|

市場調查報告書

商品編碼

1937322

鏈鋸:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Chainsaw - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

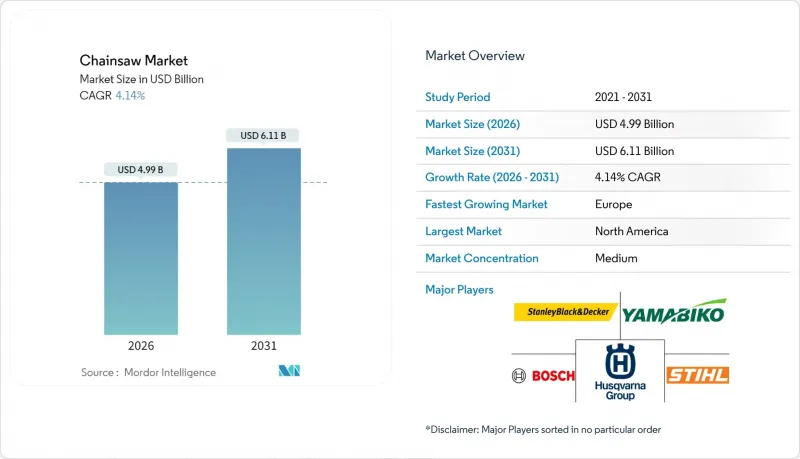

預計電鋸市場將從 2025 年的 47.9 億美元成長到 2026 年的 49.9 億美元,到 2031 年將達到 61.1 億美元,2026 年至 2031 年的複合年成長率為 4.14%。

日益嚴格的環保法規正推動市場轉型為電動鏈鋸。電池性能的提升、人體工學設計的改進以及新增的數位化功能,正在縮小電動鏈鋸與汽油鏈鋸之間的性能差距,使其對專業用戶和家庭用戶都更具吸引力。市場競爭較為溫和,少數幾家大型製造商佔據主導地位,而規模較小的製造商則透過產品差異化和區域專業化專注於特定領域。各公司正在拓展線上銷售管道,使客戶能夠有效地評估產品,從而刺激商業和住宅領域的產品更換。人們對永續性關注以及對低維護設備的需求正在影響購買模式。在都市區綠化活動和DIY潮流的推動下,鏈鋸的應用範圍正從林業擴展到一般的家庭和花園維護領域。

全球鏈鋸市場趨勢與洞察

大型木造建築對城市木材的需求不斷成長

隨著大規模木造建築的興起,木材加工的需求已超越了傳統的伐木方式。工程木製品,例如交錯層壓木材和複合板,需要在可控的生產環境中進行精確切割,並盡可能減少振動。這推動了電動鏈鋸的廣泛應用,因為電動鏈鋸能夠實現精確切割並降低噪音。加值加工商更傾向於選擇可與集塵系統整合且扭力穩定的無線型號。不斷發展的建築方法正在拓展鏈鋸的應用範圍,從原木採伐擴展到建築和工程領域,這使得電池技術和人體工學設計變得尤為重要。這種轉變為城市發展計劃和製造工廠的供應商創造了新的機會。

颱風過後伐木活動增加

頻繁發生的極端天氣事件增加了災區快速移除樹木的需求。當倒下的樹木阻塞道路、損壞基礎設施或位於重型機械無法進入的區域時,鏈鋸對於災後重建至關重要。這些作業需要輕巧、便攜且高功率的鏈鋸,以便應對複雜的地形。日益嚴格的安全法規推動了對配備先進煞車系統和數位警報器的鏈鋸的需求。這種不規則的伐木需求導致設備使用量和更換需求激增。耐用、高性能工具的製造商在災後重建期間的需求量激增,凸顯了鏈鋸在災害應變和森林管理中的重要性。

終端用戶安全責任險成本增加

不斷上漲的保險成本正在影響樹木養護公司和小規模承包商的設備選擇。先進的電池驅動鏈鋸性能優異且環保,但需要更高的初始投資。保險公司對新舊型號鏈鋸的責任險要求相似,限制了技術的普及。電子維修成本導致更高的免賠額,也讓消費者猶豫不決。這些經濟因素正在減緩設備升級和市場成長,尤其是在小規模企業中。保險成本和維修風險的雙重壓力阻礙了技術的普及,迫使製造商開發更具成本效益的設計方案和明確的安全認證。

細分市場分析

汽油動力鏈鋸憑藉其卓越的扭力和在偏遠惡劣環境下的可靠性,繼續保持著61.78%的市場佔有率,穩居市場主導地位。在電池基礎設施有限的農村地區,汽油動力鏈鋸仍然是伐木和重型作業的必備工具。電動鏈鋸市場正在擴張,尤其是在噪音和排放法規嚴格的都市區。受政府法規和室內加工需求的推動,有線電動鏈鋸的年複合成長率(CAGR)穩定成長,達到4.26%。

電池驅動鏈鋸不斷發展,配備了IP防護等級的外殼和離心式離合器,其性能足以媲美汽油動力鏈鋸。鋰電池密度、冷卻系統和韌體的改進提升了耐用性和效率。園林綠化師和樹藝師擴大採用多功能電池平台。太陽能充電站正在偏遠地區興起,以減少對燃料的依賴。氣動和液壓鏈鋸仍然適用於一些特殊應用,例如鋸木廠和高火災風險區域,在這些場所需要無火花操作。

區域分析

預計到2025年,北美將佔全球鏈鋸市場收入的33.62%,主要得益於其廣闊的森林面積、颶風災後重建工作以及日益成長的DIY文化。該地區的需求主要受政府植樹造林計畫和野火預防措施的推動,尤其是對工業汽油鏈鋸的需求。隨著公共產業擴大將植被管理外包,對配備防震技術的耐用型鏈鋸的需求也不斷成長。郊區樹木護理公司正在逐步過渡到電池驅動型鏈鋸,以符合噪音法規。製造商正在建立本地電池組組裝廠,以最大限度地降低運輸風險並縮短交貨時間。由於專業人士和消費者的雙重需求,市場持續成長,而監管要求和技術創新也在影響消費者的購買決策。電動鏈鋸正日益普及,尤其是在需要安靜運作的都市區和住宅。

預計到2031年,歐洲將以4.18%的複合年成長率實現最高成長,這主要得益於環境法規和大規模木結構建築的興起。該地區對工程木製品的重視推動了電池驅動鏈鋸的普及,這類鏈鋸噪音低、扭矩大,滿足了製造商在室內生產環境中對精密切割工具的需求。市政噪音和排放氣體法規促使專業用戶和住宅用戶選擇既符合法規要求又能保持性能的無線型號。該地區的製造工廠正在擴大產能,企業也正在投資電池技術研發。歐洲鏈鋸市場體現了該地區對永續性、安全性和營運效率的重視。都市區擴張和永續建築方法的推廣將繼續推動對靜音、零排放工具的需求。

在亞太地區,印度、印尼和越南的都市化加快以及基礎設施建設計劃的推進,為市場帶來了成長機會。當地製造商正充分利用其成本效益高的生產能力,而國際公司則在拓展其區域供應鏈。颱風災區的自然災害應變工作推動了對輕型攜帶式鏈鋸的需求。在非洲,鏈鋸的使用與農林業和土地開發密切相關,並受到農業耕作方式和資源取得的影響。儘管森林覆蓋率有限,但中東市場主要集中在都市區景觀美化和公共設施維護。南美洲的需求穩定且多樣化,主要來自農田清理和選擇性伐木作業。在這些地區,成本效益、產品耐用性和易於維護是優先考慮的因素,隨著基礎設施的完善,電池驅動工具的普及率也逐漸提高。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 都市區對木材的需求不斷成長,以滿足大型木造建築的需求。

- 颱風過後伐木活動增加

- DIY風格與電子商務工具包的興起

- 政府對低排放量電池裝置的獎勵措施

- 豪華戶外家具製造業的蓬勃發展

- 土地開墾擴大耕地面積

- 市場限制

- 終端用戶安全責任險成本增加

- 城市邊緣地區的噪音防治條例

- 加強對無毀林供應鏈的監管

- 熟練操作人員短缺

- 監管環境

- 技術展望

- 波特五力分析

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依產品類型

- 氣體類型

- 電動驅動

- 電池供電

- 氣動/液壓

- 最終用戶

- 住宅

- 產業

- 透過分銷管道

- 線下零售

- 線上平台

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- STIHL Group

- Robert Bosch GmbH

- Husqvarna Group

- Stanley Black & Decker Inc.

- Yamabiko Corporation

- Makita Corporation

- The Toro Company

- SUMEC Group Corporation(SIMOMACH)

- STIGA SpA(GGP Group)

- Einhell Germany AG

- Emak SPA

- Koki Holdings Co., Ltd.(Kohlberg Kravis Roberts)

- Honda Motor Co., Ltd.

- AL-KO GMBH

- Taizhou Bison Machinery Co., Ltd.

第7章 市場機會與未來展望

The chainsaw market is expected to grow from USD 4.79 billion in 2025 to USD 4.99 billion in 2026 and is forecast to reach USD 6.11 billion by 2031 at 4.14% CAGR over 2026-2031.

The market is experiencing a transition toward electric chainsaws due to stricter environmental regulations. Enhanced battery performance, improved ergonomics, and digital features are reducing the performance gap between electric and gas-powered models, increasing their appeal to professional users and homeowners. The market exhibits moderate competition, with several major manufacturers controlling a substantial market share, while smaller companies focus on specialized segments through product differentiation and regional approaches. Companies are expanding their online sales channels, enabling customers to evaluate products effectively, which drives replacement rates in both commercial and residential sectors. The increasing focus on sustainability and demand for low-maintenance equipment is shaping buying patterns. The expansion of urban landscaping activities and DIY trends has broadened chainsaw applications beyond forestry to include general home and garden maintenance.

Global Chainsaw Market Trends and Insights

Increasing Urban-wood Demand for Mass-timber Construction

The growth of mass-timber construction has expanded wood-processing requirements beyond traditional logging. Engineered wood products, including cross-laminated and glued-laminated timber, require precise cutting with minimal vibration in controlled fabrication environments. This has increased the adoption of electric chainsaws, which provide precise cuts and quiet operation. Value-added processors prefer cordless models that integrate with dust extraction systems and deliver consistent torque. The evolution of construction methods has expanded chainsaw applications from raw log harvesting to architectural and engineering uses, where battery technology and ergonomic design are crucial. This transformation creates opportunities for suppliers in urban development projects and fabrication facilities.

Growing Post-storm Salvage Logging Activities

The increasing frequency of extreme weather events has heightened the need for rapid timber removal in storm-affected areas. Chainsaws are essential for salvage operations when fallen trees block roads, damage infrastructure, or lie in areas inaccessible to heavy equipment. These operations require lightweight, portable, and powerful models for difficult terrain. Enhanced safety regulations have increased demand for chainsaws with advanced braking systems and digital alerts. These irregular salvage requirements create unexpected spikes in equipment usage and replacement needs. Manufacturers of durable, high-performance tools experience increased demand during recovery periods, highlighting chainsaws' importance in disaster response and forest management.

Heightened End-user Safety Liability Insurance Costs

Increasing insurance costs affect tree-service firms and small contractors' equipment decisions. Advanced battery-powered chainsaws offer improved performance and environmental benefits but require a higher initial investment. Insurance providers maintain similar liability requirements for both traditional and modern models, limiting technology adoption. Electronic component repair costs lead to higher deductibles, causing buyer hesitation. These financial factors slow fleet updates and market growth, particularly among smaller operations. The combination of insurance premiums and repair risks creates adoption barriers, requiring manufacturers to develop cost-effective designs and clear safety certifications.

Other drivers and restraints analyzed in the detailed report include:

- Rising DIY Culture and E-commerce Tool Bundles

- Government Incentives for Low-emission Battery Equipment

- Skilled-operator Labor Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Gas-powered chainsaws dominate the chainsaw market size with a 61.78% share due to their superior torque and reliability in remote and demanding environments. These models remain essential for rural logging and heavy-duty applications where battery infrastructure is limited. The electric segment is expanding, particularly in urban areas with strict noise and emission regulations. Corded electric chainsaws show steady growth at 4.26% CAGR, supported by municipal regulations and indoor fabrication requirements.

Battery-powered chainsaws continue to advance, featuring IP-rated housings and centrifugal clutches that provide gas-like performance. Improvements in lithium battery density, cooling systems, and firmware enhance durability and efficiency. The market sees increased adoption of multi-tool battery platforms among landscapers and arborists. Solar-compatible charging stations are emerging in remote locations to reduce fuel dependency. Pneumatic and hydraulic chainsaws maintain a specialized presence in mills and fire-prone areas requiring spark-free operation.

The Chainsaw Market Report is Segmented by Product Type (Gas-Powered, Electric-Powered, and More), by End-User (Residential and Industrial), by Distribution Channel (Offline Retail and Online Platforms), and by Geography (North America, Europe, Asia-Pacific, South America, The Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounts for 33.62% of the chainsaw market revenue in 2025, supported by extensive forest coverage, hurricane recovery operations, and widespread DIY practices. The region's demand is driven by government reforestation programs and wildfire prevention efforts, particularly for industrial-grade gas-powered chainsaws. The increasing trend of utilities outsourcing vegetation management has heightened demand for durable chainsaws with anti-vibration technology. Tree-care companies in suburban areas are transitioning to battery-powered units to meet noise regulations. Manufacturers have established local battery pack assembly facilities to minimize shipping risks and reduce delivery times. The market continues to grow through a combination of professional and consumer use, with regulatory requirements and innovation influencing purchase decisions. The adoption of electric models is increasing, particularly in urban and residential areas where quiet operation is essential.

Europe exhibits the highest growth rate at 4.18% CAGR through 2031, driven by environmental regulations and mass-timber construction advancement. The region's focus on engineered wood products necessitates precise cutting tools suitable for indoor manufacturing environments. This has increased the uptake of battery-powered chainsaws that offer low noise levels and high torque. Municipal noise restrictions and emissions regulations are directing both professional and residential users toward cordless models that maintain performance while meeting compliance requirements. Regional manufacturing facilities are increasing production capacity, while companies invest in battery technology development. The European chainsaw market reflects the region's focus on sustainability, safety, and operational efficiency. The expansion of urban areas and sustainable construction methods continues to increase demand for quiet, zero-emission tools.

Asia-Pacific demonstrates growth opportunities as urbanization and infrastructure projects increase in India, Indonesia, and Vietnam. Local manufacturers leverage cost-efficient production capabilities, while international companies expand regional supply chains. Natural disaster response in typhoon-affected areas increases demand for lightweight, portable chainsaws. In Africa, chainsaw use correlates with agroforestry and land development, influenced by agricultural practices and resource access. The Middle East market focuses on landscaping and municipal maintenance in urban areas despite limited forest coverage. South America maintains consistent but varied demand, primarily from agricultural clearing and selective logging operations. These regions prioritize cost-effectiveness, product durability, and maintenance simplicity, with gradual increases in battery-powered tool adoption as infrastructure develops.

- STIHL Group

- Robert Bosch GmbH

- Husqvarna Group

- Stanley Black & Decker Inc.

- Yamabiko Corporation

- Makita Corporation

- The Toro Company

- SUMEC Group Corporation (SIMOMACH)

- STIGA SpA (GGP Group)

- Einhell Germany AG

- Emak SPA

- Koki Holdings Co., Ltd. (Kohlberg Kravis Roberts)

- Honda Motor Co., Ltd.

- AL-KO GMBH

- Taizhou Bison Machinery Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Urban-wood Demand for Mass-timber Construction

- 4.2.2 Growing Post-storm Salvage Logging Activities

- 4.2.3 Rising DIY Culture and E-commerce Tool Bundles

- 4.2.4 Government Incentives for Low-emission Battery Equipment

- 4.2.5 Surge in Premium Outdoor Furniture Manufacturing

- 4.2.6 Land Clearing for Crop Expansion

- 4.3 Market Restraints

- 4.3.1 Heightened End-user Safety Liability Insurance Costs

- 4.3.2 Noise-abatement Bylaws in Peri-urban Zones

- 4.3.3 Tightening Deforestation-free Supply-chain Regulations

- 4.3.4 Skilled-operator Labor Shortages

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Gas-powered

- 5.1.2 Electric-powered

- 5.1.3 Battery-powered

- 5.1.4 Pneumatic/ Hydraulic

- 5.2 By End-user

- 5.2.1 Residential

- 5.2.2 Industrial

- 5.3 By Distribution Channel

- 5.3.1 Offline Retail

- 5.3.2 Online Platforms

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Russia

- 5.4.2.6 Spain

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 STIHL Group

- 6.4.2 Robert Bosch GmbH

- 6.4.3 Husqvarna Group

- 6.4.4 Stanley Black & Decker Inc.

- 6.4.5 Yamabiko Corporation

- 6.4.6 Makita Corporation

- 6.4.7 The Toro Company

- 6.4.8 SUMEC Group Corporation (SIMOMACH)

- 6.4.9 STIGA SpA (GGP Group)

- 6.4.10 Einhell Germany AG

- 6.4.11 Emak SPA

- 6.4.12 Koki Holdings Co., Ltd. (Kohlberg Kravis Roberts)

- 6.4.13 Honda Motor Co., Ltd.

- 6.4.14 AL-KO GMBH

- 6.4.15 Taizhou Bison Machinery Co., Ltd.