|

市場調查報告書

商品編碼

1939042

鈧:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Scandium - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

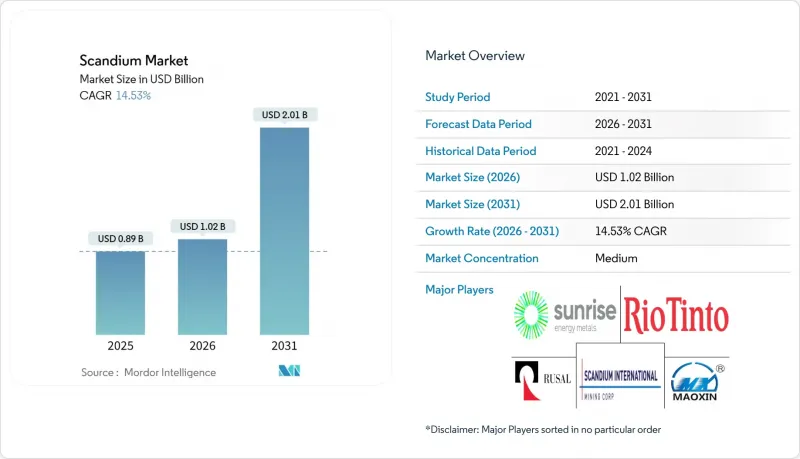

預計到 2026 年,鈧市場價值將達到 8.8 億美元,高於 2025 年的 7.7 億美元。

預計到 2031 年將達到 17.3 億美元,2026 年至 2031 年的複合年成長率為 14.5%。

這一快速成長趨勢的促進因素包括:對鈧穩定固體氧化物燃料電池(SOFC)的需求不斷成長、西方國家對關鍵礦產的優惠政策,以及下一代航太平台加速採用鋁鈧合金。中國於2025年4月實施的出口許可證制度擾亂了全球貿易流動,凸顯了供應鏈風險,促使美國、歐盟和澳洲積極投資替代供應基地。隨著鈧市場從實驗室研究對象轉變為策略性材料,那些掌握了大規模、高純度生產技術的公司佔據了有利地位。

全球鈧市場趨勢與洞察

固體氧化物燃料電池(SOFC)的應用日益廣泛

鈧穩定氧化鋯可在不犧牲離子電導率的前提下降低固體氧化物燃料電池(SOFC)的動作溫度,從而延長電池堆壽命並降低整體電廠組件成本。日本住宅能源農場的部署和歐洲分散式發電補貼計畫支撐了對氧化鈧的穩定需求。美國能源局的「2025氫能計畫」藍圖將SOFC確定為長期電網儲能的關鍵技術,並確立了長期採購前景。 Bloom Energy公司於2025年成功量產了6N級氧化鈧基電解質,證明了其在成本挑戰下的商業性可行性。從二氧化鈦廢棄物中回收鈧技術的突破性進展有望緩解長期以來限制SOFC應用僅限於高階市場的價格壓力。

航太和國防領域對鋁鈧合金的需求不斷成長

美國國防部的高超音速飛彈計畫採用鋁鈧基合金,這種合金在熱循環條件下能夠保持其晶粒結構。 NioCorp公司根據《2025年國防生產法案》與主要企業簽訂契約,供應經認證的鋁鈧合金零件,這凸顯了該金屬的戰略價值。波音和空中巴士目前正在進行一項為期10年的積層製造機身框架認證項目,其中鈧的焊接抗裂性能優於7xxx系鋁合金。航太發射業者正在採用鈧合金製造重量關鍵的推進劑儲箱,這進一步鞏固了其長期需求。

材料成本上漲和價格波動

2025年8月,6N氧化鈧現貨價格在每公斤632.95美元至715.23美元之間,精煉金屬價格在特殊訂單中可達每克269美元。年供應量約80噸,而預計2040年的潛在需求量將達到1,970噸,因此極易受到供應中斷的影響。大部分貿易為雙邊貿易,限制了原始設備製造商(OEM)的避險選擇。在景氣衰退時期,以鎳紅土礦或二氧化鈦產品形式回收鈧的生產商會減少投資,因為單位經濟效益與基礎材料價格的波動密切相關。

細分市場分析

截至2025年,合金領域將佔據鈧市場需求的最大佔有率,達到34.90%。這反映了航太鉚釘、自行車車架和體育用品領域的成熟。 IBC Advanced Alloys於2025年與NioCorp簽署了一項長期供應協議,為其供應母合金坯料,從而加強了北美價值鏈。氧化物領域預計將以15.78%的複合年成長率成長,主要受固體氧化物燃料電池(SOFC)和半導體需求成長的推動。就鈧產品市場而言,預計到2031年,氧化物需求將達到2.1億美元。氟化物和氯化物鹽主要用於電子和催化等小眾應用,而碳酸鹽鹽在研發規模上仍處於滯後狀態。高純度鈧金屬粉末是積層製造的關鍵材料,正逐漸成為未來的成長領域,但其商業產量仍低於每年5噸。

用於浸出赤泥和二氧化鈦廢棄物的第二代製程正在增加氧化物供應,並縮小其與合金的價格差距。為了平衡性能和成本,合金製造商正在嘗試降低鈧含量(0.2-0.4 wt%),這一趨勢可能有助於其在對成本敏感的汽車和無人機結構領域滲透市場。然而,用於固體氧化物燃料電池(SOFC)和微電子的氧化物買家要求純度達到99.999%,這在更廣泛的鈧市場中造成了價格兩極分化的局面。

區域分析

預計到2025年,中國將保持39.45%的鈧市場佔有率,這主要得益於其在二氧化鈦(TiO2)和稀土元素的一體化生產過程中聯合生產氧化鈧。國內需求涵蓋固態氧化物燃料電池(SOFC)原型、5G基地台陶瓷以及無人機機身等領域。自2025年4月起,出口許可政策的收緊將限制海運,迫使非中國原始設備製造商(OEM)實現供應來源多元化。美國是成長最快的消費國,預計到2031年將以15.20%的複合年成長率成長,這主要得益於國防、航太和積層製造領域需求的成長。第三類融資和美國進出口銀行的信貸額度顯著提高了NioCorp等新興生產商的計劃可行性,為北美鈧供應鏈的建構奠定了基礎。

俄羅斯憑藉俄鋁赤泥回收生產線,仍是世界三大鈧生產國之一。政治風險和製裁使對歐美市場的銷售變得複雜,但國內航太計畫消耗了大量鈧。菲律賓塔加尼托高壓酸浸(HPAL)工廠從鎳紅土礦中回收鈧,主要以氧化物形式運往日本固體氧化物燃料電池(SOFC)一體化製造商。澳洲擁有全球最大的已探明鈧礦產資源。 Sunrise Energy Metals公司的Sirestone礦床於2025年9月資源量提升了98%,可望成為亞太地區供應多元化的基礎。歐盟於2025年將鈧指定為戰略原料,這刺激了芬蘭和西班牙的探勘,並鼓勵與大洋洲的計劃進行長期供應協議談判。巴西和印度已開始探勘二氧化鈦和紅土尾礦中的鈧含量,預示著未來供應選擇將更加多樣化。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 固體氧化物燃料電池的應用日益廣泛

- 航太和國防領域對鋁鈧合金的需求不斷成長

- 關鍵礦產政策獎勵和資金籌措

- 利用Sc擴展積層製造技術

- 高介電常數Sc2O3閘極介質的技術進步

- 市場限制

- 材料成本高成本且價格波動劇烈

- 供應集中在少數國家

- 赤泥/高壓酸洗廢棄物處理中的環境、社會及治理問題

- 定價不明確且缺乏標準

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 環境影響分析

- 定價分析

第5章 市場規模與成長預測

- 依產品類型

- 氧化物

- 氟化物

- 氯化物

- 硝酸鹽

- 碘化物

- 合金

- 碳酸鹽及其他產品類型

- 按最終用戶行業分類

- 航太與國防

- 固體氧化物燃料電池(SOFC)

- 陶瓷

- 照明

- 電子設備

- 3D列印

- 體育用品

- 其他終端用戶產業

- 按地區

- 生產分析

- 中國

- 俄羅斯

- 菲律賓

- 世界其他地區

- 消費分析

- 美國

- 中國

- 俄羅斯

- 日本

- 巴西

- EU

- 世界其他地區

- 生產分析

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Ardea Resources

- Guangxi Maoxin Technology Co., Ltd

- Henan Rongjia Scandium Vanadium Technology Co., Ltd

- Huizhou Top Metal Materials Co., Ltd.

- Hunan Oriental Scandium Co., Ltd.

- Hunan Rare Earth Metal Materials Research Institute Co. Ltd.

- JSC Dalur

- MCC Group

- Niocorp Development Ltd.

- Rio Tinto

- Rusal

- Scandium Canada Ltd.

- Scandium International Mining Corporation

- Stanford Advanced Materials

- Sumitomo Metal Mining Co., Ltd.

- Sunrise Energy Metals Limited

- Treibacher Industrie Ag

第7章 市場機會與未來展望

Scandium market size in 2026 is estimated at USD 0.88 billion, growing from 2025 value of USD 0.77 billion with 2031 projections showing USD 1.73 billion, growing at 14.5% CAGR over 2026-2031.

Rising demand for scandium-stabilized solid-oxide fuel cells (SOFCs), critical-mineral policy incentives in Western economies, and accelerating adoption of aluminum-scandium alloys in next-generation aerospace platforms are driving this steep growth trajectory. China's April 2025 export-licensing rules disrupted global trade flows and highlighted supply-chain risk, spurring active government funding for alternative supply hubs in the United States, the European Union, and Australia. Companies that master large-scale, high-purity production are well positioned as the scandium market pivots from laboratory curiosity to strategic material.

Global Scandium Market Trends and Insights

Growing adoption in solid-oxide fuel cells

Scandium-stabilized zirconia lowers SOFC (solid-oxide fuel cells) operating temperature without sacrificing ionic conductivity, extending stack life, and enabling cheaper balance-of-plant components. Japan's residential Ene-Farm rollout and Europe's distributed-generation subsidies fuel steady scandium oxide demand. The US Department of Energy's 2025 Hydrogen Shot roadmap designates SOFCs as critical for long-duration grid storage, anchoring long-term procurement visibility. Bloom Energy scaled production of 6N scandium oxide-based electrolytes in 2025, proving commercial viability despite cost headwinds. Processing breakthroughs that recover scandium from titanium-dioxide waste streams could ease pricing pressure that historically limited SOFC penetration to premium markets.

Rising demand for Al-Sc alloys in aerospace and defense

Pentagon hypersonic-missile programs rely on aluminum-scandium master alloys that maintain grain structure under thermal cycling. NioCorp's 2025 agreement with defense primes to supply qualified Al-Sc alloy components under the Defense Production Act underscores the metal's strategic value. Boeing and Airbus are midway through decade-long qualification programs for additive-manufactured fuselage frames, where scandium's weld-crack resistance outperforms 7xxx-series aluminum. Space-launch operators embraced scandium alloys for weight-critical propellant tanks, reinforcing long-run demand.

High material cost and price volatility

Spot prices for 6N scandium oxide swung between USD 632.95-715.23 kg in August 2025, while distilled metal touched USD 269 g on specialty orders. Annual supply is roughly 80 t against the potential 2040 demand of 1,970 t, amplifying outage sensitivity. Most deals remain bilateral, leaving OEMs with limited hedging options. Producers recovering scandium as a by-product of nickel laterite or TiO2 see unit economics tied to host-commodity cycles, deterring new investment during downturns.

Other drivers and restraints analyzed in the detailed report include:

- Critical-mineral policy incentives and funding

- Expansion of Sc-enabled additive manufacturing

- Supply concentration in a few countries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Alloys captured the largest 2025 share at 34.90% of scandium market demand, reflecting maturation in aerospace rivets, bicycle frames, and sporting goods. IBC Advanced Alloys signed a long-term offtake with NioCorp in 2025 to supply master-alloy billets, reinforcing a North American value chain. The oxide category is the fastest-growing, projected to post a 15.78% CAGR on SOFC and semiconductor uptake. Within the scandium market size for products, oxide demand is forecast to reach USD 0.21 billion by 2031. Fluoride and chloride salts serve niche electronic and catalytic uses, while carbonate trails in R&D scale. High-purity scandium metal powder, essential for additive manufacturing, is emerging as a future growth pocket, though commercial volumes remain below 5 t per year.

Second-generation processing flowsheets that leach red mud or titanium-dioxide waste increase oxide availability, narrowing the price gap with alloys. Alloy producers are experimenting with lower scandium loadings (0.2-0.4 wt%) to balance performance and cost; this trend could help the scandium market penetrate cost-sensitive automotive and drone structures. However, oxide buyers in SOFC and microelectronics require 99.999% purity, creating a bifurcated price environment within the broader scandium market.

The Scandium Market Report is Segmented by Product Type (Oxide, Fluoride, Chloride, Iodide, Carbonate, and Other Product Types), End-User Industry (Aerospace and Defense, Solid Oxide Fuel Cells, Ceramics, Lighting, Electronics, Sporting Goods, and Other End-User Industries), and Geography (United States, China, Russia, Japan, Brazil, European Union, and Rest of the World). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

China retained 39.45% Scandium market share in 2025, underpinned by integrated TiO2 and rare-earth operations that co-recover scandium oxide. Domestic demand spans SOFC prototypes, 5G-base-station ceramics, and drone airframes. The April 2025 export-license framework tightened seaborne availability, prompting non-Chinese OEMs (original equipment manufacturers) to diversify supply. The United States is the fastest-growing consumer, forecast at 15.20% CAGR to 2031 on defense, space, and additive-manufacturing uptake. Title III funding and Ex-Im Bank facilities have materially improved project viability for NioCorp and other emerging producers, setting the stage for a North American scandium supply chain.

Russia remains a top-three producer via Rusal's red-mud-recovery lines. Political risk and sanctions complicate Western offtake, but domestic aerospace programs absorb meaningful volumes. The Philippines' Taganito HPAL plant recovers scandium from nickel laterite, primarily shipping oxide to Japanese SOFC integrators. Australia hosts the world's largest identified scandium mineral resources; Sunrise Energy Metals' Syerston deposit received a 98% resource upgrade in September 2025 and could anchor Asia-Pacific diversification. The European Union classified scandium as a strategic raw material in 2025, catalyzing exploration in Finland and Spain and prompting long-term offtake talks with Oceania projects. Brazil and India have begun mapping titanium-dioxide and laterite tailings for scandium prospects, signaling future supply-side optionality.

- Ardea Resources

- Guangxi Maoxin Technology Co., Ltd

- Henan Rongjia Scandium Vanadium Technology Co., Ltd

- Huizhou Top Metal Materials Co., Ltd.

- Hunan Oriental Scandium Co., Ltd.

- Hunan Rare Earth Metal Materials Research Institute Co. Ltd.

- JSC Dalur

- MCC Group

- Niocorp Development Ltd.

- Rio Tinto

- Rusal

- Scandium Canada Ltd.

- Scandium International Mining Corporation

- Stanford Advanced Materials

- Sumitomo Metal Mining Co., Ltd.

- Sunrise Energy Metals Limited

- Treibacher Industrie Ag

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing adoption in solid-oxide fuel cells

- 4.2.2 Rising demand for Al-Sc alloys in aerospace and defence

- 4.2.3 Critical-mineral policy incentives and funding

- 4.2.4 Expansion of Sc-enabled additive manufacturing

- 4.2.5 Breakthroughs in high-k Sc2O3 gate dielectrics

- 4.3 Market Restraints

- 4.3.1 High material cost and price volatility

- 4.3.2 Supply concentration in a few countries

- 4.3.3 ESG hurdles in red-mud / HPAL waste processing

- 4.3.4 Opaque pricing and lack of standards

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Environmental Impact Analysis

- 4.7 Price Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Oxide

- 5.1.2 Flouride

- 5.1.3 Chloride

- 5.1.4 Nitrate

- 5.1.5 Iodide

- 5.1.6 Alloy

- 5.1.7 Carbonate and Other Product Types

- 5.2 By End-user Industry

- 5.2.1 Aerospace and Defense

- 5.2.2 Solid Oxide Fuel Cells (SOFCs)

- 5.2.3 Ceramics

- 5.2.4 Lighting

- 5.2.5 Electronics

- 5.2.6 3D Printing

- 5.2.7 Sporting Goods

- 5.2.8 Other End-User Industries

- 5.3 By Geography

- 5.3.1 Production Analysis

- 5.3.1.1 China

- 5.3.1.2 Russia

- 5.3.1.3 Philippines

- 5.3.1.4 Rest of the World

- 5.3.2 Consumption Analysis

- 5.3.2.1 United States

- 5.3.2.2 China

- 5.3.2.3 Russia

- 5.3.2.4 Japan

- 5.3.2.5 Brazil

- 5.3.2.6 European Union

- 5.3.2.7 Rest of the World

- 5.3.1 Production Analysis

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Ardea Resources

- 6.4.2 Guangxi Maoxin Technology Co., Ltd

- 6.4.3 Henan Rongjia Scandium Vanadium Technology Co., Ltd

- 6.4.4 Huizhou Top Metal Materials Co., Ltd.

- 6.4.5 Hunan Oriental Scandium Co., Ltd.

- 6.4.6 Hunan Rare Earth Metal Materials Research Institute Co. Ltd.

- 6.4.7 JSC Dalur

- 6.4.8 MCC Group

- 6.4.9 Niocorp Development Ltd.

- 6.4.10 Rio Tinto

- 6.4.11 Rusal

- 6.4.12 Scandium Canada Ltd.

- 6.4.13 Scandium International Mining Corporation

- 6.4.14 Stanford Advanced Materials

- 6.4.15 Sumitomo Metal Mining Co., Ltd.

- 6.4.16 Sunrise Energy Metals Limited

- 6.4.17 Treibacher Industrie Ag

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment