|

市場調查報告書

商品編碼

1939017

清潔劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Detergents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

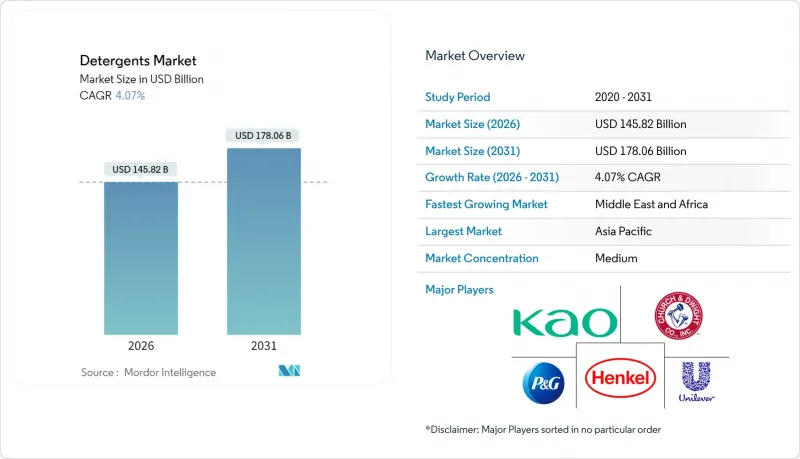

2025年清潔劑市值為1,401.2億美元,預計到2031年將達到1,780.6億美元,而2026年為1,458.2億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 4.07%。

結構性轉變的促進因素包括:可降低家庭能源消耗的冷水酶、促進超濃縮產品發展的碳定價政策,以及加速生物分解界面活性劑普及的監管要求。亞太地區由於洗衣機的快速普及,持續推動市場需求;而北美和中國的直銷訂閱服務正在重塑「最後一公里」經濟格局。競爭仍然激烈,寶潔、聯合利華和漢高等公司利用酵素技術和濃縮洗衣凝珠來維持高階定價。同時,一些區域性專業公司憑藉迎合家庭預算緊張需求的袋裝包裝,正在贏得市場佔有率。棕櫚仁油和酵素等原料成本的波動正在擠壓中端品牌的利潤空間,促使它們投資於藻類和發酵基界面活性劑,以規避供應限制。

全球清潔劑市場趨勢與洞察

新興經濟體洗衣機普及率不斷上升

在印度,預計自動洗衣機的擁有率將從2020年的14%上升到2024年的28%,這將導致人均清潔劑用量增加。這是因為滾筒式洗衣機比手洗洗衣機需要多30-40%的清潔劑。小包裝的250毫升液體洗滌劑和10次用量的洗滌劑袋既能降低成本,又能維持40%以上的利潤率。在印尼和越南,由於家電補貼和分期付款計畫的推動,自動洗衣機的普及曲線也與印度類似。目前,配方師建議使用針對30分鐘、20°C洗滌程序最佳化的酵素。BASF的Rubbergy蛋白酶在去除污漬方面效果相當,但耗能卻降低了35%。

清潔劑產業電子商務和D2C通路的快速成長

預計到2024年,消費者訂閱市場規模將達到42億美元,年增38%,主要得益於品牌方避免了零售商25%至35%的加價。較低的獲客成本(每位用戶18美元)以及第三次配送後低於15%的解約率,都為盈利提供了保障。北美地區線上銷售額佔比達32%,中國則高達41%,這主要得益於當日達物流和強調成分透明度的網紅行銷。濃縮型清潔劑凝珠和洗衣片重量減輕了70%,節省了0.12美元的最後一公里配送成本,並減少了60%的包裝廢棄物。

嚴格的國際和地方化學品法規

2023年10月,歐洲化學品管理局(ECHA)頒布了REACH法規附件十七,限制微塑膠的使用,並禁止在沖洗型清潔劑中故意使用微塑膠。過渡期為4至12年。 2024年4月,美國環保署(EPA)擴大了其PFAS法規的適用範圍,要求製造商證明界面活性劑和加工助劑中全氟烷基和多氟烷基物質的含量不超過十億分之一。這實際上禁止在工業和商用清潔產品中使用傳統的含氟表面活性劑。這些法規對缺乏研發預算進行快速配方調整的中小型區域品牌造成了不成比例的影響。同時,跨國公司可以將合規成本分攤到其每年超過50萬噸的全球產量中。

細分市場分析

到2025年,陰離子界面活性劑將佔據清潔劑市場45.84%的佔有率,這主要得益於低成本的直鏈烷基苯磺酸鹽,它們支撐著粉狀和液體清潔劑在南亞和非洲的主導地位。非離子醇乙氧基化物和烷基聚葡萄糖苷因其快速的最終生物分解性而備受青睞,預計其複合年成長率將達到4.95%,這主要受歐盟「28天內好氧分解」法規的推動。 2024年,漢高公司對Persil Sensitive洗滌劑進行了配方改良,用源自玉米澱粉的烷基多醣苷取代了40%的直鏈烷基聚葡萄糖苷,在保持產品性能的同時,將水生毒性降低了35%。

陽離子季銨鹽界面活性劑在織物柔順劑以外的應用較為有限,因為其正電荷限制了它們與陰離子界面活性劑的共配製能力。美國環保署(EPA)對季銨化合物的監管力度加大,促使人們開始試辦推廣更易生物分解的酯類季銨鹽替代品。兩性離子椰油醯胺丙基甜菜鹼預計在2024年將佔6%的使用量,用於穩定中東和北非硬水市場的泡沫。其寬廣的pH穩定性也使其適用於避免使用礦物螯合劑的冷水洗滌劑。

區域分析

到2025年,亞太地區將佔全球總量的44.10%,這主要得益於印度和印尼洗衣機擁有量翻番、中國電子商務的蓬勃發展以及消費者對高階酶清潔劑的需求成長。藍月(Blue Moon)和利比(Libbey)等本土領導品牌佔據了中國液體清潔劑市場38%的佔有率,這主要得益於線上直銷和特色香型產品。預計2024年印度市場將成長7.2%,這主要得益於針對首次購買洗衣機用戶的250毫升經濟型包裝。在日本和韓國等成熟市場,生物基羥乙磺酸界面活性劑因其能將污漬分解速度提高30%而備受關注。

預計中東和非洲地區的成長率將達到最高,為4.78%,由於都市化,人均消費量將超過3公斤。沙烏地阿拉伯的「2030願景」基礎建設正推動洗衣機普及率接近65%,從而提振了硬水洗滌劑的需求。預計到2024年,南非市場銷售量將成長5.8%,這主要得益於酵素強化型粉狀清潔劑的推廣,即使在電力供應不穩定的情況下,低溫洗滌也能保持良好的清潔效果。雖然袋裝粉狀清潔劑在撒哈拉以南非洲農村地區仍是主流,但由於前置裝載機洗衣機的普及,拉各斯和內羅畢等地對液體清潔劑的需求正在不斷成長。

歐洲和北美的成長速度放緩,但在永續性創新方面處於領先地位。在德國,獲得生態認證的產品將在2024年佔清潔劑銷售額的42%。在美國,洗衣凝珠和洗衣片將佔洗衣總量的32%,而加拿大和英國超市的補充裝服務將減少40%的包裝用量。南美洲預計在2024年成長4.2%。粉狀清潔劑仍將佔據68%的市場佔有率,但在巴西和阿根廷的都市區,液體清潔劑正在上升,這兩個國家的洗衣機擁有率超過55%。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 新興經濟體洗衣機普及率不斷上升

- 清潔劑產業電子商務和D2C通路的快速成長

- 消費者轉向環保和可生物分解配方

- 冷水酶技術的突破降低了能源消耗

- 碳排放稅增加了對超高濃度產品的需求

- 市場限制

- 嚴格的全球和地方化學品法規

- 原料價格波動(界面活性劑、酵素)

- 強制性微塑膠過濾導致配方改良成本增加

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按類型

- 陰離子清潔劑

- 陽離子界面清潔劑

- 非離子型清潔劑

- 兩性界面活性劑

- 透過使用

- 洗衣精

- 家用清潔劑

- 洗碗產品

- 燃油添加劑

- 生物試劑

- 其他用途

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 俄羅斯

- 西班牙

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Blue Moon Group

- Church & Dwight Co., Inc.

- Guangzhou Liby Group Co. Ltd

- Henkel AG & Co. KGaA

- Johnson & Johnson Private Limited

- Kao Corporation

- Lion Corporation

- Nice Group

- Procter & Gamble

- Reckitt Benckiser Group plc

- RSPL Group

- SC Johnson

- Seventh Generation Inc.

- Unilever

第7章 市場機會與未來展望

The Detergents Market was valued at USD 140.12 billion in 2025 and estimated to grow from USD 145.82 billion in 2026 to reach USD 178.06 billion by 2031, at a CAGR of 4.07% during the forecast period (2026-2031).

Structural shifts stem from cold-water enzymes that reduce household energy use, carbon-pricing policies favoring ultra-concentrated formats, and regulatory mandates that accelerate the adoption of biodegradable surfactants. The Asia-Pacific region continues to drive demand, largely due to the rapid adoption of washing machines, while direct-to-consumer (D2C) subscription services are redefining last-mile economics in North America and China. Competitive intensity remains high: Procter & Gamble, Unilever, and Henkel leverage enzyme technology and concentrated pods to command premium pricing, whereas regional specialists gain share with sachet distribution that meets tight household budgets. Input-cost volatility in palm-kernel oil and enzymes compresses margins for mid-tier brands yet hastens investment in algae-derived and fermentation-based surfactants that bypass constrained supply chains.

Global Detergents Market Trends and Insights

Rising Washing-Machine Penetration in Emerging Economies

Automatic washer ownership in India increased from 14% in 2020 to 28% in 2024, resulting in a rise in per-capita detergent usage, as drum cycles require 30%-40% more product than hand-washing. Smaller 250ml liquid packs and 10-wash sachets help keep entry prices low while sustaining margins above 40%. Similar adoption curves in Indonesia and Vietnam benefit from appliance subsidies and installment-payment schemes. Formulators now specify enzymes optimized for 30-minute, 20°C cycles, with BASF's Lavergy protease delivering equivalent stain removal at 35% lower energy consumption.

Boom in E-Commerce and D2C Channels for Detergents

Direct-to-consumer subscriptions generated USD 4.2 billion in 2024, representing a 38% year-over-year growth as brands bypass retailers' 25%-35% markup. Lower acquisition costs (USD 18 per subscriber) and churn below 15% after the third delivery underpin profitability. Online sales reached 32% in North America and 41% in China, driven by same-day logistics and influencer marketing that emphasize ingredient transparency. Concentrated pods and strips, 70% lighter than equivalent liquids, shave USD 0.12 from last-mile freight while reducing packaging waste by 60%.

Stringent Global and Regional Chemical Regulations

In October 2023, the European Chemicals Agency, under REACH Annex XVII, restricted microplastics, banning their intentional use in rinse-off detergents with transition periods of 4 to 12 years. In April 2024, the US Environmental Protection Agency expanded PFAS restrictions, requiring manufacturers to certify that surfactants and processing aids contain no per- and polyfluoroalkyl substances above 1 part per billion, effectively banning legacy fluorosurfactants in industrial and institutional cleaning products. These regulations disproportionately affect smaller regional brands, which lack the R&D budgets for rapid reformulation, while multinationals spread compliance costs over global volumes exceeding 500,000 metric tons annually.

Other drivers and restraints analyzed in the detailed report include:

- Consumer Shift to Eco-Friendly and Biodegradable Formulations

- Cold-Water Enzyme Breakthroughs Cut Energy Use

- Raw-Material Price Volatility (Surfactants, Enzymes)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Anionic surfactants held 45.84% of the Detergents market share in 2025, supported by low-cost linear alkylbenzene sulfonates that anchor powder and liquid staples in South Asia and Africa. Non-ionic alcohol ethoxylates and alkyl polyglucosides, prized for rapid ultimate biodegradation, are forecast to grow at a 4.95% CAGR, lifted by EU rules requiring aerobic breakdown within 28 days. Henkel reformulated Persil Sensitive in 2024 by substituting 40% of LAS with corn-starch-derived alkyl polyglucosides, thereby lowering aquatic toxicity by 35% while retaining the product's performance.

Cationic quaternary ammonium surfactants remain niche outside fabric softeners because their positive charge limits co-formulation with anionics. EPA scrutiny of quats is prompting pilots of faster-biodegrading ester-quat alternatives. Zwitterionic cocamidopropyl betaine, 6% of 2024 volume, stabilizes foam in hard-water markets across the Middle East and North Africa, and its broad pH stability suits cold-water pods that avoid mineral chelators.

The Detergents Market Report is Segmented by Type (Anionic, Cationic, Non-Ionic, and Zwitterionic), Application (Laundry, Household Cleaning, Dishwashing, Fuel Additives, Biological Reagents, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

The Asia-Pacific region accounted for 44.10% of the global 2025 volume, driven by a doubling of washing-machine ownership in India and Indonesia, robust e-commerce in China, and a shift toward premiumization of enzyme-rich liquids. Local champions such as Blue Moon and Liby hold a 38% share of China's liquid category through direct online engagement and tailored fragrances. India's market expanded by 7.2% in 2024, driven by affordable 250 ml packs targeting first-time machine users. Mature Japan and South Korea focus on bio-based isethionate surfactants that accelerate soil release by 30%.

The Middle East & Africa are forecast to deliver the fastest growth, with a 4.78% CAGR, as urbanization lifts per-capita consumption above 3 kg. Saudi Arabia's Vision 2030 infrastructure push raises washer penetration toward 65%, spurring demand for hard-water-tolerant pods. South Africa's market increased by 5.8% in volume in 2024, driven by enzyme-fortified powders that perform well in cold cycles, a necessity amid intermittent electricity supply. Sachet-priced powders dominate rural Sub-Saharan Africa, but liquid formats are gaining traction in Lagos and Nairobi as front-load adoption increases.

Europe and North America register slower growth but lead sustainability innovation. Germany's eco-labeled segment reached 42% of 2024 detergent sales. US pods and strips command 32% of laundry volume, and refill stations in Canadian and UK grocers reduce packaging by 40%. South America grew by 4.2% in 2024; powders still hold a 68% share, but liquids are rising in urban Brazil and Argentina, alongside washer ownership above 55%.

- Blue Moon Group

- Church & Dwight Co., Inc.

- Guangzhou Liby Group Co. Ltd

- Henkel AG & Co. KGaA

- Johnson & Johnson Private Limited

- Kao Corporation

- Lion Corporation

- Nice Group

- Procter & Gamble

- Reckitt Benckiser Group plc

- RSPL Group

- SC Johnson

- Seventh Generation Inc.

- Unilever

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising washing-machine penetration in emerging economies

- 4.2.2 Boom in e-commerce and D2C channels for detergents

- 4.2.3 Consumer shift to eco-friendly/biodegradable formulations

- 4.2.4 Cold-water enzyme breakthroughs cut energy use

- 4.2.5 Carbon-tax driven demand for ultra-concentrates

- 4.3 Market Restraints

- 4.3.1 Stringent global and regional chemical regulations

- 4.3.2 Raw-material price volatility (surfactants, enzymes)

- 4.3.3 Micro-plastic filtration mandates raise reformulation costs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Anionic Detergents

- 5.1.2 Cationic Detergents

- 5.1.3 Non-ionic Detergents

- 5.1.4 Zwitterionic (Amphoteric) Detergents

- 5.2 By Application

- 5.2.1 Laundry Cleaning Products

- 5.2.2 Household Cleaning Products

- 5.2.3 Dishwashing Products

- 5.2.4 Fuel Additives

- 5.2.5 Biological Reagents

- 5.2.6 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Spain

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Blue Moon Group

- 6.4.2 Church & Dwight Co., Inc.

- 6.4.3 Guangzhou Liby Group Co. Ltd

- 6.4.4 Henkel AG & Co. KGaA

- 6.4.5 Johnson & Johnson Private Limited

- 6.4.6 Kao Corporation

- 6.4.7 Lion Corporation

- 6.4.8 Nice Group

- 6.4.9 Procter & Gamble

- 6.4.10 Reckitt Benckiser Group plc

- 6.4.11 RSPL Group

- 6.4.12 SC Johnson

- 6.4.13 Seventh Generation Inc.

- 6.4.14 Unilever

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

清潔劑化學品市場:按技術、產品類型、劑型、最終用戶、分銷管道和應用分類-2026-2032年全球市場預測

清潔劑化學品市場:按技術、產品類型、劑型、最終用戶、分銷管道和應用分類-2026-2032年全球市場預測 2026年全球可生物分解清潔劑市場報告2026年全球天然葉醇市場報告

2026年全球可生物分解清潔劑市場報告2026年全球天然葉醇市場報告 清潔劑化學品市場分析及預測(至2035年):依類型、產品類型、應用、劑型、材料類型、製程、最終用戶、功能及技術分類清潔劑酒精市場分析及預測(至2035年):類型、產品類型、應用、劑型、材料類型、製程、技術、最終用戶、功能、解決方案

清潔劑化學品市場分析及預測(至2035年):依類型、產品類型、應用、劑型、材料類型、製程、最終用戶、功能及技術分類清潔劑酒精市場分析及預測(至2035年):類型、產品類型、應用、劑型、材料類型、製程、技術、最終用戶、功能、解決方案 全球清潔劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球清潔劑化學品市場報告

全球清潔劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球清潔劑化學品市場報告 2026-2030年全球有機清潔劑市場天然葉醇市場按包裝類型、純度等級、萃取方法、銷售管道和應用分類-2026-2032年全球預測

2026-2030年全球有機清潔劑市場天然葉醇市場按包裝類型、純度等級、萃取方法、銷售管道和應用分類-2026-2032年全球預測 清潔劑酒精市場規模、佔有率和成長分析(按產品類型、碳鍊長度、應用、終端用戶產業和地區分類)-2026-2033年產業預測

清潔劑酒精市場規模、佔有率和成長分析(按產品類型、碳鍊長度、應用、終端用戶產業和地區分類)-2026-2033年產業預測