|

市場調查報告書

商品編碼

1937316

汽車鋁擠型:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Automotive Aluminium Extrusion - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

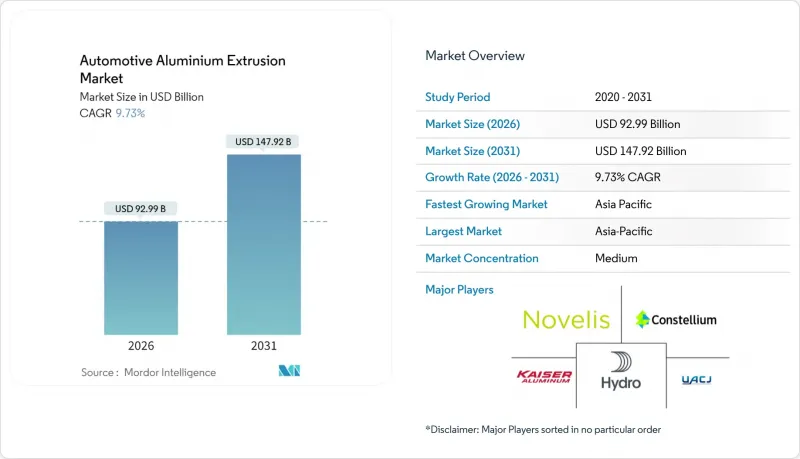

2025年汽車鋁擠型市場價值為847.5億美元,預計到2031年將達到1,479.2億美元,而2026年為929.9億美元。

預測期(2026-2031 年)的複合年成長率預計為 9.73%。

電動車平台加速轉型是推動市場需求成長的主要動力,擠壓鋁材可用於製造輕量化白色車身結構、碰撞吸能導軌以及高效能電池的隔熱外殼。合金化學和沖壓技術的不斷進步,使得製造複雜的中空型材成為可能,從而在不影響結構完整性的前提下減輕車輛重量。受美墨加協定(USMCA)和歐盟碳邊境調節機制(CBAM)的推動,區域近岸外包正在重塑供應鏈,使其與國內沖壓能力相匹配,預計僅在北美地區就將帶來可觀的資本投資。隨著一體化鋁生產商提高上游冶煉和下游擠壓生產線的產能,以確保鋁坯供應並實現閉合迴路回收,市場競爭日益激烈。同時,專業的Tier 1級製造商正透過複合材料連接技術和精密模具設計來提升自身競爭力。

全球汽車鋁擠型市場趨勢與洞察

美國、歐盟和中國的汽車二氧化碳排放法規和燃油效率標準

美國企業平均燃油經濟性標準(CAFE)要求美國車輛到2026年平均燃油經濟性達到40.4英里/加侖(約17.3公里/公升),而歐盟標準則規定到2025年二氧化碳排放不得超過95克/公里,並力爭2035年實現近零排放。中國的雙軌制同樣鼓勵輕量化材料,並對不達標者進行處罰。擠壓鋁材能夠幫助汽車製造商減輕電池重量,避免高達數千美元的罰款,使其成為一種經濟高效的優質材料。可預測的監管時間表增強了供應商對投資新模具和產能的信心。擠壓成型具有可回收性、成熟的碰撞性能數據和可擴展的生產能力,使其優於鎂合金和碳纖維等其他輕量化材料。

電池溫度控管機殼需要複雜的中空擠壓成型製程。

隨著電池化學成分的溫度範圍日益收窄,多腔擠壓成型製程將結構連接件和液冷路徑整合到單一部件中,從而減少了接頭和洩漏點。未來的固態電池將更加集中熱量,對冷卻的需求也隨之增加,而鈑金無法滿足這項需求。整合式歧管可降低壓力降和重量,表面處理則可提高其在乙二醇環境中的耐腐蝕性。跨車型標準化的電池組設計使擠壓成型製造商能夠實現規模經濟,並最佳化合金成分以獲得更優異的導熱性能。連續焊接的中空型材簡化了組裝,從而實現了電動車的大量生產。

大型電動車型材生產線缺口超過3500萬條。

儘管3500萬噸以上的壓平機僅佔汽車行業設備容量的不到五分之一,但它們提供的長尺寸沖壓能力對於生產電動車滑板車架和電池機殼至關重要。一條高噸位生產線造價可能在5000萬美元到1億美元之間,從下單到運作需要長達三年時間,這會延誤供應。此外,由於設計複雜,可用的模具製造商數量也受到限制。區域差異依然存在。雖然亞洲在產能方面領先,但北美和歐洲的電動車產量遠超過當地產能,迫使企業進口昂貴的大型零件。因此,汽車製造商正在與大型壓平機機營運商簽訂多年產能預訂協議,改變了傳統的現貨採購模式。

細分市場分析

受電動車電池組廣泛應用的推動,電池機殼和溫度控管模組將呈現最高的成長率,到2031年複合年成長率將達到9.79%。車身結構零件將保持最大佔有率,到2025年將佔汽車鋁擠型市場規模的37.21%,這得益於鋁材優異的碰撞安全性。汽車鋁擠型市場受益於巨型鑄造技術,該技術需要在鑄造的大型零件周圍使用擠壓加強筋。碰撞管理系統中可控制的變形特性有助於降低維修成本。由於其耐腐蝕性和可實現的高品質表面處理,外部飾件將保持穩定的市場佔有率。由於輕量化需求,座椅框架等內裝模組在高階市場的需求不斷成長。

零件配置正朝著多功能設計方向發展,將冷卻、佈線和結構負載路徑整合到單一型材中。供應商利用有限元素分析來最佳化壁厚,並在無需機械加工的情況下整合凸台。邊角料的閉合迴路回收符合原始設備製造商 (OEM) 的再生材料含量標準,進一步加強了買家與擠壓合作夥伴之間的聯繫。增材摩擦攪拌焊接技術無需熱影響區即可連接長擠壓件,從而形成連續的側梁組件,取代多個沖壓件。隨著電動車的普及,電池專用組件將從利基市場走向主流市場,重塑全球沖壓廠的訂單結構。

預計到2025年,乘用車產量將佔總產量的51.84%,年複合成長率(CAGR)為9.80%。這將是所有車型中佔比最高的,因為消費者對電動車的接受速度超過了重型車輛基礎設施的建設速度。輕型商用車將效仿電商物流車輛,實現城市道路的電氣化。中型和重型卡車由於電池能量密度的限制而發展滯後,但隨著兆瓦級充電技術的成熟,它們仍有成長空間。用於公車的鋁擠型材提高了耐腐蝕性,有助於降低公共運輸的生命週期成本。

與內燃機車相比,搭乘用電動車專案每輛車使用的擠壓件數量更多,即使銷量持平,也能帶來更高的單車收入。 OEM平台在轎車、跨界車和掀背車衍生上採用通用擠壓副車架,從而實現規模經濟。隨著商用車有效負載容量的重要性日益凸顯,擠壓地板樑和車頂拱架取代了沖壓鋼材,以減輕電池重量。隨著法規日益嚴格,乘用車鋁材用量將持續成為供應商生產力計畫的重要指標。

區域分析

亞太地區將持續維持領先地位,到2025年將佔全球需求的39.55%,複合年成長率達9.83%。光是中國一國在2024年提煉了大量原生鋁,為下游擠壓叢集提供具有成本競爭力的鋁坯。國內電動車銷量超過800萬輛,確保了國內需求。日本在高階合金研發方面貢獻力量,而韓國則憑藉其汽車組裝的專業技術。從礬土開採到最終壓鑄鋼軌的一體化生產模式縮短了前置作業時間,並降低了成本波動。

北美地區的成長得益於對擠壓機設備和回收能力的計畫投資。諾貝麗斯位於貝米內特的工廠新增60萬噸產能,並與廢料重熔環節全面整合,實現循環供應鏈。海德魯公司位於賓夕法尼亞州的工廠擴建進一步鞏固了在該地區的地位。美墨加協定(USMCA)的原產地規則以及對中國擠壓件徵收的反傾銷稅有助於維持其國內市場佔有率。加拿大豐富的水力發電資源減少了鋼坯的碳足跡,從而支持了原始設備製造商(OEM)的永續性承諾。

歐洲高昂的能源價格和碳邊境調節機制(CBAM)的引入,在推動低碳舉措的同時,也為傳統冶煉廠帶來了壓力。挪威廣泛採用水力發電錠和廢鋼原料,將有助於緩解成本壓力。德國和瑞典的高階OEM廠商正在指定使用先進的中空型材進行Gigacast增強,這使得供應商能夠獲得更高的利潤。回收的強制性要求需要可追溯的廢鋼流通,從而推動了數據密集型價值鏈的發展,使數位化擠壓製造商數位化受益。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 美國、歐盟和中國的車隊二氧化碳排放和燃油經濟性標準

- 電池溫度控管機殼需要複雜的中空擠壓件

- 一級擠出產能的近岸外包(美墨加協定、歐盟-CBAM)

- 電動車滲透率的提高將加速輕量化白車身的採用。

- 閉合迴路擠出生產線可節省成本並帶來廢料回收效益

- 用於高階電動車的超高速鑄造和擠壓成型混合底盤結構

- 市場限制

- 大型電動車型材壓機缺口超過3,500條

- LME鋁價波動與供應鏈投機

- 工程塑膠和碳纖維增強複合材料替代材料(用於內裝應用)

- 歐盟碳稅和區域碳排放稅的轉嫁風險

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模及成長預測(金額)

- 依組件類型

- 身體結構

- 碰撞管理系統

- 電池機殼和散熱模組

- 外部裝飾條和車頂行李架

- 內部模組

- 其他部件

- 按車輛類型

- 搭乘用車

- 輕型商用車

- 中型和大型卡車

- 巴士和長途汽車

- 按合金系列

- 可進行 6xxx 熱處理

- 7xxx 高強度

- 5xxx 不可熱處理

- 鈧和新型合金

- 印刷能力

- 15分鐘或更短

- 16~25 MN

- 26-35 MN

- 35分鐘或以上

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 俄羅斯

- 其他歐洲

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Constellium SE

- Novelis Inc.

- Norsk Hydro ASA

- Kaiser Aluminum Corp.

- UACJ Corp.

- Arconic Corp.

- Kobe Steel Ltd.

- Benteler International

- Bonnell Aluminum

- Hindalco Industries Ltd.

- Guangdong Hongtu

- ETEM Automotive

- Talco Aluminium Company

- Granges AB

- Press-Metal Aluminium

- Sapa Extrusions

- Exlabesa

- Walter Klein GmbH

- Omnimax International

- Innoval Technology

第7章 市場機會與未來展望

The Automotive Aluminium Extrusion Market was valued at USD 84.75 billion in 2025 and estimated to grow from USD 92.99 billion in 2026 to reach USD 147.92 billion by 2031, at a CAGR of 9.73% during the forecast period (2026-2031).

Demand momentum stems from the accelerated shift to electric vehicle (EV) platforms, where extruded aluminum supports lightweight body-in-white structures, crash-energy absorption rails, and high-efficiency battery thermal enclosures. Continual improvements in alloy chemistry and press technology unlock complex hollow profiles that shave curb weight without sacrificing structural integrity. Regional near-shoring, prompted by USMCA rules and the EU Carbon Border Adjustment Mechanism (CBAM), is realigning supply chains toward domestic press capacity, and capital expenditure commitments exceed a huge amount in North America alone. Competitive intensity rises as integrated aluminum producers fortify upstream smelting with downstream extrusion lines to guarantee billet availability and closed-loop recycling. At the same time, specialized Tier-1 houses differentiate through multi-material joining and precision die design.

Global Automotive Aluminium Extrusion Market Trends and Insights

Fleet CO2 & Fuel-Economy Mandates in the U.S., EU, China

Corporate Average Fuel Economy rules require 40.4 mpg U.S. fleet averages by 2026, while EU standards fix 95 g CO2/km for 2025 and move toward near-zero emissions by 2035 . China's dual-credit system likewise rewards lightweight materials and penalizes non-compliance. Extruded aluminum enables automakers to offset battery weight and avoid multi-thousand-dollar fines, making the material premium cost-effective. Predictable regulation timetables give suppliers confidence to fund new tooling and capacity. Proven recyclability, mature crash performance data, and scalable production tip the balance of extrusion over competing lightweighting options such as magnesium or carbon fiber.

Battery Thermal-Management Enclosures Require Complex Hollow Extrusions

As battery chemistries tolerate narrower temperature windows, multi-chamber extrusions combine structural mounting with liquid-coolant paths in a single part, cutting joints and leak points. Future solid-state batteries concentrate heat, intensifying cooling needs that sheet metal cannot meet. Integrated manifolds lower pressure drop and weight, while surface treatments boost corrosion resistance in glycol environments. Standardized pack designs across vehicle lines allow extrusion houses to realize economies of scale and refine alloy recipes for superior thermal conductivity. Continuous-weld hollow profiles also simplify assembly, enabling high-volume EV production.

Scarcity of More Than 35 MN Press Lines for Large EV Profiles

Presses above 35 MN account for less than one-fifth of installed automotive capacity, yet EV skateboard frames and battery enclosures require the extended lineal lengths these machines provide. A single high-tonnage line costs USD 50-100 million and needs up to three years from order to commissioning, slowing supply response. The design complexity further limits the number of qualified toolmakers. Regional imbalances persist: Asia leads installed base, while North American and European EV output surges past local capability, forcing expensive oversize component imports. Consequently, OEMs sign multi-year capacity reservations with large-press operators, altering traditional spot-buy sourcing models.

Other drivers and restraints analyzed in the detailed report include:

- Near-Shoring of Tier-1 Extrusion Capacity (USMCA, EU-CBAM)

- Rising EV Penetration Accelerates Lightweight Body-In-White Adoption

- LME Aluminum Price Volatility & Supply-Chain Speculation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Battery enclosures and thermal modules deliver the fastest 9.79% CAGR through 2031 as EV packs proliferate. Body structure elements still generated the largest 37.21% slice of the automotive aluminum extrusion market size in 2025, underscoring aluminum's crash-worthiness. The automotive aluminum extrusion market benefits from gigacasting, which necessitates extruded reinforcement rails around cast mega-components. Controlled deformation characteristics in crash-management systems lower repair costs. Exterior trim maintains a steady share thanks to corrosion resistance and premium finish opportunities. Interior modules like seat frames gain traction in luxury segments that chase every kilogram of savings.

The component mix evolves with multi-functional designs integrating cooling, routing, and structural load paths in a single profile. Suppliers leverage finite-element modeling to optimize wall thickness and incorporate bosses without machining. Closed-loop recycling of off-cuts meets OEM recycled-content quotas, further tying buyers to extrusion partners. Additive friction stir welding joins long extrusions without heat-affected zones, enabling contiguous side-sill assemblies that replace multiple stampings. As EV adoption accelerates, battery-specific components will rise from niche to mainstream, reshaping order books across global presses.

Passenger cars accounted for 51.84% of 2025 volumes and are forecast to grow at a 9.80% CAGR-the highest among vehicle classes-because consumer EV uptake outpaces infrastructure build-out for heavier segments. Light commercial vans follow as e-commerce logistics fleets electrify inner-city routes. Medium and heavy trucks lag due to battery-energy density limits, but present upside once megawatt charging matures. Aluminum extrusions in buses improve corrosion resistance, lowering lifetime operating costs for public transit agencies.

Passenger EV programs feature higher extrusion kilograms per vehicle than combustion variants, driving per-unit revenue growth even in flat volume scenarios. OEM platforms share common extruded sub-frames across sedan, crossover, and hatchback derivatives, boosting economies of scale. Commercial vehicles emphasize payload, so extruded floor beams and roof bows substitute press-formed steel, offsetting battery mass. As regulatory milestones tighten, passenger car aluminum intensity remains the bellwether for supplier capacity planning.

The Automotive Aluminum Extrusion Market Report is Segmented by Component Type (Body Structure, Crash-Management Systems, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Alloy Series (6xxx Heat-Treatable and More), Press Capacity (Less Than or Equal To15 MN, 16-25 MN, 26-35 MN, and More Than 35 MN), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific controlled 39.55% of 2025 demand, and its 9.83% CAGR keeps the region in pole position. China alone smelted over a high amount of primary aluminum in 2024, furnishing cost-competitive billet to downstream extrusion clusters. Domestic EV sales exceed 8 million units, guaranteeing local offtake. Japan contributes high-end alloy R&D, while South Korea leverages automotive assembly expertise. Integrating bauxite mines to final crash rails compresses lead times and dampens cost volatility.

North America's growth is supported by announced investments in extrusion presses and recycling capacity. Novelis's Bay Minette mill adds 600,000 tonnes of capacity, fully integrated with scrap re-melt for closed-loop supply. Hydro's Pennsylvania upgrade further embeds regional capability. USMCA rules of origin and antidumping duties on Chinese extrusions fortify the domestic share. Abundant hydropower in Canada cuts billet carbon footprint, supporting OEM sustainability pledges .

Europe's high energy prices and CBAM implementation squeeze legacy smelters but stimulate low-carbon initiatives. Norwegian hydro-powered ingot and broader adoption of scrap feedstock mitigate cost headwinds. Premium-segment OEMs in Germany and Sweden specify advanced hollow profiles for gigacast reinforcement, enabling suppliers to command value-added margins. Recycling mandates demand traceable scrap loops, promoting data-rich supply chains that reward digitalized extruders.

- Constellium SE

- Novelis Inc.

- Norsk Hydro ASA

- Kaiser Aluminum Corp.

- UACJ Corp.

- Arconic Corp.

- Kobe Steel Ltd.

- Benteler International

- Bonnell Aluminum

- Hindalco Industries Ltd.

- Guangdong Hongtu

- ETEM Automotive

- Talco Aluminium Company

- Granges AB

- Press-Metal Aluminium

- Sapa Extrusions

- Exlabesa

- Walter Klein GmbH

- Omnimax International

- Innoval Technology

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Fleet Co2 & Fuel-Economy Mandates In US, EU, China

- 4.2.2 Battery Thermal-Management Enclosures Require Complex Hollow Extrusions

- 4.2.3 Near-Shoring Of Tier-1 Extrusion Capacity (USMCA, EU-CBAM)

- 4.2.4 Rising EV Penetration Accelerates Lightweight Body-In-White Adoption

- 4.2.5 Cost-Out & Scrap-Recycling Gains From Closed-Loop Extrusion Lines

- 4.2.6 Gigacasting-Extrusion Hybrid Chassis Architectures In Premium EVs

- 4.3 Market Restraints

- 4.3.1 Scarcity Of More Than 35 Mn Press Lines For Large EV Profiles

- 4.3.2 LME Aluminum Price Volatility & Supply-Chain Speculation

- 4.3.3 Engineering Plastics & CFRP Alternatives For Interiors

- 4.3.4 EU-CBAM & Regional Carbon-Tax Pass-Through Risk

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Component Type

- 5.1.1 Body Structure

- 5.1.2 Crash-Management Systems

- 5.1.3 Battery Enclosures and Thermal Modules

- 5.1.4 Exterior Trim and Roof Rails

- 5.1.5 Interior Modules

- 5.1.6 Other Components

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Medium and Heavy-Duty Trucks

- 5.2.4 Buses and Coaches

- 5.3 By Alloy Series

- 5.3.1 6xxx Heat-Treatable

- 5.3.2 7xxx High-Strength

- 5.3.3 5xxx Non-Heat-Treatable

- 5.3.4 Scandium & Novel Alloys

- 5.4 By Press Capacity

- 5.4.1 Less than or equal to 15 MN

- 5.4.2 16-25 MN

- 5.4.3 26-35 MN

- 5.4.4 More than 35 MN

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle-East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle-East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Constellium SE

- 6.4.2 Novelis Inc.

- 6.4.3 Norsk Hydro ASA

- 6.4.4 Kaiser Aluminum Corp.

- 6.4.5 UACJ Corp.

- 6.4.6 Arconic Corp.

- 6.4.7 Kobe Steel Ltd.

- 6.4.8 Benteler International

- 6.4.9 Bonnell Aluminum

- 6.4.10 Hindalco Industries Ltd.

- 6.4.11 Guangdong Hongtu

- 6.4.12 ETEM Automotive

- 6.4.13 Talco Aluminium Company

- 6.4.14 Granges AB

- 6.4.15 Press-Metal Aluminium

- 6.4.16 Sapa Extrusions

- 6.4.17 Exlabesa

- 6.4.18 Walter Klein GmbH

- 6.4.19 Omnimax International

- 6.4.20 Innoval Technology

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment