|

市場調查報告書

商品編碼

1937368

Wi-Fi:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Wi-Fi - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

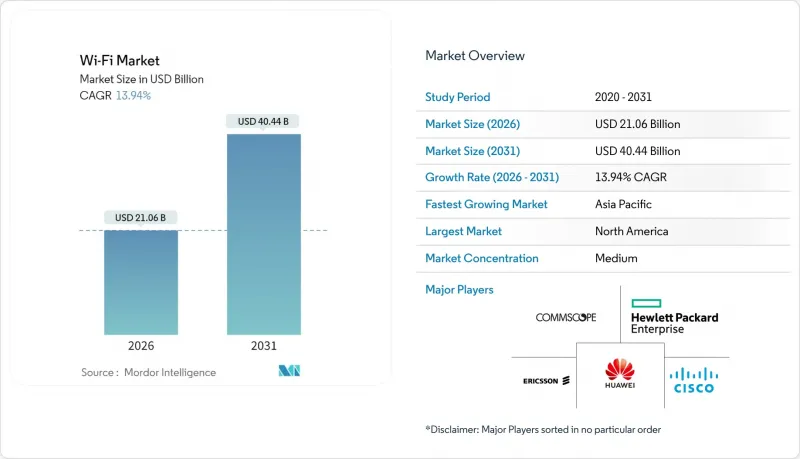

預計到 2025 年,Wi-Fi 市場價值將達到 184.8 億美元,從 2026 年的 210.6 億美元成長到 2031 年的 404.4 億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 13.94%。

推動這項加速發展的關鍵因素包括企業對無線優先架構日益成長的偏好、Wi-Fi 7 的商業化以及 OpenRoaming 標準的採用。企業意識到高容量 WLAN 對於實現混合辦公、邊緣人工智慧和即時工業自動化至關重要,從而將更新周期從八年縮短至五年。網狀網路在住宅和小規模辦公環境中的快速普及進一步擴大了潛在市場。同時,北美聯邦寬頻計畫正在為公共部門創造商機。雖然 6 GHz 頻譜分配可以暫時緩解網路堵塞,但也推動了對具有確定性延遲的三頻網路基地台可用於機器人、遠端醫療和身臨其境型現實服務。由於互通性要求避免了供應商鎖定,並使以服務為中心的新進業者能夠挑戰現有硬體供應商,因此競爭格局依然開放。

全球Wi-Fi市場趨勢與洞察

物聯網和智慧設備的興起

企業正在部署高密度感測器網路,每個網路基地台連接超過 100 個終端已成為常態。只有 Wi-Fi 6E 的 OFDMA 調度和多用戶 MIMO 功能才能經濟高效地滿足這種需求。智慧建築營運商正在透過 Wi-Fi 網狀網路整合暖通空調、照明和監控系統,從而降低 40% 的結構化佈線成本,並實現預測性維護分析。邊緣推理工作流程對 10 毫秒以下回應時間的需求,使得 Wi-Fi 7 的多連結運作極具吸引力,即使在高負載下也能保持無抖動流量。一項工業自動化試點計畫表明,專用 6 GHz 頻道的運轉率高達 99.9%,而擁塞的 5 GHz 連結的正常運作時間僅為 97.8%,這驗證了新頻譜轉換在關鍵任務機器人應用中的有效性。這些成果鼓勵企業承擔更高的初始投資,以換取長期的生產力提升。

智慧城市計畫與公共Wi-Fi部署

由於Wi-Fi部署速度更快,且在廣大的農村地區比光纖建設成本更低,地方政府的寬頻計畫越來越重視將其作為實現數位包容的主要媒介。菲律賓正投資12億美元,計畫到2028年在17,000個描籠涯(政府轄區)部署超過10萬個公共熱點,此模式已被多個新興經濟體採用。歐洲的「數位十年」計畫在2030年實現Gigabit部署,並將Wi-Fi 7網狀網路定位為山區和島嶼地區低成本的「最後一公里」替代方案。都市區正透過疊加感測器回程傳輸來為交通、空氣品質和緊急應變系統提供資金,並透過效率提升實現基礎設施的資金籌措。中立主機部署,即在開放漫遊協議下結合Wi-Fi和5G無線網路,既能實現市民無縫連接,又能透過漫遊費創造新的收入來源。

免執照頻段的頻譜擁塞和干擾

在曼哈頓等人口密集的都市區,即使部署了支援 Wi-Fi 6E 的設備,尖峰時段的吞吐量也會下降近 60%。這是因為老舊設備佔據了 2.4 GHz頻寬。微波爐、藍牙設備和老舊路由器產生的重疊噪聲,即使是自適應演算法也無法完全避免。企業擴大在其龐大的園區內聘請頻譜顧問,費用在 5 萬至 20 萬美元之間,以設計滿足服務等級目標的頻道規劃。監管機構正在考慮採用類似 CBRS 的半授權系統,以允許關鍵的物聯網流量在不受消費者干擾的情況下運作。雖然 6 GHz 頻譜的分配暫時緩解了壓力,但預計由於物聯網終端數量的指數級成長,頻譜將在五年內飽和。

細分市場分析

截至2025年,網路基地台將佔Wi-Fi市場佔有率的35.92%,顯示在收入結構轉變的背景下,硬體的重要性依然不減。同時,預計到2031年,服務領域將以15.98%的複合年成長率成長,反映出市場正向「網路即服務」(Network-as-a-Service)模式轉變,將初始投資轉化為持續的營運成本。成本壓力正推動獨立路由器和增程器走向商品化,而雲端原生編排平台則接管了傳統上由本地控制器執行的策略配置和編配功能。託管服務供應商正在利用人工智慧技術實現通道分配、負載平衡和異常檢測的自動化,與客戶自建網路相比,可將計劃外停機時間減少75%。到2031年,在成熟經濟體中,軟體和服務所佔的Wi-Fi市場規模預計將超過硬體,因為企業將生命週期柔軟性置於資產所有權之上。

這種轉變反映了更廣泛的IT採購趨勢,即優先考慮結果而非所有權。付費使用制將WLAN成本與運轉率掛鉤,既減少了預算波動,也提高了財務長的透明度。供應商不再僅僅依靠硬體,而是透過提供預防性保養、安全合規性和即時體驗評估等服務來實現差異化。邊緣閘道器和加固型物聯網橋接器雖然市場規模小規模,但成長迅速,它們能夠在惡劣的工業環境中提供可靠的連接,而這些環境的振動、灰塵和極端溫度都可能導致消費性設備損壞。嵌入網路基地台的AI晶片為通用硬體增添了價值,這些硬體以託管服務的形式交付,能夠簡化複雜性並加快生產力提升速度。

區域分析

到2025年,北美將佔據全球Wi-Fi市場40.55%的佔有率,這主要得益於650億美元的寬頻獎勵計畫和企業快速的網路更新週期。北美地區率先獲得頻寬的使用權,使其成為三頻部署的先驅,這使其在性能上領先於其他仍在等待監管部門等待核可的地區。財富500強企業平均每五年更新一次其無線區域網路(WLAN),以建構支援混合辦公的智慧辦公環境,速度比全球平均快兩年。醫療保健和教育是強勁的成長領域,需要企業級可靠性的網路來支援遠端醫療和遠端教育。

亞太地區預計將成為成長最快的地區,到2031年複合年成長率將達到15.12%,這主要得益於各國將無線網路定位為關鍵基礎設施而非補充手段的數位化策略。中國工廠自動化蓬勃發展,這得益於旨在提升國內晶片組能力的政策,也帶動了工業級Wi-Fi 6E設備的大量訂單。印度的「數位印度」計畫旨在透過Wi-Fi Mesh網路連接60萬個村莊,將無線技術定位為促進農村地區發展的關鍵推動因素。東南亞各國正在將WLAN整合到旅遊中心和出口導向產業園區,政府補貼透過縮短投資回收期加速了無線技術的普及。雅加達、曼谷和胡志明市的智慧城市資金籌措計畫進一步刺激了區域需求。

歐洲的成長穩步推進,工業4.0的實施以及《數位十年指令》強制要求在2030年實現Gigabit家庭網路連接。在阿爾卑斯山和希臘島嶼等地形崎嶇的地區,Wi-Fi提供了一種經濟高效的最後一公里解決方案。歐盟數位單一市場主導的開放漫遊協議實現了跨境無縫連接,促進了偏遠地區的旅遊業和商務旅行。德國在工業領域主導Wi-Fi應用,而北歐國家則專注於智慧電網和永續性應用,這些應用依賴節能型行波管(TWT)調度。中東和非洲地區正在投資Wi-Fi,以實現經濟多元化,擺脫對油氣資源的依賴,並彌合沙漠和山區農村地區的數位落差。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 物聯網和智慧設備的興起

- 智慧城市計畫與公共Wi-Fi部署

- WiFi 6/6E 的快速普及以及 WiFi 7 的即將推出

- 由於混合/遠端辦公模式的興起,對高容量無線區域網路 (WLAN) 的需求不斷成長。

- WiFi 和 5G 與 OpenRoaming/Passpoint 的融合

- 適用於電池供電物聯網節點的節能型TWT功能

- 市場限制

- 免執照頻段的頻譜擁塞和干擾

- 資料隱私和安全合規成本不斷增加

- 在60 GHz頻段,Li-Fi和替代技術將取代高密度WiFi應用場景。

- 晶片組供應限制導致 WiFi 7 設備發布延遲

- 價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按組件

- 硬體

- 網路基地台

- 路由器和擴展器

- 無線控制器

- 其他設備類型

- 解決方案

- 服務

- 硬體

- 終端用戶產業

- 消費者

- 企業/企業園區

- 教育

- 衛生保健

- 飯店和零售業

- 工業與物流

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲和紐西蘭

- 亞太其他地區

- 中東

- GCC

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Cisco Systems, Inc.

- Hewlett Packard Enterprise(Aruba)

- Huawei Technologies Co., Ltd.

- CommScope Holding Company Inc.(Ruckus Networks)

- Juniper Networks Inc.

- Telefonaktiebolaget LM Ericsson

- Extreme Networks, Inc.

- Ubiquiti Inc.

- Fortinet Inc.

- TP-Link Technologies Co., Ltd.

- Netgear Inc.

- D-Link Corporation

- Zyxel Communications Corp.

- Qualcomm Technologies, Inc.

- Broadcom Inc.

- Intel Corporation

- MediaTek Inc.

- Cambium Networks Ltd.

- EnGenius Networks, Inc.(Elitegroup)

- Purple WiFi Ltd.

- Cloud4Wi Inc.

- MetTel Inc.

- Singtel Group

第7章 市場機會與未來展望

The Wi-Fi Market was valued at USD 18.48 billion in 2025 and estimated to grow from USD 21.06 billion in 2026 to reach USD 40.44 billion by 2031, at a CAGR of 13.94% during the forecast period (2026-2031).

Growing enterprise preference for wireless-first architecture, the commercial debut of Wi-Fi 7, and the adoption of OpenRoaming standards are the primary forces propelling this acceleration . Enterprises view high-capacity WLAN as pivotal for hybrid work enablement, edge-hosted artificial intelligence, and real-time industrial automation, prompting refresh cycles that shorten from eight years to five. Rapid mesh penetration in residential and small-office environments further broadens the addressable base, while federal broadband programs in North America stimulate public-sector opportunities. Spectrum allocations in the 6 GHz band supply temporary congestion relief, yet also spark demand for tri-band access points that can assure deterministic latency for robotics, telemedicine, and immersive reality services. The competitive landscape remains open because interoperability requirements prevent lock-in, allowing new service-centric entrants to challenge incumbent hardware vendors.

Global Wi-Fi Market Trends and Insights

Proliferation of IoT and smart devices

Enterprises deploy dense sensor networks that often exceed 100 connected endpoints per access point, a profile economically serviced only by Wi-Fi 6E's OFDMA scheduling and multi-user MIMO capabilities. Smart-building operators integrate HVAC, lighting, and surveillance over Wi-Fi mesh to cut structured-cabling costs by 40% and enable predictive maintenance analytics. Demand for sub-10 ms response in edge inference workflows makes Wi-Fi 7's multi-link operation attractive because it sustains jitter-free traffic under load. Industrial automation pilots report 99.9% uptime on dedicated 6 GHz channels versus 97.8% on congested 5 GHz links, validating the migration to new spectrum for mission-critical robotics. These gains encourage organizations to absorb higher capital outlays in return for long-run productivity .

Smart-city initiatives and public Wi-Fi roll-outs

Municipal broadband programs increasingly favor Wi-Fi as the primary medium for digital inclusion because installation is quicker and less capital-intensive than fiber in sprawling rural territories. The Philippines commits USD 1.2 billion to deploy more than 100,000 public hotspots across 17,000 barangays by 2028, a template mirrored by several emerging economies. Europe's Digital Decade targets gigabit coverage by 2030 and positions Wi-Fi 7 mesh as an affordable last-mile alternative in mountainous and island regions. Cities monetize infrastructure by layering sensor backhaul for traffic, air-quality, and emergency-response schemes that self-fund through efficiency gains. Neutral-host deployments that blend Wi-Fi and 5G radios under OpenRoaming agreements generate fresh revenue as roaming fees while delivering seamless citizen connectivity.

Spectrum congestion and interference in unlicensed bands

Dense urban precincts such as Manhattan experience throughput drops near 60% during peak usage, even when Wi-Fi 6E hardware is present, because legacy devices crowd the 2.4 GHz spectrum. Microwave ovens, Bluetooth handsets, and older routers create overlapping noise that adaptive algorithms cannot fully evade. Enterprises increasingly hire spectrum consultants, a service costing USD 50,000-200,000 on expansive campuses, to engineer channel plans that meet service-level objectives. Regulators consider quasi-licensed regimes akin to CBRS so that critical IoT traffic can operate free of consumer interference. Although the 6 GHz allocation temporarily alleviates pressure, forecasts show saturation within five years as IoT endpoints grow exponentially.

Other drivers and restraints analyzed in the detailed report include:

- Rapid adoption of Wi-Fi 6/6E and upcoming Wi-Fi 7

- Hybrid/remote work models demanding high-capacity WLAN

- Heightened data-privacy and security compliance costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, access points contributed 35.92% to the Wi-Fi market share, underlining hardware's continuing relevance even as revenue mix shifts. The services segment, however, is projected to compound at 15.98% through 2031, reflecting the pivot to Network-as-a-Service frameworks that convert upfront capital into recurring operating expense. Cost pressures commoditize standalone routers and range extenders, while cloud-native orchestration platforms take over the policy and analytics roles previously executed by on-premises controllers. Managed service providers leverage artificial intelligence to automate channel allocation, load balancing, and anomaly detection, ultimately delivering 75% fewer unplanned-outage minutes than customer-operated networks. By 2031, the Wi-Fi market size attributed to software and services is expected to eclipse hardware contribution in mature economies as organizations prioritize life-cycle flexibility over asset ownership.

The shift mirrors broader IT procurement trends that favor outcomes over ownership. Consumption-based pricing aligns WLAN costs with occupancy levels, flattening budget spikes and improving CFO visibility. Vendors bundle proactive maintenance, security compliance, and real-time experience scoring to differentiate beyond hardware. Edge gateways and ruggedized IoT bridges constitute a small but fast-rising category, supplying deterministic connectivity in harsh industrial zones where vibration, dust, and temperature extremes invalidate consumer-grade gear. As AI chips embed inside access points, even commodity hardware gains value when offered as a managed experience that abstracts complexity and accelerates time to productivity.

The Wi-Fi Market Report is Segmented by Component (Hardware, Solutions, Services), End-User Vertical (Consumer, Enterprise/Corporate Campuses, Education, Healthcare, Hospitality and Retail, Industrial and Logistics), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounts for 40.55% of the Wi-Fi market in 2025, owing to USD 65 billion in broadband incentives and rapid enterprise refresh cycles. Early access to 6 GHz spectrum allows institutions to pioneer tri-band deployments, creating a performance gap over regions still seeking regulatory clearance. Fortune 500 companies refresh their WLAN every five years, two years faster than the global average, to equip smart offices tailored for hybrid work. Healthcare and education pillars represent robust growth nodes as telehealth and distance learning require enterprise-grade reliability.

Asia Pacific records the fastest trajectory with a 15.12% CAGR through 2031, enabled by national digital strategies that treat wireless as primary rather than complementary infrastructure. China's factory-automation boom, amplified by policy to cultivate domestic chipset capability, translates to bulk orders for industrial-grade Wi-Fi 6E equipment. India's Digital India mission envisions connecting 600,000 villages via Wi-Fi mesh, making wireless the linchpin of rural inclusion. Southeast Asian economies integrate WLAN across tourism hubs and export-oriented manufacturing parks, while government subsidies shrink payback periods and accelerate deployments. Smart-city funding rounds across Jakarta, Bangkok, and Ho Chi Minh City further elevate regional demand.

Europe's growth remains orderly as Industry 4.0 uptake and Digital Decade mandates require gigabit household coverage by 2030. Wi-Fi serves as the cost-effective last-mile solution in rugged topographies like the Alps and the Greek islands. OpenRoaming agreements spearheaded by the EU Digital Single Market create frictionless cross-border connectivity, bolstering tourism and remote business travel. Germany leads industrial adoption, whereas Nordic nations focus on smart-grid and sustainability use cases that rely on energy-efficient TWT scheduling. The Middle East and Africa invest in Wi-Fi to diversify economies beyond hydrocarbons and to bridge digital divides in rural deserts and mountainous terrain.

- Cisco Systems, Inc.

- Hewlett Packard Enterprise (Aruba)

- Huawei Technologies Co., Ltd.

- CommScope Holding Company Inc.(Ruckus Networks)

- Juniper Networks Inc.

- Telefonaktiebolaget LM Ericsson

- Extreme Networks, Inc.

- Ubiquiti Inc.

- Fortinet Inc.

- TP-Link Technologies Co., Ltd.

- Netgear Inc.

- D-Link Corporation

- Zyxel Communications Corp.

- Qualcomm Technologies, Inc.

- Broadcom Inc.

- Intel Corporation

- MediaTek Inc.

- Cambium Networks Ltd.

- EnGenius Networks, Inc. (Elitegroup)

- Purple WiFi Ltd.

- Cloud4Wi Inc.

- MetTel Inc.

- Singtel Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of IoT and smart devices

- 4.2.2 Smart-city initiatives and public WiFi roll-outs

- 4.2.3 Rapid adoption of WiFi 6/6E and upcoming WiFi 7

- 4.2.4 Hybrid/remote work models demanding high-capacity WLAN

- 4.2.5 Convergence of WiFi and 5G via OpenRoaming/Passpoint

- 4.2.6 Energy-efficient TWT features for battery-powered IoT nodes

- 4.3 Market Restraints

- 4.3.1 Spectrum congestion and interference in unlicensed bands

- 4.3.2 Heightened data-privacy/security compliance costs

- 4.3.3 Li-Fi and 60 GHz alternatives cannibalizing dense-WiFi use cases

- 4.3.4 Chipset supply constraints delaying WiFi 7 device launches

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Access Points

- 5.1.1.2 Routers and Extenders

- 5.1.1.3 Wireless Controllers

- 5.1.1.4 Other Device Types

- 5.1.2 Solutions

- 5.1.3 Services

- 5.1.1 Hardware

- 5.2 By End-user Vertical

- 5.2.1 Consumer

- 5.2.2 Enterprise/Corporate Campuses

- 5.2.3 Education

- 5.2.4 Healthcare

- 5.2.5 Hospitality and Retail

- 5.2.6 Industrial and Logistics

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 Asia Pacific

- 5.3.4.1 China

- 5.3.4.2 Japan

- 5.3.4.3 South Korea

- 5.3.4.4 India

- 5.3.4.5 Australia and New Zealand

- 5.3.4.6 Rest of Asia Pacific

- 5.3.5 Middle East

- 5.3.5.1 GCC

- 5.3.5.2 Turkey

- 5.3.5.3 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Nigeria

- 5.3.6.3 Rest of Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems, Inc.

- 6.4.2 Hewlett Packard Enterprise (Aruba)

- 6.4.3 Huawei Technologies Co., Ltd.

- 6.4.4 CommScope Holding Company Inc.(Ruckus Networks)

- 6.4.5 Juniper Networks Inc.

- 6.4.6 Telefonaktiebolaget LM Ericsson

- 6.4.7 Extreme Networks, Inc.

- 6.4.8 Ubiquiti Inc.

- 6.4.9 Fortinet Inc.

- 6.4.10 TP-Link Technologies Co., Ltd.

- 6.4.11 Netgear Inc.

- 6.4.12 D-Link Corporation

- 6.4.13 Zyxel Communications Corp.

- 6.4.14 Qualcomm Technologies, Inc.

- 6.4.15 Broadcom Inc.

- 6.4.16 Intel Corporation

- 6.4.17 MediaTek Inc.

- 6.4.18 Cambium Networks Ltd.

- 6.4.19 EnGenius Networks, Inc. (Elitegroup)

- 6.4.20 Purple WiFi Ltd.

- 6.4.21 Cloud4Wi Inc.

- 6.4.22 MetTel Inc.

- 6.4.23 Singtel Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

Wi-Fi市場-2026-2032年全球市場預測

Wi-Fi市場-2026-2032年全球市場預測 Wi-Fi 7 企業解決方案市場預測至 2034 年-按交付方式、設施類型、應用、最終用戶和地區分類的全球分析

Wi-Fi 7 企業解決方案市場預測至 2034 年-按交付方式、設施類型、應用、最終用戶和地區分類的全球分析 MiFi市場:按設備類型、最終用戶和地區分類

MiFi市場:按設備類型、最終用戶和地區分類 Wi-Fi市場趨勢

Wi-Fi市場趨勢 2026年全球Wi-Fi漫遊最佳化市場報告2026年全球無線網路基地台市場報告2026年全球託管Wi-Fi解決方案市場報告

2026年全球Wi-Fi漫遊最佳化市場報告2026年全球無線網路基地台市場報告2026年全球託管Wi-Fi解決方案市場報告 Wi-Fi市場規模、佔有率和成長分析:按交付方式、部署方式、技術、應用、最終用戶產業和地區分類-2026-2033年產業預測

Wi-Fi市場規模、佔有率和成長分析:按交付方式、部署方式、技術、應用、最終用戶產業和地區分類-2026-2033年產業預測 2026-2030年全球無線網路基地台市場

2026-2030年全球無線網路基地台市場 Wi-Fi 市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和功能分類

Wi-Fi 市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和功能分類