|

市場調查報告書

商品編碼

1938986

瀝青:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Bitumen - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

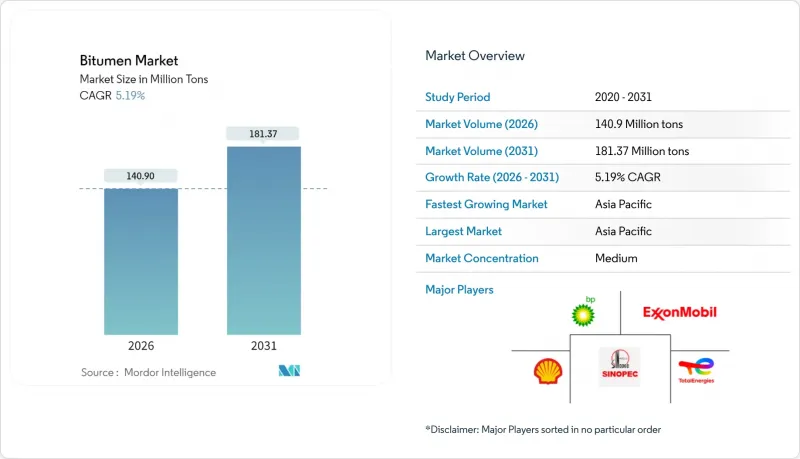

預計瀝青市場將從 2025 年的 1.3395 億噸成長到 2026 年的 1.409 億噸,到 2031 年將達到 1.8137 億噸,2026 年至 2031 年的複合年成長率為 5.19%。

公共部門在高速公路、機場跑道和氣候適應型路面方面的支出不斷增加,支撐了長期需求,而聚合物改質複合技術則開闢了一片利潤豐厚的市場。 2024年原油價格的穩定性為原料成本提供了可預測性,但預計到2026年原油價格將跌至每桶66美元,這可能會同時擴大生產利潤空間並加劇價格競爭。亞太地區仍然是主要的消費中心,這得益於積極的基礎設施投資和靈活的進口戰略,該戰略充分利用了中東產油國的價格優勢。同時,日益嚴格的環境法規正在加速向冷乳化瀝青和再生瀝青技術的轉型,從而微妙地改變瀝青市場的供應鏈和產品規格。

全球瀝青市場趨勢與洞察

道路和高速公路維修成本增加

世界各國政府正在將預算從新建設重新分配到道路維護,從而帶動透水性黏合劑和特殊路面處理材料的持續穩定消耗。美國《基礎設施投資與就業法案》已啟動超過6萬個建設計劃,僅魁北克省就在其2025-2026會計年度預算中累計358.68億加元用於道路維護。各機構體認到,及時維護的每一美元投資都能減少未來4至7美元的重組成本,進而形成維護需求的良性循環。德國5000億歐元的現代化基金將20%用於資產最佳化,並納入耐久性標準,進一步提升了氣候智慧型瀝青的性能。隨著路面管理系統的日趨成熟,採購模式正從週期性高峰轉向可預測的多年期契約,從而穩定了整個瀝青市場的採購量。

大型機場跑道擴建計劃

跑道建設計劃需要高品質的黏合劑,以承受高輪載、剪切應力和噴射機燃料洩漏。一項由沿岸地區和亞洲樞紐機場主導的、總額達7300億美元的2030年前資本支出計劃,將能源基礎設施與航空設施擴建聯繫起來。法蘭克福機場一項為期兩年的試驗路段採用腰果殼生物瀝青,顯示航空公司希望在不影響性能的前提下使用低碳材料。苯乙烯-丁二烯-苯乙烯(SBSS)聚合物改質瀝青的價格溢價高達15-25%,儘管產量仍然有限,但該細分市場的盈利卻得到了提升。能夠使其混合料設計符合國際民航組織(ICAO)標準的供應商,將更有機會贏得長期框架契約,從而加強瀝青市場的垂直整合策略。

加強對鋪路作業中溫室氣體 (GHG) 和多環芳烴 (PAH)排放的監管

監管機構正在收緊揮發性有機化合物 (VOC) 和多環芳烴 (PAH) 的暴露限值。加拿大將於 2025 年 10 月前禁止使用 PAH 含量超過 1000 ppm 的煤焦油基密封劑,這將有效地淘汰現有產品線並迫使其重新配方。結合氣相層析法和監督學習的預測分析技術現在可以識別產生異味的烷烴,從而為符合監管要求提供途徑。然而,這增加了分析成本,給小型生產商帶來了負擔。各機構也擴大採用溫拌瀝青技術,可將路面溫度降低高達 40°C。這減少了現場排放,並縮小了熱拌瀝青的應用範圍,限制了瀝青市場的需求成長。

細分市場分析

2025年,滲透級瀝青黏合劑佔據了瀝青市場66.52%的佔有率,預計到2031年將以5.62%的複合年成長率成長,這主要得益於其與傳統熱拌瀝青攪拌站的兼容性以及廣泛的氣候適應性。氧化級瀝青則用於防水和屋頂等特殊應用領域,其優異的氧化穩定性使其價格更高。瀝青乳液在全球的年產量達800萬噸,由於其排放更低、排放更少,在碎石封層和微表面處理應用中越來越受歡迎。

創新主要集中在黏度控制和環保添加劑方面。添加1%的聚磷酸鹽可以提高高溫穩定性,但超過2%則會降低儲存穩定性。生物基因改質劑,例如伊朗天然瀝青,可以提高黏度和熱塑性,延長使用壽命並減少對合成聚合物的依賴。這些漸進式改善維持了針入度等級瀝青的主導地位,同時也逐步將瀝青市場的價值轉移到特種混合料上。

瀝青市場報告按產品類型(針入度等級、氧化等級、瀝青乳液、聚合物改質瀝青及其他產品)、應用領域(道路建設、屋頂工程、黏合劑和密封劑及其他應用)以及地區(亞太地區、北美地區、歐洲地區、南美地區以及中東和非洲地區)進行細分。市場預測以噸為單位。

區域分析

亞太地區將引領市場,到2025年將佔據45.10%的市場佔有率,並在2031年之前以6.31%的複合年成長率成長,這主要得益於中國、印度和東南亞同步推進的基礎設施建設規劃。中國2023年原油日加工量將達到1,480萬桶,這將支撐國內瀝青供應和出口能力。

在北美,強勁的道路維修預算與不斷變化的環境法規正在努力平衡。受《基礎設施投資與就業法案》(IIJA) 的影響,管道需求保持穩定,而加拿大即將訂定的多環芳烴(PAH)法規正推動瀝青生產轉向乳化瀝青和冷加工製程。在歐洲,煉油廠的合理化和關閉導致區域供應趨緊,同時也為生物基替代品創造了市場機會。歐洲瀝青市場噸位可能略有下降,但隨著特種瀝青的需求超過以金額為準瀝青,預計其價值將會增加。

中東地區擁有豐富的原料和戰略性航運路線,為亞洲提供供應。預計到2030年,海灣產油國與亞洲買家之間的貿易額將達到6,820億美元,其中包括原油、成品黏合劑和改質劑。

作為新興市場,非洲和南美洲的特徵是週期性地大型企劃,從而帶動需求激增。隨著這些地區擴大互聯互通投資,擁有靈活物流和快速部署能力的供應商可能會變得更加重要。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 道路和高速公路維修成本增加

- 大規模機場跑道擴建計劃

- 新興經濟體政府主導的基礎設施獎勵策略

- 向聚合物改質瀝青過渡,打造氣候適應路面

- 透過推廣循環經濟來促進再生瀝青路面(RAP)的採用。

- 市場限制

- 針對鋪路作業制定嚴格的溫室氣體 (GHG) 和多環芳烴 (PAH)排放法規

- 原油價格波動影響原物料經濟

- 城市計劃中混凝土和複合材料路面的比例不斷增加

- 價值鏈分析

- 原料分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依產品類型

- 滲透

- 氧化級

- 瀝青乳化劑

- 聚合物改質瀝青

- 其他產品(黏度等級、稀釋等級、性能等級)

- 透過使用

- 道路建設

- 屋頂材料

- 黏合劑和密封劑

- 其他應用領域(石油和天然氣領域的塗層、運河襯砌、儲槽基礎、鐵路道安定器處理等)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 亞太其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購/合資/合約)

- 市佔率(%)/排名分析

- 公司簡介

- BMI Group Holdings UK Limited

- BP plc

- China Petroleum and Chemical Corporation(Sinopec)

- ENEOS Corporation

- Exxon Mobil Corporation

- Hindustan Petroleum Corporation Limited

- Indian Oil Corporation Ltd

- Kraton Corporation

- Mangalore Refinery and Petrochemicals Limited

- Marathon Petroleum Corporation

- Nynas AB

- Rosneft

- Shell plc

- Suncor Energy Inc.

- The Bouygues Group

- TotalEnergies

第7章 市場機會與未來展望

The Bitumen Market is expected to grow from 133.95 Million tons in 2025 to 140.9 Million tons in 2026 and is forecast to reach 181.37 Million tons by 2031 at 5.19% CAGR over 2026-2031.

Heightened public-sector spending on highways, airport runways, and climate-resilient pavements is sustaining long-run demand, while polymer-modified formulations open higher-margin niches. Stable crude-oil prices in 2024 created predictable feedstock economics, yet the projected slide to USD 66 per barrel by 2026 could both widen production margins and intensify price competition. Asia-Pacific remains the pivotal consumption hub, boosted by aggressive infrastructure outlays and flexible import strategies that exploit Middle-Eastern price discounts. Concurrently, environmental regulations accelerate the transition toward low-temperature emulsions and recycled asphalt technologies, subtly reshaping supply chains and product specifications within the bitumen market.

Global Bitumen Market Trends and Insights

Increasing Road and Highway Rehabilitation Spend

Governments are reallocating budgets from new builds toward preservation, leading to steady recurrent consumption of penetration-grade binders and specialty surface treatments. The U.S. Infrastructure Investment and Jobs Act has already launched more than 60,000 construction projects, and Quebec alone earmarked CAD 35.868 billion for roads in its 2025-2026 budget. Agencies recognize that every dollar invested in timely preservation avoids USD 4-7 in future reconstruction costs, locking in a virtuous cycle of maintenance demand. Germany's EUR 500 billion modernization fund assigns 20% to asset optimization, embedding resilience criteria that further elevate specifications for climate-adaptive bitumen grades. As pavement management systems mature, procurement shifts from cyclical surges to predictable multi-year contracts, stabilizing volume offtake across the bitumen market.

Large-Scale Airport Runway Expansion Programs

Runway projects require premium binders that tolerate high wheel loads, shear stresses, and jet-fuel spills. Gulf and Asian hubs are leading a USD 730 billion capex wave through 2030, intertwining energy infrastructure with aviation build-outs. Frankfurt Airport's two-year test strip using cashew-shell bio-bitumen illustrates airlines' push for lower-carbon materials without performance sacrifice. Polymer-modified grades with styrene-butadiene-styrene command price premiums of 15-25%, lifting segment profitability even though volumes remain modest. Suppliers capable of certifying mix designs to International Civil Aviation Organization standards are positioned to capture long-run framework agreements, reinforcing vertical integration strategies within the bitumen market.

Stringent GHG and PAH Emission Regulations on Paving Operations

Regulators are tightening exposure limits for volatile organic compounds and polycyclic aromatic hydrocarbons. Canada will prohibit coal-tar sealants exceeding 1,000 ppm PAHs by October 2025, effectively removing a traditional product class and forcing reformulations. Predictive analytics using gas chromatography coupled with supervised learning now pinpoint odor-causing alkanes, offering compliance pathways but raising analytical costs that smaller producers must absorb. Agencies also favor warm-mix technologies that lower placement temperatures by up to 40 °C, reducing on-site emissions and tightening the operating envelope for hot-mix asphalt, thereby constraining volume expansion in the bitumen market.

Other drivers and restraints analyzed in the detailed report include:

- Government Infrastructure Stimulus in Emerging Economies

- Shift to Polymer-Modified Bitumen for Climate-Resilient Pavements

- Crude-Oil Price Volatility Impacting Feedstock Economics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Penetration-grade binders held 66.52% of the bitumen market share in 2025 and are projected to grow at a 5.62% CAGR through 2031, sustained by compatibility with conventional hot-mix plants and broad climatic tolerance. Oxidized grades occupy niche waterproofing and roofing roles where oxidation stability justifies premium pricing. Bitumen emulsions, totaling 8 million tons globally, are gaining favor for chip seals and microsurfacing because they reduce energy use and lower work-zone emissions.

Innovation centers on viscosity control and ecological additives. Polyphosphoric acid at 1% dosage improves high-temperature stability, though concentrations beyond 2% can undermine storage stability. Bio-based modifiers such as Iranian natural asphalt enhance viscosity and thermoplasticity, extending service life and reducing reliance on synthetic polymers. These incremental gains sustain penetration-grade primacy but gradually shift value toward specialty formulations inside the bitumen market.

The Bitumen Report is Segmented by Product Type (Penetration Grade, Oxidized Grade, Bitumen Emulsions, Polymer-Modified Bitumen, and Other Products), Application (Road Construction, Roofing, Adhesives and Sealants, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific led with 45.10% share in 2025 and is advancing at a 6.31% CAGR to 2031, anchored by synchronized infrastructure programs across China, India, and Southeast Asia. China's processing of 14.8 million barrels per day of crude in 2023 underpins both domestic asphalt supply and export capabilities.

North America balances robust rehabilitation budgets with evolving environmental mandates. The IIJA pipeline stabilizes demand, but Canada's impending PAH restrictions catalyze a shift to emulsions and cold processes. Europe confronts refinery rationalization; closures tighten regional supply yet open market space for bio-based alternatives. The bitumen market size in Europe could contract marginally in tonnage yet expand in value as specialty grades outpace generic ones.

The Middle East leverages abundant feedstock and strategic shipping lanes to supply Asia. Trade between Gulf producers and Asian buyers is forecast to touch USD 682 billion by 2030, with finished binders and modifiers joining crude flows.

Africa and South America remain emergent, characterized by episodic megaprojects that create demand surges. Suppliers attuned to flexible logistics and rapid deployment can gain traction as these regions scale connectivity investments.

- BMI Group Holdings UK Limited

- BP p.l.c.

- China Petroleum and Chemical Corporation (Sinopec)

- ENEOS Corporation

- Exxon Mobil Corporation

- Hindustan Petroleum Corporation Limited

- Indian Oil Corporation Ltd

- Kraton Corporation

- Mangalore Refinery and Petrochemicals Limited

- Marathon Petroleum Corporation

- Nynas AB

- Rosneft

- Shell plc

- Suncor Energy Inc.

- The Bouygues Group

- TotalEnergies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing road and highway rehabilitation spend

- 4.2.2 Large-scale airport runway expansion programs

- 4.2.3 Government infrastructure stimulus in emerging economies

- 4.2.4 Shift to polymer-modified bitumen for climate-resilient pavements

- 4.2.5 Circular-economy push for reclaimed asphalt pavement (RAP) adoption

- 4.3 Market Restraints

- 4.3.1 Stringent GHG and PAH emission regulations on paving operations

- 4.3.2 Crude-oil price volatility impacting feedstock economics

- 4.3.3 Rising share of concrete and composite pavements in urban projects

- 4.4 Value Chain Analysis

- 4.5 Feedstock Analysis

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Penetration Grade

- 5.1.2 Oxidized Grade

- 5.1.3 Bitumen Emulsions

- 5.1.4 Polymer-Modified Bitumen

- 5.1.5 Other Products (Viscosity Grade, Cutback, and Performance Grade)

- 5.2 By Application

- 5.2.1 Road Construction

- 5.2.2 Roofing

- 5.2.3 Adhesives and Sealants

- 5.2.4 Other Applications (Coatings in Sectors such as Oil and Gas, Canal Lining, Tank Foundation, Railway Ballast Treatment, and Others)

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Colombia

- 5.3.2.4 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 South Korea

- 5.3.4.5 ASEAN

- 5.3.4.6 Rest of Asia-Pacific

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (MandA/JV/Agreements)

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BMI Group Holdings UK Limited

- 6.4.2 BP p.l.c.

- 6.4.3 China Petroleum and Chemical Corporation (Sinopec)

- 6.4.4 ENEOS Corporation

- 6.4.5 Exxon Mobil Corporation

- 6.4.6 Hindustan Petroleum Corporation Limited

- 6.4.7 Indian Oil Corporation Ltd

- 6.4.8 Kraton Corporation

- 6.4.9 Mangalore Refinery and Petrochemicals Limited

- 6.4.10 Marathon Petroleum Corporation

- 6.4.11 Nynas AB

- 6.4.12 Rosneft

- 6.4.13 Shell plc

- 6.4.14 Suncor Energy Inc.

- 6.4.15 The Bouygues Group

- 6.4.16 TotalEnergies

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

瀝青市場:全球市場預測,2026-2032年

瀝青市場:全球市場預測,2026-2032年 環保瀝青市場報告:按原料、等級、應用和地區分類(2026-2034 年)

環保瀝青市場報告:按原料、等級、應用和地區分類(2026-2034 年) 瀝青市場:按產品類型、應用和地區分類

瀝青市場:按產品類型、應用和地區分類 全球瀝青市場規模、佔有率、趨勢和成長分析報告(2026-2034年)瀝青乳化劑市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年環保瀝青市場:按類型、技術和應用分類-2026-2032年全球市場預測

全球瀝青市場規模、佔有率、趨勢和成長分析報告(2026-2034年)瀝青乳化劑市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年環保瀝青市場:按類型、技術和應用分類-2026-2032年全球市場預測 瀝青乳化劑市場分析及預測(至2035年):類型、產品、應用、技術、組成成分、最終用戶、劑型、材料類型、製程、解決方案瀝青市場分析及預測(至2035年):依類型、產品類型、應用、技術、最終用戶、形態、材質、製程及功能分類環保瀝青生產市場分析及預測(至2035年):類型、產品、服務、技術、應用、形式、材料類型、製程、最終用戶、設備

瀝青乳化劑市場分析及預測(至2035年):類型、產品、應用、技術、組成成分、最終用戶、劑型、材料類型、製程、解決方案瀝青市場分析及預測(至2035年):依類型、產品類型、應用、技術、最終用戶、形態、材質、製程及功能分類環保瀝青生產市場分析及預測(至2035年):類型、產品、服務、技術、應用、形式、材料類型、製程、最終用戶、設備 2026年全球瀝青市場報告

2026年全球瀝青市場報告