|

市場調查報告書

商品編碼

1937396

非洲網路安全:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Africa Cybersecurity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

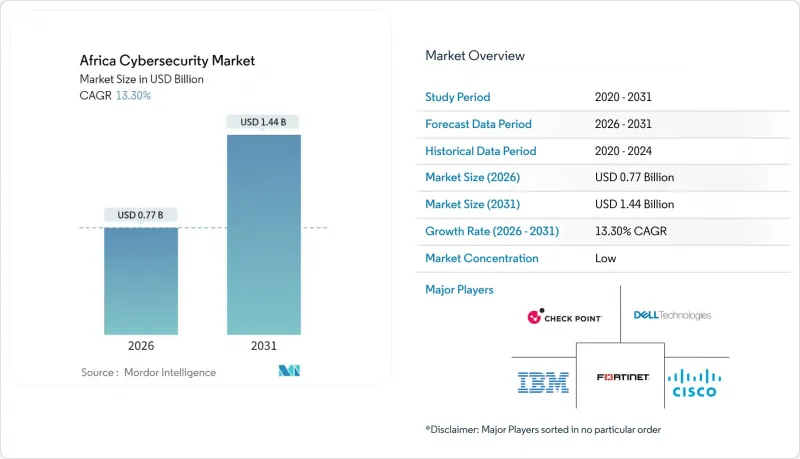

預計非洲網路安全市場將從 2025 年的 6.8 億美元成長到 2026 年的 7.7 億美元,到 2031 年達到 14.4 億美元,2026 年至 2031 年的複合年成長率為 13.3%。

這種快速成長與非洲大陸海底電纜部署的擴張、雲端資料中心規模的擴大以及區域資料保護法律的加強直接相關。微軟和G42在肯亞投資10億美元的數位生態系統計畫等超大規模資料中心業者資料中心的投資,正在將採購標準從單一解決方案轉向多層雲端原生安全平台(microsoft.com)。企業也面臨認證專業人員長期短缺的問題——每10萬人中不足2人——迫使許多企業依賴資安管理服務管治。奈及利亞的《國家資料保護法》(NDPA)和南非的《個人資訊保護法》(POPIA)等法律法規的協調統一,正迫使跨國公司將資料處理在地化,並協調跨境治理控制。同時,行動支付的普及加劇了詐騙風險,使得人工智慧驅動的生物識別和反洗錢分析在金融服務領域變得至關重要。

非洲網路安全市場趨勢與洞察

撒哈拉以南非洲地區行動支付平台的快速普及

到2024年,詐欺偵測引擎發現生物識別詐騙率高達16%,是用戶註冊時詐欺率的四倍。這凸顯了身分竊賊透過SIM卡交換和多層洗錢鏈竊取憑證的程度。在東非,由於身分證明文件不合格和檢驗系統薄弱,拒付率高達27%。僅在烏干達,預計到2024年行動支付詐騙造成的損失將達到320萬美元,這將推動人工智慧驅動的異常檢測工具和動態生物識別檢查的廣泛應用。這使得網路安全不再只是被視為合規成本,而是成為推動普惠金融成長的平台。

擴大國家資料保護條例

奈及利亞2023年《資料保護法》促使92%的受訪機構在12個月內加強了安全控制,而對Meta公司處以的2.2億美元罰款則表明監管機構願意對違規行為處以巨額罰款。肯亞在全球網路安全指數中名列前茅,並在2025年第一季偵測到25億次威脅,凸顯了早期立法如何增強一個國家的風險應對能力(technext24.com)。這正推動跨國公司朝著統一的洲際管治框架和區域資料處理中心的方向發展。

網路安全認證人才嚴重短缺(每10萬人不足2人)

光是奈及利亞一國到2030年就需要新增3萬名專業人員,而南非高薪的中級雲端安全職位年薪已超過786,648蘭特(約41,400美元),推高了當地企業的成本。為了解決人員短缺問題,企業正在採用安全營運中心即服務(SOCaaS)模式和自動化技術。雖然聯合國開發計畫署(UNDP)和卡內基美隆大學的競賽項目正在培養新人才,但它們每年的培訓能力加起來不足2,000人,結構性的人才短缺正在減緩解決方案的推廣應用。

細分市場分析

到2025年,非洲網路安全市場解決方案收入將佔總收入的67.60%,而資安管理服務正以18.2%的複合年成長率快速成長,這反映出企業正顯著轉向外包營運。由於面臨人才短缺,企業更傾向於選擇綜合性的SOC即服務(SOCaaS)方案,將威脅搜尋、合規性監控和事件回應整合到單一合約中。這種外包趨勢有助於提升Liquid C2等區域供應商的利潤率,這些供應商與超大規模資料中心業者合作,充分利用其人工智慧驅動的檢測技術。同時,解決方案細分市場面臨來自開放原始碼替代方案的價格壓力,促使供應商整合增值分析和監管工具包。

在企業應對多司法管轄區隱私法律挑戰的過程中,專業服務收入在整體服務組合中成長最快。顧問公司現在將「實施+培訓」模組打包,幫助客戶在數月而非數年內完成從基線差距評估到審核規的轉變。因此,非洲網路安全市場的支出結構正趨於整合。雖然硬體和軟體授權仍然是基礎要素,但基於合約的託管服務正在主導增量成長,提高了買賣雙方的可預測性。

到2025年,本地部署架構將佔總支出的55.10%,這反映了傳統資料中心基礎設施的現狀;而雲端採用率預計到2031年將以14.0%的複合年成長率成長。隨著工作負載遷移到區域超大規模資料中心業者資料中心,新的邊界定義不斷湧現,使得傳統防火牆難以滿足需求。 TymeBank等金融服務先驅正在展示,完全雲端部署的數位銀行如何在滿足支付卡產業資料安全標準 (PCI-DSS) 要求的同時,加快功能發布週期。因此,隨著安全存取服務邊際(SASE) 框架取代零散的VPN堆疊,預計到2031年,非洲雲端交付控制的網路安全市場規模將超過6.5億美元。

公共部門的工作負載仍然保持混合模式,因為資料主權條款通常要求將公民記錄儲存在本地。奈及利亞和埃及的本地雲端營運商利用匯率波動優勢,以該地貨幣計費,吸引那些需要可預測成本結構的政府和通訊業者租戶,優於外國供應商。他們提供的捆綁式安全控制措施有效地為國內網路安全供應商帶來了雲端託管通路的增量收入,從而增強了本地生態系統。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 撒哈拉以南非洲地區行動支付平台的快速普及

- 擴大國家資料保護條例(NDPR、DPA-Kenya、POPIA)

- 世界銀行 DE4A 數位公共基礎設施資金籌措

- 2Africa 和 Equiano 海底光纜登陸點增加頻寬並擴大攻擊面

- 沿岸地區油氣產業的OT網路安全需求

- 超大規模資料中心業者資料中心部署推動雲端原生安全

- 市場限制

- 網路安全認證人才嚴重短缺(每10萬人不足2人)

- 傳統基於SS7的通訊基礎設施

- 政府採購分散且銷售週期長

- 中小企業網路保險普及率低

- 關鍵法規結構評估

- 價值鏈分析

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 主要用例和案例研究

- 宏觀經濟因素對市場的影響

- 投資分析

第5章 市場規模與成長預測

- 報價

- 解決方案

- 應用程式安全

- 雲端安全

- 資料安全

- 身分和存取管理

- 基礎設施保護

- 綜合風險管理

- 網路安全設備

- 端點安全

- 其他服務

- 服務

- 專業服務

- 託管服務

- 解決方案

- 透過部署模式

- 本地部署

- 雲

- 按最終用戶行業分類

- BFSI

- 衛生保健

- 資訊科技和電信

- 工業與國防

- 製造業

- 零售與電子商務

- 能源與公共產業

- 其他

- 按最終用戶公司規模分類

- 中小企業

- 主要企業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Cisco Systems Inc.

- Check Point Software Technologies Ltd.

- Fortinet Inc.

- Palo Alto Networks Inc.

- IBM Corporation

- Dell Technologies(SecureWorks)

- Broadcom Inc.(Symantec)

- Trend Micro Inc.

- Sophos Group plc

- Kaspersky Lab

- Darktrace plc

- CyberArk Software Ltd.

- Dimension Data(NTT Ltd.)

- Liquid Intelligent Technologies(Liquid C2)

- BCX

- Silensec

- ESET

- Palo Alto Networks(Prisma)

- Huawei Technologies Co. Ltd.

- Oracle Corporation

第7章 市場機會與未來展望

The Africa cybersecurity market is expected to grow from USD 0.68 billion in 2025 to USD 0.77 billion in 2026 and is forecast to reach USD 1.44 billion by 2031 at 13.3% CAGR over 2026-2031.

This rapid momentum links directly to the continent's submarine-cable build-out, expanding cloud data-center footprints, and tighter regional data-protection laws. Hyperscaler investments, such as the USD 1 billion Microsoft-G42 digital-ecosystem program in Kenya, move the procurement baseline from point-solutions toward layered, cloud-native security platforms microsoft.com. Enterprises also confront a chronic shortage of certified professionals less than two experts per 100,000 population prompting many to rely on managed security service providers. Regulatory harmonization under acts such as Nigeria's NDPA and South Africa's POPIA is compelling multinational firms to localize data processing and unify governance controls across borders. Meanwhile, mobile-money adoption has heightened fraud exposure, making AI-driven biometric verification and anti-money-laundering analytics indispensable across financial services.

Africa Cybersecurity Market Trends and Insights

Rapid adoption of mobile-money platforms across SSA

Fraud-detection engines uncovered 16% biometric-fraud rates in 2024, quadruple the level at user registration, underscoring how identity-farming rings compromise credentials across SIM swaps and layered laundering chains . East Africa registers rejection rates as high as 27% due to sub-standard ID documentation and weak verification systems. Uganda alone lost USD 3.2 million to mobile-money fraud in 2024, catalyzing a surge in AI-driven anomaly-detection tools and dynamic liveness checks that reposition cybersecurity as a growth enabler for financial inclusion rather than a cost of compliance.

Expansion of national data-protection regulations

Nigeria's 2023 Data Protection Act spurred 92% of surveyed organizations to strengthen security controls within 12 months, while Meta's USD 220 million fine illustrated regulators' willingness to impose material penalties for non-compliance . Kenya's Tier 1 ranking in the Global Cybersecurity Index and the detection of 2.5 billion threats during Q1 2025 reaffirm how early statutory adoption improves national risk posture technext24.com. Multinationals are therefore pivoting to unified, continent-wide governance frameworks and localized data-processing hubs.

Severe shortage of certified cyber-security talent (< 2 pros/100 k pop.)

Nigeria alone needs 30,000 additional experts by 2030, yet premium cloud-security salaries in South Africa already exceed ZAR 786,648 (USD 41,400) for mid-level roles, inflating costs for local firms . Enterprises consequently embrace Security-Operations-Center-as-a-Service models and automation to offset human bottlenecks. Although UNDP and Carnegie Mellon competitions train new cohorts, their combined reach remains below 2,000 professionals annually, leaving a structural deficit that slows solution uptake .

Other drivers and restraints analyzed in the detailed report include:

- World Bank DE4A digital public-infrastructure funding

- Hyperscaler data-center roll-outs driving cloud-native security

- Legacy SS7-based telco infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Africa cybersecurity market recorded solutions revenue of 67.60% in 2025, yet managed-security offerings are expanding at an 18.2% CAGR, reflecting a decisive shift toward outsourced operations. Enterprises grappling with talent scarcity prefer comprehensive Security-Operations-Center-as-a-Service bundles that combine threat hunting, compliance monitoring, and incident response under single contracts. This outsourcing trend widens margins for regional providers such as Liquid C2, whose AI-infused detection stack benefits from partnerships with hyperscalers. At the same time, the solutions sub-segment faces price pressure from open-source alternatives, prompting vendors to embed value-added analytics and regulatory toolkits.

Professional-services revenue is rising fastest within the broader services mix, as firms navigate multi-jurisdictional privacy laws. Consultants now package "implementation-plus-training" modules, helping clients move from baseline gap assessments to auditable compliance in months rather than years. The Africa cybersecurity market therefore demonstrates a converging spend profile: hardware and software licenses remain foundational, but contractual managed services dominate incremental growth, improving predictability for both buyers and vendors.

On-premise architectures still captured 55.10% of 2025 spend, mirroring legacy data-center footprints, yet cloud adoption is tracking an 14.0% CAGR through 2031. Workload migration toward regional hyperscaler zones creates new perimeter definitions, rendering traditional firewalls insufficient. Financial-services pioneers such as TymeBank showcase how fully cloud-deployed digital banks can satisfy Payment Card Industry Data Security Standard (PCI-DSS) requirements while accelerating feature release cycles. Accordingly, the Africa cybersecurity market size for cloud-delivered controls is forecast to exceed USD 650 million by 2031, as secure access service edge (SASE) frameworks replace patchwork VPN stacks.

Public-sector workloads remain hybrid because data-sovereignty clauses often mandate local storage for citizen records. Local cloud operators in Nigeria and Egypt exploit currency volatility advantages over foreign providers by billing in local denominations, attracting government and telco tenants that require predictable cost structures. Their bundled security controls effectively an extension of cloud hosting channel incremental revenue toward domestic cybersecurity vendors, reinforcing regional ecosystems.

The Africa Cybersecurity Market Report Segments the Industry Into Offering (Solutions and Services), Deployment Mode (On-Premise, and Cloud), End-User Vertical (BFSI, Healthcare, IT and Telecom, Industrial and Defense, Manufacturing, Retail and E-Commerce, Energy and Utilities, and Others), and End-User Enterprise Size (SMEs, and Large Enterprises). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Cisco Systems Inc.

- Check Point Software Technologies Ltd.

- Fortinet Inc.

- Palo Alto Networks Inc.

- IBM Corporation

- Dell Technologies (SecureWorks)

- Broadcom Inc. (Symantec)

- Trend Micro Inc.

- Sophos Group plc

- Kaspersky Lab

- Darktrace plc

- CyberArk Software Ltd.

- Dimension Data (NTT Ltd.)

- Liquid Intelligent Technologies (Liquid C2)

- BCX

- Silensec

- ESET

- Palo Alto Networks (Prisma)

- Huawei Technologies Co. Ltd.

- Oracle Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Mobile-Money Platforms Across SSA

- 4.2.2 Expansion of National Data-Protection Regulations (NDPR, DPA-Kenya, POPIA)

- 4.2.3 World-Bank DE4A Digital Public-Infrastructure Funding

- 4.2.4 2Africa and Equiano Cable Landings Expanding Bandwidth Attack Surface

- 4.2.5 OT Cybersecurity Demand in Gulf-of-Guinea Oil and Gas

- 4.2.6 Hyperscaler Data-Center Roll-outs Driving Cloud-Native Security

- 4.3 Market Restraints

- 4.3.1 Severe Shortage of Certified Cyber-Security Talent ( <2 Pros/100k pop.)

- 4.3.2 Legacy SS7-Based Telco Infrastructure

- 4.3.3 Fragmented Government Procurement and Long Sales Cycles

- 4.3.4 Low Cyber-Insurance Penetration Among SMEs

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Key Use Cases and Case Studies

- 4.9 Impact on Macroeconomic Factors of the Market

- 4.10 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.1.1 Application Security

- 5.1.1.2 Cloud Security

- 5.1.1.3 Data Security

- 5.1.1.4 Identity and Access Management

- 5.1.1.5 Infrastructure Protection

- 5.1.1.6 Integrated Risk Management

- 5.1.1.7 Network Security Equipment

- 5.1.1.8 Endpoint Security

- 5.1.1.9 Other Services

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By End-User Vertical

- 5.3.1 BFSI

- 5.3.2 Healthcare

- 5.3.3 IT and Telecom

- 5.3.4 Industrial and Defense

- 5.3.5 Manufacturing

- 5.3.6 Retail and E-commerce

- 5.3.7 Energy and Utilities

- 5.3.8 Others

- 5.4 By End-User Enterprise Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Cisco Systems Inc.

- 6.4.2 Check Point Software Technologies Ltd.

- 6.4.3 Fortinet Inc.

- 6.4.4 Palo Alto Networks Inc.

- 6.4.5 IBM Corporation

- 6.4.6 Dell Technologies (SecureWorks)

- 6.4.7 Broadcom Inc. (Symantec)

- 6.4.8 Trend Micro Inc.

- 6.4.9 Sophos Group plc

- 6.4.10 Kaspersky Lab

- 6.4.11 Darktrace plc

- 6.4.12 CyberArk Software Ltd.

- 6.4.13 Dimension Data (NTT Ltd.)

- 6.4.14 Liquid Intelligent Technologies (Liquid C2)

- 6.4.15 BCX

- 6.4.16 Silensec

- 6.4.17 ESET

- 6.4.18 Palo Alto Networks (Prisma)

- 6.4.19 Huawei Technologies Co. Ltd.

- 6.4.20 Oracle Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

網路安全市場:按組件、安全類型、組織規模、部署模式和產業分類-2026-2032年全球市場預測

網路安全市場:按組件、安全類型、組織規模、部署模式和產業分類-2026-2032年全球市場預測 人工智慧網路安全市場預測至2034年—按交付方式、安全類型、部署方式、技術、應用、最終用戶和地區分類的全球分析金融科技網路安全解決方案市場預測至2034年-按組件、安全類型、部署模式、組織規模、應用、最終用戶和地區分類的全球分析

人工智慧網路安全市場預測至2034年—按交付方式、安全類型、部署方式、技術、應用、最終用戶和地區分類的全球分析金融科技網路安全解決方案市場預測至2034年-按組件、安全類型、部署模式、組織規模、應用、最終用戶和地區分類的全球分析 2026-2030年全球智慧體與自主人工智慧系統網路安全解決方案市場

2026-2030年全球智慧體與自主人工智慧系統網路安全解決方案市場 2026年全球建築網路安全市場報告2026年全球電網網路安全市場報告2026年全球旅遊安全市場報告

2026年全球建築網路安全市場報告2026年全球電網網路安全市場報告2026年全球旅遊安全市場報告 全球數位攻防靶場市場報告:實際結果與預測(2021-2032)2026年全球Web3安全市場報告2026年全球電信網路安全解決方案市場報告

全球數位攻防靶場市場報告:實際結果與預測(2021-2032)2026年全球Web3安全市場報告2026年全球電信網路安全解決方案市場報告