|

市場調查報告書

商品編碼

1939086

汽車電力電子:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Automotive Power Electronics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

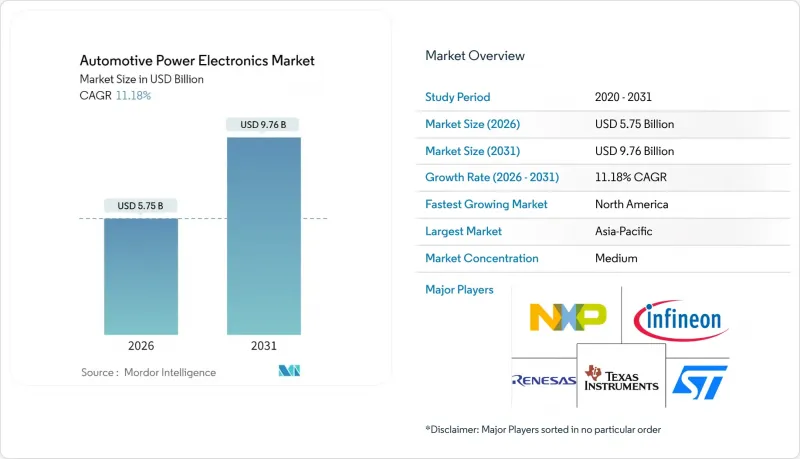

汽車電力電子市場預計將從 2025 年的 51.7 億美元成長到 2026 年的 57.5 億美元,並預計在 2031 年達到 97.6 億美元,2026 年至 2031 年的複合年成長率為 11.18%。

這一成長與全球汽車保有量加速電氣化、向800V電氣架構的過渡以及為提高能源效率和熱性能而日益廣泛應用的寬能能隙半導體相吻合。需求主要集中在牽引逆變器、車載充電器和DC-DC轉換器上,這些產品構成了現代電池式電動車的電子基礎。

汽車電力電子市場全球趨勢及展望

電動車普及率的快速成長和充電基礎設施建設的進步

電動車的加速普及將對電力電子需求產生倍增效應,因為每輛電動車所需的半導體元件數量是傳統汽車的三到五倍。預計2023年,中國電動車市場滲透率將達到35.7%,不同地區由於充電基礎設施的可用性和消費者偏好不同,對電力電子的需求也各不相同。向150kW及以上直流快速充電的過渡將需要能夠處理高電流密度並保持熱穩定性的先進功率模組,這為功率轉換、保護和溫度控管整合解決方案的供應商創造了機會。

加強全球汽車排放氣體法規

主要汽車市場的法規結構正從傳統的廢氣排放氣體擴展到涵蓋全生命週期碳排放和能源效率要求。歐盟的歐盟7排放標準(將於2025年生效)對氮氧化物和顆粒物排放設定了嚴格的限制,並強制要求幾乎所有車型採用混合動力或純電動動力傳動系統。中國的雙軌制和加州的先進清潔汽車II法規也施加了類似的合規壓力,同時也為電力電子系統設定了最低能源效率標準,並鼓勵寬能能隙半導體而非傳統的矽裝置。這些法規迫使汽車製造商優先考慮能夠最大限度提高能量轉換效率的電力電子解決方案,加速了碳化矽(SiC)和氮化鎵(GaN)技術的應用,儘管它們的初始成本較高。法規的影響不僅限於動力傳動系統,還包括溫度控管系統、照明和輔助動力單元(APU),從而擴大了汽車電力電子供應商的潛在市場。

高功率密度下的溫度控管挑戰

對緊湊輕巧的電力電子模組的需求造成了散熱瓶頸,限制了其性能和可靠性,尤其是在驅動逆變器應用中功率密度超過 50 kW/L 時。對於工作頻率高於 20 kHz 的 800 V 系統,傳統的風冷方案已無法滿足需求,需要採用液冷系統,這會增加車輛架構的成本、複雜性和潛在的故障模式。先進的導熱界面材料和嵌入式冷卻通道可將散熱效率提高 30%–40%。然而,這些解決方案需要大量的工程投資和製造流程的改進,從而導致開發週期延長和認證成本增加。在商用車和摩托車領域,由於空間限制和成本敏感性,溫度控管的挑戰更為嚴峻,這可能會延緩這些領域向更高電壓架構的過渡。

細分市場分析

到2025年,功率模組將佔汽車電力電子市場46.52%的佔有率,這反映出汽車製造商傾向於選擇將多個半導體裝置、閘極驅動器和保護電路整合到散熱最佳化封裝中的解決方案。隨著OEM廠商尋求簡化組裝並增強空間受限應用中的溫度控管,產業向更高整合度的轉變推動了這個細分市場的發展。在800V牽引逆變器應用中,SiC功率模組憑藉其卓越的效率和散熱性能,預計將在2031年之前以20.98%的複合年成長率實現顯著成長。功率IC在車身電子設備和輔助系統中將保持穩定的需求,而分立元件將用於需要客製化散熱解決方案和極高可靠性的特殊應用。

整合化趨勢已超越傳統界限,供應商正在開發整合微控制器、電流感測和診斷功能的智慧電源模組,以實現預測性維護和系統最佳化。這種向「智慧」電源模組的演進為供應商提供了差異化機遇,同時也滿足了汽車製造商對降低系統複雜性和提高功能安全合規性的需求。 ISO 26262認證要求更加強調模組化方法以及可驗證的故障隔離和診斷覆蓋範圍,這進一步推動了電源模組市場在所有車型和驅動配置中的成長。

到2025年,動力傳動系統系統將佔汽車電力電子市場62.04%的佔有率,預計到2031年將保持18.75%的強勁複合年成長率,因為電氣化將傳統的機械系統轉變為電子控制的電力轉換網路。該細分市場包括牽引逆變器、直流-直流轉換器、車載充電器和電池管理系統,這些組件共同決定了車輛的續航里程、充電速度和能源效率。車身電子應用(例如照明、空調和資訊娛樂系統)是一個規模雖小但穩定的市場細分,受益於LED技術的應用和每輛車電子元件數量的增加。由於高級駕駛輔助系統(ADAS)的廣泛應用和日益成長的網路安全需求,安全電子正在成為一個高成長的細分市場,需要專門的電源管理解決方案。

動力傳動系統產業的領先地位反映了能量轉換方式從機械能向電能的根本性轉變,電力電子效率直接影響車輛性能和消費者接受度。新一代驅動逆變器透過先進的溫度控管技術(包括嵌入式冷卻和相變材料)實現了超過100kW/L的功率密度,而寬能能隙半導體與矽基解決方案相比,可將開關損耗降低60-80%。這種技術進步為能夠提供整合式動力傳動系統總成解決方案的供應商創造了機遇,這些解決方案可以最佳化整個子系統而非單一組件。

區域分析

到2025年,亞太地區汽車電力電子市場佔有率將達到42.35%,這主要得益於中國作為全球最大電動車市場的地位以及日本在寬能能隙半導體製造領域的領先地位。從原料到成品車的一體化供應鏈,使得電力電子產品的生產能夠快速擴張,同時保持成本競爭力。韓國專注於高階電動車平台,而印度二輪車電動化進程的加速,都催生了對量產型和專用型電力電子產品的需求。該地區的製造生態系統受益於汽車製造商和半導體晶圓代工廠之間建立的穩固合作關係,從而促進了碳化矽功率模組和整合域控制器等下一代技術的快速應用。

預計到2031年,北美將以19.53%的複合年成長率實現最高成長,這主要得益於《通膨控制法案》中3700億美元的清潔能源計劃以及汽車製造商在國內生產電動車的努力。該地區對800V架構和快速充電基礎設施的重視,正在創造對寬能能隙半導體的高階需求。同時,製造業回流計畫旨在建立關鍵電力電子元件的國內供應鏈。加拿大的採礦業為電力電子製造提供了必要的原料。相較之下,墨西哥的汽車製造地為尋求降低供應鏈風險的北美原始設備製造商(OEM)提供了經濟高效的組裝能力。

歐洲在高階汽車領域保持強大的地位和監管主導。歐盟的「綠色交易」推動了積極的電氣化目標和排放標準,從而促進了先進電力電子解決方案的發展。該地區在功能安全標準和環境法規方面的專業知識使其在全球市場中擁有競爭優勢。同時,現有汽車供應商正利用與整車製造商(OEM)的合作關係,在轉型為電動過程中獲取價值。德國的工業基礎和法國的半導體技術為該地區的電力電子發展提供了支持,而北歐國家的可再生能源資源則有助於實現符合汽車製造商碳中和目標的永續製造流程。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電動車日益普及以及充電基礎建設的進步

- 加強全球汽車排放氣體法規

- 對先進ADAS和安全電子產品的需求不斷成長

- 原始設備製造商轉向 800V 電氣架構

- 一級供應商快速採用SiC/GaN功率元件設計

- 將逆變器功能整合到網域控制器中

- 市場限制

- 高功率密度下的溫度控管挑戰

- 半導體供應週期性受限

- 寬能能隙材料的初始成本較高

- 高壓元件缺乏統一的全球標準

- 價值/價值鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模及成長預測(價值(美元))

- 依設備類型

- 功率積體電路

- 電源模組

- 分立元件

- 透過使用

- 動力傳動系統系統

- 人體電子系統

- 安全電子設備

- 按車輛類型

- 搭乘用車

- 輕型商用車

- 摩托車

- 中型和重型商用車輛

- 按驅動類型

- 內燃機車輛

- 混合動力電動車(HEV)

- 電池式電動車(BEV)

- 按組件

- 電源模組

- 轉換器

- 控制器

- 轉變

- 電池管理系統

- 車用充電器

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 土耳其

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Infineon Technologies AG

- Semiconductor Components Industries, LLC(onsemi)

- STMicroelectronics NV

- Renesas Electronics Corporation

- ROHM Co., Ltd.

- Mitsubishi Electric Corporation

- NXP Semiconductors NV

- Texas Instruments Incorporated

- Robert Bosch GmbH(Semiconductors for Mobility)

- Vishay Intertechnology, Inc.

- Toshiba Electronic Devices & Storage Corporation

- Littelfuse Inc.

- Analog Devices, Inc.

- Semikron Danfoss International GmbH

- Astemo, Ltd.

- Valeo SA

- Continental AG

- Wolfspeed, Inc.

- StarPower Semiconductor Ltd.

第7章 市場機會與未來展望

The automotive power electronics market is expected to grow from USD 5.17 billion in 2025 to USD 5.75 billion in 2026 and is forecast to reach USD 9.76 billion by 2031 at 11.18% CAGR over 2026-2031.

This growth aligns with the accelerating electrification of global vehicle fleets, the migration to 800V electrical architectures, and the rising use of wide-bandgap semiconductors that enhance energy efficiency and thermal performance. Demand is concentrated in traction inverters, on-board chargers, and DC-DC converters, which form the electronic backbone of modern battery-electric vehicles.

Global Automotive Power Electronics Market Trends and Insights

Surge in EV Adoption and Charging Infrastructure Build-Out

The acceleration of electric vehicle adoption creates a multiplicative effect on power electronics demand, as each EV requires 3-5 times more semiconductor content than conventional vehicles. China's EV market reached 35.7% penetration in 2023, with each region driving distinct power electronics requirements based on charging infrastructure capabilities and consumer preferences. The shift toward 150 kW+ DC fast charging necessitates advanced power modules capable of handling higher current densities while maintaining thermal stability, creating opportunities for suppliers who can deliver integrated solutions that combine power conversion, protection, and thermal management functions.

Stricter Global Vehicle-Emission Regulations

Regulatory frameworks across major automotive markets have intensified beyond traditional tailpipe emissions to encompass lifecycle carbon footprints and energy efficiency mandates. The European Union's Euro 7 standards, practical from 2025, impose stringent limits on nitrogen oxides and particulate matter that effectively mandate hybrid or electric powertrains for most vehicle segments. China's dual-credit system and California's Advanced Clean Cars II regulation create similar compliance pressures, while also establishing minimum efficiency thresholds for power electronics systems that favor wide-bandgap semiconductors over traditional silicon devices. These regulations drive automakers to prioritize power electronics solutions that maximize energy conversion efficiency, leading to accelerated adoption of SiC and GaN technologies despite their higher initial costs. The regulatory influence extends beyond powertrains to encompass thermal management systems, lighting, and auxiliary power units, broadening the addressable market for automotive power electronics suppliers.

Thermal-Management Challenges at Higher Power Densities

The push toward compact, lightweight power electronics modules creates thermal bottlenecks that limit performance and reliability, particularly as power densities exceed 50kW/L in traction inverter applications. Traditional air-cooling solutions prove inadequate for 800V systems operating at switching frequencies above 20kHz, necessitating liquid cooling systems that add cost, complexity, and potential failure modes to vehicle architectures. Advanced thermal interface materials and embedded cooling channels can improve heat dissipation by 30-40%. However, these solutions require significant engineering investment and manufacturing process changes, which extend development timelines and increase qualification costs. The thermal management challenge becomes more acute in commercial vehicles and two-wheelers, where space constraints and cost sensitivity limit the adoption of sophisticated cooling solutions, potentially slowing the transition to higher-voltage architectures in these segments.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Advanced ADAS and Safety Electronics

- OEM Migration to 800V Electrical Architectures

- Cyclical Semiconductor Supply Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Power modules captured 46.52% of the automotive power electronics market share in 2025, reflecting automakers' preference for integrated solutions that combine multiple semiconductor devices, gate drivers, and protection circuits in thermally optimized packages. The segment benefits from the industry's shift toward higher integration levels, as OEMs seek to simplify assembly and enhance thermal management in space-constrained applications. SiC power modules are expected to demonstrate exceptional growth, with a 20.98% CAGR through 2031, driven by their superior efficiency and thermal performance in 800V traction inverter applications. Power ICs maintain steady demand in body electronics and auxiliary systems, while discrete devices serve specialized applications that require custom thermal solutions or extreme reliability.

The integration trend extends beyond traditional boundaries, with suppliers developing intelligent power modules that incorporate microcontrollers, current sensing, and diagnostic capabilities to enable predictive maintenance and system optimization. This evolution toward "smart" power modules creates differentiation opportunities for suppliers while addressing automakers' demands for reduced system complexity and improved functional safety compliance. ISO 26262 certification requirements are increasingly favoring modular approaches that can demonstrate fault isolation and diagnostic coverage, further supporting the growth trajectory of the power module segment across all vehicle types and drive configurations.

Powertrain systems command 62.04% of the automotive power electronics market share in 2025. They are expected to maintain a robust 18.75% CAGR growth through 2031, as electrification transforms traditional mechanical systems into electronically controlled power conversion networks. The segment encompasses traction inverters, DC-DC converters, onboard chargers, and battery management systems that collectively determine vehicle range, charging speed, and energy efficiency. Body electronics applications, including lighting, climate control, and infotainment systems, represent a smaller but stable market segment that benefits from the adoption of LED technology and the increasing electronic content per vehicle. Safety and security electronics emerge as a high-growth niche, driven by the proliferation of ADAS and cybersecurity requirements that demand specialized power management solutions.

The powertrain segment's dominance reflects the fundamental shift from mechanical to electrical energy conversion, where power electronics efficiency directly impacts vehicle performance and consumer acceptance. Advanced thermal management techniques, including embedded cooling and phase-change materials, enable power densities exceeding 100 kW/L in next-generation traction inverters. Meanwhile, wide-bandgap semiconductors reduce switching losses by 60-80% compared to silicon-based solutions. This technological evolution creates opportunities for suppliers who can deliver integrated powertrain solutions that optimize across multiple subsystems rather than individual components.

The Automotive Power Electronics Market Report is Segmented by Device Type (Power ICs, Power Modules, Discrete Devices), Application (Powertrain Systems, Body Electronics, Safety and Security Electronics), Vehicle Type (Passenger Cars and More), Drive Type (ICE Vehicles and More), Component (Power Modules and More), and Geography (North America and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commands 42.35% of the automotive power electronics market share in 2025, driven by China's position as the world's largest EV market and Japan's leadership in wide-bandgap semiconductor manufacturing. The region's integrated supply chain, spanning from raw materials to finished vehicles, enables rapid scaling of power electronics production while maintaining cost competitiveness. South Korea's focus on premium EV platforms and India's emerging two-wheeler electrification create diverse demand patterns that support both high-volume and specialized power electronics applications. The region's manufacturing ecosystem benefits from established relationships between automotive OEMs and semiconductor foundries, facilitating the rapid deployment of next-generation technologies like SiC power modules and integrated domain controllers.

North America exhibits the fastest regional growth at 19.53% CAGR through 2031, supported by the Inflation Reduction Act's USD 370 billion in clean energy incentives and automakers' commitments to domestic EV production. The region's focus on 800V architectures and fast-charging infrastructure creates premium demand for wide-bandgap semiconductors, while reshoring initiatives aim to establish domestic supply chains for critical power electronics components. Canada's mining sector provides access to essential materials for the manufacturing of power electronics. In contrast, Mexico's automotive manufacturing base offers cost-effective assembly capabilities for North American OEMs seeking to reduce supply chain risks.

Europe maintains a strong position in premium vehicle segments and regulatory leadership, with the European Union's Green Deal driving aggressive electrification targets and emissions standards that favor advanced power electronics solutions. The region's expertise in functional safety standards and environmental regulations creates competitive advantages in global markets. At the same time, established automotive suppliers leverage their OEM relationships to capture value in the transition to electric mobility. Germany's industrial base and France's semiconductor capabilities support regional power electronics development, while Nordic countries' renewable energy resources enable sustainable manufacturing processes that align with automakers' carbon neutrality commitments.

- Infineon Technologies AG

- Semiconductor Components Industries, LLC (onsemi)

- STMicroelectronics NV

- Renesas Electronics Corporation

- ROHM Co., Ltd.

- Mitsubishi Electric Corporation

- NXP Semiconductors N.V.

- Texas Instruments Incorporated

- Robert Bosch GmbH (Semiconductors for Mobility)

- Vishay Intertechnology, Inc.

- Toshiba Electronic Devices & Storage Corporation

- Littelfuse Inc.

- Analog Devices, Inc.

- Semikron Danfoss International GmbH

- Astemo, Ltd.

- Valeo SA

- Continental AG

- Wolfspeed, Inc.

- StarPower Semiconductor Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in EV Adoption and Charging Infrastructure Build-Out

- 4.2.2 Stricter Global Vehicle-Emission Regulations

- 4.2.3 Rising Demand for Advanced ADAS and Safety Electronics

- 4.2.4 OEM Migration to 800 V Electrical Architectures

- 4.2.5 Rapid Design-In of SiC/GaN Power Devices by Tier-1 Suppliers

- 4.2.6 Integration of Inverter Functions Into Domain Controllers

- 4.3 Market Restraints

- 4.3.1 Thermal-Management Challenges at Higher Power Densities

- 4.3.2 Cyclical Semiconductor Supply Constraints

- 4.3.3 High Upfront Cost of Wide-Band-Gap Materials

- 4.3.4 Absence of Unified Global Standards for High-Voltage Components

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Device Type

- 5.1.1 Power ICs

- 5.1.2 Power Modules

- 5.1.3 Discrete Devices

- 5.2 By Application

- 5.2.1 Powertrain Systems

- 5.2.2 Body Electronics

- 5.2.3 Safety and Security Electronics

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Two-Wheelers

- 5.3.4 Medium and Heavy-Duty Commercial Vehicles

- 5.4 By Drive Type

- 5.4.1 Internal Combustion Engine (ICE) Vehicles

- 5.4.2 Hybrid Electric Vehicles (HEVs)

- 5.4.3 Battery Electric Vehicles (BEVs)

- 5.5 By Component

- 5.5.1 Power Modules

- 5.5.2 Converters

- 5.5.3 Controllers

- 5.5.4 Switches

- 5.5.5 Battery Management Systems

- 5.5.6 On-Board Chargers

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Turkey

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Infineon Technologies AG

- 6.4.2 Semiconductor Components Industries, LLC (onsemi)

- 6.4.3 STMicroelectronics NV

- 6.4.4 Renesas Electronics Corporation

- 6.4.5 ROHM Co., Ltd.

- 6.4.6 Mitsubishi Electric Corporation

- 6.4.7 NXP Semiconductors N.V.

- 6.4.8 Texas Instruments Incorporated

- 6.4.9 Robert Bosch GmbH (Semiconductors for Mobility)

- 6.4.10 Vishay Intertechnology, Inc.

- 6.4.11 Toshiba Electronic Devices & Storage Corporation

- 6.4.12 Littelfuse Inc.

- 6.4.13 Analog Devices, Inc.

- 6.4.14 Semikron Danfoss International GmbH

- 6.4.15 Astemo, Ltd.

- 6.4.16 Valeo SA

- 6.4.17 Continental AG

- 6.4.18 Wolfspeed, Inc.

- 6.4.19 StarPower Semiconductor Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

汽車電力電子市場預測至2034年-全球分析(按組件、裝置類型、車輛類型、動力傳動系統、應用、最終用戶和地區分類)

汽車電力電子市場預測至2034年-全球分析(按組件、裝置類型、車輛類型、動力傳動系統、應用、最終用戶和地區分類) 汽車電力電子市場:按類型、材料、組件、應用、車輛類型、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

汽車電力電子市場:按類型、材料、組件、應用、車輛類型、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 汽車電力電子市場:依技術、冷卻方式、功率等級、產品類型、車輛類型和應用分類-2026-2032年全球市場預測

汽車電力電子市場:依技術、冷卻方式、功率等級、產品類型、車輛類型和應用分類-2026-2032年全球市場預測 電動車電力電子市場分析與預測(至2035年):類型、產品類型、技術、組件、應用、設備、最終用戶、功能、安裝配置、解決方案電動車電力電子及逆變器市場預測至2034年-按組件、車輛類型、技術類型、最終用戶和地區分類的全球分析

電動車電力電子市場分析與預測(至2035年):類型、產品類型、技術、組件、應用、設備、最終用戶、功能、安裝配置、解決方案電動車電力電子及逆變器市場預測至2034年-按組件、車輛類型、技術類型、最終用戶和地區分類的全球分析 2026年全球汽車電力電子市場報告2026年全球電動汽車電力電子市場報告2035年電動車電力電子氮化鎵市場分析與預測:按類型、產品、服務、技術、組件、應用、材料類型、裝置、製程和最終用戶分類汽車電力電子市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材料類型、裝置、最終用戶分類

2026年全球汽車電力電子市場報告2026年全球電動汽車電力電子市場報告2035年電動車電力電子氮化鎵市場分析與預測:按類型、產品、服務、技術、組件、應用、材料類型、裝置、製程和最終用戶分類汽車電力電子市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材料類型、裝置、最終用戶分類 全球汽車電力電子市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球汽車電力電子市場規模、佔有率、趨勢和成長分析報告(2026-2034)