|

市場調查報告書

商品編碼

1939067

生物防治:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Biological Control - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

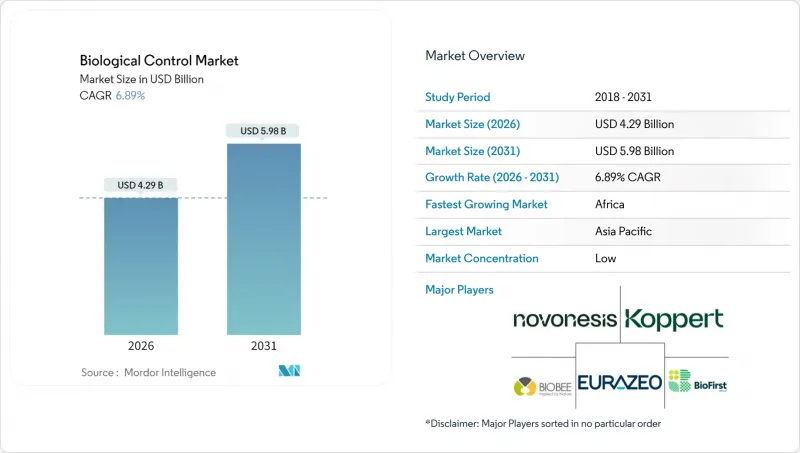

預計到 2025 年,生物防治市場價值將達到 40.1 億美元,到 2031 年將達到 59.8 億美元,高於 2026 年的 42.9 億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 6.89%。

經濟高效的微生物平台、自動化昆蟲養殖以及對傳統農藥日益成長的監管壓力,正在加速生物農藥在主要作物系統中的應用。亞太地區透過廣泛的政府補貼計畫推動全球需求,而非洲積極的糧食舉措則支撐著最快的成長前景。害蟲對合成化學品的快速抗藥性以及消費者對認證有機產品日益成長的偏好,持續推動目標面積的擴大。同時,發酵技術的創新和長效配方的開發正在縮小生物農藥與傳統化學農藥的性能差距,使生物農藥更具競爭力。

全球生物防治市場趨勢與洞察

嚴格禁止使用劇毒合成農藥

監管機構持續淘汰高風險化學品,並推廣生物防治的即時方案。歐盟的「從農場到餐桌」戰略要求到2030年將化學農藥的使用量減少50%,而美國環保署(EPA)已從2024年起註銷了40多種活性成分。巴西和印度也宣布了類似的法規,將於2024年生效,從而擴大了近期可用於生物防治的面積。這些政策措施鼓勵生產者加速產品上市,並促使農民重新思考其作物保護方案,轉向綜合蟲害管理(IPM)框架。

全球對經認證的有機農產品的需求不斷成長

預計到2024年,全球有機食品銷售額將達到1,340億美元,其中美國、德國和中國的年成長率均超過8%。超級市場正在推行零殘留供應商政策,迫使生產商採用生物添加劑以維持認證。有機食品的農場收購價通常比傳統農產品高出20%至40%,這抵消了生物藥品的高成本,並鼓勵其在高價值園藝領域進一步應用。

許多活體產品的商業性保存期限較短。

大多數微生物生物防治劑在冷藏條件下僅能存活兩到四周,這需要高成本的低溫運輸物流系統,嚴重限制了其在電力供應不穩定地區的市場滲透。儘管包封技術和冷凍保護劑配方方面的最新進展在初步研究中顯示出將產品保存期限延長一倍的潛力,但這些改進與合成化學替代品所達到的多年穩定性相比仍相去甚遠。

細分市場分析

2025年,大型生物防治產品在生物防治市場中佔據主導地位,市場佔有率高達97.25%,這得益於數十年來有益昆蟲生產的商業性發展以及服務於全球農業市場的成熟分銷網路。該領域的領先地位源於其在田間應用中久經考驗的有效性,以及農民對捕食性昆蟲和寄生性天敵釋放程序的熟悉程度。其中,對行栽作物系統中土壤害蟲防治尤為有效的昆蟲病原線蟲,在大型生物防治產品類別中佔據最大佔有率。同時,捕食性和寄生性天敵在溫室等可控環境條件下也表現優異。

微生物製劑正成為一股新興的成長引擎,預計2031年將以8.59%的複合年成長率成長。向微生物製劑的轉變反映了發酵過程和製劑穩定性的技術進步,這些進步正在克服傳統細菌和真菌生物防治劑的限制。近期監管部門核准的多菌株微生物產品擴大了其潛在應用範圍,尤其是在高價值園藝作物領域,其精準施用能力使其能夠獲得較高的定價。其他微生物製劑,包括病毒和原生動物製劑,目前仍處於小眾應用領域,但在傳統方法失效的特定害蟲群落中展現出良好的效果。按類型分類的細分市場表明,不同的生物防治機制正根據目標害蟲的生物學特性和作物生產系統,找到最佳的商業性應用途徑。

生物防治市場報告按類型(宏觀生物防治、微觀生物防治)、作物類型(經濟作物、園藝作物、大田作物)和地區(非洲、亞太地區、歐洲、中東、北美、南美)進行細分。市場預測以價值(美元)和數量(公噸)為單位。

區域分析

到2025年,亞太地區將佔據生物防治市場66.80%的佔有率,這反映了中國覆蓋1.65億公頃土地的強制性農藥減量政策以及印度慷慨的補貼計畫。中國的《國家農藥減量行動計畫》旨在2030年將化學農藥的使用量減少40%,並資助省級培訓中心開展田間規模的寄生性天敵釋放示範。印度的《國家永續農業使命》正在資助30個區域生產基地,為小規模農戶合作社提供微生物投入品。

預計到2031年,非洲將以10.44%的複合年成長率實現全球最快增速,這主要得益於各國政府將糧食安全目標與捐助者資助的永續性項目相結合。奈及利亞公私合營舉措旨在到2027年為200萬小規模農戶提供服務,而埃及正在建設15個本地生產中心,以減少對進口的依賴。本地生產能力將有助於供應更新鮮的產品,並避免低溫運輸缺口。

預計歐洲和北美將保持穩定成長,這得益於歐盟的「從農場到餐桌」戰略和高階有機產業的發展。歐洲生物防治市場的規模受惠於通用農業政策(CAP)的補貼機制,可涵蓋高達70%的產品成本。在北美,價值1,340億美元的有機零售通路正在推動對生物作物保護的需求,其產品價格比傳統產品高出20%至40%。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章 報告

第3章執行摘要和主要發現

第4章:主要產業趨勢

- 有機耕作面積

- 人均有機產品支出

- 法律規範

- 澳洲

- 巴西

- 加拿大

- 中國

- 法國

- 德國

- 印度

- 印尼

- 義大利

- 日本

- 墨西哥

- 荷蘭

- 菲律賓

- 俄羅斯

- 西班牙

- 泰國

- 土耳其

- 英國

- 美國

- 越南

- 價值鍊和通路分析

- 市場促進因素

- 嚴格禁止使用劇毒合成農藥

- 全球對經認證的有機農產品的需求不斷成長

- 害蟲對傳統殺蟲劑的抗藥性加速增強

- 政府對引進綜合蟲害管理(IPM)和生物材料提供補貼

- 昆蟲養殖自動化降低了宏觀生物養殖的成本

- 一種突破性的捕食性細菌平台,專門針對植物病原體

- 市場限制

- 許多活體產品的商業性保存期限很短。

- 需要經過多個機構的漫長報名手續。

- 用於生產下一代微生物製劑的無菌發酵設施產能有限

- 微氣候相關的效能差異會削弱農民的信心

第5章 市場規模和成長預測(價值和數量)

- 形式

- 宏觀生物學

- 生物體

- 致病線蟲

- 寄生天敵

- 掠食者

- 生物體

- 微生物

- 生物體

- 細菌生物防治劑

- 真菌生物防治劑

- 其他微生物

- 生物體

- 宏觀生物學

- 作物類型

- 經濟作物

- 園藝作物

- 田間作物

- 按地區

- 非洲

- 按國家/地區

- 埃及

- 奈及利亞

- 南非

- 其他非洲地區

- 按國家/地區

- 亞太地區

- 按國家/地區

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 菲律賓

- 泰國

- 越南

- 亞太其他地區

- 按國家/地區

- 歐洲

- 按國家/地區

- 法國

- 德國

- 義大利

- 荷蘭

- 俄羅斯

- 西班牙

- 土耳其

- 英國

- 其他歐洲地區

- 按國家/地區

- 中東

- 按國家/地區

- 伊朗

- 沙烏地阿拉伯

- 其他中東地區

- 按國家/地區

- 北美洲

- 按國家/地區

- 加拿大

- 墨西哥

- 美國

- 北美其他地區

- 按國家/地區

- 南美洲

- 按國家/地區

- 阿根廷

- 巴西

- 其他南美洲

- 按國家/地區

- 非洲

第6章 競爭情勢

- 關鍵策略舉措

- 市佔率分析

- 公司概況

- 公司簡介

- Koppert Biological Systems BV

- BASF SE

- Bayer AG

- Syngenta Group

- BioFirst Group

- Valent BioSciences(Sumitomo Chemical Co., Ltd.)

- Certis Biologicals(Mitsui and Co.)

- Andermatt Group AG

- Novonesis

- Pro Farm(Bioceres Crop Solutions)

- Bioline AgroSciences Ltd(InVivo Group)

- De Sangosse

- T Stanes and Company Limited(Amalgamations Group)

- Biobee Ltd

第7章:CEO們需要思考的關鍵策略問題

The biological control market was valued at USD 4.01 billion in 2025 and estimated to grow from USD 4.29 billion in 2026 to reach USD 5.98 billion by 2031, at a CAGR of 6.89% during the forecast period (2026-2031).

Cost-effective microbial platforms, automation in insect rearing, and mounting regulatory pressure against conventional pesticides are accelerating adoption across major crop systems. Asia-Pacific drives global demand through expansive government subsidy programs, while Africa's aggressive food-security initiatives anchor the fastest growth outlook. Rapid pest resistance to synthetic chemistries and rising consumer preference for certified-organic produce continue to expand addressable acreage. Meanwhile, fermentation innovation and longer shelf-life formulations are narrowing historical performance gaps with chemical alternatives, strengthening the competitive position of biological inputs.

Global Biological Control Market Trends and Insights

Stringent bans on high-toxicity synthetic pesticides

Regulators continue to phase out high-risk chemistries, catalyzing immediate substitution opportunities for biological solutions. The European Union Farm-to-Fork Strategy mandates a 50% cut in chemical pesticide use by 2030, and the United States Environmental Protection Agency (EPA) has canceled more than 40 active ingredients since 2024. Brazil and India issued parallel restrictions in 2024, increasing near-term acreage available for biocontrol adoption. These policy moves encourage manufacturers to accelerate product launches and spur farmers to recalibrate crop-protection programs toward IPM frameworks.

Rising global demand for certified-organic produce

Global organic food sales climbed to USD 134 billion in 2024, with annual growth above 8% in the United States, Germany, and China. Supermarkets enforce residue-free supplier policies, pushing growers to adopt biological inputs that preserve certification. Premium farm-gate prices, typically 20-40% above conventional produce, offset higher biological agent costs and facilitate deeper penetration in high-value horticulture.

Short commercial shelf-life for many living products

Most macrobial biocontrol agents maintain viability for only 2-4 weeks even under refrigerated conditions, necessitating expensive cold-chain logistics systems and significantly restricting market penetration in regions experiencing unreliable electricity supply. While recent technological advances in encapsulation methods and cryoprotectant formulations have demonstrated the potential to double product shelf-life in pilot studies, these improvements still fall considerably short of matching the multi-year stability achieved by synthetic chemical alternatives.

Other drivers and restraints analyzed in the detailed report include:

- Accelerating pest resistance to conventional chemistries

- Government subsidies for IPM adoption and biological inputs

- Protracted multi-agency registration timelines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Macrobials maintained their commanding 97.25% market share of the biological control market in 2025, reflecting decades of commercial development in beneficial insect production and established distribution networks that serve agricultural markets worldwide. The segment's dominance stems from proven efficacy in field applications and farmer familiarity with release protocols for predatory insects and parasitoids. Entomopathogenic nematodes represent the largest macrobial category, particularly effective against soil-dwelling pests in row crop systems. At the same time, predators and parasitoids excel in greenhouse environments where environmental conditions can be controlled.

Microbials are emerging as the growth engine with an 8.59% forecast CAGR through 2031. The shift toward microbials reflects technological advances in fermentation processes and formulation stability that are addressing historical limitations of bacterial and fungal biocontrol agents. Recent regulatory approvals for multi-strain microbial products are expanding application possibilities, particularly in high-value horticultural crops, where precision application justifies premium pricing. Other microbials, including viral and protozoan agents, remain niche applications but show promise for specific pest complexes where conventional approaches have failed. The form segmentation evolution indicates how different biological mechanisms are finding optimal commercial applications based on target pest biology and crop production systems.

The Biological Control Market Report is Segmented by Form (Macrobials, Microbials), Crop Type (Cash Crops, Horticultural Crops, and Row Crops), and Geography (Africa, Asia-Pacific, Europe, Middle East, North America, and South America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Geography Analysis

Asia-Pacific commanded 66.80% of the biological control market in 2025, reflecting 165 million hectares under mandatory pesticide-reduction mandates in China and generous subsidies in India. China's National Action Plan for Pesticide Reduction targets a 40% cut in chemical use by 2030 and funds provincial training centers that demonstrate field-scale parasitoid releases. India's National Mission for Sustainable Agriculture finances 30 regional production hubs supplying microbials to smallholder cooperatives.

Africa posts the fastest 10.44% CAGR to 2031 as governments combine food-security goals with donor-funded sustainability programs. Nigeria's public-private initiative plans to serve 2 million smallholders by 2027, while Egypt builds 15 local production sites to lessen import dependence. Local capacity enables fresher products and circumvents cold-chain gaps.

Europe and North America register steady gains supported by the European Union Farm-to-Fork Strategy and premium organic sectors. The biological control market size for Europe benefits from CAP reimbursements that cover up to 70% of product costs. North America leans on a USD 134 billion organic retail channel that secures premiums of 20-40% above conventional produce, reinforcing demand for biological crop protection.

- Koppert Biological Systems B.V.

- BASF SE

- Bayer AG

- Syngenta Group

- BioFirst Group

- Valent BioSciences (Sumitomo Chemical Co., Ltd.)

- Certis Biologicals (Mitsui and Co.)

- Andermatt Group AG

- Novonesis

- Pro Farm (Bioceres Crop Solutions)

- Bioline AgroSciences Ltd (InVivo Group)

- De Sangosse

- T Stanes and Company Limited (Amalgamations Group)

- Biobee Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 Brazil

- 4.3.3 Canada

- 4.3.4 China

- 4.3.5 France

- 4.3.6 Germany

- 4.3.7 India

- 4.3.8 Indonesia

- 4.3.9 Italy

- 4.3.10 Japan

- 4.3.11 Mexico

- 4.3.12 Netherlands

- 4.3.13 Philippines

- 4.3.14 Russia

- 4.3.15 Spain

- 4.3.16 Thailand

- 4.3.17 Turkey

- 4.3.18 United Kingdom

- 4.3.19 United States

- 4.3.20 Vietnam

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Stringent bans on high-toxicity synthetic pesticides

- 4.5.2 Rising global demand for certified-organic produce

- 4.5.3 Accelerating pest resistance to conventional chemistries

- 4.5.4 Government subsidies for IPM adoption and biological inputs

- 4.5.5 Insect-rearing automation slashing cost of macrobials

- 4.5.6 Breakthrough predatory bacterial platforms targeting phytopathogens

- 4.6 Market Restraints

- 4.6.1 Short commercial shelf-life for many living products

- 4.6.2 Protracted multi-agency registration timelines

- 4.6.3 Limited sterile fermentation capacity for next-gen microbials

- 4.6.4 Micro-climate-driven efficacy variability undermining farmer confidence

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Form

- 5.1.1 Macrobials

- 5.1.1.1 By Organism

- 5.1.1.1.1 Entamopathogenic Nematodes

- 5.1.1.1.2 Parasitoids

- 5.1.1.1.3 Predators

- 5.1.1.1 By Organism

- 5.1.2 Microbials

- 5.1.2.1 By Organism

- 5.1.2.1.1 Bacterial Biocontrol Agents

- 5.1.2.1.2 Fungal Biocontrol Agents

- 5.1.2.1.3 Other Microbials

- 5.1.2.1 By Organism

- 5.1.1 Macrobials

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Country

- 5.3.1.1.1 Egypt

- 5.3.1.1.2 Nigeria

- 5.3.1.1.3 South Africa

- 5.3.1.1.4 Rest of Africa

- 5.3.1.1 By Country

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Country

- 5.3.2.1.1 Australia

- 5.3.2.1.2 China

- 5.3.2.1.3 India

- 5.3.2.1.4 Indonesia

- 5.3.2.1.5 Japan

- 5.3.2.1.6 Philippines

- 5.3.2.1.7 Thailand

- 5.3.2.1.8 Vietnam

- 5.3.2.1.9 Rest of Asia-Pacific

- 5.3.2.1 By Country

- 5.3.3 Europe

- 5.3.3.1 By Country

- 5.3.3.1.1 France

- 5.3.3.1.2 Germany

- 5.3.3.1.3 Italy

- 5.3.3.1.4 Netherlands

- 5.3.3.1.5 Russia

- 5.3.3.1.6 Spain

- 5.3.3.1.7 Turkey

- 5.3.3.1.8 United Kingdom

- 5.3.3.1.9 Rest of Europe

- 5.3.3.1 By Country

- 5.3.4 Middle East

- 5.3.4.1 By Country

- 5.3.4.1.1 Iran

- 5.3.4.1.2 Saudi Arabia

- 5.3.4.1.3 Rest of Middle East

- 5.3.4.1 By Country

- 5.3.5 North America

- 5.3.5.1 By Country

- 5.3.5.1.1 Canada

- 5.3.5.1.2 Mexico

- 5.3.5.1.3 United States

- 5.3.5.1.4 Rest of North America

- 5.3.5.1 By Country

- 5.3.6 South America

- 5.3.6.1 By Country

- 5.3.6.1.1 Argentina

- 5.3.6.1.2 Brazil

- 5.3.6.1.3 Rest of South America

- 5.3.6.1 By Country

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Koppert Biological Systems B.V.

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Syngenta Group

- 6.4.5 BioFirst Group

- 6.4.6 Valent BioSciences (Sumitomo Chemical Co., Ltd.)

- 6.4.7 Certis Biologicals (Mitsui and Co.)

- 6.4.8 Andermatt Group AG

- 6.4.9 Novonesis

- 6.4.10 Pro Farm (Bioceres Crop Solutions)

- 6.4.11 Bioline AgroSciences Ltd (InVivo Group)

- 6.4.12 De Sangosse

- 6.4.13 T Stanes and Company Limited (Amalgamations Group)

- 6.4.14 Biobee Ltd

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

生物防治市場-全球市場預測(2026-2032年)

生物防治市場-全球市場預測(2026-2032年) 生物防治市場:依類型、作物、原料、應用、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

生物防治市場:依類型、作物、原料、應用、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 2026 年至 2035 年抗蟲種子性狀的市場機會、成長要素、產業趨勢分析與預測。

2026 年至 2035 年抗蟲種子性狀的市場機會、成長要素、產業趨勢分析與預測。 2026年全球生物防治市場報告

2026年全球生物防治市場報告 生物防治市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、功能、處理方法、作物類型、地區和競爭格局分類,2021-2031年)磁珠以微珠為基礎市場按產品類型、技術、應用和最終用戶分類,全球預測(2026-2032年)

生物防治市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、功能、處理方法、作物類型、地區和競爭格局分類,2021-2031年)磁珠以微珠為基礎市場按產品類型、技術、應用和最終用戶分類,全球預測(2026-2032年) 生物防治市場規模、佔有率及成長分析(依產品類型、作物類型、目標害蟲、配方、應用方法、通路及地區分類)-2026-2033年產業預測

生物防治市場規模、佔有率及成長分析(依產品類型、作物類型、目標害蟲、配方、應用方法、通路及地區分類)-2026-2033年產業預測 全球生物防治市場(2024-2028)

全球生物防治市場(2024-2028)