|

市場調查報告書

商品編碼

1939064

工程塑膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Engineering Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

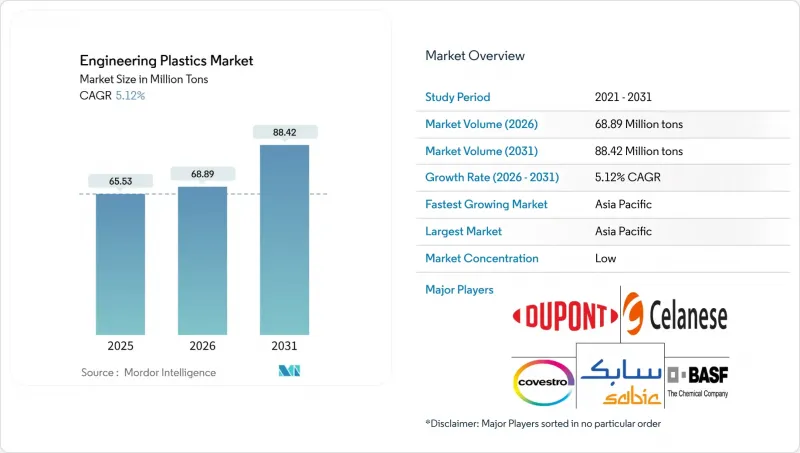

2025年工程塑膠市場價值為6,225萬噸,預計2031年將達到8,354萬噸,高於2026年的6,538萬噸。

預計在預測期(2026-2031 年)內,複合年成長率將達到 5.03%。

輕量化計畫在交通運輸和航太的應用、車輛和工業設備的電氣化以及半導體製造的日益普及,都推動了對高強度重量比和幾何自由度高的材料的需求。亞太地區持續的產能投資、商業規模化學回收的興起以及旨在提高燃油效率和減少碳排放的法規,進一步增強了這一成長勢頭。

全球工程塑膠市場趨勢與洞察

促進交通運輸和航太領域的輕量化發展

汽車燃油經濟法規(例如,美國CAFE標準要求到2025年達到54.5英里/加侖的燃油經濟性)正在推動汽車製造商(OEM)進行輕量化研發,預計每減重10%,燃油經濟性就能提高6%至8%。飛機項目也呈現類似的趨勢。波音787飛機採用50%的複合材料材料,實現了22%的燃油節省;空中巴士A350飛機採用53%的複合材料,也取得了類似的燃油經濟性提升。碳纖維增強熱塑性塑膠(CFTP)正日益普及,因為與熱固性塑膠不同,CFTP可以重新加熱和回收利用,自動化纖維鋪放技術正在縮短生產週期。風力發電機葉片目前消耗的碳纖維比航太工業還要多,100公尺長的碳纖維葉片比玻璃纖維葉片減重38%。這些成功案例增強了正在評估用於輪轂、座椅和飛機輔助結構的聚合物基結構的OEM製造商的信心。

電氣化所帶來的快速需求

高壓電動車需要具有優異阻燃性和介電強度的機殼,這推動了對聚亞苯硫醚、聚醚醚酮和玻璃纖維增強聚醯胺的需求。特斯拉Optimus原型機等機器人生產線凸顯了PEEK在連續使用下的耐久性,證明了其在高檔致動器中的有效性。人工智慧晶片的半導體製造廠在細間距連接器中使用液晶聚合物,這種聚合物在260°C以上的溫度下仍能保持尺寸穩定性,從而確保無鉛回流焊接過程中的訊號完整性。電動車(EV)架構從400V到800V的過渡對介電強度提出了更高的要求,原始設備製造商(OEM)要求絕緣材料的相對追蹤指數(CTI)達到600或更高。同時,聚碳酸酯-矽氧烷混合物擴大被用於防止熱失控,無需依賴厚重的金屬屏蔽層即可阻止熱傳遞。

單體價格波動

丙烯和乙烯價格與原油價格波動密切相關。這是因為亞洲裂解裝置嚴重依賴石腦油,原油價格每上漲10美元/桶,丙烯成本就會上漲90美元/噸,從而擠壓了以固定價格OEM合約銷售的轉換商的利潤空間。 2025年上半年,中國苯乙烯單體產能達2,151萬噸,佔全球供應量的49%。這導致現貨價格暴跌至高成本生產商的現金成本以下。主要經濟體之間關稅的提高進一步扭曲了貿易流量,迫使苯乙烯類ABS和聚碳酸酯工廠大幅減產。高性能樹脂,例如聚醯亞胺,尤其容易受到價格波動的影響,因為特種二酐單體的交易價格是商品原料價格的四到五倍,這限制了下游市場供應緊張時轉嫁價格上漲的能力。

細分市場分析

聚對苯二甲酸乙二醇酯(PET)在工程塑膠市場中佔據主導地位,預計到2025年將維持50.05%的市場佔有率,這主要得益於飲料和硬包裝的普遍需求。然而,該領域面臨一次性產品需求成長放緩以及日益提高的再生材料含量目標,這需要對生產流程進行投資。隨著汽車製造商選擇生物基PA11來減少範圍3排放,同時又不影響拉伸強度,聚醯胺共混物正重新受到青睞。氟聚合物雖然目前在工程塑膠市場僅佔個位數的中等佔有率,但預計將以7.34%的複合年成長率快速成長,這得益於其卓越的耐化學性和耐熱性,使其在航太線材塗層和7奈米以下晶片製造領域得到廣泛應用。

聚碸、PEEK(聚醚醚酮)和液晶聚合物適用於熔點高於280°C、連續使用溫度高於240°C的特定應用。聚碳酸酯雖然因其雙酚A(BPA)含量在食品容器中的應用而備受關注,但其優異的抗衝擊性使其在玻璃製品和家用電器機殼保持主導地位。聚甲醛因其良好的加工性能而適用於齒輪和窗戶升降器,而苯乙烯共聚物的性能介於通用ABS樹脂和特殊共混物之間,是兼顧強度和成本的家用電器框架的標準材料。

工程塑膠市場報告按樹脂類型(含氟聚合物、液晶聚合物、聚醯胺、聚丁烯對苯二甲酸酯、聚碳酸酯等)、終端用戶產業(航太、汽車、建築等)和地區(亞太、北美、歐洲、南美、中東和非洲)進行細分。市場預測以數量(噸)和價值(美元)為單位。

區域分析

預計到2025年,亞太地區將佔全球工程塑膠市場佔有率的55.10%,並在2031年之前以5.38%的複合年成長率成長,這主要得益於中國和印度產能的擴張、電動車(EV)的加速普及以及電子產品出口需求的持續成長。中國的苯乙烯產量已佔全球總產量的49%,鞏固了其在該地區的價格主導。同時,各國政府也積極推動高附加價值聚合物的自給自足。印度正利用稅額扣抵和進口關稅減免等政策,吸引那些覬覦其南部汽車產業基地的跨國模具製造商。日本專注於半導體光掩模用超高純度聚合物,這表明該地區的聚合物市場覆蓋範圍廣,從大規模生產到高附加價值應用均有涉及。

北美地區得益於民用航太領域的強勁需求以及從密西根州延伸至喬治亞的不斷擴張的電池製造走廊。包括美國稅法S 45Z無污染燃料抵免(針對化學回收生產)在內的先進回收立法支持,正在刺激循環經濟領域的創新。歐洲正透過其「綠色交易」引領永續性發展,推動生物基聚醯胺和化學回收聚碳酸酯的研發。然而,高昂的電力成本和關於全氟烷基和多氟烷基物質(PFAS)的爭議阻礙了含氟聚合物產能的擴張。

由於巴西和阿根廷汽車產業的本土化,南美洲市場正經歷漸進式成長,但高性能樹脂仍依賴淨進口。中東和非洲地區正崛起為投資熱點,這得益於阿布達比國家石油公司(ADNOC)的垂直整合策略,一旦科思創的產能協同效應得以實現,該地區有望成為特種工程樹脂的淨出口地區。在所有地區,推動工程塑膠市場規模成長的因素是供應鏈全球化以及下游製造業的轉型,而不僅僅是樹脂生產基地的擴張。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 促進交通運輸和航太領域的輕量化發展

- 電氣化主導和快速需求成長

- 亞太地區製造業轉移趨勢

- 電動車電池模組外殼採用情況

- 化學品回收供應增加

- 原始設備製造商轉向生物基光聲/光熱療法

- 市場限制

- 單體價格波動

- 加強包裝法規

- 螢石相關氟樹脂短缺

- 金屬積層製造(AM)替代的風險

- 價值鍊和通路分析

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 產業間競爭

- 進出口趨勢

- 氟樹脂交易

- 聚醯胺(PA)交易

- 聚對苯二甲酸乙二酯(PET)貿易

- 聚甲基丙烯酸甲酯(PMMA)貿易

- 聚甲醛(POM)貿易

- 苯乙烯共聚物(ABS和SAN)的貿易

- 聚碳酸酯(PC)貿易

- 價格趨勢

- 氟樹脂

- 聚碳酸酯(PC)

- 聚對苯二甲酸乙二醇酯(PET)

- 聚甲醛(POM)

- 聚甲基丙烯酸甲酯(PMMA)

- 苯乙烯共聚物(ABS 和 SAN)

- 聚醯胺(PA)

- 回收利用概述

- 聚醯胺(PA)回收趨勢

- 聚碳酸酯(PC)回收趨勢

- 聚對苯二甲酸乙二醇酯(PET)回收趨勢

- 苯乙烯共聚物(ABS 和 SAN)的回收趨勢

- 法律規範

- 授權人概覽

- 產品概覽

- 終端用戶產業趨勢

- 航太(航太零件生產收入)

- 汽車(汽車產量)

- 建築與施工(新建建築占地面積)

- 電氣電子設備(電氣電子設備生產收入)

- 包裝(塑膠包裝用量)

第5章 市場規模及成長預測(數量與以金額為準)

- 依樹脂類型

- 氟樹脂

- 乙烯-四氟乙烯(ETFE)

- 氟化乙烯丙烯(FEP)

- 聚四氟乙烯(PTFE)

- 聚偏氟乙烯(PVF)

- 聚二氟亞乙烯(PVDF)

- 其他樹脂類型

- 液晶聚合物(LCP)

- 聚醯胺(PA)

- 芳香聚醯胺

- 聚醯胺(PA)6

- 聚醯胺(PA)66

- 聚鄰苯二甲醯胺

- 聚丁烯對苯二甲酸酯(PBT)

- 聚碳酸酯(PC)

- 聚醚醚酮(PEEK)

- 聚對苯二甲酸乙二醇酯(PET)

- 聚醯亞胺(PI)

- 聚甲基丙烯酸甲酯(PMMA)

- 聚甲醛(POM)

- 苯乙烯共聚物(ABS、SAN)

- 氟樹脂

- 按最終用戶行業分類

- 航太

- 車

- 建築/施工

- 電氣和電子設備

- 工業和機械

- 包裝

- 其他終端用戶產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 馬來西亞

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 俄羅斯

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Alfa SAB de CV

- Arkema

- Asahi Kasei Corporation

- BASF

- Celanese Corporation

- CHIMEI

- Covestro AG

- Dongyue Group

- Envalior

- DuPont

- Evonik Industries AG

- Far Eastern New Century Co., Ltd.

- Indorama Ventures Public Company Limited.

- Lanxess AG

- LG Chem

- Mitsubishi Chemical Group Corporation

- SABIC

- Syensqo

- Teijin Limited

- Toray Industries Inc.

- Victrex plc

第7章 市場機會與未來展望

第8章:執行長面臨的關鍵策略挑戰

The Engineering Plastics Market was valued at 62.25 million tons in 2025 and estimated to grow from 65.38 million tons in 2026 to reach 83.54 million tons by 2031, at a CAGR of 5.03% during the forecast period (2026-2031).

Demand stems from lightweighting programs across the mobility and aerospace sectors, the electrification of vehicles and industrial equipment, and the growing adoption of semiconductor fabrication, all of which reward materials that offer high strength-to-weight ratios and geometric freedom. Sustained capital spending on Asia-Pacific capacity, the emergence of chemical recycling at a commercial scale, and regulatory pushes for fuel economy and carbon reduction further reinforce growth momentum.

Global Engineering Plastics Market Trends and Insights

Lightweighting Push in Mobility and Aerospace

Automotive fuel-economy mandates, such as the US CAFE target of 54.5 mpg by 2025, intensify OEM (original equipment manufacturer) focus on weight reduction, and every 10% mass cut yields 6-8% efficiency gains. Aircraft programs illustrate parallel dynamics: the Boeing 787 achieved 22% fuel savings with 50% composite content, while the Airbus A350 utilizes 53% composites to achieve a similar effect. Carbon-fiber-reinforced thermoplastics gain share because they can be reheated and recycled, unlike thermosets, and automated fiber placement lowers cycle times. Wind-turbine blades now consume larger volumes of carbon fiber than the aerospace industry, with 100-meter blades trimming mass by 38% compared to glass-fiber designs. These successes raise confidence among OEMs evaluating polymer-based structures for wheels, seating, and secondary aircraft structures.

Electrification-Led Demand Spike

High-voltage electric vehicles require enclosures that offer robust flame retardancy and dielectric strength, pushing polyphenylene sulfide, polyether ether ketone, and glass-filled polyamide consumption upward. Robotics lines such as Tesla's Optimus prototype highlight PEEK's longevity under continuous duty, validating higher-end grades for actuators. Semiconductor fabs scaling for AI chips adopt liquid-crystal polymers for fine-pitch connectors that remain dimensionally stable above 260 °C, preserving signal integrity during lead-free reflow. The migration from 400-V to 800-V EV (electric vehicle) architectures amplifies dielectric stress, prompting OEMs to specify insulation with comparative tracking index (CTI) values above 600. Meanwhile, thermal-runaway barriers increasingly incorporate polycarbonate-siloxane blends to prevent heat propagation without resorting to heavy metallic shields.

Monomer Price Volatility

Propylene and ethylene prices track crude swings because Asian crackers rely heavily on naphtha; a USD 10/bbl oil jump can increase propylene costs by USD 90/ton, compressing converters' margins when selling into fixed-price OEM contracts. China's styrene monomer capacity reached 21.51 million tons in H1 2025, accounting for 49% of the global supply and triggering spot price collapses below cash costs for high-cost producers. Tariff escalations between major economies further distort trade flows, forcing rapid output cuts at styrene-based ABS and polycarbonate plants. Volatility particularly stings high-performance resins such as polyimide, whose specialized dianhydride monomers command 4-5X commodity feedstock prices, limiting the ability to pass on surges in tight downstream markets.

Other drivers and restraints analyzed in the detailed report include:

- APAC Manufacturing Migration

- EV Battery Module Housings Adoption

- Packaging Regulations Tightening

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyethylene terephthalate (PET) maintained a commanding 50.05% engineering plastics market share in 2025, driven by ubiquitous demand for beverages and rigid packaging. Yet the segment contends with plateauing single-use volumes and mounting recycled-content targets that require process investments. Polyamide blends are gaining renewed traction as automakers opt for bio-based PA11 to reduce scope 3 emissions without compromising tensile strength. Fluoropolymers, although comprising only a mid-single-digit slice of the engineering plastics market, post the fastest 7.34% CAGR because their unrivaled chemical and thermal resistance support aerospace wire coatings and sub-7 nm chip making.

Polysulfones, PEEK (Polyetheretherketone or Polyether Ether Ketone), and liquid-crystal polymers are suitable for niche applications where melting points exceed 280°C and continuous-use temperatures surpass 240°C. Polycarbonate endures scrutiny for BPA (Bisphenol A) in foodware but retains dominance in glazing and consumer electronics housings due to its impact resilience. Polyoxymethylene offers machining ease for gears and window lifters, while styrene copolymers bridge the gap between commodity ABS (Acrylonitrile Butadiene Styrene) and specialty blends, making them a go-to for appliance frames that require balanced toughness and cost.

The Engineering Plastics Market Report is Segmented by Resin Type (Fluoropolymer, Liquid Crystal Polymer, Polyamide, Polybutylene Terephthalate, Polycarbonate, and More), End-User Industry (Aerospace, Automotive, Building and Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons) and Value (USD).

Geography Analysis

The Asia-Pacific region led with a 55.10% engineering plastics market share in 2025 and is expected to expand at a 5.38% CAGR through 2031, driven by the build-out of Chinese and Indian capacities, accelerating EV adoption, and sustained electronics export demand. Chinese styrene production, already 49% of global output, reinforces regional price leadership, while state policies encourage high-value polymer self-sufficiency. India leverages tax credits and import duty relief to draw multinational molders eyeing southern automotive hubs. Japan focuses on ultra-high-purity polymers for semiconductor photomasks, demonstrating the region's spectrum from volume to value.

North America enjoys robust demand from the commercial aerospace sector and an expanding battery-manufacturing corridor that stretches from Michigan to Georgia. Legislative support for advanced recycling, including the US Internal Revenue Code S 45Z clean-fuel credits applicable to chemical recycling outputs, incentivizes innovation in the circular economy. Europe champions sustainability leadership through the Green Deal, spurring R&D in bio-based PA and chemically recycled polycarbonate, although high power costs and PFAS debates weigh on fluoropolymer capacity additions.

South America sees incremental growth tied to automotive localization in Brazil and Argentina, yet remains net-import-reliant for high-performance grades. Middle East & Africa emerge as investment destinations following ADNOC's vertical integration move, which positions the region as a potential net exporter of specialty engineering resins once Covestro capacity synergies materialize. Across all regions, the globalization of supply chains means that engineering plastics market size evolves in lock-step with downstream manufacturing shifts rather than mere resin production footprints.

- Alfa S.A.B. de C.V.

- Arkema

- Asahi Kasei Corporation

- BASF

- Celanese Corporation

- CHIMEI

- Covestro AG

- Dongyue Group

- Envalior

- DuPont

- Evonik Industries AG

- Far Eastern New Century Co., Ltd.

- Indorama Ventures Public Company Limited.

- Lanxess AG

- LG Chem

- Mitsubishi Chemical Group Corporation

- SABIC

- Syensqo

- Teijin Limited

- Toray Industries Inc.

- Victrex plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Lightweighting Push in Mobility and Aerospace

- 4.2.2 Electrification-led and Demand Spike

- 4.2.3 Asia-Pacific Manufacturing Migration

- 4.2.4 EV Battery Module Housings Adoption

- 4.2.5 Chemical-recycling Supply Boosts

- 4.2.6 OEM switch to bio-based PA/PTT

- 4.3 Market Restraints

- 4.3.1 Monomer Price Volatility

- 4.3.2 Packaging Regulations Tightening

- 4.3.3 Fluorspar-linked Fluoropolymer Shortage

- 4.3.4 Metal AM substitution threat

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Industry Rivalry

- 4.6 Import And Export Trends

- 4.6.1 Fluoropolymer Trade

- 4.6.2 Polyamide (PA) Trade

- 4.6.3 Polyethylene Terephthalate (PET) Trade

- 4.6.4 Polymethyl Methacrylate (PMMA) Trade

- 4.6.5 Polyoxymethylene (POM) Trade

- 4.6.6 Styrene Copolymers (ABS and SAN) Trade

- 4.6.7 Polycarbonate (PC) Trade

- 4.7 Price Trends

- 4.7.1 Fluoropolymer

- 4.7.2 Polycarbonate (PC)

- 4.7.3 Polyethylene Terephthalate (PET)

- 4.7.4 Polyoxymethylene (POM)

- 4.7.5 Polymethyl Methacrylate (PMMA)

- 4.7.6 Styrene Copolymers (ABS and SAN)

- 4.7.7 Polyamide (PA)

- 4.8 Recycling Overview

- 4.8.1 Polyamide (PA) Recycling Trends

- 4.8.2 Polycarbonate (PC) Recycling Trends

- 4.8.3 Polyethylene Terephthalate (PET) Recycling Trends

- 4.8.4 Styrene Copolymers (ABS and SAN) Recycling Trends

- 4.9 Regulatory Framework

- 4.10 Licensors Overview

- 4.11 Production Overview

- 4.12 End-use Sector Trends

- 4.12.1 Aerospace (Aerospace Component Production Revenue)

- 4.12.2 Automotive (Automobile Production)

- 4.12.3 Building and Construction (New Construction Floor Area)

- 4.12.4 Electrical and Electronics (Electrical and Electronics Production Revenue)

- 4.12.5 Packaging(Plastic Packaging Volume)

5 Market Size and Growth Forecasts (Volume and Value)

- 5.1 By Resin Type

- 5.1.1 Fluoropolymer

- 5.1.1.1 Ethylenetetrafluoroethylene (ETFE)

- 5.1.1.2 Fluorinated Ethylene-propylene (FEP)

- 5.1.1.3 Polytetrafluoroethylene (PTFE)

- 5.1.1.4 Polyvinylfluoride (PVF)

- 5.1.1.5 Polyvinylidene Fluoride (PVDF)

- 5.1.1.6 Other Sub Resin Types

- 5.1.2 Liquid Crystal Polymer (LCP)

- 5.1.3 Polyamide (PA)

- 5.1.3.1 Aramid

- 5.1.3.2 Polyamide (PA) 6

- 5.1.3.3 Polyamide (PA) 66

- 5.1.3.4 Polyphthalamide

- 5.1.4 Polybutylene Terephthalate (PBT)

- 5.1.5 Polycarbonate (PC)

- 5.1.6 Polyether Ether Ketone (PEEK)

- 5.1.7 Polyethylene Terephthalate (PET)

- 5.1.8 Polyimide (PI)

- 5.1.9 Polymethyl Methacrylate (PMMA)

- 5.1.10 Polyoxymethylene (POM)

- 5.1.11 Styrene Copolymers (ABS, SAN)

- 5.1.1 Fluoropolymer

- 5.2 By End-User Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Electrical and Electronics

- 5.2.5 Industrial and Machinery

- 5.2.6 Packaging

- 5.2.7 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Australia

- 5.3.1.6 Malaysia

- 5.3.1.7 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 United Kingdom

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Nigeria

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)**/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Production Capacity, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Alfa S.A.B. de C.V.

- 6.4.2 Arkema

- 6.4.3 Asahi Kasei Corporation

- 6.4.4 BASF

- 6.4.5 Celanese Corporation

- 6.4.6 CHIMEI

- 6.4.7 Covestro AG

- 6.4.8 Dongyue Group

- 6.4.9 Envalior

- 6.4.10 DuPont

- 6.4.11 Evonik Industries AG

- 6.4.12 Far Eastern New Century Co., Ltd.

- 6.4.13 Indorama Ventures Public Company Limited.

- 6.4.14 Lanxess AG

- 6.4.15 LG Chem

- 6.4.16 Mitsubishi Chemical Group Corporation

- 6.4.17 SABIC

- 6.4.18 Syensqo

- 6.4.19 Teijin Limited

- 6.4.20 Toray Industries Inc.

- 6.4.21 Victrex plc

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Self-Healing Plastics

8 Key Strategic Questions for CEOs

先進工程熱塑性塑膠市場預測至2034年-按產品類型、加工技術、應用和地區分類的全球分析

先進工程熱塑性塑膠市場預測至2034年-按產品類型、加工技術、應用和地區分類的全球分析 全球聚甲醛樹脂市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球聚甲醛樹脂市場規模、佔有率、趨勢和成長分析報告(2026-2034) MPPE工程塑膠市場規模、佔有率和成長分析:按產品類型、配方類型、應用、終端用戶產業和地區分類-2026-2033年產業預測工程塑膠市場規模、佔有率、成長及全球產業分析:按類型和應用分類,區域洞察及2026-2034年預測

MPPE工程塑膠市場規模、佔有率和成長分析:按產品類型、配方類型、應用、終端用戶產業和地區分類-2026-2033年產業預測工程塑膠市場規模、佔有率、成長及全球產業分析:按類型和應用分類,區域洞察及2026-2034年預測 2026年全球工程塑膠市場報告

2026年全球工程塑膠市場報告 5G專用工程塑膠:按樹脂類型、製程、應用和最終用途產業分類的全球預測,2026-2032年PA66工程塑膠市場依製造流程、產品類型、等級及最終用途產業分類-2026-2032年全球預測先進工程聚合物市場預測至2032年:按聚合物類型、形態、性能、技術、最終用戶和地區分類的全球分析

5G專用工程塑膠:按樹脂類型、製程、應用和最終用途產業分類的全球預測,2026-2032年PA66工程塑膠市場依製造流程、產品類型、等級及最終用途產業分類-2026-2032年全球預測先進工程聚合物市場預測至2032年:按聚合物類型、形態、性能、技術、最終用戶和地區分類的全球分析 日本工程塑膠市場報告(按樹脂類型、最終用途產業和地區分類,2026-2034年)

日本工程塑膠市場報告(按樹脂類型、最終用途產業和地區分類,2026-2034年) 工程塑膠市場規模、佔有率和成長分析(按樹脂類型、最終用途和地區分類)-2026-2033年產業預測

工程塑膠市場規模、佔有率和成長分析(按樹脂類型、最終用途和地區分類)-2026-2033年產業預測