|

市場調查報告書

商品編碼

1937423

ESG評估服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ESG Rating Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

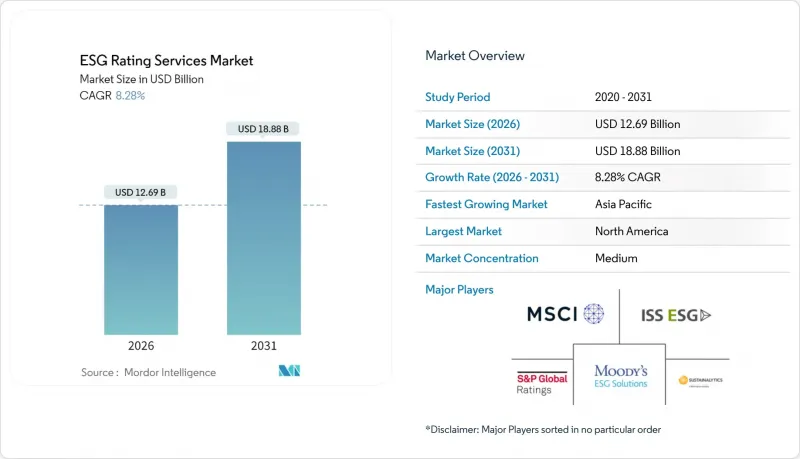

預計到 2026 年,ESG 評估服務市場規模將達到 126.9 億美元,高於 2025 年的 117.2 億美元。

預計到 2031 年將達到 188.8 億美元,2026 年至 2031 年的複合年成長率為 8.28%。

這項成長的驅動力來自強制性資訊揭露制度的普及,例如歐盟企業永續發展報告指令 (CSRD) 和美國證券交易委員會 (SEC) 的氣候變遷規則,以及機構投資者對標準化永續發展指標日益成長的需求。資產管理公司正在增加對詳細、機器可讀的 ESG 資料集的預算,企業也爭相獲取第三方評估,以支持與相關人員的溝通和監管申報。數據供應商之間的整合使得主要供應商能夠將評分和分析功能打包在一起,而諸如自然相關財務資訊揭露工作組 (TNFD) 等框架的擴展則推動了生物多樣性指標方面的產品創新。然而,美國一些州的政治反對以及供應商之間持續存在的低相關性,都為這一領域的強勁前景蒙上了一層陰影。

全球ESG評級服務市場趨勢與洞察

從2025年起,強制性資訊揭露制度的激增將重塑市場需求。

企業永續發展報告指令 (CSRD) 於 2025 年 1 月全面實施,要求約 5 萬家公司發布雙重重要性 ESG 報告,評級機構將這些報告轉化為可供投資者參考的評分。同時,國際標準理事會 (ISSB) 的 IFRS S1 和 S2 標準在 15 個司法管轄區獲得採納,建立了一項全球報告標準,提高了發行人的合規門檻。 [3] 能夠協調 CSRD、ISSB 和美國證券交易委員會 (SEC) 規則手冊中調查方法的機構將獲得競爭優勢,因為企業更傾向於獲得能夠滿足多個監管機構要求的單一評分。協調一致有助於揭露關於排放、員工多元化和管治結構的詳細、審核的指標,從而提升資料深度。因此,ESG評級服務市場對將原始數據、檢驗和分析整合到單一訂閱中的垂直整合解決方案的需求日益成長。韓國、巴西和加拿大持續的監管更新正在推動目標報告量的成長,確保資訊揭露主導的成長能夠從西方擴展到全球中端市場。

資產管理公司利用人工智慧增強的ESG分析尋求超額收益

機構投資者正計劃將2024年技術預算的15%至20%分配給ESG數據基礎設施,這標誌著投資結構正從回顧性的合規轉向追求超額收益的分析。貝萊德的Aladdin平台將ESG風險分析應用於其管理的21兆美元資產,而道富銀行則利用機器學習技術每天處理4萬個永續發展指標。評級機構目前正在發布基於API的“數據湖”,為即時攝取新聞、衛星數據和物聯網感測器數據的量化模型提供數據。 MSCI報告稱,在納入衡量氣候風險的另類資料集後,其ESG分析部門2024年的營收成長了40%。買方量化分析師越來越重視前瞻性指標,例如資本支出與淨零排放路徑的一致性,而這些領域需要強大且持續更新的資料流。因此,ESG評級服務市場正在獎勵那些能夠提供清晰、標準化、機器可讀且整合到投資組合管理系統中的資料來源的供應商。

歐盟ESG評級規定限制經營模式整合

歐盟ESG評級條例將於2025年生效,屆時將禁止向評級公司提供諮詢服務,並強制要求諮詢部門進行結構性分離。 ISS ESG和Sustainalytics等公司將被要求建立資訊隔離牆、審查管治並揭露利益衝突管理程序。據估計,主要供應商每年的合規成本將高達200萬至500萬歐元,這將擠壓其營運利潤空間並延緩產品推出。該條例還將限制對諮詢客戶所開發的內部研究成果的重複使用,迫使企業進行重複資料收集,從而減少交叉銷售收入,並引發人們對綜合解決方案有效性的質疑,進而推動了近期ESG評級服務市場的併購活動。

細分市場分析

到2025年,ESG評估將佔ESG評估服務市場38.10%的佔有率,在使資本配置與永續性目標保持一致方面發揮著至關重要的作用。隨著《企業永續發展報告指令》(CSRD)強制要求對永續發展報告進行第三方鑑證,以及國際永續發展標準理事會(ISSB)倡導審核層級的嚴謹性,檢驗和鑑證服務正以9.35%的複合年成長率快速成長。預計到2031年,檢驗ESG評估服務市場規模將達到48.1億美元,鞏固其作為企業進入受監管資訊揭露環境的最佳切入點的地位。四大審核事務所正在部署整合審核、氣候科學和精算技能的多學科團隊,加劇競爭並提高整體市場滲透率。對於尋求特定產業框架的發行人而言,諮詢和客製化服務仍然至關重要,但避免利益衝突的壓力正在限制歐洲的收入潛力。 ISSA 5000 將於 2025 年投入使用,屆時標準制定將減少調查方法的碎片化,並減少採購保證方面的摩擦。

ESG評級服務市場正日益採用自動化資料擷取、利用自然語言處理(NLP)進行說明檢驗以及整合衛星影像進行現場驗證等技術。即時保證縮短了報告週期,增強了投資人信心。全球企業正尋求將檢驗查核點嵌入其核心系統,以便將永續性績效指標(KPI)自動反映在季度報告中。競爭格局有利於提供模組化保證方案的供應商,這些方案可從單一主題檢驗擴展到企業級永續性審核。新興企業正在利用區塊鏈時間戳來增強資料完整性,迫使現有企業加快創新步伐。從基於計劃的合約模式轉向基於訂閱模式的轉變,正在使ESG評級服務市場服務領域的收入來源更加多元化。

區域分析

北美地區創造了最大的區域收入,預計到2025年將佔ESG評級服務市場規模的39.85%。這主要得益於該地區高達50兆美元的機構資產管理規模(AUM)以及美國證券交易委員會(SEC)氣候報告規則的實施,該規則影響了7,000家發行人。加州公共僱員退休系統(CalPERS)等退休基金要求對超過20億美元的股票持股進行ESG評級,大學捐贈基金也將ESG評分納入其策略性資產配置。然而,24個州通過的反ESG法案加劇了政策的不確定性,迫使服務提供者發布免責聲明,確保指數符合州法規,並應對政治爭議帶來的聲譽風險。

亞太地區以8.78%的複合年成長率呈現最快成長態勢,這主要得益於新加坡強制上市公司在2025年前提交氣候報告的藍圖,以及日本對佔該國市值70%的優質市場公司採用符合氣候相關財務資訊揭露框架(TCFD)的資訊揭露要求。印度的企業責任與永續性報告架構涵蓋了前1000家上市公司,其國內數據收集平台促進了與全球評級機構的合作。中國2060年淨零排放承諾將環境、社會和治理(ESG)的重要性擴展到國有企業,而東協正在製定強調統一評級資訊的永續金融分類體系。這些發展勢頭使亞太地區成為ESG評級服務市場成長的關鍵驅動力。

在歐洲,《企業永續性報告指令》(CSRD)、歐盟分類法和《永續金融揭露條例》(SFDR)透過對約5萬家公司施加ESG義務,支持了兩位數的收入成長。該地區的雙重重要性標準要求發行人同時報告財務重要性和影響重要性,提高了數據細分的標準,並塑造了全球最佳實踐。拉丁美洲和中東/非洲等小規模的地區正在謹慎地取得進展。巴西的B3交易所強制要求揭露永續發展訊息,而阿拉伯聯合大公國的綠色金融框架正在幫助石油出口經濟體調整發展方向。新興市場的數據匱乏、有限的鑑證能力以及信用風險問題仍然阻礙相關法規的採用。然而,隨著監管要求的日益嚴格,在這些地區率先部署相關法規的供應商將有望獲得先發優勢。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章:目錄 - ESG評估服務市場

第2章 引言

- 研究假設和市場定義

- 調查範圍

第3章調查方法

第4章執行摘要

第5章 市場情勢

- 市場概覽

- 市場促進因素

- 2025 年後強制資訊揭露制度的激增(歐盟企業永續發展報告指令、美國證券交易委員會氣候條例、國際永續發展準則理事會)

- 資產管理公司利用人工智慧驅動的、分解的ESG資料集尋求超額收益。

- 快速整合原始資料供應商可以實現捆綁式評級和資料產品。

- 擴展自然與生物多樣性相關指標(TNFD)

- 將ESG API整合到交易/風險管理系統中的金融科技

- 民營市場投資者對可比較ESG評分的需求日益成長

- 市場限制

- 對混合估值和諮詢模式的監管限制(歐盟ESG估值法規)

- 供應商之間持續的低相關性正在削弱投資者信心。

- 美國主要州的政治反彈和反ESG立法

- 新興市場中小企業缺乏檢驗的範圍3數據

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第6章 市場規模與成長預測

- 按服務類型

- ESG評估

- ESG 數據和評分

- ESG分析工具

- ESG保證與檢驗

- 諮詢/客製化

- 最終用戶

- 資產管理公司

- 資產所有者和退休基金

- 銀行和其他金融機構

- 非金融公司

- 保險公司

- 政府和公共機構

- 其他相關人員

- 資產類別覆蓋範圍

- 庫存產品

- 固定收益(公司債/公債)

- 私募市場和替代投資

- 實體資產(基礎設施/房地產)

- 多元資產組合

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 其他南美洲

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟

- 北歐國家

- 其他歐洲地區

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 北美洲

第7章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- MSCI

- Sustainalytics/Morningstar

- ISS ESG

- S&P Global ESG Scores

- Moody's ESG Solutions

- LSEG Refinitiv

- Bloomberg ESG

- Fitch(Sustainable Fitch)

- FTSE Russell

- EcoVadis

- CDP

- Arabesque S-Ray

- Clarity AI

- RepRisk

- FactSet Truvalue Labs

- Vigeo Eiris

- GRESB

- Standard Ethics

- Inrate

- CSRHub

第8章:市場機會與未來展望

- 閒置頻段與未滿足需求評估

ESG rating services market size in 2026 is estimated at USD 12.69 billion, growing from 2025 value of USD 11.72 billion with 2031 projections showing USD 18.88 billion, growing at 8.28% CAGR over 2026-2031.

Growth is propelled by the convergence of mandatory disclosure regimes such as the EU Corporate Sustainability Reporting Directive (CSRD) and the U.S. Securities and Exchange Commission (SEC) climate rule, coupled with rising institutional investor demand for standardized sustainability metrics. Asset managers are widening budgets for granular, machine-readable ESG datasets, while corporates rush to secure third-party ratings that validate stakeholder communications and regulatory filings. Consolidation among data vendors lets leading providers package scores with analytics, and the expansion of frameworks like the Task Force on Nature-related Financial Disclosures (TNFD) is catalyzing product innovation around biodiversity metrics. Political pushback in several U.S. states and persistent low correlation across providers temper the otherwise robust outlook.

Global ESG Rating Services Market Trends and Insights

Post-2025 Surge in Mandatory Disclosure Regimes Reshapes Market Demand

The CSRD took full effect in January 2025, obliging roughly 50,000 companies to publish double-materiality ESG reports that rating providers convert into investor-grade scores. Simultaneously, the ISSB's IFRS S1 and S2 standards have been adopted in 15 jurisdictions, establishing a global reporting baseline that raises the compliance bar for issuers[3]. Providers able to synchronize methodologies across CSRD, ISSB, and the SEC rulebook win a competitive advantage because corporates prefer a single score that satisfies multiple regulators. Harmonization fuels data depth as firms disclose granular, audit-ready metrics on emissions, workforce diversity, and governance structures. Consequently, the ESG rating services market experiences heavier demand for vertically integrated offerings that bundle raw data, verification, and analytics into one subscription. Persistent regulatory updates in South Korea, Brazil, and Canada expand addressable volumes, ensuring that disclosure-driven growth extends beyond Europe and the United States into global mid-cap universes.

Asset Managers Pursue Alpha Through AI-Enhanced ESG Analytics

Institutional investors allocated 15-20% of 2024 technology budgets to ESG data infrastructure, signaling a structural pivot from backward-looking compliance toward alpha-seeking analytics. BlackRock's Aladdin platform applied ESG risk analytics across USD 21 trillion in AUM, while State Street processed 40,000 sustainability metrics daily using machine learning. Rating providers now release API-based "data lakes" that feed quantitative models ingesting news, satellite feeds, and IoT sensors in real time. MSCI reported 40% revenue growth in ESG analytics during 2024 after embedding alternative data sets measuring physical climate risk. Buy-side quants increasingly weight forward-looking metrics such as capital expenditure alignment to net-zero pathways, and these fields require robust, continuously updated data streams. The ESG rating services market, therefore, rewards providers capable of delivering clean, normalized, machine-readable feeds integrated into portfolio-management systems.

EU ESG Ratings Regulation Constrains Business-Model Integration

Entering force in 2025, the EU ESG Ratings Regulation bans providers from offering advisory services to rated entities, compelling structural separation of consulting arms. Firms such as ISS ESG and Sustainalytics must erect Chinese walls, overhaul governance, and disclose conflict-management procedures. Estimated compliance costs range from EUR 2 million to EUR 5 million annually for large vendors, eroding operating margins and delaying product roll-outs. The rule also restricts the reuse of internal research produced for consulting clients, forcing duplicative data collection. These constraints reduce cross-selling revenues and challenge the integrated-solutions thesis, driving recent M&A in the ESG rating services market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Consolidation of Raw-Data Vendors Enables Comprehensive Offerings

- TNFD Framework Drives Nature-Related Financial Disclosure Adoption

- Correlation Challenges Undermine Rating Credibility and Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

ESG ratings captured 38.10% of the ESG rating services market in 2025, underscoring their foundational role in aligning capital allocation with sustainability objectives. Verification and assurance services rise at a 9.35% CAGR because CSRD mandates third-party assurance for sustainability statements while ISSB encourages audit-like rigor. The ESG rating services market size for verification is expected to reach USD 4.81 billion by 2031, cementing its position as the preferred gateway for corporates entering regulated disclosure landscapes. Big Four accounting firms deploy cross-disciplinary teams combining audit, climate science, and actuarial skill sets, which drives price competition but also increases overall market penetration. Advisory and customization maintain relevance among issuers seeking sector-specific frameworks, yet pressures to avoid conflicts of interest temper revenue potential in Europe. As ISSA 5000 becomes operative in 2025, standard-setting should reduce methodological fragmentation and lower assurance-procurement friction.

The ESG rating services market witnesses technology infusion as providers automate data ingestion, apply NLP for narrative verification, and integrate satellite imagery for onsite confirmation. Real-time attestations shorten reporting cycles and refine investor confidence. Global corporates aim to embed verification checkpoints inside enterprise resource-planning systems, ensuring that sustainability KPIs roll automatically into quarterly filings. Competitive dynamics favor vendors offering modular assurance packages that can range from single-topic verification to enterprise-wide sustainability audits. Emerging players leverage blockchain timestamps to enhance data integrity, challenging incumbents to accelerate innovation. Subscription-based models gradually replace project-based engagements, diversifying revenue streams within the ESG rating services market size for services.

The ESG Rating Services Market is Segmented by Service Type (ESG Ratings, ESG Data & Scores, and More), End-User (Asset Managers, Asset Owners & Pension Funds, and More), Asset-Class Coverage (Equity Instruments, Fixed-Income (Corporate & Sovereign), Private Markets & Alternatives, Real Assets (Infrastructure / Real Estate), and More), and Geography. The Market Forecasts are Provided in Value (USD).

Geography Analysis

North America generated the largest regional revenue in 2025 at 39.85% share of the ESG rating services market size, bolstered by institutional AUM of USD 50 trillion and imminent SEC climate reporting rules affecting 7,000 issuers [SEC]. Pension funds such as CalPERS mandate ESG ratings for equity holdings above USD 2 billion, while university endowments integrate scores into strategic asset allocations. Yet 24 state-level anti-ESG statutes inject policy uncertainty, compelling providers to issue disclaimers, maintain state-compliant indexes, and manage reputational exposure to political discourse.

Asia-Pacific exhibits the fastest expansion at 8.78% CAGR, driven by Singapore's roadmap requiring listed firms to publish climate reports by 2025 and Japan's adoption of TCFD-aligned disclosures for prime-market companies representing 70% of domestic capitalization. India's Business Responsibility and Sustainability Reporting framework covers the top 1,000 listed entities, prompting domestic data collection platforms to collaborate with global rating houses. China's 2060 net-zero pledge extends ESG relevance to state-owned enterprises, while ASEAN develops a sustainable finance taxonomy that favors harmonized rating inputs. The momentum positions Asia-Pacific as the focal engine for incremental growth within the ESG rating services market.

Europe sustains double-digit revenue streams anchored in the CSRD, EU Taxonomy, and SFDR, collectively imposing ESG obligations on roughly 50,000 companies. The bloc's double-materiality lens requires issuers to report on both financial and impact materiality, raising data granularity standards that shape global best practices. Smaller regions like Latin America and the Middle East & Africa proceed cautiously; Brazil's B3 exchange mandates sustainability disclosures, and the UAE's green-finance framework supports pathway alignment for oil-exporting economies. Data scarcity, limited assurance capacity, and emerging-market credit-risk concerns continue to slow penetration. Nonetheless, providers that pre-position in these regions stand to capture first-mover advantages once regulatory expectations tighten.

- MSCI

- Sustainalytics / Morningstar

- ISS ESG

- S&P Global ESG Scores

- Moody's ESG Solutions

- LSEG Refinitiv

- Bloomberg ESG

- Fitch (Sustainable Fitch)

- FTSE Russell

- EcoVadis

- CDP

- Arabesque S-Ray

- Clarity AI

- RepRisk

- FactSet Truvalue Labs

- Vigeo Eiris

- GRESB

- Standard Ethics

- Inrate

- CSRHub

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Table of Contents - ESG Rating Services Market

2 Introduction

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

3 Research Methodology

4 Executive Summary

5 Market Landscape

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Post-2025 surge in mandatory disclosure regimes (EU CSRD, SEC climate rule, ISSB)

- 5.2.2 Asset-manager hunt for alpha via AI-ready granular ESG datasets

- 5.2.3 Rapid consolidation of raw-data vendors enabling bundled rating/data offers

- 5.2.4 Expansion of nature- and biodiversity-linked metrics (TNFD)

- 5.2.5 Fintech integration of ESG APIs into trading?/?risk systems

- 5.2.6 Rising demand from private-market investors for comparable ESG scores

- 5.3 Market Restraints

- 5.3.1 Regulatory caps on mixed rating-consulting models (EU ESG Ratings Regulation)

- 5.3.2 Persistent low correlation among providers eroding investor confidence

- 5.3.3 Political backlash & anti-ESG legislation in key U.S. states

- 5.3.4 Scarcity of verifiable Scope-3 data for SMEs in emerging markets

- 5.4 Value / Supply-Chain Analysis

- 5.5 Regulatory Landscape

- 5.6 Technological Outlook

- 5.7 Porter's Five Forces

- 5.7.1 Threat of New Entrants

- 5.7.2 Bargaining Power of Suppliers

- 5.7.3 Bargaining Power of Buyers

- 5.7.4 Threat of Substitute Products

- 5.7.5 Competitive Rivalry

6 Market Size & Growth Forecasts

- 6.1 By Service Type (Value)

- 6.1.1 ESG Ratings

- 6.1.2 ESG Data & Scores

- 6.1.3 ESG Analytics & Tools

- 6.1.4 ESG Assurance & Verification

- 6.1.5 Advisory / Customization

- 6.2 By End-User (Value)

- 6.2.1 Asset Managers

- 6.2.2 Asset Owners & Pension Funds

- 6.2.3 Banks & Other FIs

- 6.2.4 Corporates (Non-Financial)

- 6.2.5 Insurance Companies

- 6.2.6 Governments & Public Institutions

- 6.2.7 Other Stakeholders

- 6.3 By Asset-Class Coverage

- 6.3.1 Equity Instruments

- 6.3.2 Fixed-Income (Corp & Sovereign)

- 6.3.3 Private Markets & Alternatives

- 6.3.4 Real Assets (Infra / RE)

- 6.3.5 Multi-Asset Portfolios

- 6.4 By Geography (Value)

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.1.3 Mexico

- 6.4.2 South America

- 6.4.2.1 Brazil

- 6.4.2.2 Peru

- 6.4.2.3 Chile

- 6.4.2.4 Argentina

- 6.4.2.5 Rest of South America

- 6.4.3 Europe

- 6.4.3.1 United Kingdom

- 6.4.3.2 Germany

- 6.4.3.3 France

- 6.4.3.4 Spain

- 6.4.3.5 Italy

- 6.4.3.6 BENELUX

- 6.4.3.7 NORDICS

- 6.4.3.8 Rest of Europe

- 6.4.4 Asia-Pacific

- 6.4.4.1 India

- 6.4.4.2 China

- 6.4.4.3 Japan

- 6.4.4.4 Australia

- 6.4.4.5 South Korea

- 6.4.4.6 South-East Asia

- 6.4.4.7 Rest of Asia-Pacific

- 6.4.5 Middle East & Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.5.4 Nigeria

- 6.4.5.5 Rest of Middle East & Africa

- 6.4.1 North America

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 7.4.1 MSCI

- 7.4.2 Sustainalytics / Morningstar

- 7.4.3 ISS ESG

- 7.4.4 S&P Global ESG Scores

- 7.4.5 Moody's ESG Solutions

- 7.4.6 LSEG Refinitiv

- 7.4.7 Bloomberg ESG

- 7.4.8 Fitch (Sustainable Fitch)

- 7.4.9 FTSE Russell

- 7.4.10 EcoVadis

- 7.4.11 CDP

- 7.4.12 Arabesque S-Ray

- 7.4.13 Clarity AI

- 7.4.14 RepRisk

- 7.4.15 FactSet Truvalue Labs

- 7.4.16 Vigeo Eiris

- 7.4.17 GRESB

- 7.4.18 Standard Ethics

- 7.4.19 Inrate

- 7.4.20 CSRHub

8 Market Opportunities & Future Outlook

- 8.1 White-space & Unmet-Need Assessment

綠色金融和ESG投資金融科技平台市場預測至2034年-全球分析(按組成部分、技術、產品類型、交易類型、應用、最終用戶和地區分類)

綠色金融和ESG投資金融科技平台市場預測至2034年-全球分析(按組成部分、技術、產品類型、交易類型、應用、最終用戶和地區分類) ESG評級服務市場-全球產業規模、佔有率、趨勢、機會與預測:按服務類型、應用、地區和競爭格局分類,2021-2031年綠色金融科技和ESG金融平台市場預測至2034年-全球分析(按組件、部署模式、技術、產品類型、應用、最終用戶和地區分類)

ESG評級服務市場-全球產業規模、佔有率、趨勢、機會與預測:按服務類型、應用、地區和競爭格局分類,2021-2031年綠色金融科技和ESG金融平台市場預測至2034年-全球分析(按組件、部署模式、技術、產品類型、應用、最終用戶和地區分類) 2026年全球環境、社會與管治(ESG)關聯保險市場報告2026年全球太空法與管治市場報告

2026年全球環境、社會與管治(ESG)關聯保險市場報告2026年全球太空法與管治市場報告 ESG風險管理市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶及解決方案分類

ESG風險管理市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶及解決方案分類 ESG投資市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年

ESG投資市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年 ESG軟體市場規模、佔有率和趨勢分析報告:按部署模式、類型、組織規模、最終用途、地區和細分市場預測,2026-2033年

ESG軟體市場規模、佔有率和趨勢分析報告:按部署模式、類型、組織規模、最終用途、地區和細分市場預測,2026-2033年 ESG軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

ESG軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) ESG認證市場規模、佔有率和成長分析(按認證類型、產業垂直領域、最終用戶、服務類型、環境影響和地區分類)-2026-2033年產業預測

ESG認證市場規模、佔有率和成長分析(按認證類型、產業垂直領域、最終用戶、服務類型、環境影響和地區分類)-2026-2033年產業預測