|

市場調查報告書

商品編碼

1939093

聲波感測器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Acoustic Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

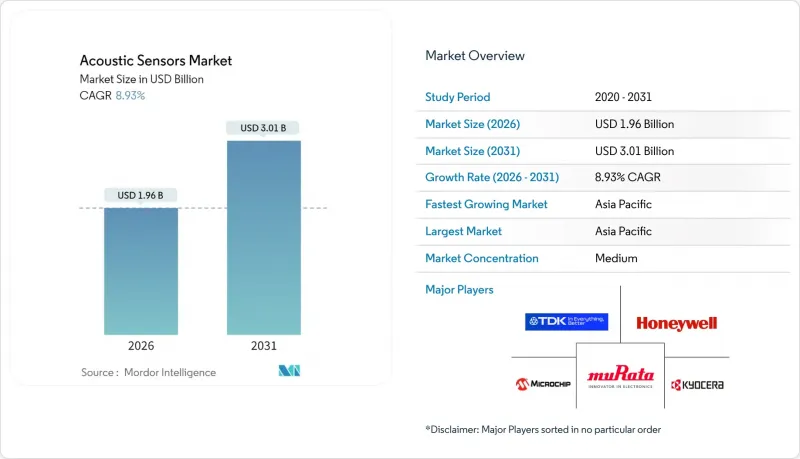

預計到 2026 年,聲波感測器市場規模將達到 19.6 億美元,高於 2025 年的 18 億美元。

預計到 2031 年將達到 30.1 億美元,2026 年至 2031 年的複合年成長率為 8.93%。

這一成長主要受以下因素驅動:5G 和 Wi-Fi 7 對高頻濾波器的強勁需求、交通運輸的電氣化、工業物聯網 (IIoT) 的快速普及以及小型化進程的持續推進。通訊基礎設施的升級推動了體聲波 (BAW) 濾波器的銷售,而表面聲波 (SAW) 裝置在 3 GHz 以下頻段的應用領域也保持著成長勢頭。電動車 (EV) 和高級駕駛輔助系統 (ADAS) 需要無電池無線感測技術,以減輕線束重量並抵抗強烈電磁干擾。 IIoT 使用者目前傾向於使用邊緣聲波感測器進行預測性維護,而可印刷壓電薄膜則實現了結構健康監測和醫療拋棄式產品領域的超低成本部署。在競爭格局方面,大型半導體公司的進入正在加速創新週期,而壓電基板供不應求和地緣政治風險在供應鏈中也日益凸顯。

全球聲波感測器市場趨勢與洞察

5G 和 Wi-Fi 7 基礎設施的快速普及將推動高頻濾波器的需求。

隨著通訊業者升級到 5G 和 Wi-Fi 7,他們需要工作頻率高於 3 頻寬 的濾波器,而電子濾波器在該頻段的性能已接近極限。表面聲波 (SAW)頻寬,尤其是體聲波 (BAW) 裝置,能夠提供所需的陡峭滾降特性和低插入損耗。村田製作所 2024 年的產能擴張計畫與支援 6 GHz 頻段 Wi-Fi 7 的智慧型手機訂單直接相關。

車輛電氣化將加速無線感測技術的應用。

電動車平台傾向於採用輕量化、無電池的感測器,這些感測器能夠採集振動或射頻能量。大陸集團將於2024年推出的無線聲學胎壓監測裝置,不僅符合ISO 26262功能安全標準,在高電磁干擾環境下也展現可靠性。

溫度漂移和惡劣環境包裝限制

石英元件的溫度漂移為 20 至 50 ppm/°C,需要高成本的補償電路或氣密封裝,對於航太設計而言,-55°C 至 +125°C 的溫度範圍內,其成本可能比商用元件高成本%,而且振動應力會增加重新校準的需求。

細分市場分析

預計到2025年,聲波感測器市場規模將達到11.9億美元。在製程工業中,由於可靠的電源供應和資料傳輸,有線方案仍然是首選。然而,價值6.1億美元的無線解決方案預計將成長更快,這主要得益於維修的經濟效益和電動車的需求。無線解決方案10.74%的複合年成長率反映了能源採集技術的進步,這些技術延長了維護週期。基於IEC 61508的標準化和冗餘射頻通訊協定正在推動其在關鍵任務系統中的應用。

風能產業的安裝商報告稱,森薩塔的無電池節點使用壽命延長了10年以上。無線部署被認為是聲波感測器市場的主要成長動力,因為佈線成本的降低和部署速度的加快可以抵消設備初始價格較高的問題。

預計到2025年,聲表面波(SAW)裝置的市場規模將達到12.4億美元(聲波感測器市場佔有率為69.10%),在3GHz以下頻段應用領域佔據主導地位,並得益於成熟且經濟的石英加工技術。然而,隨著通訊領域頻率的不斷提升,體聲波(BAW)裝置在3GHz以上頻段展現出卓越的性能優勢,從而帶來了5.6億美元的市場機會。 TDK在日本投資1億美元用於BAW元件,目標市場為Wi-Fi 7和5G設備,這將推動BAW元件實現兩位數的成長。

雖然 SAW 在工業和消費領域得到了廣泛應用,但基於物理原理的上限頻率限制確保了 BAW 在高頻寬需求領域繼續佔據主導地位。

區域分析

預計到2025年,亞太地區將創造6.7億美元的市場規模,佔全球總營收的37.20%,複合年成長率(CAGR)為9.81%。中國不斷擴大的製造地和日本卓越的材料技術鞏固了該地區的市場主導地位。韓國5G的快速部署和電動車出口將進一步擴大該地區的聲波感測器市場規模。

北美緊追在後,投入5.1億美元,主要得益於工業IoT改裝和航太領域嚴格的可靠性要求。聯邦政府資助的高超音速飛行器監測計畫正在加速國防領域的應用。歐洲投入4.3億美元,受惠於電動車強制令以及強調永續性和工人安全的基建監測法規。

雖然中東、非洲和南美洲仍在發展中,但在石油和天然氣、採礦和智慧計劃中,無線、無電池節點非常適合偏遠和危險的地點,試點部署正在進行中。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 5G 和 Wi-Fi 7 的快速部署正在推動高頻 SAW/BAW 濾波器的需求。

- 汽車產業向電動車和高級駕駛輔助系統(ADAS)的轉型正在加速無線、無電池感測器的應用。

- 工業IoT和預測性維護計劃的成長

- 印刷式軟性壓電薄膜可實現超低成本感測表面

- 微型MEMS麥克風促進了語音使用者介面在穿戴和可聽裝置中的普及。

- 政府法規強制要求對環境和基礎設施進行即時監測

- 市場限制

- 惡劣環境下的溫度漂移與包裝挑戰

- 在高精度細分市場中,與光學和電容式替代方案競爭

- 半導體供應鏈的波動性正在推高前置作業時間和投入成本。

- 材料標準碎片化阻礙了跨平台互通性

- 產業價值/價值鏈分析

- 監管現狀和標準

- 技術展望(邊緣運算和人工智慧分析)

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 競爭對手之間的競爭

- 替代品的威脅

第5章 市場規模與成長預測

- 按類型

- 有線

- 無線的

- 按波形類型

- 表面聲波(SAW)

- 瑞利表面波

- 體聲波(BAW)

- 表面聲波(SAW)

- 透過檢測參數

- 溫度

- 壓力

- 扭力

- 濕度

- 大量的

- 黏度

- 透過使用

- 車

- 航太/國防

- 家用電子電器

- 衛生保健

- 產業

- 環境監測

- 其他用途

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 中東

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Murata Manufacturing Co., Ltd.

- TDK Corporation

- KYOCERA Corporation

- Honeywell International Inc.

- Microchip Technology Inc.(Vectron International)

- Transense Technologies plc

- Pro-micron GmbH & Co. KG

- CTS Corporation

- IFM Electronic GmbH

- Dytran Instruments, Inc.

- Campbell Scientific, Inc.

- API Technologies Corp.

- SENSeOR SAS

- CeramTec GmbH

- Boston Piezo-Optics Inc.

- Teledyne Microwave Solutions

- Raltron Electronics Corporation

- Taiyo Yuden Co., Ltd.

- AVX Corporation

- Althen GmbH Mess-und Sensortechnik

- Sensor Technology Ltd.

第7章 市場機會與未來展望

Acoustic sensor market size in 2026 is estimated at USD 1.96 billion, growing from 2025 value of USD 1.8 billion with 2031 projections showing USD 3.01 billion, growing at 8.93% CAGR over 2026-2031.

The expansion is fueled by soaring high-frequency filtering demand for 5G and Wi-Fi 7, electrification in transportation, rapid industrial Internet of Things (IIoT) adoption, and continuing miniaturization initiatives. Telecommunications infrastructure upgrades are propelling bulk acoustic wave (BAW) filter sales, while surface acoustic wave (SAW) devices sustain growth in sub-3 GHz applications. Electric vehicles (EVs) and advanced driver assistance systems (ADAS) require battery-free wireless sensing to cut harness weight and withstand strong electromagnetic interference. IIoT users now favor edge-enabled acoustic sensors for predictive maintenance, and printed piezoelectric films promise ultra-low-cost deployments across structural health and medical disposables. Competitive dynamics reflect semiconductor majors entering the space, intensifying innovation cycles but exposing the supply chain to piezoelectric substrate shortages and geopolitical risks.

Global Acoustic Sensors Market Trends and Insights

Rapid 5G and Wi-Fi 7 Infrastructure Driving High-Frequency Filter Demand

Telecommunications providers upgrading to 5G and Wi-Fi 7 need filters operating above 3 GHz, a range where electronic alternatives falter. SAW and especially BAW devices deliver the required steep roll-off and low insertion loss. Murata's 2024 capacity expansion directly aligns with smartphone orders targeting the 6 GHz Wi-Fi 7 band.

Automotive Electrification Accelerating Wireless Sensing Adoption

EV platforms favor lightweight, battery-free sensors that harvest vibration or RF energy. Continental's 2024 launch of wireless acoustic tire-pressure units illustrates reliability under high electromagnetic interference while meeting ISO 26262 functional-safety demands.

Temperature Drift and Harsh-Environment Packaging Limitations

Quartz-based devices drift 20-50 ppm / °C, forcing costly compensation or hermetic sealing. Aerospace designs spanning -55 °C to +125 °C may cost 300-500% more than commercial units, and vibration stresses accelerate recalibration needs.

Other drivers and restraints analyzed in the detailed report include:

- Growth of IIoT and Predictive-Maintenance Programs

- Printed and Flexible Piezoelectric Films Enabling Ultra-Low-Cost Sensing

- Semiconductor Supply-Chain Volatility Impacting Material Availability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The acoustic sensor market size attributed to wired devices reached USD 1.19 billion in 2025. Wired formats remain favored for reliable power and data in process industries. However, wireless solutions, valued at USD 0.61 billion, are growing faster due to retrofit economics and EV demand. Wireless solutions' 10.74% CAGR reflects energy-harvesting breakthroughs that extend maintenance intervals. Standardization under IEC 61508 and redundant RF protocols improves acceptance in mission-critical systems.

Installers in wind energy report service-life gains exceeding 10 years from Sensata's battery-free nodes. Lower cabling costs and accelerated deployment offset initial device premiums, positioning wireless deployments as a primary growth vector in the acoustic sensor market.

SAW devices contributed USD 1.24 billion, equal to 69.10% acoustic sensor market share in 2025, favored for sub-3 GHz applications and mature, economical quartz processing. Yet ascending frequencies in telecom open USD 0.56 billion BAW opportunities with performance advantages above 3 GHz. TDK's USD 100 million Japanese line targets Wi-Fi 7 and 5G handsets, validating BAW's double-digit expansion.

While SAW maintains broad adoption across industrial and consumer segments, physics-based frequency ceilings ensure BAW's sustained outperformance wherever high-band requirements dominate.

The Acoustic Sensor Market Report is Segmented by Type (Wired, Wireless), Wave Type (Surface Acoustic Wave, Bulk Acoustic Wave), Sensing Parameter (Temperature, Pressure, Torque, Humidity, Mass, Viscosity), Application (Automotive, Aerospace and Defense, Consumer Electronics, Healthcare, Industrial, Environmental Monitoring, Other Applications), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific provided USD 0.67 billion, commanding 37.20% 2025 revenue and pacing at 9.81% CAGR. China's fab expansions and Japan's materials leadership buttress regional advantages. South Korea's rapid 5G roll-out and EV exports further enlarge the regional acoustic sensor market size.

North America followed with USD 0.51 billion, sustained by IIoT retrofits and stringent aerospace reliability requirements. Federal programs funding hypersonic vehicle monitoring accelerate defense uptake. Europe delivered USD 0.43 billion, benefiting from EV mandates and infrastructure monitoring regulations emphasizing sustainability and worker safety.

Middle East and Africa and South America remain nascent yet attract pilot deployments for oil-and-gas, mining, and smart-city projects where wireless battery-free nodes suit remote or hazardous locales.

- Murata Manufacturing Co., Ltd.

- TDK Corporation

- KYOCERA Corporation

- Honeywell International Inc.

- Microchip Technology Inc. (Vectron International)

- Transense Technologies plc

- Pro-micron GmbH & Co. KG

- CTS Corporation

- IFM Electronic GmbH

- Dytran Instruments, Inc.

- Campbell Scientific, Inc.

- API Technologies Corp.

- SENSeOR SAS

- CeramTec GmbH

- Boston Piezo-Optics Inc.

- Teledyne Microwave Solutions

- Raltron Electronics Corporation

- Taiyo Yuden Co., Ltd.

- AVX Corporation

- Althen GmbH Mess- und Sensortechnik

- Sensor Technology Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid 5G and Wi-Fi 7 roll-outs raising demand for high-frequency SAW/BAW filters

- 4.2.2 Automotive shift to EVs and ADAS accelerating wireless, battery-free sensor adoption

- 4.2.3 Growth of Industrial IoT and predictive-maintenance programs

- 4.2.4 Printed and flexible piezoelectric films enabling ultra-low-cost sensing surfaces

- 4.2.5 Miniaturized MEMS microphones powering voice-UI proliferation in wearables and hearables

- 4.2.6 Government regulations mandating real-time environmental and infrastructure monitoring

- 4.3 Market Restraints

- 4.3.1 Temperature-drift and packaging challenges in harsh environments

- 4.3.2 Competition from optical and capacitive alternatives in high-precision niches

- 4.3.3 Semiconductor supply-chain volatility pushing lead-times and input costs higher

- 4.3.4 Fragmented material standards hindering cross-platform interoperability

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape and Standards

- 4.6 Technological Outlook (Edge and AI analytics)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Wired

- 5.1.2 Wireless

- 5.2 By Wave Type

- 5.2.1 Surface Acoustic Wave (SAW)

- 5.2.1.1 Rayleigh Surface Wave

- 5.2.2 Bulk Acoustic Wave (BAW)

- 5.2.1 Surface Acoustic Wave (SAW)

- 5.3 By Sensing Parameter

- 5.3.1 Temperature

- 5.3.2 Pressure

- 5.3.3 Torque

- 5.3.4 Humidity

- 5.3.5 Mass

- 5.3.6 Viscosity

- 5.4 By Application

- 5.4.1 Automotive

- 5.4.2 Aerospace and Defense

- 5.4.3 Consumer Electronics

- 5.4.4 Healthcare

- 5.4.5 Industrial

- 5.4.6 Environmental Monitoring

- 5.4.7 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Murata Manufacturing Co., Ltd.

- 6.4.2 TDK Corporation

- 6.4.3 KYOCERA Corporation

- 6.4.4 Honeywell International Inc.

- 6.4.5 Microchip Technology Inc. (Vectron International)

- 6.4.6 Transense Technologies plc

- 6.4.7 Pro-micron GmbH & Co. KG

- 6.4.8 CTS Corporation

- 6.4.9 IFM Electronic GmbH

- 6.4.10 Dytran Instruments, Inc.

- 6.4.11 Campbell Scientific, Inc.

- 6.4.12 API Technologies Corp.

- 6.4.13 SENSeOR SAS

- 6.4.14 CeramTec GmbH

- 6.4.15 Boston Piezo-Optics Inc.

- 6.4.16 Teledyne Microwave Solutions

- 6.4.17 Raltron Electronics Corporation

- 6.4.18 Taiyo Yuden Co., Ltd.

- 6.4.19 AVX Corporation

- 6.4.20 Althen GmbH Mess- und Sensortechnik

- 6.4.21 Sensor Technology Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

智慧音訊系統市場預測至2034年-按產品類型、系統、組件、應用、最終用戶和地區分類的全球分析

智慧音訊系統市場預測至2034年-按產品類型、系統、組件、應用、最終用戶和地區分類的全球分析 高精度聲波感測器市場分析與預測(至2035年):類型、產品類型、技術、組件、應用、材料類型、最終用戶、功能、安裝方式、解決方案

高精度聲波感測器市場分析與預測(至2035年):類型、產品類型、技術、組件、應用、材料類型、最終用戶、功能、安裝方式、解決方案 全球浸沒式超音波掃描顯微鏡市場分析及預測(至2032年)

全球浸沒式超音波掃描顯微鏡市場分析及預測(至2032年) 2026年全球海洋聲波感測器市場報告

2026年全球海洋聲波感測器市場報告 全球氣密封裝超音波感測器市場(按輸出類型、安裝方式、頻率範圍、換能器材料、應用和最終用戶產業分類)預測(2026-2032年)壓電浸沒式超音波換能器市場(按產品類型、頻率範圍、材料類型、應用和最終用戶產業分類),全球預測,2026-2032年壓電超音波換能器市場:按產品類型、運作頻率、材料、應用和最終用戶分類,全球預測(2026-2032年)海洋振動地震探勘市場按探勘類型、平台類型、合約類型、頻率類型和應用分類-全球預測,2026-2032年超音波換能器市場按應用、產品類型、頻率範圍、最終用戶和銷售管道,全球預測(2026-2032年)

全球氣密封裝超音波感測器市場(按輸出類型、安裝方式、頻率範圍、換能器材料、應用和最終用戶產業分類)預測(2026-2032年)壓電浸沒式超音波換能器市場(按產品類型、頻率範圍、材料類型、應用和最終用戶產業分類),全球預測,2026-2032年壓電超音波換能器市場:按產品類型、運作頻率、材料、應用和最終用戶分類,全球預測(2026-2032年)海洋振動地震探勘市場按探勘類型、平台類型、合約類型、頻率類型和應用分類-全球預測,2026-2032年超音波換能器市場按應用、產品類型、頻率範圍、最終用戶和銷售管道,全球預測(2026-2032年) 聲波感測器市場規模、佔有率和成長分析(按感測器類型、技術、終端用戶產業和地區分類)-2026-2033年產業預測

聲波感測器市場規模、佔有率和成長分析(按感測器類型、技術、終端用戶產業和地區分類)-2026-2033年產業預測