|

市場調查報告書

商品編碼

1937333

陶瓷膜:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Ceramic Membranes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

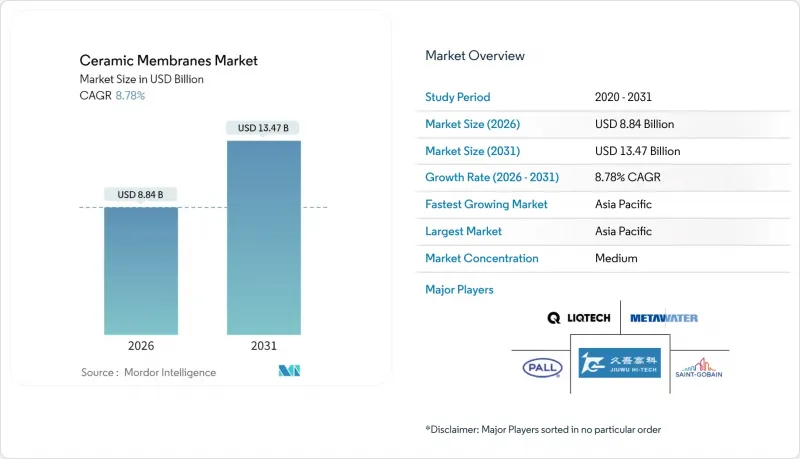

2025年陶瓷膜市值為81.3億美元,預計到2031年將達到134.7億美元,而2026年為88.4億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 8.78%。

這一成長反映了工業水處理、食品加工和聚合物材料性能不足的嚴苛製程分離領域對高效過濾解決方案的快速需求。限制廢水污染物排放的監管要求、不斷上漲的能源價格促使低壓運行,以及亞太地區基礎設施建設支出的成長,都在推動產業結構向長壽命陶瓷裝置轉變。競爭的焦點在於製造流程的計劃,證明了該技術的擴充性,並證實市政營運商已開始將陶瓷系統視為面向未來的資產。

全球陶瓷膜市場趨勢及展望

對水和污水處理基礎設施的需求不斷成長

世界各地的供水事業正在用陶瓷組件替換老舊的過濾設備,這些陶瓷組件即使在嚴苛的清洗條件和原水水質波動的情況下也能保持水流穩定。中國和印度的國家獎勵策略已撥款數十億美元用於先進的水處理和再利用技術,而美國的《基礎設施投資與就業法案》也優先考慮符合美國環保署(EPA)膜過濾指南的污染物去除技術。這些資金的湧入使供水事業更有信心選擇價格較高的陶瓷組件。工程、採購和施工(EPC)承包商擴大預先指定使用碳化矽(SiC)或氧化鋁撬裝組件,以應對預計從2027年起實施的更嚴格的排放和微量污染物法規。系統整合商也指出,陶瓷元件可以與節省空間的薄膜生物反應器(MBR)無縫整合,從而釋放土地資源有限的城市水廠的占地面積。

全球更嚴格的工業污水法規

根據美國環保署 (EPA) 40 CFR 法規和歐盟工業排放指令,工業業者面臨日益嚴厲的處罰。這兩項法規均將高選擇性薄膜指定為處理難處理污水的最佳可行可用技術(BAT)。製藥廠必須在排放前去除溶劑殘留物和內分泌干擾物,而石化廠則面臨含油生產廢水快速堵塞聚合物纖維的挑戰。陶瓷裝置在反覆接觸腐蝕性或氧化性清潔劑後仍能保持結構完整,從而減少了可能危及許可證合規性的非計劃性停機時間。監管的確定性已將採購決策從可自由選擇的升級轉變為納入定期工廠檢修的風險緩解措施。由於更換期限明確,供應商可以擁有可預測的需求管道,並據此規劃工廠使用率。

高昂的資本和營運成本

與同等容量的聚合物系統相比,陶瓷設備的成本可能是其兩到三倍,這使得資金籌措有限的地區難以實施。小規模市政當局通常依賴最低競標補貼機制,而這種機制並未考慮全生命週期成本。對於投資回收期嚴格限制在三年以內的工業企業而言,儘管陶瓷設備具有潛在的節能效果,但由於財務部門低估了避免停機帶來的收益,他們可能會擱置陶瓷設備的安裝計劃。此外,由於需要儲備備件(例如專用高壓墊片和金屬外殼),營運成本也會增加。然而,隨著製程自動化和全球生產規模的擴大,陶瓷設備的價格將持續下降,預計從2027年起,這些限制將得到緩解。

細分市場分析

到2025年,氧化鋁基膜將佔據陶瓷膜市場44.12%的佔有率,這得益於成熟的窯爐生產計劃、豐富的原料以及在市政和食品應用微過濾的成功案例。供應商利用現有的隧道窯和擠出機來維持有利的成本結構,即使在能源價格上漲時期也是如此。這種規模優勢促進了價格競爭,並推動陶瓷膜市場持續向對成本敏感的細分市場擴張。氧化鋁的中性表面化學性質使其能夠採用後處理塗層來調節選擇性,而無需改變基材結構。同時,儘管二氧化鈦薄膜的市場規模較小,但其複合年成長率卻高達9.80%,成為成長最快的薄膜。二氧化鈦膜的光催化和高通量特性使其非常適合去除新興目標物質,例如藥物和內分泌干擾物。

二氧化鈦細分市場受益於研發進展,透過摻雜配方降低了煅燒溫度,從而減少了生產過程中的能源投入和碳排放強度。碳化矽目前應用尚不廣泛,但在油氣生產水處理領域的需求量卻高達兩位數,因為該領域pH值波動和磨蝕性固態會損壞其他材料。氧化鋯和二氧化矽變體則適用於一些特殊分離應用,例如高溫苛性染料回收和低壓食品澄清。

陶瓷膜市場報告按材料類型(氧化鋁、二氧化矽、二氧化鈦、氧化鋯、碳化矽及其他)、終端用戶產業(水及污水處理、食品飲料、化學、製藥及其他)和地區(亞太、北美、歐洲、南美、中東和非洲)進行細分。市場預測以美元以金額為準。

區域分析

預計到2025年,亞太地區將佔據陶瓷膜市場52.98%的收入佔有率,並在2031年之前保持10.02%的複合年成長率。中國的五年計畫撥款940億美元用於升級改造水資源再利用設施,將推動工業園區對氧化鋁和碳化矽管材的批量採購。印度特倫甘納邦和古吉拉突邦的製藥產業叢集正在向陶瓷超過濾轉型,以滿足日益嚴格的零排放法規。同時,一個日本財團正在政府支持的先進材料計畫下,致力於改善低缺陷碳化矽支撐體。

北美仍然是領先的部署區域,這主要得益於美國環保署 (EPA) 的嚴格執法以及成熟的油氣生產水處理市場。德克薩斯州的頁岩油氣作業正在試驗使用碳化矽膜進行耐鹽鹽水淨化,據報道,該技術提高了處理能力,並減少了卡車運輸量和深井注入量。美國也正在率先採用飲用水水資源再利用,加州的公共產業運作先進的陶瓷基水處理廠,以確保抗旱供水。

歐洲的佔有率既反映了其工業傳統,也反映了其強力的環保政策。德國、法國和荷蘭正在食品級海水淡化廠進行改造,加裝二氧化鈦裝置,與傳統的螺旋纏繞式系統相比,可將苛性鈉用量減少一半。中東和非洲地區對用於逆滲透的陶瓷海水預處理技術越來越感興趣,尤其是在極端溫度會對聚合物濾芯的耐久性構成挑戰的地區。阿拉伯聯合大公國的一條試點生產線已證明,該技術能夠降低化學品消耗並延長清洗週期,為波灣合作理事會成員國從2026年起建設兆瓦級海水淡化廠鋪平了道路。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 對用水和污水處理基礎設施的需求不斷成長

- 全球更嚴格的工業污水法規

- 與聚合物薄膜相比,使用壽命更長,生命週期成本更低。

- 擴大乳製品和飲料行業的蛋白質濃縮工藝

- PVDF膜的相關監管趨勢推動了陶瓷膜的採用。

- 市場限制

- 高昂的資本和營運成本

- 低壓聚合物替代品在低TDS應用中日益普及

- 地方政府供水事業缺乏操作人員專業技能

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依材料類型

- 氧化鋁

- 二氧化矽

- 提泰妮婭

- 氧化鋯

- 碳化矽

- 其他材質(玻璃材質、氧化鎂、碳、玻璃陶瓷複合材料等)

- 按最終用戶行業分類

- 水和污水處理

- 食品/飲料

- 化工

- 製藥

- 其他(生物技術、紡織、石油化工等)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 土耳其

- 俄羅斯

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 卡達

- 阿拉伯聯合大公國

- 奈及利亞

- 埃及

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- ALSYS

- atech innovations GmbH

- Ceraflo Pte Ltd

- GEA Group Aktiengesellschaft

- JIUWU HI-TECH

- Kovalus Separation Solutions

- LiqTech Holding A/S

- Membracon

- METAWATER. CO. LTD

- Nanostone

- Pall Corporation

- Qua Group LLC

- Saint-Gobain

- Sterlitech Corporation

- TAMI Industries

第7章 市場機會與未來展望

The Ceramic Membranes Market was valued at USD 8.13 billion in 2025 and estimated to grow from USD 8.84 billion in 2026 to reach USD 13.47 billion by 2031, at a CAGR of 8.78% during the forecast period (2026-2031).

This expansion reflects rapid uptake of robust filtration solutions in industrial water treatment, food processing, and harsh-process separation where polymeric materials underperform. Regulatory mandates that limit effluent contaminants, rising energy prices that reward low-pressure operation, and expanding infrastructure spending in Asia-Pacific collectively reinforce a secular shift toward long-life ceramic units. Competitive activity centers on manufacturing innovations that trim sintering temperatures, refine pore-size control, and embed photocatalytic surfaces, allowing suppliers to differentiate on total cost of ownership rather than headline capital outlay. Demonstration projects such as Singapore's 65 million-liter-per-day installation highlight technical scalability and underscore how municipal utilities now view ceramic systems as future-proof assets.

Global Ceramic Membranes Market Trends and Insights

Rising Demand for Water and Wastewater Treatment Infrastructure

Utilities worldwide are replacing aging filtration assets with ceramic designs that maintain flux under aggressive cleaning and variable feedwater quality. National stimulus programs in China and India allocate multibillion-dollar budgets to advanced treatment and reuse, while the U.S. Infrastructure Investment and Jobs Act prioritizes contaminant removal technologies aligned with EPA membrane guidance. These capital flows give utilities confidence to select ceramic modules despite higher ticket prices. Engineering-, procurement-, and construction-contractors increasingly pre-specify silicon carbide or alumina skids as a hedge against tightening discharge limits and micro-pollutant rules expected after 2027. Integrators also note that ceramic elements integrate smoothly with low-footprint membrane bioreactors, freeing floor space in land-constrained urban plants.

Stringent Industrial Effluent Regulations Worldwide

Industrial operators face rising penalties under EPA 40 CFR rules and the EU Industrial Emissions Directive, both of which identify high-selectivity membranes as best available technology for difficult waste streams. Pharmaceutical facilities must remove solvent traces and endocrine-disrupting compounds before discharge, while petrochemical sites contend with oil-laden produced water that quickly blinds polymeric fibers. Ceramic units remain structurally intact after repeated exposure to caustic or oxidizing cleaners, cutting unplanned downtime that would otherwise jeopardize permit compliance. Regulatory certainty has therefore shifted purchasing decisions from discretionary upgrades to risk-mitigation essentials that slot into cyclical plant turnarounds. Because replacement deadlines are codified, vendors enjoy a predictable demand pipeline and can plan factory utilization accordingly.

High Capital and Operating Costs

Ceramic equipment can cost two to three times as much as polymeric systems of equivalent capacity, discouraging adoption where funding windows are narrow. Smaller municipalities often rely on grant cycles that favor lowest-bid awards, which seldom account for lifecycle economics. Industrial plants with tight payback criteria under three years may shelve ceramic proposals despite potential energy savings because finance teams undervalue avoided downtime. Operating costs also climb when spare parts inventories must include specialty gaskets and metal housings rated for higher pressures. However, steady price erosion from process automation and increasing global production scale is expected to soften this restraint after 2027.

Other drivers and restraints analyzed in the detailed report include:

- Longer Service-Life and Lower Lifecycle Cost vs. Polymeric Membranes

- Expansion of Dairy and Beverage Protein-Concentration Processes

- Prevalence of Low-Pressure Polymeric Alternatives in Low-TDS Uses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Alumina elements held 44.12% of the ceramic membranes market share in 2025 due to mature kiln schedules, abundant raw materials, and proven performance in microfiltration of municipal and food streams. Suppliers exploit existing tunnel kilns and extruders, driving cost positions that remain favorable even as energy prices climb. Such a scale underpins price competition that keeps the ceramic membranes market expanding into cost-sensitive verticals. Alumina's neutral surface chemistry also supports post-treatment coatings that tailor selectivity without altering base structure. In contrast, titania membranes, while accounting for a smaller revenue base, posted the fastest 9.80% CAGR because their photocatalytic and high-flux attributes align with emerging removal targets such as pharmaceuticals and endocrine disruptors.

The titania sub-segment benefits from research and development breakthroughs that lower firing temperatures through doped formulations, trimming energy input and shrinking carbon intensity of production. Silicon carbide options, though niche today, show double-digit demand from oil-and-gas produced-water treatment where pH swings and abrasive solids destroy other materials. Zirconia and silica variants satisfy specialty separations including hot caustic dye recovery and low-pressure food clarification.

The Ceramic Membranes Report is Segmented by Material Type (Alumina, Silica, Titania, Zirconium Oxide, Silicon Carbide, and Others), End-User Industry (Water and Wastewater Treatment, Food and Beverage, Chemical Industry, Pharmaceutical, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated the ceramic membranes market with 52.98% revenue share in 2025 and is projected to sustain a 10.02% CAGR through 2031. China's Five-Year Plan earmarks USD 94 billion for water-reuse upgrades, unlocking bulk purchases of alumina and silicon carbide tubes for industrial parks. Indian pharmaceutical clusters in Telangana and Gujarat switch to ceramic ultrafiltration to meet tightened zero-liquid-discharge mandates, while Japanese consortia refine low-defect silicon carbide supports under government-backed advanced-materials programs.

North America remains a key adopter owing to EPA enforcement vigor and a mature oil-and-gas produced-water treatment market. Texas shale operations trial silicon carbide membranes for salt-tolerant brine polishing, reporting throughput gains that reduce trucking and deep-well-injection volumes. The United States also hosts early adopters of potable reuse, with California utilities commissioning ceramic-based advanced treatment trains to secure a drought-resilient supply.

Europe's share reflects both industrial heritage and strong environmental policy alignment. Germany, France, and the Netherlands retrofit food-grade plants with titania units that halve caustic usage compared with legacy spiral-wound systems. The Middle East and Africa register growing interest in ceramic seawater pretreatment for reverse-osmosis desalination, especially where temperature extremes challenge polymeric cartridge endurance. Pilot lines in the United Arab Emirates have demonstrated lower chemical consumption and longer cleaning intervals, paving the way for multi-megawatt desal buildouts in the Gulf Cooperation Council states post-2026.

- ALSYS

- atech innovations GmbH

- Ceraflo Pte Ltd

- GEA Group Aktiengesellschaft

- JIUWU HI-TECH

- Kovalus Separation Solutions

- LiqTech Holding A/S

- Membracon

- METAWATER. CO. LTD

- Nanostone

- Pall Corporation

- Qua Group LLC

- Saint-Gobain

- Sterlitech Corporation

- TAMI Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Water and Wastewater Treatment Infrastructure

- 4.2.2 Stringent Industrial Effluent Regulations Worldwide

- 4.2.3 Longer Service-Life and Lower Lifecycle Cost Vs. Polymeric Membranes

- 4.2.4 Expansion of Dairy and Beverage Protein-Concentration Processes

- 4.2.5 Pending PVDF-Based Membrane Restrictions Driving Ceramic Adoption

- 4.3 Market Restraints

- 4.3.1 High Capital and Operating Costs

- 4.3.2 Prevalence of Low-Pressure Polymeric Alternatives in Low-TDS Uses

- 4.3.3 Limited Operator Expertise at Municipal Utilities

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Alumina

- 5.1.2 Silica

- 5.1.3 Titania

- 5.1.4 Zirconium Oxide

- 5.1.5 Silicon Carbide

- 5.1.6 Others (Glassy Materials, Magnesia, carbon, Glass-Ceramic composites, etc.)

- 5.2 By End-user Industry

- 5.2.1 Water and Wastewater Treatment

- 5.2.2 Food and Beverage

- 5.2.3 Chemical Industry

- 5.2.4 Pharmaceutical

- 5.2.5 Others (Biotechnology, Textile, Petrochemical, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ALSYS

- 6.4.2 atech innovations GmbH

- 6.4.3 Ceraflo Pte Ltd

- 6.4.4 GEA Group Aktiengesellschaft

- 6.4.5 JIUWU HI-TECH

- 6.4.6 Kovalus Separation Solutions

- 6.4.7 LiqTech Holding A/S

- 6.4.8 Membracon

- 6.4.9 METAWATER. CO. LTD

- 6.4.10 Nanostone

- 6.4.11 Pall Corporation

- 6.4.12 Qua Group LLC

- 6.4.13 Saint-Gobain

- 6.4.14 Sterlitech Corporation

- 6.4.15 TAMI Industries

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

陶瓷薄膜市場:依產品類型、材料、技術和最終用戶分類-2026-2032年全球市場預測

陶瓷薄膜市場:依產品類型、材料、技術和最終用戶分類-2026-2032年全球市場預測 陶瓷薄膜市場:按材料、應用、技術和地區分類

陶瓷薄膜市場:按材料、應用、技術和地區分類 全球陶瓷膜市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球陶瓷膜市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球陶瓷膜市場報告氧化鋁基陶瓷膜市場按孔徑、材料類型、製造流程、膜結構、應用和終端用戶產業分類,全球預測,2026-2032年陶瓷膜檢測設備市場(按設備類型、檢測技術、膜材料、檢測參數、應用和最終用戶分類)—2026-2032年全球預測飲用水用陶瓷平板膜市場:按膜材料、孔徑、流道結構、組件類型、運行模式、應用和最終用戶分類,全球預測(2026-2032年)

2026年全球陶瓷膜市場報告氧化鋁基陶瓷膜市場按孔徑、材料類型、製造流程、膜結構、應用和終端用戶產業分類,全球預測,2026-2032年陶瓷膜檢測設備市場(按設備類型、檢測技術、膜材料、檢測參數、應用和最終用戶分類)—2026-2032年全球預測飲用水用陶瓷平板膜市場:按膜材料、孔徑、流道結構、組件類型、運行模式、應用和最終用戶分類,全球預測(2026-2032年) 陶瓷膜市場規模、佔有率及成長分析(按材料、應用、技術及地區分類)-2026-2033年產業預測

陶瓷膜市場規模、佔有率及成長分析(按材料、應用、技術及地區分類)-2026-2033年產業預測 陶瓷膜市場規模、佔有率、趨勢分析報告:按技術、應用、地區、細分市場預測,2025-2030 年

陶瓷膜市場規模、佔有率、趨勢分析報告:按技術、應用、地區、細分市場預測,2025-2030 年 2030年陶瓷膜市場預測:按產品類型、材料、應用和地區進行的全球分析

2030年陶瓷膜市場預測:按產品類型、材料、應用和地區進行的全球分析