|

市場調查報告書

商品編碼

1939002

美國農業機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)United States Agricultural Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

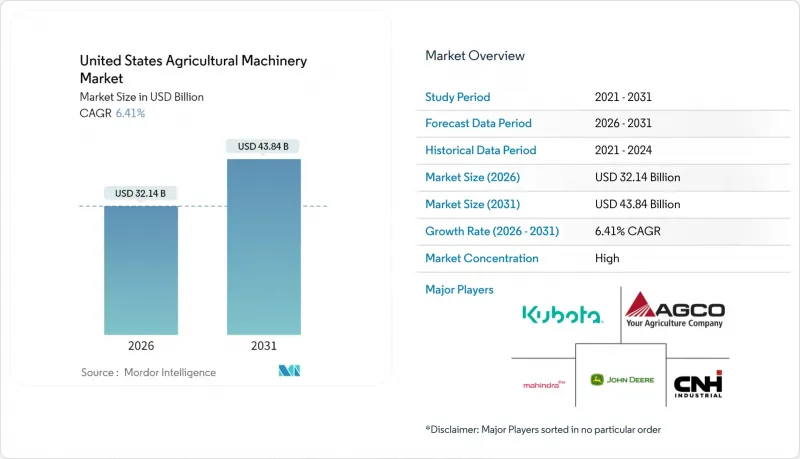

2025年美國農業機械市場價值為302億美元,預計到2031年將達到438.4億美元,高於2026年的321.4億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 6.41%。

聯邦政府對氣候友善實踐、精準技術改造和電氣化投資的激勵措施有助於抵消市場週期性波動。設備所有者正致力於提升永續性目標,這增加了對遠端資訊處理、預測性維護和自動駕駛系統的需求。經銷商整合正在改善售後服務網路,而租賃和訂閱方案則有助於緩解利率上升的影響。日益嚴重的水資源短缺和更嚴格的排放法規正在推動美國農機市場灌溉領域的強勁成長。

美國農機市場趨勢與洞察

擴大精密農業改裝套件的使用範圍

透過數據驅動的改進,改裝方案能夠幫助農民延長現有設備的使用壽命,同時減少高達 30% 的化肥和農藥用量。每台曳引機 5 萬美元的改裝投資遠低於購買全新自動駕駛設備所需的 40 萬美元,且投資回收期通常不到三年。中型農場正擴大採用這些方案,以在不增加債務的情況下保持成本競爭力。設備經銷商可以透過安裝和調試改造套件獲得附加服務收入,從而加強客戶關係並提高盈利。隨著模組化升級延長設備更換週期,原始設備製造商 (OEM) 正將重心從設備銷售轉向軟體和整合服務。

主要OEM廠商的電氣化藍圖

約翰迪爾計劃於2026年推出首款全電動自動駕駛曳引機,並已投資Kreisel Electric公司為其供應電池。 AGCO公司正在試行芬特e100 Vario電動曳引機,計畫於2024年投入使用,並計畫將研發投入增加60%,專注於研發電動動力傳動系統。目前電池的能量密度限制了電動曳引機的應用範圍,使其功率只能達到120馬力以下,足以滿足果園、蔬菜農場和酪農的需求。美國自然資源保護局(NRCS)提供一項成本分攤計劃,可涵蓋超過50%的購買成本,從而降低小規模農場的經濟負擔。製造商預計,未來電池技術的進步將使更高功率的應用成為可能,而目前的技術發展正推動零件供應商擴大在美國的電池和逆變器生產規模。

經銷商技術人員短缺

農業機械服務業正面臨嚴重的勞動力短缺。服務網點的整合減少了實體網點的數量,導致在關鍵的播種和收穫季節響應時間延長。現代精密農業機械需要先進的診斷能力,而當地勞動力市場無法滿足這些需求,迫使原始設備製造商(OEM)擴展遠端支援服務並引入模組化零件更換系統。這些勞動力限制正在阻礙農民購買農業機械。

細分市場分析

到2025年,曳引機將維持在美國農業機械市場50.62%的佔有率,這反映了其在犁地、播種和物料輸送的重要作用。該細分市場的收入成長主要由高功率機型推動,同時,小型曳引機在專業農業應用中採用電動驅動系統的比例也在不斷成長。灌溉設備雖然規模較小,但預期成長率最高,到2031年複合年成長率將達9.26%。現代灌溉系統,包括中心支軸式噴灌機、滴灌管線和感測器控制閥,整合了即時土壤濕度數據,可將用水量減少高達25%。這一成長與西部各州的地下水法規以及聯邦政府「節水智慧」(WaterSMART)計劃的獎勵相吻合。

在犁地系統中,製造商正採用可變深度耕作技術來減少土壤擾動,儘管犁地農業不斷擴張,但仍保持穩定的成長。先進的播種和種植設備實現了單粒播種,提高了發芽率和精準施肥。收割設備的需求與作物價格密切相關,但配備預測速度自動化功能的新型聯合收割機透過提高燃油效率和作業效率,推動了設備的更新換代需求。農民越來越傾向於升級現有設備,例如增加自動駕駛引導和變數施肥控制設備功能,而不是購買新設備,這使得零件和數位化業務收益超過了設備銷售額。在所有設備類別中,感測器系統和ISOBUS相容控制器正在建立品牌無關的生態系統,並降低製造商鎖定效應。這迫使傳統製造商提供開放的API,以維持其在曳引機市場的地位。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 精密農業改裝套件的廣泛應用

- 主要OEM廠商的電氣化藍圖

- 擴大遠端資訊處理技術在預測性維護的應用

- 氣候變遷津貼獎勵

- 客製化設備租賃模式的激增

- 創業投資的機器人Start-Ups瞄準特種作物

- 市場限制

- 經銷商技術人員短缺

- 遍遠地區連網機器的 5G 覆蓋不穩定

- 商品價格波動限制了農機設備的資本支出;

- 為滿足美國環保署 (EPA) Tier 5排放標準,需要較長的前置作業時間。

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依產品類型

- 聯結機

- 犁地機械

- 犁

- 光環

- 耕耘機

- 其他犁地和栽培機械

- 種植機械

- 播種機

- 播種機

- 撒佈器

- 其他播種機

- 收割機

- 結合

- 飼料收割機

- 其他收割機

- 乾草和飼料機械

- 割草機

- 打包機

- 其他牧場和飼料機械

- 灌溉機械

- 噴水灌溉

- 滴灌

- 其他灌溉機械

- 其他農業機械

- 按農場規模

- 不到500英畝

- 500至2000英畝

- 超過2000英畝

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Deere & Company

- CNH Industrial NV

- AGCO Corporation

- Kubota Corporation

- Mahindra & Mahindra Ltd.

- CLAAS KGaA mbH

- KUHN SAS

- Same Deutz-Fahr SPA

- Kinze Manufacturing

- Horsch, LLC

- Ploeger Oxbo Group BV

- Argo Tractors SpA

- Netafim Limited(An Orbia Business)

- Valmont Industries, Inc.

- Yanmar Holdings Co., Ltd.

第7章 市場機會與未來展望

The United States agricultural machinery market was valued at USD 30.2 billion in 2025 and estimated to grow from USD 32.14 billion in 2026 to reach USD 43.84 billion by 2031, at a CAGR of 6.41% during the forecast period (2026-2031).

Federal incentives for climate-smart practices, precision technology retrofits, and electrification investments help counterbalance cyclical market fluctuations. Equipment owners focus on upgrading capabilities to reduce operational costs and achieve sustainability goals, increasing demand for telematics, predictive maintenance, and autonomous-ready systems. Dealer consolidation improves after-sales service networks, while leasing and subscription options help mitigate the impact of higher interest rates. The irrigation segments demonstrate higher growth rates in the United States agricultural machinery market, driven by increasing water scarcity and stricter emissions regulations.

United States Agricultural Machinery Market Trends and Insights

Widespread Adoption of Precision-Ag Retro-Fit Kits

Retro-fit solutions enable farmers to extend their existing fleet's lifespan while reducing fertilizer and pesticide usage by up to 30% through data-driven improvements. The investment of USD 50,000 per tractor for retrofitting is significantly lower than the USD 400,000 required for new autonomous-ready equipment, typically resulting in a return on investment within three years. Mid-scale row-crop farms increasingly adopt these solutions to maintain cost competitiveness without increasing debt. Equipment dealers benefit from additional service revenue through installation and calibration of retrofit kits, which strengthens customer relationships and improves profitability. The growing adoption of modular upgrades extends equipment replacement cycles, causing Original Equipment Manufacturers (OEMs) to shift their focus from unit sales to software and integration services.

Electrification Road-Maps by Major Original Equipment Manufacturers

Deere & Company plans to launch its first all-electric, autonomous-capable tractor in 2026 and has invested in Kreisel Electric for battery supply. AGCO introduced the Fendt e100 Vario to pilot fleets in 2024, supported by a 60% increase in research and development spending focused on electric powertrains. Current battery density limits electric tractors to under-120-horsepower applications, which align with the requirements of fruit, vegetable, and dairy farms. The Natural Resources Conservation Service (NRCS) offers cost-share programs that can cover over 50% of purchase costs, reducing financial barriers for small farms. While manufacturers expect future battery technology improvements to enable higher-horsepower applications, current progress has encouraged component suppliers to expand United States battery and inverter production.

Dealer Technician Shortage

The equipment service industry faces a significant labor shortage. The consolidation of service locations has reduced the number of physical stores, increasing response times during critical planting and harvest periods. Modern precision equipment requires specialized diagnostic capabilities that exceed the skills available in rural labor markets, compelling Original Equipment Manufacturers (OEMs) to expand remote support services and implement modular component replacement systems. These labor constraints have led farmers to restrict their purchases of agricultural machinery.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of Telematics-Based Predictive Maintenance

- Climate-Smart Grant Incentives

- Lengthy Environmental Protection Agency Tier 5 Emission Compliance Lead-Times

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tractors maintain a 50.62% share of the United States agricultural machinery market in 2025, demonstrating their essential role in tillage, seeding, and material handling. The segment's revenue growth stems from high-horsepower models, while compact tractors increasingly incorporate electric drivetrains for specialty farming applications. Irrigation equipment, though a smaller segment, is projected to achieve the highest growth rate at 9.26% CAGR through 2031. Modern irrigation systems, including center pivots, drip lines, and sensor-controlled valves, integrate real-time soil moisture data, reducing water consumption by up to 25%. This growth aligns with Western state groundwater regulations and federal WaterSMART program incentives.

In plowing and cultivating systems, manufacturers incorporate variable-depth tillage technology to reduce soil disruption, maintaining steady growth despite increasing no-till farming practices. Advanced seeding and planting equipment enable precise single-kernel placement, improving emergence rates and supporting precise nutrient application. While harvesting machinery demand correlates with row-crop prices, new combines featuring predictive ground-speed automation improve fuel efficiency and throughput, driving replacement demand. Farmers increasingly opt to upgrade existing equipment with autonomous guidance and variable-rate controllers instead of purchasing new machinery, resulting in parts and digital service revenue exceeding equipment sales. Across equipment categories, sensor systems and ISOBUS-compatible controllers establish brand-independent ecosystems, reducing manufacturer lock-in and requiring traditional manufacturers to provide open APIs to maintain tractor market position.

The United States Agricultural Machinery Market Report is Segmented by Product Type (Tractors, Plowing and Cultivating Machinery, and More), and by Farm Size (Less Than 500 Acres, 500-2, 000 Acres, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Deere & Company

- CNH Industrial NV

- AGCO Corporation

- Kubota Corporation

- Mahindra & Mahindra Ltd.

- CLAAS KGaA mbH

- KUHN SAS

- Same Deutz-Fahr S.P.A.

- Kinze Manufacturing

- Horsch, LLC

- Ploeger Oxbo Group B.V.

- Argo Tractors S.p.A.

- Netafim Limited (An Orbia Business)

- Valmont Industries, Inc.

- Yanmar Holdings Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Widespread Adoption of Precision-Ag Retro-Fit Kits

- 4.2.2 Electrification Road-Maps by Major Original Equipment Manufacturers

- 4.2.3 Rising Adoption of Telematics-Based Predictive Maintenance

- 4.2.4 Climate-Smart Grant Incentives

- 4.2.5 Surge in Bespoke Equipment Leasing Models

- 4.2.6 Venture-Backed Robotics Start-Ups Targeting Speciality Crops

- 4.3 Market Restraints

- 4.3.1 Dealer Technician Shortage

- 4.3.2 Patchy Rural 5G Coverage for Connected Machinery

- 4.3.3 Volatile Commodity-Price Swings Curbing Farm Capital Expenditure

- 4.3.4 Lengthy Environmental Protection Agency Tier 5 Emission Compliance Lead-times

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Tractors

- 5.1.2 Plowing and Cultivating Machinery

- 5.1.2.1 Plows

- 5.1.2.2 Harrows

- 5.1.2.3 Cultivators and Tillers

- 5.1.2.4 Other Plowing and Cultivating Machinery

- 5.1.3 Planting Machinery

- 5.1.3.1 Seed Drills

- 5.1.3.2 Planters

- 5.1.3.3 Spreaders

- 5.1.3.4 Other Planting Machinery

- 5.1.4 Harvesting Machinery

- 5.1.4.1 Combine Harvesters

- 5.1.4.2 Forage Harvesters

- 5.1.4.3 Other Harvesting Machinery

- 5.1.5 Haying and Forage Machinery

- 5.1.5.1 Mowers

- 5.1.5.2 Balers

- 5.1.5.3 Other Haying and Forage Machinery

- 5.1.6 Irrigation Machinery

- 5.1.6.1 Sprinkler Irrigation

- 5.1.6.2 Drip Irrigation

- 5.1.6.3 Other Irrigation Machinery

- 5.1.7 Other Agricultural Machinery

- 5.2 By Farm Size

- 5.2.1 Less Than 500 acres

- 5.2.2 500-2,000 acres

- 5.2.3 More Than 2,000 acres

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 CNH Industrial NV

- 6.4.3 AGCO Corporation

- 6.4.4 Kubota Corporation

- 6.4.5 Mahindra & Mahindra Ltd.

- 6.4.6 CLAAS KGaA mbH

- 6.4.7 KUHN SAS

- 6.4.8 Same Deutz-Fahr S.P.A.

- 6.4.9 Kinze Manufacturing

- 6.4.10 Horsch, LLC

- 6.4.11 Ploeger Oxbo Group B.V.

- 6.4.12 Argo Tractors S.p.A.

- 6.4.13 Netafim Limited (An Orbia Business)

- 6.4.14 Valmont Industries, Inc.

- 6.4.15 Yanmar Holdings Co., Ltd.

7 Market Opportunities and Future Outlook

除草機器人市場:按組件、類型、運作方式、銷售管道、應用和最終用途分類-2026-2032年全球市場預測農作物殘渣處理機械市場:按類型、機械化程度、動力來源、應用、最終用途和分銷管道分類-2026-2032年全球市場預測

除草機器人市場:按組件、類型、運作方式、銷售管道、應用和最終用途分類-2026-2032年全球市場預測農作物殘渣處理機械市場:按類型、機械化程度、動力來源、應用、最終用途和分銷管道分類-2026-2032年全球市場預測 2026年全球自主作物殘茬管理機器人市場報告農業橡膠履帶市場:2026-2032年全球市場預測(依應用程式、銷售管道、履頻寬度、橡膠配方類型、履帶長度及最終用戶類型分類)

2026年全球自主作物殘茬管理機器人市場報告農業橡膠履帶市場:2026-2032年全球市場預測(依應用程式、銷售管道、履頻寬度、橡膠配方類型、履帶長度及最終用戶類型分類) 自主農業車輛市場:策略性洞察與預測(2026-2031年)溶離設備市場:2026-2032年全球市場預測(依設備類型、自動化程度、技術、應用、最終用戶及銷售管道)農業和施工機械市場:按產品類型、功率範圍、引擎類型、應用、最終用戶和分銷管道分類——2026-2032年全球預測穀物螺旋輸送機市場:按類型、動力來源、容量、應用、最終用戶和分銷管道分類-2026-2032年全球預測紅外線瀝青加熱器市場:按產品類型、電源、移動性、應用、最終用戶、分銷管道分類,全球預測(2026-2032年)

自主農業車輛市場:策略性洞察與預測(2026-2031年)溶離設備市場:2026-2032年全球市場預測(依設備類型、自動化程度、技術、應用、最終用戶及銷售管道)農業和施工機械市場:按產品類型、功率範圍、引擎類型、應用、最終用戶和分銷管道分類——2026-2032年全球預測穀物螺旋輸送機市場:按類型、動力來源、容量、應用、最終用戶和分銷管道分類-2026-2032年全球預測紅外線瀝青加熱器市場:按產品類型、電源、移動性、應用、最終用戶、分銷管道分類,全球預測(2026-2032年) 農業設備市場規模、佔有率、趨勢和預測:按設備類型、應用、銷售管道和地區分類,2026-2034年

農業設備市場規模、佔有率、趨勢和預測:按設備類型、應用、銷售管道和地區分類,2026-2034年