|

市場調查報告書

商品編碼

1937344

氯化聚乙烯:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Chlorinated Polyethylene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

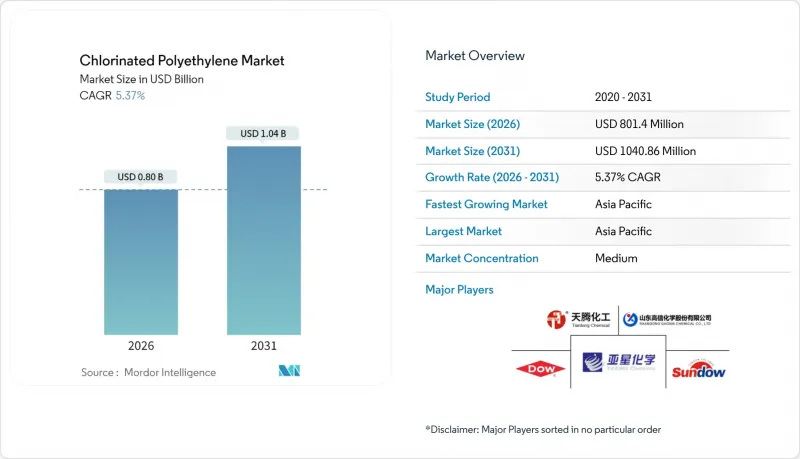

預計到 2026 年,氯化聚乙烯市場規模將達到 8.014 億美元,高於 2025 年的 7.6056 億美元。

預計到 2031 年將達到 10.4086 億美元,2026 年至 2031 年的複合年成長率為 5.37%。

這種持續成長反映了該聚合物作為熱可塑性橡膠的作用日益增強,彌合了傳統橡膠和塑膠之間的差距,並擴大應用於電纜護套、衝擊改質劑和軟管等領域。強勁的需求主要受三個因素驅動:電動車的加速普及、日益嚴格的建築規範鼓勵使用耐用型PVC共混物,以及東亞氯鹼一體化產業叢集所提供的價格競爭力。能夠提供符合無鹵防火安全標準、高介電強度和循環經濟計劃的配方的供應商,正在贏得汽車製造商和建築承包商的青睞。山東省產能的快速擴張和內部氯氣採購持續對全球價格構成下行壓力,但其生產規模的擴大也降低了長期供不應求的風險。同時,歐洲對氯化塑膠的公共採購限制和原料價格的波動,為成本轉嫁帶來了挑戰,只有技術靈活的生產商才能應對。

全球氯化聚乙烯市場趨勢及洞察

綠建築應用領域對PVC的需求激增

隨著建築師轉向使用再生PVC門窗和牆板,永續建築標準推動了氯化聚乙烯(CPE)消費量的成長。這些材料即使在低溫下也需要優異的抗衝擊性能。氯化聚乙烯135A最佳化了高回收配方中的熔融性能,使加工商能夠在保持韌性的同時減少對其他加工助劑的需求。尋求LEED和BREEAM認證積分的建築商現在指定使用CPE改質型材,因為實驗數據證實,與未改質PVC相比,CPE改質型材在更寬的溫度範圍內具有穩定的延展性。添加生物基塑化劑的聚合物共混物進一步增強了這一優勢,減少了原生氯的總體用量——這是綠色政府採購競標中的關鍵論點。因此,在再生PVC流中能夠展現穩定Izod衝擊值的氯化聚乙烯等級在大都會圈維修專案中獲得了銷售優勢。

電動車的快速普及推動了對電纜護套材料的需求。

電動車平台依賴高壓線束、充電線和電池冷卻管路,這些部件必須能夠承受液體飛濺、熱循環和電磁干擾。氯化聚乙烯具有過氧化物硫化三元乙丙橡膠 (EPDM) 所缺乏的關鍵介電強度和低溫柔柔軟性,這使得汽車製造商在從 400V 架構過渡到 800V 架構時能夠標準化護套材料。設計工程師特別重視其對磷酸酯類冷卻劑的耐受性,這種失效模式限制了許多熱塑性硫化橡膠的應用。隨著軟管直徑因電池加熱迴路的全面普及而增大,氯化聚乙烯彈性體在低溫下保持彎曲半徑的優勢變得更加顯著。目前,UL 94 V-0 認證、無鹵素、預著色氯化聚乙烯 (CPE) 化合物的供應商表示,他們已收到來自原始設備製造商 (OEM) 的多年採購承諾,並明確了報廢回收目標。

氯氣和乙烯價格波動

受苛性鈉供需動態以及氧化鋁精煉廠需求變化的影響,氯氣現貨價格在12個月內波動超過60%,給在公開市場上採購氯氣的非一體化氯乙烯(CPE)生產商帶來了壓力。同時,美國墨西哥灣沿岸蒸汽裂解裝置的停產擴大了乙烯合約溢價,並提高了下游氯化聚乙烯原料的成本。高能耗的膜電解進一步加劇了電價飆升,將變動成本推入了「下游需求中斷轉嫁區」。雖然一體化生產商更有能力抵禦價格波動,但需要透過原物料庫存來緩衝價格波動,這加劇了其營運資金緊張的局面。混煉商透過調整配方降低氯含量來抵消部分影響,但這種策略限制了最高熱變形溫度,並縮小了應用範圍。

細分市場分析

2025年,CPE 135A的銷售量將保持在52.90%,這得益於其均衡的分子量分佈,從而確保了硬質PVC在牆板和型材擠出生產線中具有更高的韌性。 135A級產品相對較低的慕尼粘度降低了混煉成本,因此深受高產能建築型材擠出機的青睞。同時,CPE 135B預計將以5.46%的複合年成長率成長,因為軟管、管材和耐化學腐蝕墊片的混煉商願意為其卓越的耐油耐酸性能支付溢價。需求加速成長主要集中在氫氣軟管領域,由於壓力評級的提高,該領域對滲透性能的要求也越來越高。具有客製化氯含量的特種等級產品佔總價值的18%,這得益於太陽能電池板背板共擠出這一細分市場,該市場要求產品在145°C下經兩小時的烘箱老化穩定性。

本產品領域的創新主要圍繞在以135B為基礎的無鹵阻燃型產品展開,這些產品兼具V-0阻燃等級和300%的斷裂伸長率。製造商採用反應擠出技術將磷基團直接錨定到聚合物鏈上,從而減少泛白和表麵粉化。雖然產量仍處於早期階段,但其在鐵路墊片應用中的早期應用已證明了商業性可行性。一些過氧化氫交聯的氯化聚乙烯(CPE)雖然技術上不屬於標準編號系統,但由於它們無需更換模具即可替代過氧化物硫化的三元乙丙橡膠(EPDM),因此具有很強的議價能力。這些趨勢表明,未來氯化聚乙烯市場的產品組合變化不僅取決於價格,還取決於性能差異化。

氯化聚乙烯市場報告按產品(CPE 135A、CPE 135B、其他產品)、應用(衝擊改質劑、電線電纜塗層、軟管和管材、黏合劑、其他應用)和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行細分。市場預測以以金額為準和銷售兩種形式提供。

區域分析

到2025年,亞太地區將佔總收入的72.10%,鞏固其主導地位,這主要得益於中國一體化的氯鹼聯合企業和不斷擴張的下游PVC產業。到2031年,亞太地區5.70%的複合年成長率凸顯了東南亞、印度和韓國的成長勢頭,這些地區正在建設電動車電池超級工廠,建設支出持續成長。當地自有氯氣供應降低了現金成本,並吸引西方混料生產商簽訂加工合約以規避運費風險。日本特種電纜製造商也依賴區域供應,但為了滿足其獨特的防火安全標準,他們需要從歐洲進口高價值的母粒,這反映了區域內CPE性能特徵的貿易往來。

在美國,一波電動車補貼浪潮刺激了高壓電纜的需求。然而,由於北美只有兩家工廠生產這種聚合物,轉換器公司不得不從太平洋沿岸進口以補充需求。墨西哥的乘用車組裝和家電工廠正在推動當地需求,而美墨加協定(USMCA)的條款正在促進線束組件的採購,鼓勵洲內採購。

在歐洲,由於禁止公共採購氯化塑膠,擴張速度放緩。然而,永續性的壓力正在推動CPE回收的研究與發展。目前,一家德國型材擠出製造商正在測試一種基於溶劑的剝離循環工藝,以從窗框邊角料中回收含CPE的組件。在中東和非洲,由於卡達和沙烏地阿拉伯的大型企劃需要能夠承受紫外線和沙粒磨損的耐用電線塗層,預計需求將溫和成長。巴西是南美洲的關鍵市場,當地住宅建設的復甦正在推動對CPE抗衝擊改質PVC管材的需求。然而,匯率波動限制了需求的快速成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 綠建築應用領域對PVC的需求激增

- 電動車的快速電氣化正在推動對電纜護套材料的需求。

- 向無鹵阻燃CPE混合材料過渡

- 透過擴大中國供給面來增強價格競爭力

- 用於氫氣加註基礎設施的耐油軟管

- 市場限制

- 氯氣和乙烯價格波動

- 歐盟公共採購中禁止使用氯化塑膠

- 提高TPV作為替代彈性體的性能

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依產品

- CPE 135A

- CPE 135B

- 其他產品

- 透過使用

- 衝擊改質劑

- 電線電纜護套材料

- 軟管和管件

- 黏合劑

- 其他用途

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Aurora Material Solutions

- Bontecn Group China Co. Ltd

- Dow

- Dycon Chemicals

- Epigral Limited

- Hangzhou Keli Chemical Co. Ltd

- Jiangsu Tianteng Chemical Industry Co. Ltd

- Resonac Holdings Corporation

- Shandong Gaoxin Chemical Co. Ltd

- Shandong Ketian Chemical Co. Ltd

- Shandong Novista Chemical Ltd(Novista Group)

- Shandong Rike Chemical Co.,Ltd

- Shandong Xiangsheng New Materials Technology Co. Ltd

- Shandong Xuye New Materials Co. Ltd

- Sundow Polymers Co. Ltd

- Weifang Yaxing Chemical Co. Ltd

第7章 市場機會與未來展望

Chlorinated Polyethylene Market size in 2026 is estimated at USD 801.4 million, growing from 2025 value of USD 760.56 million with 2031 projections showing USD 1040.86 million, growing at 5.37% CAGR over 2026-2031.

This sustained expansion mirrors the polymer's expanding role as a thermoplastic elastomer that bridges traditional rubber and plastic functions, finding growing use across cable jacketing, impact modifiers, and flexible hose products. Demand resilience stems from three visible forces: accelerating electric-vehicle electrification, stricter building codes favoring durable PVC blends, and the competitive pricing unlocked by integrated chlor-alkali clusters in East Asia. Suppliers that align formulations with halogen-free fire-safety rules, elevated dielectric thresholds, and circular-economy ambitions are capturing specification wins from automakers and construction contractors. Rapid capacity additions in Shandong, coupled with captive chlorine sourcing, continue to pressure global price floors, yet that same manufacturing scale reduces the risk of chronic shortages. Conversely, public-procurement restrictions on chlorinated plastics in Europe and raw-material price gyrations raise cost-pass-through challenges that only technologically agile producers can navigate.

Global Chlorinated Polyethylene Market Trends and Insights

Surging PVC Demand in Green Building Applications

Sustainable-building rules spur incremental chlorinated polyethylene consumption as architects shift toward recycled PVC doors, windows, and siding that still need robust impact performance at low temperatures. Chlorinated polyethylene 135A optimizes fusion in high-recycled-content formulations, letting converters cut separate processing aids without sacrificing toughness. Builders seeking LEED or BREEAM points now specify CPE-modified profiles because lab data confirm stable ductility across a wider temperature band than unmodified PVC. Polymer blends that integrate bio-based plasticizers push that advantage further by reducing overall virgin chlorine intensity, a key talking point in green-public-procurement bids. Consequently, chlorinated polyethylene grades that can demonstrate consistent Izod impact values in secondary PVC streams are winning volume awards in metropolitan retrofits.

Rapid EV Electrification Driving Cable Jacketing Demand

Electric-vehicle platforms rely on high-voltage harnesses, charging cords, and battery-coolant lines that must withstand fluid splash, thermal cycling, and electromagnetic interference. Chlorinated polyethylene delivers the critical dielectric strength and low-temperature flexibility missing in peroxide-cured EPDM, enabling automakers to standardize jacketing compounds even as they move from 400 V to 800 V architectures. Design engineers particularly value the polymer's resistance to phosphate-ester coolant exposure, a failure mode that limits many thermoplastic vulcanizates. Shifts toward full-battery heating loops enlarge hose diameters, magnifying the benefit of low-temperature bend radius retention inherent to chlorinated polyethylene elastomers. Suppliers offering pre-colored halogen-free CPE compounds with UL 94 V-0 ratings now report multi-year sourcing nominations from original-equipment manufacturers unabashedly targeting end-of-life recyclability targets.

Volatile Chlorine and Ethylene Costs

Spot prices for chlorine swung by more than 60% within 12 months as caustic-soda dynamics shifted with alumina-refining demand, squeezing non-integrated CPE producers that purchase chlorine on the open market. Meanwhile, ethylene contract premiums widened on steam-cracker outages in the U.S. Gulf Coast, raising polyethylene feedstock costs for downstream chlorination. Energy-intensive membrane-cell electrolysis further magnifies electricity price spikes, pushing variable costs into a territory where passing them downstream risks demand destruction. Integrated producers withstand turbulence better, yet even they face higher working-capital locks because raw-material inventories must buffer price whiplash. Compounders offset part of the impact by reformulating with lower chlorination levels, but that strategy caps achievable heat-deflection temperatures and thus limits application windows.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Halogen-Free Flame-Retardant CPE Hybrids

- Chinese Supply-Side Expansion Enhancing Price Competitiveness

- EU Public-Procurement Bans on Chlorinated Plastics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

CPE 135A retained 52.90% of 2025 volumes because its balanced molecular-weight distribution reliably boosts rigid PVC toughness in siding and profile extrusion lines. Grade 135A's relatively low Mooney viscosity keeps compounding costs contained, which appeals to high-throughput construction profile extruders. Conversely, CPE 135B demonstrates a 5.46% CAGR projection as formulators in hose, tubing, and chemical-tolerant gaskets pay premiums for its superior oil and acid resistance. Demand acceleration concentrates in hydrogen-service hoses where permeation limits tighten with rising pressure ratings. Specialty grades with custom chlorine content represent 18% of value, benefitting from co-extrusion niches in solar-panel back-sheets that need two-hour oven-aging stability at 145 °C.

Innovation inside the product landscape orbits around halogen-free flame-retardant variants built on the 135B backbone that marry V-0 flame rating with 300% elongation at break. Producers deploy reactive extrusion to lock phosphorus moieties directly into the polymer chain, reducing blooming and surface chalking. Although volumes remain nascent, early adopters in rail-transit gasket applications validate commercial readiness. Some high-dicumyl-peroxide cross-linkable CPEs, while technically outside standard numbering, command strong bargaining power because they replace peroxide-cured EPDM without tooling changes. These dynamics underline how performance differentiation rather than price alone will define future product-mix shifts inside the chlorinated polyethylene market.

The Chlorinated Polyethylene Market Report is Segmented by Product (CPE 135A, CPE 135B, and Other Products), Application (Impact Modifiers, Wire and Cable Jacketing, Hose and Tubing, Adhesives, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value and Volume.

Geography Analysis

Asia-Pacific generated 72.10% of 2025 revenue, reaffirming the region's leadership anchored in China's integrated chlor-alkali complexes and its expansive downstream PVC industries. A 5.70% CAGR to 2031 underscores momentum across Southeast Asia, India, and South Korea, where EV battery gigafactories sprout and construction spending persists. Local captive chlorine supplies compress cash-cost curves, drawing in Western compounders that set up tolling deals to hedge against freight volatility. Japan's specialty cable producers also lean on regional supply, though they import premium halogen-free masterbatches from Europe for distinct fire-safety norms, reflecting an intra-regional trade of performance flavors of CPE.

The United States benefits from an EV subsidy wave that accelerates high-voltage cable demand. However, only two North American plants produce the polymer, forcing converters to backfill via Pacific-coast imports. Mexico's passenger-vehicle assembly lines and appliance factories enhance regional pull, aided by USMCA provisions that favor continental sourcing of wiring content.

Europe faces slower expansion given public procurement bans on chlorinated plastics. Sustainability pressures nonetheless trigger research and development on CPE recycling, with German profile extruders trialing solvent-based delamination loops to harvest CPE-rich fractions from window offcuts. Middle-East and Africa hold modest but rising prospects as megaprojects in Qatar and Saudi Arabia demand durable wire-coating materials that cope with UV and sand abrasion. Brazil anchors South America, where residential-building rebounds lift demand for CPE impact-modified PVC pipes, yet currency volatility tempers aggressive uptake.

- Aurora Material Solutions

- Bontecn Group China Co. Ltd

- Dow

- Dycon Chemicals

- Epigral Limited

- Hangzhou Keli Chemical Co. Ltd

- Jiangsu Tianteng Chemical Industry Co. Ltd

- Resonac Holdings Corporation

- Shandong Gaoxin Chemical Co. Ltd

- Shandong Ketian Chemical Co. Ltd

- Shandong Novista Chemical Ltd (Novista Group)

- Shandong Rike Chemical Co.,Ltd

- Shandong Xiangsheng New Materials Technology Co. Ltd

- Shandong Xuye New Materials Co. Ltd

- Sundow Polymers Co. Ltd

- Weifang Yaxing Chemical Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging PVC Demand in Green Building Applications

- 4.2.2 Rapid EV Electrification Driving Cable Jacketing Demand

- 4.2.3 Shift Toward Halogen-Free Flame-Retardant CPE Hybrids

- 4.2.4 Chinese Supply-Side Expansion Enhancing Price Competitiveness

- 4.2.5 Oil-Resistant Hoses for Hydrogen Refuelling Infrastructure

- 4.3 Market Restraints

- 4.3.1 Volatile Chlorine and Ethylene Costs

- 4.3.2 EU Public-Procurement Bans on Chlorinated Plastics

- 4.3.3 TPV Performance Advances as Substitute Elastomers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 CPE 135A

- 5.1.2 CPE 135B

- 5.1.3 Other Products

- 5.2 By Application

- 5.2.1 Impact Modifiers

- 5.2.2 Wire and Cable Jacketing

- 5.2.3 Hose and Tubing

- 5.2.4 Adhesives

- 5.2.5 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Aurora Material Solutions

- 6.4.2 Bontecn Group China Co. Ltd

- 6.4.3 Dow

- 6.4.4 Dycon Chemicals

- 6.4.5 Epigral Limited

- 6.4.6 Hangzhou Keli Chemical Co. Ltd

- 6.4.7 Jiangsu Tianteng Chemical Industry Co. Ltd

- 6.4.8 Resonac Holdings Corporation

- 6.4.9 Shandong Gaoxin Chemical Co. Ltd

- 6.4.10 Shandong Ketian Chemical Co. Ltd

- 6.4.11 Shandong Novista Chemical Ltd (Novista Group)

- 6.4.12 Shandong Rike Chemical Co.,Ltd

- 6.4.13 Shandong Xiangsheng New Materials Technology Co. Ltd

- 6.4.14 Shandong Xuye New Materials Co. Ltd

- 6.4.15 Sundow Polymers Co. Ltd

- 6.4.16 Weifang Yaxing Chemical Co. Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Research and Development on Advanced CPE Grades

氯化聚乙烯市場:依形態、性能等級、應用、終端用戶產業及通路分類-2026-2032年全球預測

氯化聚乙烯市場:依形態、性能等級、應用、終端用戶產業及通路分類-2026-2032年全球預測 2025-2033年氯化聚乙烯市場報告(依等級類型、應用、最終用途產業及地區)

2025-2033年氯化聚乙烯市場報告(依等級類型、應用、最終用途產業及地區) 氯化聚乙烯 (CPE) 市場、全球需求分析、地區、應用及預測(~2034年)

氯化聚乙烯 (CPE) 市場、全球需求分析、地區、應用及預測(~2034年) 氯化聚乙烯市場規模、佔有率和成長分析(按產品、氯含量、應用、最終用途行業和地區)- 2025-2032 年行業預測

氯化聚乙烯市場規模、佔有率和成長分析(按產品、氯含量、應用、最終用途行業和地區)- 2025-2032 年行業預測 2030 年氯化聚乙烯市場預測:按等級、應用和地區進行的全球分析氯化聚乙烯市場、規模、佔有率、趨勢、行業分析報告:依產品、應用和地區 - 市場預測(2025-2034)氯化聚乙烯的全球市場(2018年~2034年)

2030 年氯化聚乙烯市場預測:按等級、應用和地區進行的全球分析氯化聚乙烯市場、規模、佔有率、趨勢、行業分析報告:依產品、應用和地區 - 市場預測(2025-2034)氯化聚乙烯的全球市場(2018年~2034年) 2024 年至 2031 年氯化聚乙烯市場(按等級、應用和地區劃分)

2024 年至 2031 年氯化聚乙烯市場(按等級、應用和地區劃分)