|

市場調查報告書

商品編碼

1939091

醋酸:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Acetic Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

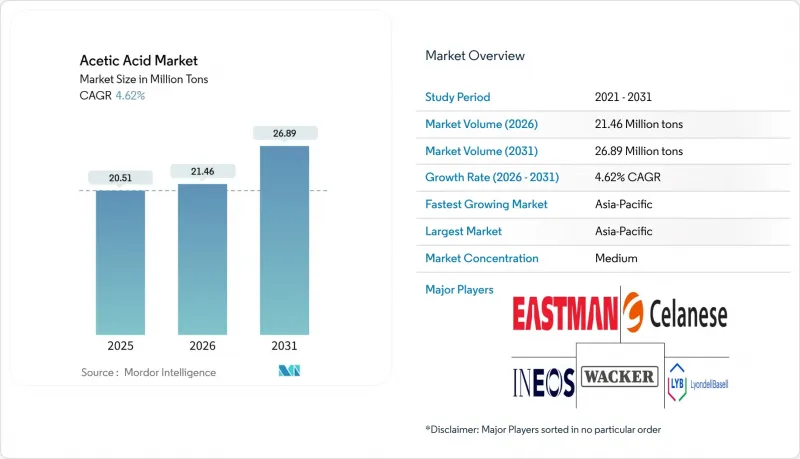

預計到 2026 年,醋酸市場規模將達到 2,048 萬噸,高於 2025 年的 1,958 萬噸。

預計到 2031 年將達到 2,562 萬噸,2026 年至 2031 年的複合年成長率為 4.58%。

對醋酸乙烯單體、純對苯二甲酸和新興電池級電解液的強勁需求支撐著市場成長。規模化帶來的成本效益、永續性的永續發展需求以及與下游製程的整合,正在提升生產商的利潤率。亞太地區繼續佔據主導地位,因為聚酯、黏合劑和溶劑的消費量依然居高不下。監管審查的加強正在加速對低碳生產技術和碳捕獲計劃的投資,進一步塑造醋酸市場的競爭動態。

全球醋酸市場趨勢與洞察

對醋酸乙烯單體的需求不斷成長

醋酸乙烯單體是水性黏合劑和塗料配方中不可或缺的成分,能夠賦予產品優異的黏合強度和柔軟性。這些特性符合嚴格的溶劑排放環保法規,尤其是在建設業和汽車製造業。亞太地區佔全球醋酸乙烯酯單體消費量的60%以上,推動了在需求中心附近進行乙醯基一體化生產的投資。塞拉尼斯位於南京新建的醋酸乙烯酯和乙烯生產裝置新增7萬噸產能,充分展現了位置優勢。

純對苯二甲酸的消費量增加

紡織和包裝產業對聚酯的需求不斷成長,推動了純對苯二甲酸)消費量的成長,進而促進了乙酸作為溶劑和反應介質的應用。中國石油化學集團公司(中石化)位於江蘇省的年產300萬噸的單線PTA裝置,目前已成為亞太地區的標準生產規模。規模較大的裝置在提高乙酸利用效率的同時,也維持了整體需求的成長。區域供應不平衡,例如印度PTA價格溢價,為靈活的供應商提供了套利機會。

與羰基化反應相關的二氧化碳/揮發性排放法規

北美和歐洲的監管機構目前正在對羰基化反應器和蒸餾製程的排放進行監管。美國環保署 (EPA) 的監管指南和加拿大的《環境保護法》都在收緊排放限制。合規需要投資碳捕獲和先進的洗滌器,這有利於擁有充足資金的大型生產商。 Serenes 公司位於克利爾湖的工廠維修項目捕獲了用於甲醇合成的二氧化碳,為綜合排放樹立了標竿。

細分市場分析

到2025年,受建築和汽車行業對水性黏合劑需求成長的推動,醋酸乙烯單體將佔醋酸市場佔有率的27.25%。聚醋酸乙烯酯和乙烯-醋酸乙烯酯共聚物透過取代無法滿足新排放標準的溶劑型體系,正在確保市場成長。 Serenes和Ineos正利用後後向整合建立下游供應鏈並降低成本。

受服飾和瓶裝樹脂中聚酯需求成長的推動,純對苯二甲酸年成長率 (CAGR) 達到 4.95%。乙酸乙酯在醫藥和塗料溶劑領域保持穩定需求,而乙酸酐儘管在香菸過濾嘴領域需求下降,但在醫藥乙醯化應用方面仍表現強勁。衍生產品的需求模式反映了生產商在整個乙醯化過程中創造附加價值的策略。一體化企業正在將大宗乙酸生產轉化為高利潤的下游產品,以在原物料價格波動期間確保收入。

此乙酸報告按衍生物(醋酸乙烯單體、純對苯二甲酸、乙酸乙酯等)、生產路線(甲醇羰基化、乙醛氧化等)、應用(塑膠和聚合物、食品和飲料、黏合劑、油漆和塗料、紡織品、醫療、其他應用)和地區(亞太地區、北美、歐洲、南美、中東和非洲)分析市場。

區域分析

預計到2025年,亞太地區將佔全球醋酸市場佔有率的68.10%,並在2031年之前以5.05%的複合年成長率成長。光是中國就控制著全球約55%的醋酸產能,使其擁有規模經濟和區域定價權。該地區龐大的聚酯和黏合劑產業也有助於穩定需求,即使在外部經濟波動的情況下也是如此。

北美消費市場日趨成熟,同時低碳生產領域也獲得了大量投資。塞拉尼斯公司位於克利爾湖的工廠擴建項目產能達130萬噸,該項目整合了二氧化碳捕集技術和穩定的原料供應,以確保競爭力。旨在減少排放的計劃正在推動美國和加拿大的生物基計劃,並有可能將部分進口產品轉向國內供應。

在歐洲,循環經濟原則和嚴格的生命週期評估是首要任務。獲得低碳足跡認證的生產商在汽車和包裝行業中享有優先採購權。新興的中東和非洲地區正尋求擴大產能,以利用其具有競爭力的原料成本,但基礎設施和法規結構仍在發展中。在拉丁美洲,受聚酯瓶樹脂和食品防腐劑應用的推動,醋酸市場穩步成長,但與亞太地區的生產規模相比仍然有限。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 對醋酸乙烯單體(VAM)的需求不斷成長

- 純對苯二甲酸(PTA)消費量增加

- 乙酸酯溶劑在高固態塗料的應用拓展

- 在淨零排放目標下,生物基醋酸的應用趨勢

- 鋰離子電池電解液添加劑的新應用

- 市場限制

- 波動性甲醇原料價格

- 與羰基化反應相關的二氧化碳和揮發性有機化合物排放法規

- 針對中國產品的反傾銷措施

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 導數

- 醋酸乙烯單體(VAM)

- 純對苯二甲酸(PTA)

- 乙酸乙酯

- 乙酸酐

- 其他衍生產品

- 透過製造程序

- 甲醇羰基化

- 乙醛氧化

- 環氧乙烷

- 生物基發酵

- 透過使用

- 塑膠和聚合物

- 食品/飲料

- 黏合劑、油漆和塗料

- 紡織業

- 醫療保健

- 其他用途

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Celanese Corporation

- Daicel Corporation

- Eastman Chemical Company

- Gujarat Narmada Valley Fertilizers & Chemicals Limited

- INEOS

- Jiangsu SOPO(Group)Co., Ltd.

- Kingboard Holdings Ltd.

- LyondellBasell Industries Holdings BV

- Mitsubishi Chemical Group Corporation

- PetroChina Company Limited

- SABIC

- Sekab

- Shandong Hualu Hengsheng Group Co., Ltd.

- Shanghai Huayi Fine Chemical Co., Ltd

- Sipchem Company

- Tanfac Industries Ltd

- Wacker Chemie AG

- Yankuang Energy Group Company Limited

第7章 市場機會與未來展望

Acetic Acid market size in 2026 is estimated at 20.48 Million tons, growing from 2025 value of 19.58 Million tons with 2031 projections showing 25.62 Million tons, growing at 4.58% CAGR over 2026-2031.

Robust demand across vinyl acetate monomer, purified terephthalic acid, and emerging battery-grade electrolytes anchors growth. Scale-based cost efficiency, rising sustainability mandates, and downstream integration strengthen producer margins. Asia-Pacific dominance persists as polyester, adhesive, and solvent consumption remains high. Investment in low-carbon production technologies and carbon-capture projects is accelerating as regulatory scrutiny tightens, further shaping competitive dynamics in the acetic acid market.

Global Acetic Acid Market Trends and Insights

Increasing Demand for Vinyl Acetate Monomer

Water-based adhesive and coating formulations rely on vinyl acetate monomer for superior bonding strength and flexibility. These attributes meet stricter environmental rules on solvent emissions, especially in construction and automotive production. Asia-Pacific accounts for more than 60% of global VAM consumption, encouraging integrated acetyl chain investments near demand hubs. Celanese started a new vinyl acetate ethylene unit in Nanjing that adds 70,000 tons of capacity, illustrating the proximity advantage.

Rising Consumption of Purified Terephthalic Acid

Polyester growth in textiles and packaging drives higher purified terephthalic acid volumes, sustaining acetic acid usage as solvent and reaction medium. Sinopec's single-train PTA plant in Jiangsu, with 3 million tons annual capacity, shows the scale now typical in Asia-Pacific production. Larger units improve acetic acid utilization efficiency yet keep total demand rising. Regional supply imbalances, such as India's premium PTA pricing, allow flexible suppliers to capture arbitrage gains.

Carbonylation-Related CO2/VOC Emission Regulations

North American and European regulators now target emissions from carbonylation reactors and distillation steps. The EPA's control guidelines and Canada's Environmental Protection Act both tighten emission thresholds. Compliance requires investments in carbon capture and advanced scrubbers, favoring larger producers with available capital. Celanese's Clear Lake retrofit captures CO2 for methanol synthesis, setting a benchmark for integrated abatement.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Acetate-Ester Solvents in High-Solids Coatings

- Emerging Use in Li-Ion Battery Electrolyte Additives

- Anti-Dumping Actions Against Chinese Exports

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vinyl acetate monomer held 27.25% acetic acid market share in 2025 as construction and automotive sectors favored water-based adhesives. Polyvinyl acetate and ethylene-vinyl acetate copolymers secure growth by replacing solvent-borne systems that fail new emission norms. Celanese and INEOS leverage backward integration to keep costs low and service captive downstream units.

Purified terephthalic acid, growing at a 4.95% CAGR, benefits from polyester expansion in apparel and bottle resin. Ethyl acetate maintains steady use in pharmaceutical and coating solvents, while acetic anhydride demonstrates resilience in pharmaceutical acetylation despite cigarette filter decline. Derivative demand patterns reflect producer strategies that capture value along the acetyl chain. Integrated operators convert commodity acetic acid volumes into higher-margin downstream products, protecting earnings during feedstock price swings.

The Acetic Acid Report is Segmented by Derivative (Vinyl Acetate Monomer, Purified Terephthalic Acid, Ethyl Acetate, and More), Production Route (Methanol Carbonylation, Acetaldehyde Oxidation, and More), Application (Plastics and Polymers, Food and Beverage, Adhesives Paints and Coatings, Textile, Medical, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific dominated with 68.10% acetic acid market share in 2025 and is forecast to grow at 5.05% CAGR through 2031. China alone controls about 55% of global capacity, granting scale economies and regional pricing influence. The region's large polyester and adhesive industries stabilize volume demand even during external economic swings.

North America exhibits mature consumption yet notable investment in low-carbon production. Celanese's 1.3 million ton Clear Lake upgrade integrates carbon capture and feedstock security to ensure competitiveness. Regulatory focus on emission reduction promotes bio-based projects across the United States and Canada, potentially shifting a portion of import volumes to domestic supply.

Europe prioritizes circular economy principles and stringent lifecycle assessments. Producers with verified low-carbon footprints gain procurement preference among automotive and packaging customers. Emerging Middle East and Africa capacity aims to leverage competitive feedstock costs, yet infrastructure and regulatory frameworks remain in development. Latin America experiences steady acetic acid market growth tied to polyester bottle resin and food preservative applications, but scale is limited compared with Asia-Pacific production.

- Celanese Corporation

- Daicel Corporation

- Eastman Chemical Company

- Gujarat Narmada Valley Fertilizers & Chemicals Limited

- INEOS

- Jiangsu SOPO (Group) Co., Ltd.

- Kingboard Holdings Ltd.

- LyondellBasell Industries Holdings B.V.

- Mitsubishi Chemical Group Corporation

- PetroChina Company Limited

- SABIC

- Sekab

- Shandong Hualu Hengsheng Group Co., Ltd.

- Shanghai Huayi Fine Chemical Co., Ltd

- Sipchem Company

- Tanfac Industries Ltd

- Wacker Chemie AG

- Yankuang Energy Group Company Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Vinyl Acetate Monomer (VAM)

- 4.2.2 Rising Consumption of Purified Terephthalic Acid (PTA)

- 4.2.3 Expansion of Acetate-Ester Solvents in High-Solids Coatings

- 4.2.4 Bio-Based Acetic Acid Adoption Under Net-Zero Mandates

- 4.2.5 Emerging Use in Li-Ion Battery Electrolyte Additives

- 4.3 Market Restraints

- 4.3.1 Volatile Methanol Feedstock Pricing

- 4.3.2 Carbonylation-Related CO?/VOC Emission Regulations

- 4.3.3 Anti-Dumping Actions Against Chinese Exports

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Derivative

- 5.1.1 Vinyl Acetate Monomer (VAM)

- 5.1.2 Purified Terephthalic Acid (PTA)

- 5.1.3 Ethyl Acetate

- 5.1.4 Acetic Anhydride

- 5.1.5 Other Derivatives

- 5.2 By Production Route

- 5.2.1 Methanol Carbonylation

- 5.2.2 Acetaldehyde Oxidation

- 5.2.3 Ethylene Oxidation

- 5.2.4 Bio-based Fermentation

- 5.3 By Application

- 5.3.1 Plastics and Polymers

- 5.3.2 Food and Beverage

- 5.3.3 Adhesives, Paints and Coatings

- 5.3.4 Textile

- 5.3.5 Medical

- 5.3.6 Other Applications

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/ Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Celanese Corporation

- 6.4.2 Daicel Corporation

- 6.4.3 Eastman Chemical Company

- 6.4.4 Gujarat Narmada Valley Fertilizers & Chemicals Limited

- 6.4.5 INEOS

- 6.4.6 Jiangsu SOPO (Group) Co., Ltd.

- 6.4.7 Kingboard Holdings Ltd.

- 6.4.8 LyondellBasell Industries Holdings B.V.

- 6.4.9 Mitsubishi Chemical Group Corporation

- 6.4.10 PetroChina Company Limited

- 6.4.11 SABIC

- 6.4.12 Sekab

- 6.4.13 Shandong Hualu Hengsheng Group Co., Ltd.

- 6.4.14 Shanghai Huayi Fine Chemical Co., Ltd

- 6.4.15 Sipchem Company

- 6.4.16 Tanfac Industries Ltd

- 6.4.17 Wacker Chemie AG

- 6.4.18 Yankuang Energy Group Company Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment

醋酸市場規模、佔有率、趨勢和預測:按應用、最終用途和地區分類,2026-2034年

醋酸市場規模、佔有率、趨勢和預測:按應用、最終用途和地區分類,2026-2034年 醋酸市場:2026-2032年全球市場預測(依等級、生產流程、形態、通路及最終用戶分類)

醋酸市場:2026-2032年全球市場預測(依等級、生產流程、形態、通路及最終用戶分類) 2026年全球乙二胺四乙酸(EDTA)市場研究報告

2026年全球乙二胺四乙酸(EDTA)市場研究報告 醋酸市場規模、佔有率和趨勢分析報告:按應用、地區和細分市場預測(2026-2033 年)

醋酸市場規模、佔有率和趨勢分析報告:按應用、地區和細分市場預測(2026-2033 年) 醋酸市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年

醋酸市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年 醋酸市場:按應用和地區分類

醋酸市場:按應用和地區分類 醋酸市場規模、佔有率及成長分析(依生產路線、應用、最終用途產業及地區分類)-2026-2033年產業預測氯乙酸市場:依產品類型和地區分類

醋酸市場規模、佔有率及成長分析(依生產路線、應用、最終用途產業及地區分類)-2026-2033年產業預測氯乙酸市場:依產品類型和地區分類 2026年全球醋酸市場報告

2026年全球醋酸市場報告 醋酸市場 - 全球產業規模、佔有率、趨勢、機會及預測(按應用、終端用戶產業、地區及競爭格局分類,2021-2031年)

醋酸市場 - 全球產業規模、佔有率、趨勢、機會及預測(按應用、終端用戶產業、地區及競爭格局分類,2021-2031年)