|

市場調查報告書

商品編碼

1937315

非洲廢棄物管理:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Africa Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

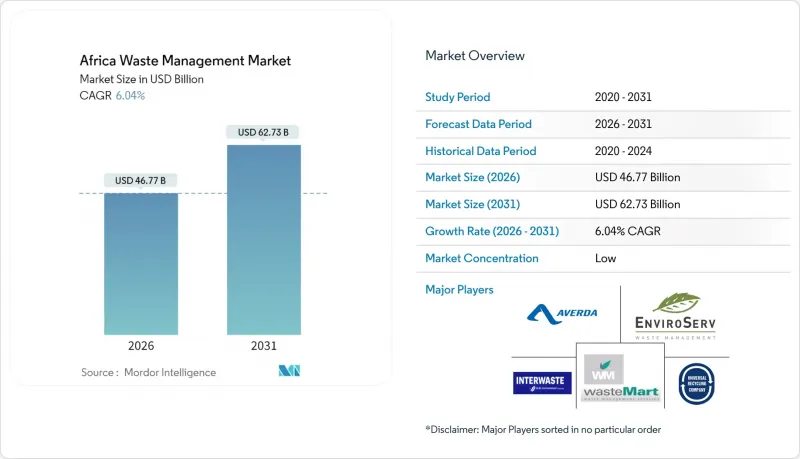

預計到 2026 年,非洲廢棄物管理市場價值將達到 467.7 億美元,高於 2025 年的 441.1 億美元,預計到 2031 年將達到 627.3 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 6.04%。

快速的都市化正以前所未有的速度向本已不堪重負的市政系統注入垃圾,從而推動了對私營部門垃圾收集、處理和回收解決方案的需求。隨著各國政府逐步推行生產者延伸責任制(EPR),投資人對垃圾處理的興趣日益濃厚,而科技公司則引進人工智慧驅動的路線最佳化技術以提高收集效率。儘管垃圾焚化發電(WtE)營運商已獲得氣候融資支持,但其他大型處理設施仍面臨資金缺口。市場競爭仍然分散,但不斷上漲的合規成本有利於那些能夠將非正規垃圾收集者納入正規價值鏈的企業。

非洲廢棄物管理市場趨勢與洞察

城市人口成長是城市垃圾產生的主要促進因素。

非洲都市區每年新增約2,200萬居民,導致家庭消費和每日垃圾產量增加。光是拉各斯市每天就產生13,000至14,000噸廢棄物,但只有0.37%的垃圾被分流到正規回收部門,凸顯了基礎設施的嚴重不足。垃圾收集車隊的擴充速度跟不上需求,迫使市政當局將業務外包,並鼓勵私人投資建造垃圾轉運站和資源回收設施。集中式市政廢棄物降低了每噸垃圾的處理成本,提高了垃圾焚化發電和垃圾分類廠的計劃經濟效益。因此,人口趨勢將確保城市廢棄物在2030年後仍將是非洲廢棄物管理市場的支柱。

政府提高回收目標並推廣生產者責任延伸制度

肯亞2024年的生產者責任延伸制度(EPR)要求生產者承擔廢棄物收集和回收的費用,這與南非《國家環境管理廢棄物法》下的強制性方案類似。埃及正在製定一項永續回收舉措,將非正規廢棄物收集者與持證加工商聯繫起來,在提高材料品質的同時保障生計。合規成本正促使回收從自願項目轉變為法律義務,迫使品牌所有者與認證運營商簽訂長期服務合約。這些強制性規定正在穩步擴大塑膠、金屬和電子廢棄物回收設施的原料供應,從而提振整個非洲廢棄物管理市場的收入。

掩埋監管和執法力度不足

東非超過90%的廢棄物仍被傾倒在露天垃圾場,排放的甲烷氣體和滲濾液威脅地下水。光是亞的斯亞貝巴的萊皮垃圾場就接收未經檢驗的廢棄物,而該市的正規廢棄物收集率僅65%。監管不力使得未經授權的運輸者得以規避垃圾場收費,導致合規經營者無力承擔高昂的營運成本,並損害了設計完善的掩埋的經濟效益。缺乏統一的檢查機制使得市政當局無法收回營運成本,也無法落實「污染者付費」原則,阻礙了整個非洲廢棄物管理市場廢棄物基礎設施的現代化進程。

細分市場分析

2025年,受人口向都市區遷移導致家庭消費成長的推動,住宅廢棄物將佔非洲廢棄物管理市場的60.45%。同時,受購物中心和辦公大樓擴張的推動,商業垃圾量預計將以8.52%的複合年成長率成長,從而帶動了對定期收集和安全文件銷毀的需求。零售連鎖店簽訂多年契約,以履行其在生產者延伸責任制(EPR)下的收集義務,這為綜合服務提供者提供了可預測的垃圾量。工業廢棄物產生者,尤其是在南非,面臨日益嚴格的危險廢棄物法規,這使得他們更加依賴獲得許可的處置合作夥伴。由於醫療保健投資的增加,醫療廢棄物也在增加,這為獲得認證的焚燒爐創造了利潤豐厚的市場。

非洲廢棄物管理市場受惠於多樣化的原料來源。不斷成長的基礎設施預算推動了建築和拆除廢棄物的增加,而農業殘餘物則為城郊地區的沼氣化提供了機會。威立雅在多個非洲國家採用的多源服務模式,透過結合住宅和商業契約,實現了高回報特種廢棄物處理量與處理量之間的平衡,展現了其價值。非正式網路在塑膠收集方面仍然發揮著重要作用,但正規的集散商正開始透過特許經營模式吸收這些網路,從而提供標準化的安全培訓,並透過行動支付提高透明度。

非洲廢棄物管理報告按產生來源(住宅、商業、工業、醫療保健等)、服務類型(收集、運輸、分類/分類等)、廢棄物類型(生活廢棄物、工業危險廢棄物、電子廢棄物、塑膠等)和地區(奈及利亞、南非、埃及、肯亞、非洲其他地區)進行細分。市場預測以美元以金額為準為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 城市人口成長是城市垃圾產生量增加的主要原因。

- 各國政府正在提高回收目標並推廣生產者延伸責任制(EPR)框架。

- 投資者對廢棄物發電(WtE)計劃的興趣日益濃厚

- 數位化採集和路線最佳化平台

- 偏遠礦區塑膠燃料生產的離網微型熱解技術

- 市場限制

- 掩埋監管和執法力度薄弱。

- 缺乏用於大規模加工資產的資金

- 非正規部門的根深蒂固阻礙了正規私人投資。

- 廢棄物發電廠的氣候變遷保險缺口

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 物流基礎設施洞察

- Start-Ups創新特輯

第5章 市場規模及成長預測(價值,單位:十億美元)

- 按來源

- 住宅

- 商業設施(零售商店、辦公室等)

- 產業

- 醫療(健康和醫藥)

- 建築和廢棄物廢棄物

- 其他(引擎廢棄物、農業廢棄物等)

- 按服務類型

- 收集、運輸、分類和分離

- 處理/處置

- 掩埋處置

- 回收和資源回收

- 焚燒和廢棄物發電

- 其他(化學處理、堆肥等)

- 其他(諮詢、審核、訓練等)

- 依廢物類型

- 都市固態廢棄物

- 工業用危險廢棄物

- 電子廢棄物

- 塑膠廢棄物

- 醫療廢棄物

- 建築和拆除廢棄物

- 農業廢棄物

- 其他特殊廢棄物(放射性廢棄物等)

- 按地區

- 奈及利亞

- 南非

- 埃及

- 肯亞

- 其他非洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Averda

- EnviroServ

- Interwaste

- WasteMart

- Universal Recycling Company

- Desco

- PETCO

- The Glass Recycling Company

- Oricol Environmental Services

- WeCyclers

- The Waste Group

- SA Waste

- Veolia Africa

- SUEZ Recycling & Recovery Africa

- Biffa South Africa

- Mr Green Africa

- TakaTaka Solutions

- EcoPost

- Stericycle(MedWaste Africa)

- Dangote Recycling

第7章 市場機會與未來展望

The Africa Waste Management Market size in 2026 is estimated at USD 46.77 billion, growing from 2025 value of USD 44.11 billion with 2031 projections showing USD 62.73 billion, growing at 6.04% CAGR over 2026-2031.

Rapid urbanization funnels unprecedented waste volumes into already-strained municipal systems, creating space for private-sector collection, treatment, and recycling solutions. Investor appetite grows as governments adopt extended producer responsibility (EPR) rules, while technology firms deploy AI-enabled route optimization to raise collection efficiencies. Waste-to-energy (WtE) developers are securing climate-finance backing, yet capital gaps persist for other large-scale treatment assets. Competition remains fragmented, but rising compliance costs favor operators able to integrate informal collectors into formal value chains.

Africa Waste Management Market Trends and Insights

Rising Urban Population Driving Municipal Solid Waste Volumes

Africa's cities gain roughly 22 million new residents every year, elevating household consumption and daily waste flows. Lagos alone generates 13,000-14,000 tons of refuse each day, yet formal recycling diverts just 0.37%, underscoring severe infrastructure gaps. Collection fleets struggle to keep pace, prompting municipalities to outsource operations and invite private investment in transfer stations and material-recovery facilities. Concentrated urban waste streams lower per-ton processing costs, improving project economics for WtE and sorting plants. Demographic trends will therefore keep municipal solid waste (MSW) the anchor of the Africa waste management market well beyond 2030.

Government Push for Higher Recycling Targets & EPR Frameworks

Kenya's 2024 EPR regulations oblige producers to finance end-of-life collection and recycling, mirroring South Africa's mandatory schemes under the National Environmental Management Waste Act. Egypt has rolled out a sustainable recycling initiative that links informal pickers to licensed processors, raising material quality while preserving livelihoods. Compliance costs are shifting recycling from voluntary programs to legally enforced obligations, pushing brand owners to sign long-term service contracts with certified operators. These mandates steadily enlarge feedstock volumes for plastic, metal, and e-waste recycling facilities, bolstering revenues across the Africa waste management market.

Weak Landfill Regulation & Enforcement

More than 90% of East Africa's waste still winds up in open dumps, releasing methane and leachate that threaten groundwater. Addis Ababa's Repi site alone receives wastes unchecked, yet only 65% of the city's refuse is formally collected. Non-enforcement allows unlicensed haulers to undercut compliant operators by dodging gate fees, eroding the economics of engineered landfills. Without uniform inspection regimes, municipalities cannot recover operating costs or enforce polluter-pays principles, delaying modernization of disposal infrastructure across the Africa waste management market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Investor Interest in Waste-to-Energy Projects

- Digitized Collection & Route-Optimization Platforms

- Capital Scarcity for Large-Scale Treatment Assets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Residential streams secured 60.45% of the Africa waste management market share in 2025 as household consumption grew alongside urban migration. Commercial volumes, however, are projected to post an 8.52% CAGR, fueled by mall and office expansion that heightens demand for scheduled pickups and secure document destruction. Retail chains sign multi-year contracts to meet EPR take-back obligations, adding predictable tonnage for integrated service providers. Industrial generators confront tighter hazardous-waste regulations, particularly in South Africa, pushing them toward licensed disposal partners. Medical waste also rises with increased healthcare investment, creating a high-margin niche for certified incineration firms.

The Africa waste management market benefits from diverse feedstocks: construction and demolition debris escalates as infrastructure budgets climb, while agricultural residues present biogas opportunities in peri-urban zones. Veolia's multi-source service model across several African countries showcases the value of bundling residential and commercial contracts to balance volume with higher-yield specialty waste. Informal networks remain pivotal for plastics retrieval, yet formalized aggregators are beginning to absorb them via franchise schemes that deliver standardized safety training and mobile-payment transparency.

The Africa Waste Management Report is Segmented by Source (Residential, Commercial, Industrial, Medical, and More), by Service Type (Collection, Transportation, Sorting & Segregation, and More), by Waste Type (Municipal Solid, Industrial Hazardous, E-Waste, Plastic, and More), and by Geography (Nigeria, South Africa, Egypt, Kenya, Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Averda

- EnviroServ

- Interwaste

- WasteMart

- Universal Recycling Company

- Desco

- PETCO

- The Glass Recycling Company

- Oricol Environmental Services

- WeCyclers

- The Waste Group

- SA Waste

- Veolia Africa

- SUEZ Recycling & Recovery Africa

- Biffa South Africa

- Mr Green Africa

- TakaTaka Solutions

- EcoPost

- Stericycle (MedWaste Africa)

- Dangote Recycling

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising urban population driving municipal solid waste volumes

- 4.2.2 Government push for higher recycling targets & EPR frameworks

- 4.2.3 Growing investor interest in waste-to-energy (WtE) projects

- 4.2.4 Digitised collection & route-optimisation platforms

- 4.2.5 Off-grid micro-pyrolysis for plastics-to-fuel in remote mines

- 4.3 Market Restraints

- 4.3.1 Weak landfill regulation & enforcement

- 4.3.2 Capital scarcity for large-scale treatment assets

- 4.3.3 Informal sector lock-in that deters formal private investment

- 4.3.4 Climate-linked insurance gaps for WtE plants

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Force Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Logistics Infrastructure Insights

- 4.9 Startup & Innovation Spotlight

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Source

- 5.1.1 Residential

- 5.1.2 Commercial (retail, office, etc.)

- 5.1.3 Industrial

- 5.1.4 Medical (Health and Pharmaceutical)

- 5.1.5 Construction & Demolition

- 5.1.6 Others (institutional, agricultural, etc)

- 5.2 By Service Type

- 5.2.1 Collection, Transportation, Sorting & Segregation

- 5.2.2 Disposal / Treatment

- 5.2.2.1 Landfill

- 5.2.2.2 Recycling & Resource Recovery

- 5.2.2.3 Incineration & Waste-to-Energy

- 5.2.2.4 Others (Chemical Treatment, Composting, etc.)

- 5.2.3 Others (Consulting, Audit & Training, etc.)

- 5.3 By Waste Type

- 5.3.1 Municipal Solid Waste

- 5.3.2 Industrial Hazardous Waste

- 5.3.3 E-waste

- 5.3.4 Plastic Waste

- 5.3.5 Biomedical Waste

- 5.3.6 Construction & Demolition Waste

- 5.3.7 Agricultural Waste

- 5.3.8 Other Specialized Waste (radio active, etc)

- 5.4 By Geography

- 5.4.1 Nigeria

- 5.4.2 South Africa

- 5.4.3 Egypt

- 5.4.4 Kenya

- 5.4.5 Rest of Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Averda

- 6.4.2 EnviroServ

- 6.4.3 Interwaste

- 6.4.4 WasteMart

- 6.4.5 Universal Recycling Company

- 6.4.6 Desco

- 6.4.7 PETCO

- 6.4.8 The Glass Recycling Company

- 6.4.9 Oricol Environmental Services

- 6.4.10 WeCyclers

- 6.4.11 The Waste Group

- 6.4.12 SA Waste

- 6.4.13 Veolia Africa

- 6.4.14 SUEZ Recycling & Recovery Africa

- 6.4.15 Biffa South Africa

- 6.4.16 Mr Green Africa

- 6.4.17 TakaTaka Solutions

- 6.4.18 EcoPost

- 6.4.19 Stericycle (MedWaste Africa)

- 6.4.20 Dangote Recycling

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

廢棄物管理市場:依服務類型、廢棄物類型、處理技術和最終用戶分類-2026-2032年全球市場預測

廢棄物管理市場:依服務類型、廢棄物類型、處理技術和最終用戶分類-2026-2032年全球市場預測 智慧廢棄物管理市場預測至2034年-全球分析(按組件、廢棄物類型、解決方案類型、技術、最終用戶和地區分類)

智慧廢棄物管理市場預測至2034年-全球分析(按組件、廢棄物類型、解決方案類型、技術、最終用戶和地區分類) 全球 PFAS廢棄物管理市場:按處理技術、服務類型、最終用途產業和地區分類 - 預測(至 2031 年)

全球 PFAS廢棄物管理市場:按處理技術、服務類型、最終用途產業和地區分類 - 預測(至 2031 年) 2026年全球多氟烷基物質(PFAS)廢棄物管理市場報告2026年全球廢棄物管理與回收服務市場報告2026年全球紡織廢棄物管理市場報告2026年全球廢棄物管理軟體市場報告2026年全球放射性廢棄物管理系統市場報告2026年全球水務和廢棄物管理諮詢服務市場報告

2026年全球多氟烷基物質(PFAS)廢棄物管理市場報告2026年全球廢棄物管理與回收服務市場報告2026年全球紡織廢棄物管理市場報告2026年全球廢棄物管理軟體市場報告2026年全球放射性廢棄物管理系統市場報告2026年全球水務和廢棄物管理諮詢服務市場報告 全球廢棄物管理軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球廢棄物管理軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)