|

市場調查報告書

商品編碼

1939096

線控系統:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)X-by-wire System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

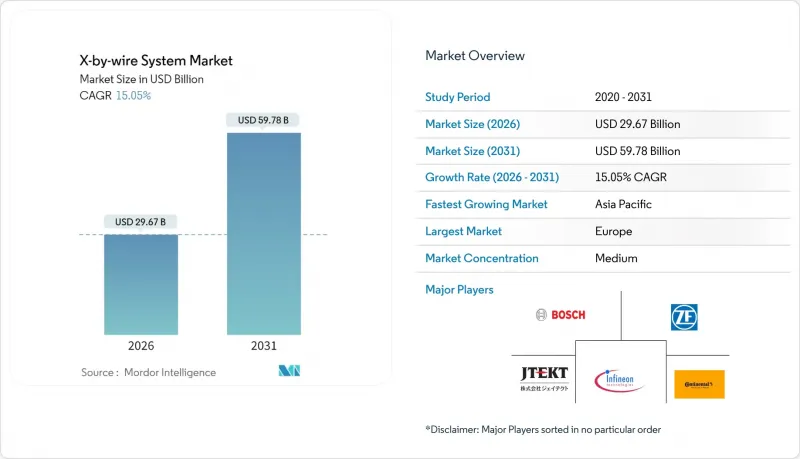

據估計,到 2026 年,線控系統市場價值將達到 296.7 億美元,高於 2025 年的 257.9 億美元,預計到 2031 年將達到 597.8 億美元。

預計2026年至2031年年複合成長率(CAGR)為15.05%。

加速推進電氣化、向軟體定義車輛轉型以及自動駕駛需求的共同作用,正促使機械聯鎖裝置被可程式設計電子控制系統所取代,這些控制系統用於控制油門、煞車、轉向、泊車和換檔功能。電池式電動車(BEV)已主導這一普及趨勢,因為其電氣基礎設施和滑板式平台消除了實體佈線限制並減輕了重量。諸如修訂後的ECE R 79.01標準(允許線控轉向而無需機械備份)等監管里程碑正在掃清剩餘的核准障礙。儘管各方競相提供將轉向、煞車和驅動系統整合到緊湊、無線可調單元中的模組化架構,但功能安全和網路安全合規性仍然是限制因素。

全球線控系統市場趨勢與洞察

推廣高級駕駛輔助系統和自動駕駛

不斷提升的自動化程度要求實現瞬時、可重複的控制執行,而這只有電子系統才能做到。一款大型純電動皮卡上安裝的線控轉向系統,因其性能優於機械轉向柱,榮獲了一項著名的技術獎。 4-5級自動化需要超過1000 TOPS的運算負載,要求致動器在微秒級做出回應。新型車輛的感測器套件會收集數百個資料流,需要透過線控介面將其轉換為精確的動態資訊。功能安全和網路安全法規(ISO 26262和ISO/SAE 21434)確立了明確的合規路徑,但也延長了開發週期。

全球安全和二氧化碳排放法規正在推動向電子產品的轉變

歐盟2025-2034年平均排放氣體法規實際上強制推行電氣化,這反過來又促進了能夠最佳化能源管理的電子控制子系統的應用。 ECE R 79.01標準正式批准了全電子轉向系統,並取消了機械備用系統的要求,這表明監管機構對冗餘電子安全通道充滿信心。強制性的高級緊急煞車和盲點監測系統也依賴線控精度,這加速了汽車製造商從液壓和電纜式系統向電子控制系統的轉型。

功能安全認證的障礙

取得線控系統 (X-by-wire) 的 ISO 26262 功能安全認證十分複雜,耗時耗力。線控系統的汽車安全完整性等級 (ASIL) 要求通常為 ASIL-C 或 ASIL-D 等級,並需要進行廣泛的檢驗流程,與傳統機械系統相比,這可能會使開發時間延長 18 至 24 個月。人工智慧和機器學習演算法的整合也為 ISO PAS 8800 認證帶來了額外的挑戰。線控系統全面獲得 ASIL-D 認證的測試和檢驗成本可能超過 5,000 萬美元,這對中小型原始設備製造商 (OEM) 和一級供應商而言,無疑是一筆巨大的財務負擔。

細分市場分析

到2025年,線控煞車系統將佔據線控系統市場39.42%的佔有率,這反映了該系統在ADAS煞車距離保障和能量回收煞車最佳化方面的重要性。隨著電動車的普及和能源回收策略對電煞車驅動的依賴性增強,線控制動系統的市場規模預計將顯著擴大。受監管合規性和自動駕駛技術進步的推動,線控轉向系統將以16.23%的複合年成長率實現最快成長。油門、停車和換檔等功能也逐漸取代電纜和液壓系統,但它們的相對價值貢獻仍然較低。

合約的簽訂體現了規模經濟效應:一家北美汽車製造商採購了500萬套線控煞車系統,將電子後煞車與液壓前煞車相結合,以平衡成本。在電子轉向系統領域,一款中國豪華轎車獲得了政府核准,採用全電子轉向系統,為其他製造商樹立了先例。供應商的研發藍圖目前正趨向於將電子轉向系統和線控煞車系統整合到一個密封單元中的角落模組,從而縮短組裝時間並簡化認證流程。

到2025年,乘用車將佔線控制動系統出貨量的73.65%,反映了輕型車輛的整體需求趨勢。然而,受車隊電氣化強制令以及線控制動系統在商業應用中帶來的營運優勢的推動,中型和重型卡車市場將以17.78%的複合年成長率加速成長。預計到2031年,商用卡車線控制動系統的市場規模將顯著成長,這主要得益於基於運作週期的投資回收期計算,例如煞車能量回收和維護成本降低。

車隊管理人員對電子驅動技術帶來的空中下載 (OTA) 診斷和預測性維護功能讚賞有加。初步試點計畫已證實,採用線控轉向技術可實現拖車自動定位,將場內操作時間縮短約 40%。輕型商用車 (LCV) 市場正經歷穩定成長,其中整合線控系統的電動平台越來越受到「最後一公里」配送應用的青睞。 REE Automotive 的 Leopard EV 就是一個典型的例子,它採用角式模組化架構,可實現自主配送作業。

區域分析

歐洲在2025年仍維持主導,市佔率將達35.20%。嚴格的二氧化碳排放目標和全面的安全法規系統性地優先考慮電子控制系統,而非傳統的機械控制系統。德國和法國的汽車製造商將首先在高階電動車中引入有線控制系統,待成本下降後再推廣到大眾市場車型。區域供應商正利用其數百年來累積的底盤技術經驗,同時轉型發展控制器軟體的專業知識。 ECE R 79.01法規所體現的監管確定性,為現有企業和新參與企業提供了投資信心。

亞太地區將成為成長引擎,到2031年將維持18.06%的複合年成長率。中國電動車的快速普及以及線控轉向量產車的早期獲批,為該地區的推廣應用樹立了典範。該地區憑藉其成熟的電子製造能力和供應鏈,能夠以具有競爭力的成本滿足線控轉向系統對複雜感測器和致動器的需求。日本和韓國提供高精度致動器和整合式轉角模組原型,這些產品已在無人計程車上進行實地測試。

北美市場正穩步成長,這主要得益於自動駕駛技術的大規模投資以及商用車電氣化的強制要求。特斯拉大規模訂購線控煞車訂單標誌著這一擴張勢頭強勁。美國半導體製造能力為先進的網域控制器提供了支持,網路安全框架也在不斷發展以符合國際ISO標準。隨著皮卡和SUV平台向滑板式電動車架構轉型,釋放出用於電子執行機構的封裝空間,電動車的普及速度正在加快。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 推廣先進的駕駛輔助系統和自動駕駛技術

- 全球安全標準和二氧化碳排放法規賦予電子產品優勢。

- 電動車包裝和輕量化優勢

- 採用數位底盤的成本節約型平台

- 支援OTA調優的軟體定義底盤

- 適用於車隊的轉角模組電動滑板

- 市場限制

- 功能安全認證的障礙

- 傳統平台整合成本高昂

- 車載網路安全挑戰

- 冗餘級感測器供不應求

- 價值/供應鏈分析

- 監管環境

- 技術展望 - 線控架構

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按類型

- 線控油門系統

- 線控煞車系統

- 線控轉向系統

- 線控泊車系統

- 線控換檔系統

- 按車輛類型

- 搭乘用車

- 輕型商用車

- 中型和重型商用車輛

- 按組件

- 感應器和踏板模組

- 致動器

- 電控系統(ECU)

- 依推進類型

- 內燃機車輛

- 混合動力汽車

- 電池式電動車

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Continental AG

- ZF Friedrichshafen AG

- Robert Bosch GmbH

- JTEKT Corporation

- Nexteer Automotive

- Infineon Technologies AG

- Nissan Motor Corporation

- Tesla Inc.

- Audi AG

- Toyota Motor Corporation

- Hitachi Astemo Ltd.

- Denso Corporation

- Curtiss-Wright Corporation

- CTS Corporation

- Valeo SA

- Orscheln Products LLC

- Torc Robotics

- Jaguar Land Rover

- REE Automotive

第7章 市場機會與未來展望

X-by-wire systems market size in 2026 is estimated at USD 29.67 billion, growing from 2025 value of USD 25.79 billion with 2031 projections showing USD 59.78 billion, growing at 15.05% CAGR over 2026-2031.

Accelerated electrification mandates, the software-defined-vehicle shift, and autonomy requirements are converging to displace mechanical linkages with programmable electronic control across throttle, brake, steer, park, and shift functions. Battery-electric vehicles (BEVs) already dominate adoption because their electrical infrastructure and skateboard platforms eliminate physical routing constraints while lowering weight. Regulatory milestones, such as the revised ECE R 79.01 that now permits steer-by-wire without a mechanical backup, are removing remaining approval bottlenecks. Competitive intensity is climbing as suppliers race to deliver corner-module architectures that bundle steering, braking, and drive systems into compact, over-the-air-tunable units, while functional-safety and cybersecurity compliance remain gating factors.

Global X-by-wire System Market Trends and Insights

Advanced-driver-assistance and Autonomy Push

Growing levels of automated driving demand instantaneous, repeatable control execution that only electronic systems can provide. A steer-by-wire implementation on a leading battery pickup recently earned a high-profile technology award, highlighting the performance leap over mechanical columns. Computing loads for Level 4-5 autonomy exceed 1,000 TOPS, making micro-second-scale actuator response mandatory. Sensor suites in new vehicles now collect hundreds of data streams; translating them into precise dynamics requires by-wire interfaces. Functional-safety and cybersecurity regulations (ISO 26262 and ISO/SAE 21434) establish clear compliance paths but lengthen development cycles.

Global Safety and CO2 Rules Favour Electronics

The EU's 2025-2034 fleet-average emissions limits effectively compel electrification, and by extension, electronic control subsystems that optimize energy management. ECE R 79.01 now formally allows full electronic steering systems, eliminating the mechanical fallback requirement and signaling regulators' trust in redundant electronic safety channels. Mandated advanced emergency braking and blind-spot monitoring systems similarly rely on by-wire precision, accelerating OEM migration away from hydraulics and cables.

Functional-safety Certification Hurdles

The complexity of achieving ISO 26262 functional safety certification for X-by-wire systems presents significant time and cost barriers. Automotive Safety Integrity Level (ASIL) requirements for by-wire systems typically demand ASIL-C or ASIL-D ratings, necessitating extensive validation processes that can extend development timelines by 18-24 months compared to traditional mechanical systems. The integration of AI and machine learning algorithms introduces additional certification challenges under ISO PAS 8800. Testing and validation costs for X-by-wire systems can exceed USD 50 million for comprehensive ASIL-D certification, creating financial barriers particularly challenging for smaller OEMs and tier-1 suppliers.

Other drivers and restraints analyzed in the detailed report include:

- EV Packaging and Weight-saving Benefits

- Digital Chassis Cost-saving Platforms

- High Integration Cost for Legacy Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Brake-by-wire secured a 39.42% X-by-wire systems market share in 2025, reflecting the system's centrality to ADAS stop-distance guarantees and regenerative-braking optimization. The X-by-wire systems market size for braking is projected to expand significantly as EV penetration rises and energy-recuperation strategies depend on electric brake actuation. Steer-by-wire shows the fastest upswing at 16.23% CAGR, enabled by regulatory acceptance and autonomy programs. Other functions like throttle, park, and shift continue to replace cables and hydraulics steadily, but their relative value content remains lower.

Contract awards reveal scale economies: a single North American OEM sourced brake-by-wire for 5 million units, combining electronic rear brakes with hydraulic fronts to balance cost. In steer-by-wire, a Chinese flagship sedan won government approval for full electronic steering, setting a precedent others will follow. Supplier roadmaps now converge on corner modules merging steer and brake-by-wire into sealed units, slashing assembly time and simplifying homologation.

Passenger cars represented 73.65% of the X-by-wire systems market 2025 shipments, mirroring overall light-vehicle demand. Nevertheless, medium and heavy trucks are accelerating at an 17.78% CAGR, driven by fleet electrification mandates and the operational advantages that X-by-wire systems provide in commercial applications. The X-by-wire systems market size for commercial trucks is expected to grow significantly by 2031, underpinned by duty-cycle-driven payback calculations linked to brake regeneration and reduced maintenance.

Fleet managers value over-the-air diagnostics and predictive maintenance unlocked by electronic actuation. Early pilots show steer-by-wire enabling automated trailer positioning, cutting yard maneuver time by approximately 40%. Light Commercial Vehicles experience moderate growth as last-mile delivery applications increasingly favor electric platforms with integrated by-wire controls, exemplified by REE Automotive's Leopard EV, which utilizes corner-module architecture for autonomous delivery operations.

The X-By-Wire Systems Market Report is Segmented by Type (Throttle-By-Wire, Brake-By-Wire, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Component (Sensors and Pedal Modules, Actuators, and ECUs), Propulsion Type (Internal-Combustion Engine, Hybrid, and Battery-Electric), and Geography (North America, South America, Europe, and More). Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe retained leadership at 35.20% share in 2025 owing to stringent CO2 emission targets and comprehensive safety regulations that systematically favor electronic control systems over traditional mechanical alternatives. German and French OEMs deploy by wire on premium EVs first, then cascade to mass segments once cost curves dip. Regional suppliers exploit centuries of chassis know-how while pivoting to domain-controller software expertise. Regulatory certainty, embodied in ECE R 79.01, gives investment confidence to both incumbents and new entrants.

Asia-Pacific is the growth engine with an 18.06% CAGR through 2031. China's rapid BEV uptake and early approval of steer-by-wire production vehicles have created the blueprint for regional adoption. The area benefits from established electronics manufacturing capabilities and supply chains supporting X-by-wire systems' complex sensor and actuator requirements at competitive costs. Japan and South Korea contribute high-precision actuators and integrated corner-module prototypes that are already being field-tested on the robotaxis.

North America posts steady gains, supported by significant investments in autonomous driving technologies and commercial vehicle electrification mandates. A high-volume brake-by-wire award to Tesla underlines scaling momentum. U.S. semiconductor capacity supports advanced domain controllers, while cybersecurity frameworks evolve to align with global ISO standards. Uptake accelerates as pickup-truck and SUV platforms transition to skateboard EV architectures, freeing packaging for electronic actuation.

- Continental AG

- ZF Friedrichshafen AG

- Robert Bosch GmbH

- JTEKT Corporation

- Nexteer Automotive

- Infineon Technologies AG

- Nissan Motor Corporation

- Tesla Inc.

- Audi AG

- Toyota Motor Corporation

- Hitachi Astemo Ltd.

- Denso Corporation

- Curtiss-Wright Corporation

- CTS Corporation

- Valeo SA

- Orscheln Products LLC

- Torc Robotics

- Jaguar Land Rover

- REE Automotive

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advanced-driver-assistance and Autonomy Push

- 4.2.2 Global Safety and CO2 Rules Favour Electronics

- 4.2.3 EV Packaging and Weight-saving Benefits

- 4.2.4 Digital Chassis Cost-saving Platforms

- 4.2.5 OTA-tunable Software-defined Chassis

- 4.2.6 Corner-module EV Skateboards for Fleets

- 4.3 Market Restraints

- 4.3.1 Functional-safety Certification Hurdles

- 4.3.2 High Integration Cost for Legacy Platforms

- 4.3.3 In-vehicle-network Cyber-security Gaps

- 4.3.4 Supply Crunch of Redundancy-grade Sensors

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook - X-by-wire Control Architectures

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Type

- 5.1.1 Throttle-by-wire System

- 5.1.2 Brake-by-wire System

- 5.1.3 Steer-by-wire System

- 5.1.4 Park-by-wire System

- 5.1.5 Shift-by-wire System

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Medium and Heavy Commercial Vehicles

- 5.3 By Component

- 5.3.1 Sensors and Pedal Modules

- 5.3.2 Actuators

- 5.3.3 Electronic Control Units (ECUs)

- 5.4 By Propulsion Type

- 5.4.1 Internal-Combustion Engine Vehicles

- 5.4.2 Hybrid Vehicles

- 5.4.3 Battery-Electric Vehicles

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle-East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Continental AG

- 6.4.2 ZF Friedrichshafen AG

- 6.4.3 Robert Bosch GmbH

- 6.4.4 JTEKT Corporation

- 6.4.5 Nexteer Automotive

- 6.4.6 Infineon Technologies AG

- 6.4.7 Nissan Motor Corporation

- 6.4.8 Tesla Inc.

- 6.4.9 Audi AG

- 6.4.10 Toyota Motor Corporation

- 6.4.11 Hitachi Astemo Ltd.

- 6.4.12 Denso Corporation

- 6.4.13 Curtiss-Wright Corporation

- 6.4.14 CTS Corporation

- 6.4.15 Valeo SA

- 6.4.16 Orscheln Products LLC

- 6.4.17 Torc Robotics

- 6.4.18 Jaguar Land Rover

- 6.4.19 REE Automotive

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

線控系統市場:按組件、推進類型、系統類型、技術、銷售管道和車輛類型分類-全球預測,2026-2032年

線控系統市場:按組件、推進類型、系統類型、技術、銷售管道和車輛類型分類-全球預測,2026-2032年 線控刹車安全標準合規市場預測至2034年-按組件、系統類型、車輛類型、技術、應用和地區分類的全球分析

線控刹車安全標準合規市場預測至2034年-按組件、系統類型、車輛類型、技術、應用和地區分類的全球分析 汽車線控系統市場 - 全球產業規模、佔有率、趨勢、機會、預測:按車輛類型、系統類型、地區和競爭對手分類,2021-2031年

汽車線控系統市場 - 全球產業規模、佔有率、趨勢、機會、預測:按車輛類型、系統類型、地區和競爭對手分類,2021-2031年 線控系統市場報告:按類型、車輛類型和地區分類(2026-2034 年)

線控系統市場報告:按類型、車輛類型和地區分類(2026-2034 年) 2026年全球汽車線控系統市場報告

2026年全球汽車線控系統市場報告 全球線傳系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)日本線控系統市場報告(按車輛類型(乘用車、商用車)、應用類型(油門線控系統、煞車線控系統、轉向線控系統、停車線控系統、換檔線控系統)和地區分類,2026-2034 年)

全球線傳系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)日本線控系統市場報告(按車輛類型(乘用車、商用車)、應用類型(油門線控系統、煞車線控系統、轉向線控系統、停車線控系統、換檔線控系統)和地區分類,2026-2034 年) X-by-Wire 市場,按組件類型、按系統類型、按自主級別、按技術、按應用、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測

X-by-Wire 市場,按組件類型、按系統類型、按自主級別、按技術、按應用、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測 汽車線控系統市場規模、佔有率和趨勢分析報告:按車輛、類型、地區和細分市場預測,2024-2030 年

汽車線控系統市場規模、佔有率和趨勢分析報告:按車輛、類型、地區和細分市場預測,2024-2030 年