Zebronics India Pvt. Ltd.

- AOMAIS Audio(Shenzhen Jin Wen Hua)

- SoundBot Inc.

第7章 市場機會與未來展望

The Bluetooth Speaker Market was valued at USD 18.32 billion in 2025 and estimated to grow from USD 21.93 billion in 2026 to reach USD 53.79 billion by 2031, at a CAGR of 19.65% during the forecast period (2026-2031).

Robust demand stems from smart-home adoption, mass music-streaming uptake, battery cost declines, and the commercialization of Bluetooth LE Audio, each widening the addressable user base while shortening replacement cycles. Asia-Pacific leads current unit volumes thanks to competitive manufacturing clusters and a rapidly expanding middle class, while North America and Europe deliver premium average selling prices (ASPs) on the back of early smart-home penetration. Voice-assistant-enabled models are the fastest-growing category, yet Bluetooth-only speakers still represent the largest sub-segment because they deliver a simple, low-latency experience that does not rely on Wi-Fi. Competitive dynamics are shifting toward consolidation as established brands purchase luxury audio houses to secure patented technologies and brand cachet, thereby raising entry barriers for commodity players.

Global Bluetooth Speaker Market Trends and Insights

Rapid Adoption of Smart-Home Ecosystems

Seamless interoperability delivered by the Matter standard elevates Bluetooth speakers from stand-alone entertainment devices to multifunction smart-home hubs. Amazon's 2025 Echo Show range illustrates the shift by embedding Fire TV services, auto-framing video communications, and full Matter, Zigbee, and Thread support in a single unit. Inter-brand compatibility lowers switching costs and drives premium replacement demand as households unify lighting, HVAC, and security control via voice-enabled speakers. Chinese ODM platforms such as LegatoXP shorten product development cycles, letting second-tier brands enter the smart-home space with smaller engineering budgets. Collectively, these forces accelerate household penetration, intensify brand competition, and enlarge the total volume opportunity for the Bluetooth speaker market.

Expansion of Music-Streaming Subscriptions

Music-streaming services surpassed 750 million paid subscribers in 2024, boosting demand for hardware capable of high-resolution and spatial-audio playback. As codecs such as LC3, LDAC, and aptX Lossless mature, users recognize audible quality deltas between legacy devices and next-generation speakers, prompting replacement purchases. Subscription platforms also encourage multi-device plans that natively support group listening, thereby favoring multi-room speakers over single-speaker setups. Streaming's recurring revenue model fosters promotional bundling, where discounted speakers act as customer-acquisition vehicles, further stimulating hardware volumes throughout the forecast window.

Rampant Counterfeiting and Piracy

Unauthorized factories replicate popular designs, flooding e-commerce channels with low-quality imitations that undercut legitimate brands on price and erode consumer trust. Counterfeits often omit essential safety circuits, raising the risk of battery fires and accelerating brand-protection expenditures for authentication technologies, blockchain labeling, and legal enforcement. While premium players deploy security holograms and supply-chain tracing, smaller vendors lack capital for large-scale monitoring, exposing them to revenue leaks and reputational damage.

Other drivers and restraints analyzed in the detailed report include:

- Bluetooth LE Audio and Auracast Roll-out

- Outdoor Recreation and Van-Life Boom

- Safety Recalls Tied to Battery Fires

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fixed and wall-mounted units accounted for 68.75% of the Bluetooth speaker market share in 2025, illustrating consumers' preference for power-fed systems that integrate seamlessly with televisions and multi-room platforms. This segment's steady revenue base gives manufacturers predictable upgrade cycles tied to smart-home renovation projects. Portable speakers, however, post a 21.95% CAGR, gaining from urban outdoor activities and remote-work mobility.

Fixed solutions emphasize audio fidelity, bass response, and voice-assistant control, traits that favor higher ASPs and bundling with streaming services. Portable designs optimize for rugged builds, lighter weight, and prolonged battery life, attracting first-time buyers in emerging markets. The two sub-segments, therefore, expand in parallel rather than cannibalize, yielding a diversified revenue structure for the overall Bluetooth speaker market.

Residential settings delivered 60.55% of the Bluetooth speaker market size in 2025 and also hold the fastest 21.85% CAGR, underscoring the permanence of home-centric entertainment habits formed during pandemic lockdowns. Continuous smart-home upgrades keep the replacement cycle under four years, far shorter than the historical averages for legacy hi-fi components.

Commercial demand, restaurants, hotels, and small offices, remains important for premium installed systems but faces elongated procurement processes and tighter capital budgets. As voice assistants mature, residential speakers increasingly serve as hubs for lighting and HVAC control, blending functional utility with leisure use and cementing their primacy in long-term demand projections for the Bluetooth speaker market.

The Global Bluetooth Speaker Market Report is Segmented by Portability (Portable, Fixed/Wall-Mounted), Application (Residential, Commercial), Connectivity Technology (Bluetooth-Only, and More), Distribution Channel (Online-Only Retailers, and More), Price Range (Economy Less Than USD 50, and More), and Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 31.45% of the Bluetooth speaker market share in 2025, generating a 21.15% CAGR to 2031 on the back of manufacturing scale, youth-oriented consumption, and rapid smartphone proliferation. Chinese OEMs leverage proximity to printed-circuit and battery supply chains to compress lead times and capitalize on domestic demand, which is forecast to surpass CNY 5.8 trillion for professional AV equipment by 2030. Government incentives for IoT ecosystems further accelerate the adoption of smart speakers, solidifying regional leadership in both volume and innovation.

North America trails in unit volumes yet achieves the highest ASPs. Early smart-home adoption and consumer willingness to pay for voice-assistant integration keep the region's gross margins above global averages. Outdoor recreation trends-from national park camping to city rooftop gatherings- stimulate demand for ruggedized models with multi-device pairing. Brand loyalty is strong, allowing category leaders such as Sonos to maintain premium shelf space even amid price-based competition.

Europe posts steady mid-teen growth, backed by stringent quality and cybersecurity standards that favor established brands. The updated Radio Equipment Directive effective August 2024 mandates secure boot and network safeguards, effectively filtering out low-end imports lacking compliance budgets. Consumers reward compliance with premium pricing, prompting local and international manufacturers to certify early and use CE markings as marketing differentiators, sustaining a value-heavy contribution to global Bluetooth speaker market revenues.

- Sony Group Corporation

- Samsung Electronics Co., Ltd. (Harman International Industries, Inc.)

- Panasonic Holdings Corporation

- Bose Corporation

- Beats Electronics LLC (Apple Inc.)

- Koninklijke Philips N.V.

- LG Electronics Inc.

- Logitech International S.A.

- Sonos, Inc.

- Bang & Olufsen A/S

- Yamaha Corporation

- Altec Lansing LLC

- JVCKENWOOD Corporation

- Anker Innovations Technology Co., Ltd.

- Ultimate Ears (Logitech)

- Tribit Audio (Thesy Technology Co., Ltd.)

- Onkyo Home Entertainment Corporation

- Zebronics India Pvt. Ltd.

- AOMAIS Audio (Shenzhen Jin Wen Hua)

- SoundBot Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid adoption of smart-home ecosystems

- 4.2.2 Expansion of music-streaming subscriptions

- 4.2.3 Falling ASPs of lithium-ion batteries

- 4.2.4 Outdoor recreation and van-life boom

- 4.2.5 Bluetooth LE Audio and Auracast roll-out

- 4.2.6 Growing demand for immersive classroom audio

- 4.3 Market Restraints

- 4.3.1 Rampant counterfeiting and piracy

- 4.3.2 Margin erosion from price wars

- 4.3.3 Safety recalls tied to battery fires

- 4.3.4 Stricter EU EMI limits for more than 30 W speakers

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Portability

- 5.1.1 Portable

- 5.1.2 Fixed / Wall-Mounted

- 5.2 By Application

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.3 By Connectivity Technology

- 5.3.1 Bluetooth-only

- 5.3.2 Bluetooth + Wi-Fi (Multi-room)

- 5.3.3 Smart Speakers w/ Voice Assistant

- 5.4 By Distribution Channel

- 5.4.1 Online-Only Retailers

- 5.4.2 Omnichannel Consumer-Electronics Stores

- 5.5 By Price Range

- 5.5.1 Economy (Less than USD 50)

- 5.5.2 Mid-range (USD 50-199)

- 5.5.3 Premium (More than USD 200)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Sony Group Corporation

- 6.4.2 Samsung Electronics Co., Ltd. (Harman International Industries, Inc.)

- 6.4.3 Panasonic Holdings Corporation

- 6.4.4 Bose Corporation

- 6.4.5 Beats Electronics LLC (Apple Inc.)

- 6.4.6 Koninklijke Philips N.V.

- 6.4.7 LG Electronics Inc.

- 6.4.8 Logitech International S.A.

- 6.4.9 Sonos, Inc.

- 6.4.10 Bang & Olufsen A/S

- 6.4.11 Yamaha Corporation

- 6.4.12 Altec Lansing LLC

- 6.4.13 JVCKENWOOD Corporation

- 6.4.14 Anker Innovations Technology Co., Ltd.

- 6.4.15 Ultimate Ears (Logitech)

- 6.4.16 Tribit Audio (Thesy Technology Co., Ltd.)

- 6.4.17 Onkyo Home Entertainment Corporation

- 6.4.18 Zebronics India Pvt. Ltd.

- 6.4.19 AOMAIS Audio (Shenzhen Jin Wen Hua)

- 6.4.20 SoundBot Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2026-2030年全球藍牙音箱市場

2026-2030年全球藍牙音箱市場 藍牙音箱市場:按便攜性、應用、銷售管道和地區分類

藍牙音箱市場:按便攜性、應用、銷售管道和地區分類 可攜式藍牙音箱市場:依防水等級、價格範圍、設計類型和銷售管道分類-2026-2032年全球市場預測藍牙音箱市場:依產品類型、應用和銷售管道-2026-2032年全球市場預測

可攜式藍牙音箱市場:依防水等級、價格範圍、設計類型和銷售管道分類-2026-2032年全球市場預測藍牙音箱市場:依產品類型、應用和銷售管道-2026-2032年全球市場預測 藍牙音箱市場報告:按便攜性、類型、價格、銷售管道和地區分類(2026-2034 年)戶外迷你音箱市場:按連接類型、電池容量、價格範圍、防水等級、揚聲器輸出功率、分銷管道和應用領域分類-全球預測,2026-2032年

藍牙音箱市場報告:按便攜性、類型、價格、銷售管道和地區分類(2026-2034 年)戶外迷你音箱市場:按連接類型、電池容量、價格範圍、防水等級、揚聲器輸出功率、分銷管道和應用領域分類-全球預測,2026-2032年 藍牙音箱市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、技術、銷售管道、地區和競爭格局分類,2021-2031年)防水藍牙音箱市場 - 全球產業規模、佔有率、趨勢、機會、預測:按充電技術、應用、地區和競爭格局分類,2021-2031年可攜式戶外揚聲器市場:按連接技術、價格範圍、產品類型、電源、揚聲器配置、分銷管道和最終用戶分類-2026-2032年全球預測

藍牙音箱市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、技術、銷售管道、地區和競爭格局分類,2021-2031年)防水藍牙音箱市場 - 全球產業規模、佔有率、趨勢、機會、預測:按充電技術、應用、地區和競爭格局分類,2021-2031年可攜式戶外揚聲器市場:按連接技術、價格範圍、產品類型、電源、揚聲器配置、分銷管道和最終用戶分類-2026-2032年全球預測