|

市場調查報告書

商品編碼

1939080

水性醇酸塗料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Water-based Alkyd Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

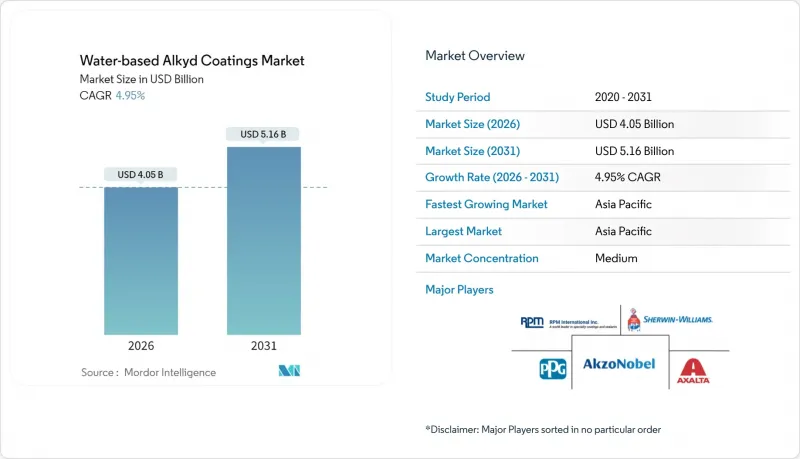

2025年水性醇酸塗料市場價值為38.6億美元,預計2031年將達到51.6億美元,高於2026年的40.5億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 4.95%。

這一成長得益於更嚴格的環境法規、建設產業的復甦以及持續的產品創新。製造商正致力於研發低揮發性有機化合物(VOC)配方和無鈷乾燥系統,以滿足全球日益嚴格的法規要求。亞太地區加速工業化進程以及政府對溶劑排放的嚴厲打擊,推動了該地區的消費成長。北美和歐洲的建築翻新週期支撐了基礎需求,而汽車修補漆等快速成長的細分市場則受益於更短的加工時間和更低的能源成本。策略整合和垂直一體化幫助主要品牌保持了定價權,但生物基乳液為尋求差異化的新參與企業提供了機會。

全球水性醇酸塗料市場趨勢及洞察

從溶劑型技術轉向水性技術

全球法規正推動塗料系統從溶劑型轉變為水性醇酸樹脂。 2018年上海實施的溶劑型建築塗料禁令促使中國建設產業在全國推廣使用水性醇酸樹脂,改變了原料流動,並對區域供應鏈產生了影響。美國環保署(EPA)計劃於2025年修訂其氣霧劑塗料VOC排放法規,這將進一步刺激對低反應性材料的需求。像Perstorp這樣的供應商正在展示新一代乳化劑,這些乳化劑能夠在不影響塗料硬度或光澤度的前提下,將VOC排放降至接近零。能夠兼顧法規合規性和傳統表現的企業將獲得先發優勢,並增強客戶忠誠度。

建築業復甦與重新粉刷週期

由於老舊住宅存量以及DIY的成本效益,住宅重新粉刷的需求仍然強勁,抵消了新建房屋數量的放緩。據剪切機-Williams)稱,其專業通路已占美國塗料銷售量的63%,這充分體現了其專業經銷商網路的價值。亞洲塗料公司(Asian Paints)透過一項48億美元的計劃,將其裝飾塗料產能提高了一倍以上,以響應印度的「人人有房」計劃。這些趨勢表明,即使GDP成長幅度不大,也能透過重新粉刷的需求確保穩定的銷售量,從而減輕經濟週期的影響。

與溶劑型塗料相比:乾燥和固化時間更長

高濕度會減緩水分蒸發,導致工期延長和人事費用增加。 Polint 的速乾型 DTM 醇酸乳液可加快施工速度,但仍需最佳化乾燥劑配方。配方師正致力於研發鈷替代技術,以降低毒性並保持乾燥速度。儘管近年來性能差距正在縮小,但赤道氣候地區的施工人員仍然傾向於選擇溶劑型塗料用於外牆施工。

細分市場分析

預計到2025年,建築塗料將佔水性醇酸塗料市場規模的46.02%,這反映了持續的翻新週期以及住宅室內裝修法規主導的需求。配方師正在研發適用於生活空間的低氣味塗料,其揮發性有機化合物(VOC)含量限制已降至50克/公升。在亞洲塗料及其區域競爭對手的主導,亞洲地區的產能擴張與城市住宅規劃保持同步。增強的耐久性,例如不泛黃的塗層,提升了乙烯基丙烯酸塗料的價值提案。

汽車修補塗料產業將維持最高的成長率,到2031年複合年成長率將達到6.28%。阿克蘇諾貝爾的Sikkens Autowave Optima可降低噴漆室能耗60%,並將塗料層數限制在1.5層,進而提高工廠生產效率並降低碳排放強度。工業金屬、木材和船舶產業在水性醇酸樹脂乳液技術達到ISO 12944防腐蝕標準後,開始採用水性醇酸樹脂。家具製造商歡迎符合企業永續性目標的生物基產品,而機械和船舶塗料則為需要先進阻隔添加劑的專業人士提供了機會。

水性醇酸塗料市場報告按應用領域(建築、防護/工業金屬、木器塗料等)、終端用戶行業(建築與基礎設施、工業OEM、汽車與交通運輸、船舶與海洋工程等)以及地區(亞太地區、北美、歐洲、南美、中東和非洲)進行細分。市場預測以美元計價。

區域分析

預計到2025年,亞太地區將佔全球營收的41.05%,並在2031年之前以5.45%的複合年成長率成長。中國上海等城市實施的溶劑禁令正在推動符合標準的水性醇酸樹脂的全面轉型。國家標準將鉛含量限制在90毫克/公斤以內,進一步強化了這項轉型,為國內製造商提供了技術要求和出口優勢。強勁的建築需求、不斷成長的汽車保有量以及消費者意識的提高,都在支撐多個細分市場的需求。

北美憑藉著完善的分銷網路和嚴格的環境法規,保持著強勁的市場地位。加州50克/公升的污染物排放限值推動了研發,而專業的汽車修補服務也帶動了市場需求。美國製造商正透過利用管理式銷售管道和自有品牌協議來最佳化利潤率。在汽車修補領域,隨著鈑金噴漆店意識到縮短製程時間的優勢,他們正迅速採用這項技術。

歐洲持續保持創新活力,生物基乳化劑和無鈷乾燥劑已較早商業化。儘管成熟的消費結構限制了銷售成長,但歷史建築的維修和節能維修支撐了穩定的需求。歐盟綠色交易的獎勵促進了公共部門採購低揮發性有機化合物(VOC)塗料,並給予符合標準的供應商優先競標權。

隨著城市基礎設施的擴張,南美洲的需求正在逐步成長,尤其是在巴西,世界盃前的設施翻新工程更是推動了這一成長。儘管各國監管力道不盡相同,但日益增強的健康意識正促使買家轉向水基系統。在中東和非洲,市場存在著早期發展機遇,尤其是在高階商業建築和油氣基礎設施領域,這些領域需要兼具耐腐蝕性和合規性的解決方案。價格敏感度和極端氣候限制了轉換率,凸顯了開發濕度最佳化配方和本地化混合的必要性。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 從溶劑型技術轉向水性技術

- 建築業復甦與重新粉刷週期

- 全球加強對揮發性有機化合物(VOC)和有害空氣污染物(HAP)的監管

- 對低氣味內牆塗料的偏好

- 生物基醇酸乳液達到商業化規模

- 市場限制

- 與溶劑型塗料相比,乾燥和固化時間更長。

- 新興經濟體的價格敏感性

- 濕度導致的耐候性受限

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 透過使用

- 建築學

- 防護/工業金屬

- 木器漆

- 汽車修補漆

- 其他(船舶、機械)

- 按最終用戶行業分類

- 建築和基礎設施

- 工業OEM

- 汽車和運輸設備

- 海洋/近海

- 家具和配件

- 其他

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Akzo Nobel NV

- Axalta Coating Systems, LLC

- Benjamin Moore & Co.

- Brillux GmbH & Co. KG

- Caparol Paints

- Cloverdale Paint Inc.

- Hempel A/S

- Jotun

- Kansai Paint Co.,Ltd.

- NATIONAL PAINTS FACTORIES CO. LTD.

- NIPSEA Group

- PPG Industries Inc.

- RPM International Inc.

- The Sherwin-Williams Company

- Tikkurila

第7章 市場機會與未來展望

The Water-based Alkyd Coatings Market was valued at USD 3.86 billion in 2025 and estimated to grow from USD 4.05 billion in 2026 to reach USD 5.16 billion by 2031, at a CAGR of 4.95% during the forecast period (2026-2031).

Stronger environmental compliance rules, a recovering construction sector, and steady product innovation underpin this growth. Manufacturers focus on low-VOC formulations and cobalt-free drying systems to satisfy tightening global regulations. Asia-Pacific dominates consumption, helped by accelerated industrialization and government crackdowns on solvent emissions. Architectural repaint cycles in North America and Europe sustain baseline demand, while fast-growth niches such as automotive refinish benefit from shorter process times and lower energy costs. Strategic consolidation and vertical integration give leading brands pricing power, yet bio-based emulsions open doors for differentiated challengers.

Global Water-based Alkyd Coatings Market Trends and Insights

Shift from Solvent- to Water-based Technology

Global mandates catalyze the conversion from solvent systems to water-based alkyds. Shanghai's 2018 ban on solvent architectural paints triggered nationwide adoption across Chinese construction, altering raw-material flows and influencing regional supply chains. The U.S. EPA's 2025 update of aerosol-coating VOC rules further boosts demand for less reactive ingredients. Suppliers such as Perstorp showcase next-generation emulsifiers that allow near-zero VOC performance without sacrificing hardness or gloss. Firms able to balance compliance with legacy performance secure early mover premiums and strengthen customer loyalty.

Construction Sector Recovery and Repaint Cycles

Residential repainting remains resilient as aging housing stock and DIY affordability offset slower new builds. Sherwin-Williams reports that its pro-contractor channel already captures 63% of U.S. paint volumes, reinforcing the value of professional networks. Asian Paints more than doubled decorative capacity with a USD 4.8 billion program to serve India's Housing for All initiative. These patterns illustrate that even modest GDP growth can unlock steady volume through repaint demand, cushioning cyclicality.

Longer Drying/Curing Time vs. Solvent Systems

Water slows evaporation under high humidity, lengthening project schedules and raising labor costs. Fast-dry DTM alkyd emulsions from Polynt shorten cycles yet still depend on optimized drier blends. Formulators wrestle with cobalt-replacement to mitigate toxicity while preserving siccative action. Performance gaps narrow each year, but contractors in equatorial climates often default to solvent formulations for exterior work.

Other drivers and restraints analyzed in the detailed report include:

- Tightening Global VOC and HAP Regulations

- Preference for Low-odor Indoor Paints

- Humidity-Driven Weatherability Limitations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Architectural coatings generated 46.02% of the water-based alkyd coatings market size in 2025, reflecting sustained repaint cycles and regulation-driven demand in residential interiors. Formulators deliver low-odor paints suited to occupied spaces and VOC limits as low as 50 g/L. Asian capacity expansion, led by Asian Paints and regional peers, keeps pace with urban housing programs. Longevity improvements such as non-yellowing finishes strengthen value propositions versus vinyl acrylics.

The automotive refinish segment will post the fastest 6.28% CAGR through 2031. AkzoNobel's Sikkens Autowave Optima cuts booth energy 60% and reduces layers to 1.5, enhancing shop throughput and lowering carbon intensity. Industrial metal, wood, and marine niches adopt water-borne alkyds as emulsification technologies hit ISO 12944 corrosion benchmarks. Furniture makers welcome bio-based variants that align with corporate sustainability goals, while machinery and offshore coatings represent specialized opportunities requiring advanced barrier additives.

The Water-Based Alkyd Coatings Report is Segmented by Application (Architectural, Protective/Industrial Metal, Wood Finishes, and More), End-User Industry (Construction and Infrastructure, Industrial OEM, Automotive and Transportation, Marine and Offshore, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 41.05% of global revenue in 2025 and is set to advance at a 5.45% CAGR through 2031. China's solvent bans in cities such as Shanghai prompt wholesale migration to compliant water-based alkyds. National standards capping lead at 90 mg/kg further reinforce the shift, giving domestic producers technical mandates and export leverage. Robust construction, expanding automotive fleets, and rising consumer awareness anchor multi-segment demand.

North America maintains a strong position built on established distribution and stringent environmental codes. California's 50 g/L limit catalyzes research and development, while professional repaint services drive volume. U.S. producers leverage controlled channels and private-label contracts to optimize margins. Rapid adoption in automotive refinish accelerates as bodyshops realize cycle-time reduction.

Europe remains innovation-centric with early commercialization of bio-based emulsions and cobalt-free dryers. Mature consumption moderates volume growth, yet retrofitting of historical buildings and energy-efficient refurbishments sustain steady demand. EU Green Deal incentives encourage public-sector procurement of low-VOC coatings, giving compliant suppliers favored-bidder status.

South America witnesses incremental uptake as urban infrastructure expands, especially in Brazil's pre-World Cup facility renewals. Regulatory enforcement varies by country, but rising health awareness nudges buyers toward water-borne systems. Middle-East and Africa present early-stage opportunities centered on high-end commercial and oil-gas infrastructure needing corrosion-resistant yet compliant solutions. Price sensitivity and climate extremes temper speed of conversion, underlining the need for humidity-optimized formulations and local blending.

- Akzo Nobel N.V.

- Axalta Coating Systems, LLC

- Benjamin Moore & Co.

- Brillux GmbH & Co. KG

- Caparol Paints

- Cloverdale Paint Inc.

- Hempel A/S

- Jotun

- Kansai Paint Co.,Ltd.

- NATIONAL PAINTS FACTORIES CO. LTD.

- NIPSEA Group

- PPG Industries Inc.

- RPM International Inc.

- The Sherwin-Williams Company

- Tikkurila

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift from Solvent to Water-Based Technology

- 4.2.2 Construction Sector Recovery and Repaint Cycles

- 4.2.3 Tightening Global VOC and HAP Regulations

- 4.2.4 Preference for Low-Odor Indoor Paints

- 4.2.5 Bio-Based Alkyd Emulsions Reach Commercial Scale

- 4.3 Market Restraints

- 4.3.1 Longer Drying/Curing Time Vs. Solvent Systems

- 4.3.2 Price Sensitivity in Emerging Economies

- 4.3.3 Humidity-Driven Weatherability Limitations

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Application

- 5.1.1 Architectural

- 5.1.2 Protective/Industrial Metal

- 5.1.3 Wood Finishes

- 5.1.4 Automotive Refinish

- 5.1.5 Others (Marine, Machinery)

- 5.2 By End-User Industry

- 5.2.1 Construction and Infrastructure

- 5.2.2 Industrial OEM

- 5.2.3 Automotive and Transportation

- 5.2.4 Marine and Offshore

- 5.2.5 Furniture and Joinery

- 5.2.6 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)**/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 Axalta Coating Systems, LLC

- 6.4.3 Benjamin Moore & Co.

- 6.4.4 Brillux GmbH & Co. KG

- 6.4.5 Caparol Paints

- 6.4.6 Cloverdale Paint Inc.

- 6.4.7 Hempel A/S

- 6.4.8 Jotun

- 6.4.9 Kansai Paint Co.,Ltd.

- 6.4.10 NATIONAL PAINTS FACTORIES CO. LTD.

- 6.4.11 NIPSEA Group

- 6.4.12 PPG Industries Inc.

- 6.4.13 RPM International Inc.

- 6.4.14 The Sherwin-Williams Company

- 6.4.15 Tikkurila

7 Market Opportunities and Future Outlook

醇酸樹脂市場:依原料、技術、應用和最終用途分類-2026-2032年全球市場預測

醇酸樹脂市場:依原料、技術、應用和最終用途分類-2026-2032年全球市場預測 改質醇酸樹脂市場規模、佔有率和成長分析:按樹脂類型、應用和地區分類-2026-2033年產業預測

改質醇酸樹脂市場規模、佔有率和成長分析:按樹脂類型、應用和地區分類-2026-2033年產業預測 2026年全球醇酸塗料市場報告2026年全球醇酸樹脂市場報告環氧改質丙烯酸酯市場按類型、等級和應用分類,全球預測(2026-2032年)矽基改質樹脂冷媒市場(依產品種類、等級、最終用途產業及銷售管道),全球預測(2026-2032年)

2026年全球醇酸塗料市場報告2026年全球醇酸樹脂市場報告環氧改質丙烯酸酯市場按類型、等級和應用分類,全球預測(2026-2032年)矽基改質樹脂冷媒市場(依產品種類、等級、最終用途產業及銷售管道),全球預測(2026-2032年) 改質環氧樹脂市場規模、佔有率和成長分析(依改質劑類型、應用、終端用戶產業、銷售管道和地區分類)-2026-2033年產業預測

改質環氧樹脂市場規模、佔有率和成長分析(依改質劑類型、應用、終端用戶產業、銷售管道和地區分類)-2026-2033年產業預測 全球醇酸樹脂市場

全球醇酸樹脂市場 改質諾伏勒克環氧樹脂市場報告:趨勢、預測和競爭分析(至 2031 年)醇酸塗料市場報告:趨勢、預測與競爭分析(至2031年)

改質諾伏勒克環氧樹脂市場報告:趨勢、預測和競爭分析(至 2031 年)醇酸塗料市場報告:趨勢、預測與競爭分析(至2031年)