|

市場調查報告書

商品編碼

1937339

烷基糖苷:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Alkyl Polyglycoside - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

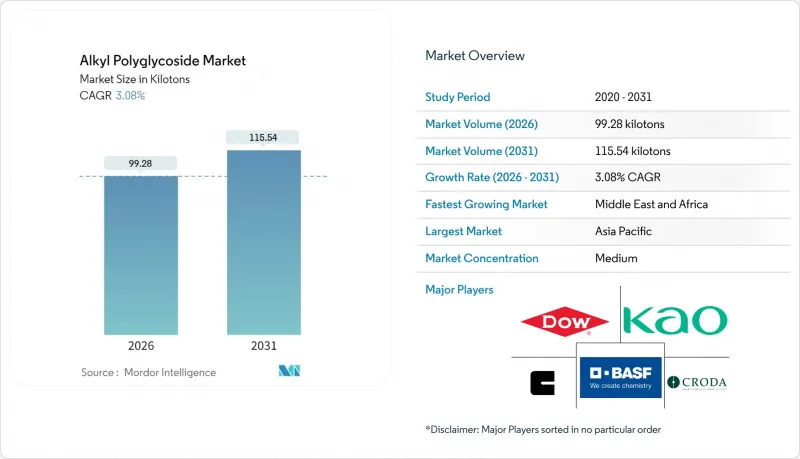

預計到 2026 年,烷基聚醣苷市場規模將達到 99.28 千噸,高於 2025 年的 96.31 千噸。

預計到 2031 年,產量將達到 115.54 千噸,預計從 2026 年到 2031 年的複合年成長率為 3.08%。

需求成長主要受以下因素驅動:有害非離子界面活性劑的逐步淘汰、配方快速轉向生物基原料,以及產能的穩定擴張穩定了原料供應。家用和個人護理產品製造商擴大指定使用烷基聚葡萄糖苷界面活性劑以滿足生態標籤標準,而油田服務公司則採用APG可濕性粉劑來滿足環境排放限制。亞洲製造商正利用其在棕櫚油和椰子油衍生脂醇類採購方面的地理優勢來確保出口契約,而歐洲供應商則透過強調永續性的品牌建設來確立高階市場地位。儘管原物料價格波動,且面臨來自甜菜鹼和氨基氧化物的競爭,但隨著大型綜合化工企業擴大生產規模和共用製程技術,成本曲線仍在持續改善。

全球烷基糖苷市場趨勢及洞察

家用和個人保健產品對生物基界面活性劑的需求不斷成長

為了獲得生態標籤認證和優質貨架空間,品牌所有者正在調整產品系列,專注於無硫酸鹽和植物來源成分。來自跨國消費品製造商的大訂單確保了未來需求的穩定,促使供應商擴大產能,並改善用於沖洗型和免沖洗型產品的專用等級。配方師們看重烷基聚葡萄糖苷界面活性劑的溫和性、酵素協同作用和無硫酸鹽特性,同時也能保持高效的去污能力。精通數位技術的消費者正在仔細查看成分標籤,這給零售商施加了壓力,要求他們儲備含有可識別的糖基界面活性劑的成品。亞洲契約製造正在積極回應,提供整合烷基多醣苷的承包解決方案,從而縮短全球自有品牌零售商的創新前置作業時間。

逐步淘汰壬基酚聚氧乙烯醚(NPE)和其他有害界面活性劑

歐洲化學品管理局 (ECHA) 已禁止壬基酚聚氧乙烯醚 (NPE) 的大部分用途,從而推動了全球供應鏈加速替代計畫的實施。美國《有毒物質管制法》(TSCA) 的風險評估和各州層級的舉措與歐洲的立場相呼應,縮短了替代品的檢驗週期。烷基聚葡萄糖苷乙烯醚殘留,從而減輕了文件負擔和下游廢棄物處理風險。採購部門報告稱,與根據例外條款維持 NPE 庫存相比,過渡到 APG 可降低合規成本。明確的政策方向降低了人們對技術風險的認知,使 APG 成為設施清潔和紡織品加工領域非離子替代品的標準選擇。

天然脂醇類與澱粉原料價格波動

脂醇類成本約佔烷基聚葡萄糖苷變動成本的65%,這使得生產商極易受到原料價格波動的影響,而原料價格波動又受到生物柴油強制摻混政策和受天氣影響的收割週期的影響。 2023年,C12-C14醇的價格跌至每噸1,467美元,隨後在2024年反彈超過30%,這主要是由於厄爾尼諾現象導致棕櫚油產量下降。現貨價格的飆升迫使生產商每季調整價格,這給簽訂固定零售合約的清潔劑配方生產商帶來了不確定性。雖然一些烷基多醣苷供應商透過簽訂長期人工林合約來對沖風險,但乾旱、勞動力短缺和植物檢疫限制仍然可能限制交付。投資者在為新建烷基多醣苷工廠分配資金時會考慮這些不確定性,這可能導致計劃啟動時間延長。

細分市場分析

到2025年,脂醇類類產品將佔總產量的42.10%,這將支撐未來數十年的規模經濟效益,並確保清潔劑醇裂解裝置穩定供應月桂醇。精湛的生產流程可確保產品在顏色、氣味和聚合度方面的一致性——這些都是大眾市場濃縮清潔劑的關鍵特性。植物油基產品將以3.55%的複合年成長率(CAGR)實現最高成長,這得益於連續酯交換和酶促合成技術的進步,這些技術能夠縮短生產週期並降低碳排放強度。預計到2031年,植物油衍生的烷基聚葡萄糖苷市場規模將從2025年的27.54千噸成長至33.92千噸,這反映了東協和南美生物柴油叢集集群原料的快速多元化。

新興的醣類和玉米粉基烷基聚葡萄糖苷產品,憑藉兩位數的毛利率,為小眾個人保健產品線提供服務,彌補了供應鏈不成熟和單位成本高的不足。同時,脂醇類生產商正在改進衝擊流反應器,將醇與葡萄糖的莫耳比降低到3:1以下,從而減少5%的原料投入並提高產量。供應商正將這些工藝創新與基於區塊鏈的溯源模組結合,追蹤人工林的來源,以滿足歐洲零售商的溯源要求。隨著植物油技術的規模化應用,其與脂醇類產品的價格差異正在縮小,促使企業採取聯合投資策略,模糊傳統的細分市場界線。

烷基聚葡萄糖苷市場報告按產品類型(脂醇類、糖、玉米粉、植物油及其他)、應用領域(個人護理及化妝品、家居用品、工業清潔劑、農藥及其他)和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行細分。市場預測以噸為單位。

區域分析

到2025年,亞太地區將佔全球產量的45.90%,這主要得益於中國一體化的石化產業群聚以及東南亞棕櫚油資源的接近性。當地的稅收優惠政策鼓勵對磺基琥珀酸酯、APG和甜菜鹼生產線的投資,從而在寧波和上海周邊地區打造出具有競爭力的製造群。印度美容和個人護理市場(預計到2025年價值200億美元)隨著無硫酸鹽洗髮精逐漸滲透到區域性城市,國內對APG的需求也不斷成長。泰國和馬來西亞已鞏固其作為脂醇類原料供應中心的地位,透過位於邦巴功和關丹的製造地商(OEM)大量出口APG。

儘管中東和非洲地區的市場規模較小,但預計該地區將以3.52%的複合年成長率(CAGR)實現最快成長,直至2031年。這主要得益於石油公司對用於提高採收率試驗井的環保添加劑的需求。沙烏地阿拉伯朱拜勒的一家下游企業正在運作一座APG中試工廠,該工廠毗鄰一條乙氧基化物生產線,從而實現了表面活性劑在同一物流區域內的混合。一家南非商用清潔劑配方生產商正在使用本地配製的APG濃縮液,以滿足超級市場自有品牌的永續性評分標準。地方政府的綠色採購政策正在公共清潔合約中優先考慮生物基表面活性劑,從而創造了穩定的需求基礎。

北美和歐洲的需求量正以個位數的溫和速度成長,這得益於積極的非離子介面活性劑劑(NPE)淘汰計劃和零售商自願加入的化學品監控清單。 Pilot Chemical公司獲得在俄亥俄州獨家生產Bio IOS技術的許可,該許可證將於2026年開始生效,這標誌著美國生物基界面活性劑領域將迎來新的資本投資。歐洲高階市場正在採用APG和氨基氧化物的混合物來平衡成本和發泡性能,而加州配方師則依靠APG來滿足更嚴格的消費品安全法規。儘管南美洲的絕對銷量落後於其他地區,但其在作物保護助劑領域正展現出強勁的成長勢頭,APG較低的植物毒性使其能夠滲透到Glyphosate替代配方中。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 家用和個人保健產品對生物基界面活性劑的需求不斷成長

- 逐步淘汰壬基酚聚氧乙烯醚(NPE)和其他有害界面活性劑

- 脂醇類供應商的產能擴張與後向整合

- APG可濕性粉劑在鹼性工業清潔劑和油田流體的應用日益廣泛

- 低成本的高密度衝擊流反應器可實現醇與葡萄糖比例小於 3:1。

- 市場限制

- 天然脂醇類與澱粉原料價格波動

- 可用的其他溫和界面活性劑(例如,甜菜鹼、氨基氧化物)

- 透過嚴格的RSPO/無毀林棕櫚油供應審核,嚴格把控原料採購。

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依產品類型

- 脂醇類

- 糖

- 玉米粉

- 植物油

- 其他產品類型

- 透過使用

- 個人護理和化妝品

- 居家護理產品

- 工業用清潔劑

- 農業化學品

- 其他應用

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 印尼

- 泰國

- 馬來西亞

- 越南

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 土耳其

- 俄羅斯

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 埃及

- 奈及利亞

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- BASF

- Brillachem

- Clariant

- Croda International plc

- Dow

- Evonik Industries

- FENCHEM

- Galaxy Surfactants

- Kao Corporation

- Pilot Chemical Corp.

- Seppic(Arkema Group)

- Shanghai Chenhua International Trade Co., Ltd.

- Shanghai Fine Chemical Co., Ltd.

- Shanghai Sunwise Chemical Co., Ltd

- Silver Fern Chemical LLC.

第7章 市場機會與未來展望

Alkyl Polyglycoside market size in 2026 is estimated at 99.28 kilotons, growing from 2025 value of 96.31 kilotons with 2031 projections showing 115.54 kilotons, growing at 3.08% CAGR over 2026-2031.

Demand is driven by regulatory phase-outs of hazardous non-ionic surfactants, rapid shifts in formulation toward bio-based ingredients, and steady capacity additions that stabilize the raw-material supply. Home-care and personal-care producers increasingly specify Alkyl polyglucoside surfactants to align with ecolabel criteria, while oil-field service companies adopt APG hydrotropes to meet environmental discharge limits. Asian manufacturers capitalize on their proximity to palm- and coconut-based fatty alcohols to secure export contracts, whereas European suppliers leverage sustainability branding to achieve premium positioning. Despite feedstock price fluctuations and competition from betaines and amino oxides, cost curves continue to improve as integrated chemical majors scale up production and share process expertise.

Global Alkyl Polyglycoside Market Trends and Insights

Growing Demand for Bio-Based Surfactants in Home and Personal-Care Formulations

Brand owners reposition product portfolios around non-sulfate, plant-derived ingredients to secure ecolabel certifications and capture premium shelf space. Volume commitments from multinational fast-moving consumer goods companies create forward visibility, encouraging suppliers to expand capacity and refine grades tailored to rinse-off and leave-on products. Formulators favor Alkyl polyglucoside surfactants for mildness, low irritation, and synergy with enzymes, enabling sulfate-free laundry detergents that still deliver high soil removal. Digital-savvy consumers scrutinize ingredient lists, pushing retailers to stock finished goods containing recognizable sugar-based surfactants. Asian contract manufacturers respond with turnkey offerings that integrate APGs, shortening innovation lead times for global private-label retailers.

Regulatory Phase-Out of Nonyl-Phenol Ethoxylates and Other Hazardous Surfactants

The European Chemicals Agency banned NPEs in most applications, triggering accelerated substitution programs that ripple across global supply chains. US TSCA risk evaluations and state-level initiatives mirror Europe's stance, compressing customer timelines to validate alternatives. Alkyl polyglucoside surfactants fulfill performance specifications without secondary alcohol ethoxylate residues, easing dossier preparation and reducing downstream disposal liabilities. Procurement teams cite lower compliance costs when transitioning to APGs versus maintaining NPE-based inventories under derogation clauses. The clear direction of policy lowers perceived technology risk, making APGs the default non-ionic replacement in institutional cleaning and textile processing.

Volatility in Natural Fatty-Alcohol and Starch Feedstock Prices

Fatty-alcohol costs represent roughly 65% of Alkyl polyglucoside variable expenses, leaving producers vulnerable to commodity swings tied to bio-diesel mandates and weather-linked harvest cycles. After dropping to USD 1,467 per ton in 2023, C12-C14 alcohols rebounded by more than 30% in 2024 due to El Nino-related palm-oil yield reductions. Spot spikes force quarterly price resets that unsettle detergent formulators operating under fixed retail contracts. Some APG suppliers hedge their risks with long-term plantation agreements; however, drought, labor shortages, and phytosanitary restrictions can still curtail deliveries. Investors weigh these uncertainties when allocating capital to greenfield APG plants, which can occasionally result in lengthened project gestation periods.

Other drivers and restraints analyzed in the detailed report include:

- Capacity Additions and Backward Integration of Fatty-Alcohol Suppliers

- Rising Adoption of APG Hydrotropes in Alkaline Industrial Cleaning and Oil-Field Fluids

- Availability of Alternative Mild Surfactants (e.g., Betaines, Amino-Oxides)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fatty alcohol-based grades captured 42.10% of 2025 volume, underscoring decades of scale efficiencies and readily available lauryl alcohol streams from detergent-alcohol crackers. Their process familiarity assures consistent color, odor, and degree of polymerization, features critical to mass-market detergent concentrates. Vegetable-oil-derived variants exhibit the highest 3.55% CAGR, as continuous transesterification and enzymatic synthesis technologies enable shorter cycle times and lower carbon intensity. The Alkyl polyglucoside market size associated with vegetable-oil pathways is projected to expand from 27.54 kilotons in 2025 to 33.92 kilotons by 2031, reflecting rapid feedstock diversification among ASEAN and South American biodiesel clusters.

Up-and-coming sugar- and corn-starch-based APGs service niche personal-care lines that command double-digit gross margins, compensating for immature supply chains and higher unit costs. Meanwhile, fatty-alcohol producers refine impinging-stream reactors that reduce the alcohol-to-glucose molar ratio below 3:1, slicing raw-material inputs by 5% and enhancing yield. Suppliers pair these process strides with blockchain-enabled traceability modules that map the origins of plantations, satisfying traceability mandates from European retailers. As vegetable-oil technologies scale, price differentials versus fatty-alcohol routes narrow, inviting co-investment strategies that blur traditional segment boundaries.

The Alkyl Polyglucoside Market Report is Segmented by Product Type (Fatty Alcohol, Sugar, Corn-Starch, Vegetable Oil, and Other Product Type), Application (Personal Care and Cosmetics, Home-Care Products, Industrial Cleaners, Agricultural Chemicals, and Other Application), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

The Asia-Pacific region retained 45.90% of the global volume in 2025, driven by integrated petrochemical complexes in China and the proximity of palm oil in Southeast Asia. Provincial tax incentives encourage investment in sulfosuccinate, APG, and betaine lines, fostering a competitive manufacturing cluster around Ningbo and Shanghai. India's beauty and personal care sector, valued at USD 20 billion for 2025, amplifies domestic APG pull-through as sulfate-free shampoos penetrate Tier-II cities. Thailand and Malaysia consolidate their role as fatty-alcohol feedstock hubs, supplying Bangpakong and Kuantan sites that dispatch bulk APG to Japanese OEMs.

The Middle East and Africa are projected to post the fastest 3.52% CAGR through 2031, albeit from a smaller base, as national oil companies seek environmentally compatible additives for enhanced-oil-recovery pilot wells. Saudi downstream initiatives in Jubail include pilot APG units adjacent to ethoxylate trains, enabling surfactant blending within a single logistical zone. South African formulators of institutional cleaners adopt locally blended APG concentrates to meet supermarket private-label sustainability scorecards. Regional governments use green-procurement policies to prioritize bio-based surfactants for municipal cleaning contracts, building steady baseline demand.

North American and European volumes grow at modest single-digit rates underpinned by aggressive NPE withdrawal schedules and voluntary retailer chemical watch lists. Pilot Chemical's exclusive license to manufacture Bio IOS technology in Ohio from 2026 signals fresh capital injection into U.S. bio-based surfactants. European premium segments feature APG blends with amino-oxides to balance cost and foaming, while California formulators lean on APG to comply with Safer Consumer Products regulations. South America trails in absolute volume but registers momentum in crop-protection adjuvants, leveraging APG's low phytotoxicity to penetrate glyphosate replacement formulations.

- BASF

- Brillachem

- Clariant

- Croda International plc

- Dow

- Evonik Industries

- FENCHEM

- Galaxy Surfactants

- Kao Corporation

- Pilot Chemical Corp.

- Seppic (Arkema Group)

- Shanghai Chenhua International Trade Co., Ltd.

- Shanghai Fine Chemical Co., Ltd.

- Shanghai Sunwise Chemical Co., Ltd

- Silver Fern Chemical LLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for bio-based surfactants in home and personal-care formulations

- 4.2.2 Regulatory phase-out of nonyl-phenol ethoxylates (NPEs) and other hazardous surfactants

- 4.2.3 Capacity additions and backward integration of fatty-alcohol suppliers

- 4.2.4 Rising adoption of APG hydrotropes in alkaline industrial cleaning and oil-field fluids

- 4.2.5 Cost-cutting high-gravity impinging-stream reactors enabling <3:1 alcohol-to-glucose ratios

- 4.3 Market Restraints

- 4.3.1 Volatility in natural fatty-alcohol and starch feedstock prices

- 4.3.2 Availability of alternative mild surfactants (e.g., betaines, amino-oxides)

- 4.3.3 Stringent RSPO/deforestation-free palm supply audits tightening raw-material access

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Fatty Alcohol

- 5.1.2 Sugar

- 5.1.3 Corn-starch

- 5.1.4 Vegetable Oil

- 5.1.5 Other Product Type

- 5.2 By Application

- 5.2.1 Personal Care and Cosmetics

- 5.2.2 Home-care Products

- 5.2.3 Industrial Cleaners

- 5.2.4 Agricultural Chemicals

- 5.2.5 Other Application

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Indonesia

- 5.3.1.6 Thailand

- 5.3.1.7 Malaysia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Nordic Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 Nigeria

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF

- 6.4.2 Brillachem

- 6.4.3 Clariant

- 6.4.4 Croda International plc

- 6.4.5 Dow

- 6.4.6 Evonik Industries

- 6.4.7 FENCHEM

- 6.4.8 Galaxy Surfactants

- 6.4.9 Kao Corporation

- 6.4.10 Pilot Chemical Corp.

- 6.4.11 Seppic (Arkema Group)

- 6.4.12 Shanghai Chenhua International Trade Co., Ltd.

- 6.4.13 Shanghai Fine Chemical Co., Ltd.

- 6.4.14 Shanghai Sunwise Chemical Co., Ltd

- 6.4.15 Silver Fern Chemical LLC.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

全球烷基糖苷市場:市場規模、佔有率、趨勢和成長分析(2026-2034)

全球烷基糖苷市場:市場規模、佔有率、趨勢和成長分析(2026-2034) 烷基聚葡萄糖苷市場機會、成長要素、產業趨勢分析及2026-2035年預測。

烷基聚葡萄糖苷市場機會、成長要素、產業趨勢分析及2026-2035年預測。 烷基聚葡萄糖苷市場按產品類型、最終用途和地區分類

烷基聚葡萄糖苷市場按產品類型、最終用途和地區分類 烷基聚葡萄糖苷市場規模、佔有率及成長分析(按產品、主要功能、應用及地區分類)-2026-2033年產業預測

烷基聚葡萄糖苷市場規模、佔有率及成長分析(按產品、主要功能、應用及地區分類)-2026-2033年產業預測 烷基聚醣(APG)-全球市場佔有率和排名、總收入和需求預測(2025-2031年)

烷基聚醣(APG)-全球市場佔有率和排名、總收入和需求預測(2025-2031年) 烷基多醣市場-全球產業規模、佔有率、趨勢、機會及預測,依最終用途(個人護理及化妝品、居家護理產品、工業清潔劑、農業化學品、其他)細分,按地區及競爭情況,2020-2030 年預測

烷基多醣市場-全球產業規模、佔有率、趨勢、機會及預測,依最終用途(個人護理及化妝品、居家護理產品、工業清潔劑、農業化學品、其他)細分,按地區及競爭情況,2020-2030 年預測 全球烷基聚葡萄糖苷市場

全球烷基聚葡萄糖苷市場 2018-2034年全球烷基多醣體(APG)市場需求及預測分析

2018-2034年全球烷基多醣體(APG)市場需求及預測分析 烷基聚葡萄糖苷(APG)生物界面活性劑市場報告:趨勢、預測和競爭分析(至 2031 年)烷基聚葡萄糖苷界面活性劑市場報告:趨勢、預測和競爭分析(至2031年)

烷基聚葡萄糖苷(APG)生物界面活性劑市場報告:趨勢、預測和競爭分析(至 2031 年)烷基聚葡萄糖苷界面活性劑市場報告:趨勢、預測和競爭分析(至2031年)