|

市場調查報告書

商品編碼

1937301

汽車用直流-直流轉換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Automotive Dc-Dc Converter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

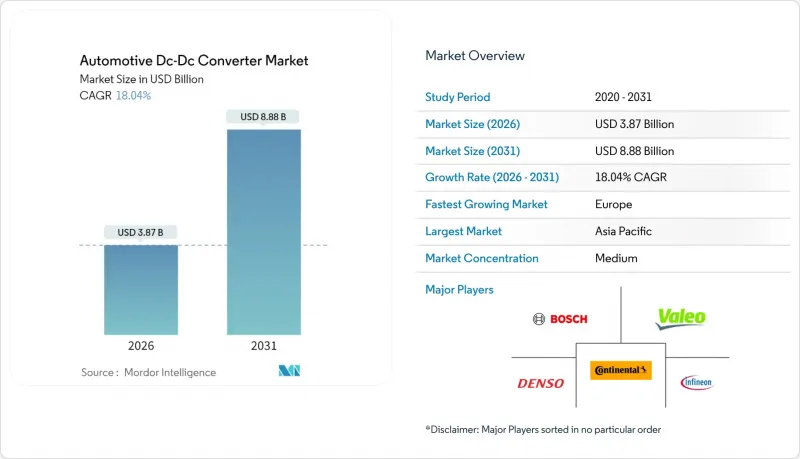

汽車直流-直流轉換器市場預計將從 2025 年的 32.8 億美元成長到 2026 年的 38.7 億美元,預計到 2031 年將達到 88.8 億美元,2026 年至 2031 年的複合年成長率為 18.04%。

快速的電氣化、向48V輕混架構的轉變以及驅動電池從400V向800V的升級,都為這一顯著成長提供了支撐。能夠管理高壓區和低壓區之間能量流動的雙向拓樸結構,構成了下一代電動平台的設計基礎。諸如碳化矽(SiC)和氮化鎵(GaN)等寬能能隙半導體不斷提升功率密度和效率,從而能夠製造更小更輕的轉換器模組,並簡化車輛封裝要求。從區域來看,亞太地區憑藉中國的生產規模佔據主導地位,而歐洲則由於嚴格的二氧化碳減排目標和碳中和政策,成長速度最快。競爭格局由全系統供應商和專業半導體製造商之間的合作所決定,這種合作不斷突破性能極限,並加快了先進電力電子產品的上市速度。

全球汽車直流-直流轉換器市場趨勢及展望

純電動車和插電式混合動力車產量快速成長

隨著全球電動車生產計畫的擴大,汽車製造商向800V動力傳動系統轉型,以縮短快速充電時間,因此對高效能轉換器的需求也不斷成長。特斯拉在其車隊中採用48V配電系統,正是這種轉變為簡化佈線和提高效率方向的體現。商用車製造商也在效仿,例如馬克卡車整合了多區域轉換器,在不犧牲可靠性的前提下,為動力系統、輔助設備和駕駛員舒適性供電。雙向拓撲結構實現了日常的車網互動(V2G),將停放的車輛轉化為能源資產。這進一步強化了對先進轉換器大規模生產的需求。擴大生產規模將進一步降低單一晶片的成本,從而促進先進技術的普及應用。比亞迪2024年的銷售預測表明,產量的增加直接提升了各個價位車型對轉換器的需求。

全球趨勢趨向強制性48V輕度混合動力

歐洲的二氧化碳排放最後期限和北美日益嚴格的CAFE標準正迫使汽車製造商採用48V系統,以在不投資全面電氣化的情況下逐步降低排放。歐洲汽車零件供應商協會(ACEA)預測,到2025年,48V架構將在新型輕度混合動力車中近乎普及。重型車輛領域也在效法。國際汽車製造商也正在推廣類似技術,以保持在受監管市場的出口競爭力。基於ISO 21780的統一標準有助於跨平台實施,大幅縮短開發時間,並支援近期內轉換器出貨量的增加。

功率密度的溫度控管限制

功率超過數千瓦的轉換器會在矽元件和磁芯中產生高溫,而傳統的鋁製散熱器無法承受這種高溫,尤其是在商用車底盤等空間有限的場所。 Belle Firth公司推出了一款液冷式4kW轉換器,旨在解決重型設備運作週期中結溫過高的問題。儘管SiC和GaN裝置效率很高,但在400kHz的開關頻率下仍會產生大量的熱量,因此需要使用精密的冷卻板或介質油通道進行散熱。

細分市場分析

商用平台的發展速度將超過乘用車,2026年至2031年的複合年成長率將達到19.50%。到2025年,商用平台將佔據汽車直流-直流轉換器市場63.55%的佔有率。車隊採購商正在透過降低燃油和維護成本來評估電動出行的回報,這加速了對堅固耐用型轉換器的需求,這些轉換器用於為輔助液壓泵、升降機和空調系統供電。在政府對零排放卡車的支援下,預計到2031年,商用車直流-直流轉換器市場規模將超過21.8億美元。乘用車在銷量方面仍將保持領先地位,預計到2025年,全球輕型汽車產量將超過8000萬輛,每輛汽車將配備兩到四個低功耗主導,用於資訊娛樂、照明和ADAS域控制器。

採用模式正在分化。乘用車製造商優先考慮48V輕混系統以滿足車隊平均排放目標,而卡車製造商則擴大直接採用高壓純電動車(BEV)和燃料電池電動車(FCEV),以應對都市區禁怠速區的要求。商用車的運作週期對冷卻板和灌封材料提出了更高的要求,這為導熱介面材料供應商帶來了售後市場機會。車網互動(V2G)帶來的收益吸引了物流營運商,他們整合固定電力容量用於夜間充電,進一步推動了雙向轉換器的出貨量。

到2025年,純電動車(BEV)將佔據汽車直流-直流轉換器市場73.12%的佔有率,因為所有純電動車都需要至少一個高壓轉換器來為車載負載供電。然而,與輕度混合動力車出貨量相關的汽車直流-直流轉換器市場規模預計到2031年將以21.95%的複合年成長率成長,因為對成本敏感的細分市場會採用48V系統以避免充電基礎設施的限制。雙向拓樸結構將12V鉛酸電池配件與48V鋰電池組連接起來,這需要嚴格的電壓調節精度來保護現有電子元件。插電式混合動力汽車在有購車補貼的市場中仍佔有一席之地,但其轉換器的銷售量和額定功率介於輕度混合動力車和純電動車之間。

燃料電池電動車目前仍屬於小眾市場,但每個燃料電池堆都會輸出高壓直流電,需要將其降至 12V,有時還需要升壓以負載平衡。這促使轉換器供應商開發出具有可互換磁性元件的模組化基板,以適應 350V、450V 和 800V 的母線電壓,而無需重新設計控制 ASIC,從而縮短了整個推進系統變體的設計時間。

到2025年,隔離式轉換器將佔據54.62%的市場佔有率,這主要得益於驅動電路和輔助電路之間電氣隔離的安全要求。同時,雙向轉換器將以22.05%的複合年成長率成長,隨著車載(V2L)和車網(V2G)功能從高階配置走向主流配置,其市佔率也將持續擴大。這些產品採用兩相交錯拓撲結構,以確保平穩的雙向功率流動,並需要數位控制迴路和即時診斷功能。非隔離式升降壓轉換器則是面向成本受限的輕混車型,這類車型的電池組電壓低於60V,且爬電距離易於控制。

採用碳化矽 (SiC) 可將開關頻率提升至 200 kHz 以上,同時減少變壓器匝數和磁鐵體積。 Wolfspeed 的 22 kW 參考產品展示了 SiC 模組如何實現更小的雙向封裝並提高峰值效率。先進的韌體使轉換器能夠充當資料節點,透過 CAN-FD 總線報告效率、溫度和故障代碼,從而為預測性維護服務奠定基礎。

區域分析

亞太地區將引領全球汽車直流-直流轉換器市場,到2025年將佔據46.92%的市場佔有率,這主要得益於中國汽車生產規模和日本的電力電子技術。預計中國電動車銷量將從2024年的690萬輛激增至2025年的1,100萬輛,將顯著增加乘用車和輕型商用車對轉換器的需求。 TDK等日本公司提供的緊湊型平面磁性元件高度降低30%,進一步鞏固了該地區的技術創新優勢。韓國汽車製造商(OEM)根據政府藍圖,計劃在2030年實現450萬輛零排放汽車的目標,這推動了韓國國內半導體生態系統對用於汽車量產的碳化矽(SiC)晶圓進行認證。儘管補貼逐步減少,但由於城市級零排放區的建設以及對歐洲的出口需求,預計國內需求仍將保持強勁。

預計到2031年,歐洲將以21.24%的複合年成長率實現最快成長,這主要得益於2030年將車輛二氧化碳排放標準收緊至57.5克/公里。德國供應商正與歐盟合作設計不含稀土元素的電機,並結合針對800V電壓最佳化的轉換器,專注於提升系統整體效率。歐盟替代燃料基礎設施法規要求使用雙向充電器以支援電網服務通訊協定,這進一步增加了轉換器規格的複雜性。法雷奧(Valeo)和羅姆(ROHM)等合作夥伴將熱模擬軟體和碳化矽(SiC)晶圓技術結合,加速產業化進程。基於聯合國歐洲經濟委員會(UNECE)R-100標準的標準化測試程序簡化了轉換器的跨境認證,使新參與企業更容易進入市場。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 純電動車和插電式混合動力車產量快速成長

- 全球趨勢:強制推行48V輕混動力系統

- 降低矽/鎵奈米帶元件的成本

- 向分區電氣和電子架構過渡

- 車輛到負載 (V2L) 電源功能

- 商用電動車對電動電能輸出裝置(ePTO)的需求

- 市場限制

- 功率密度溫度控管限制

- 汽車級被動元件供不應求

- 網路安全認證開銷

- 400kHz電磁干擾(EMI)相容性

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按車輛類型

- 搭乘用車

- 商用車輛

- 依推進類型

- 電池式電動車(BEV)

- 插電式混合動力汽車(PHEV)

- 燃料電池電動車(FCEV)

- 輕度混合動力(48V MHEV)

- 依產品類型

- 獨立轉換器

- 非隔離式轉換器

- 雙向轉換器

- 按輸入電壓範圍

- 低於40伏

- 40~70 V

- 70伏特或以上

- 按輸出功率和額定功率

- 小於3千瓦

- 3~6 kW

- 6千瓦或以上

- 透過使用

- 12V輔助負載

- 48V/12V雙向系統

- 高壓牽引支撐

- ADAS和資訊娛樂系統

- 溫度控管系統

- 最終用戶

- 原廠配套

- 售後改裝

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Bosch

- Denso

- Valeo

- Continental

- Infineon Technologies

- BorgWarner

- Toyota Industries

- TDK

- Panasonic

- Hella

- Aptiv

- Alps Alpine

- Marelli

- Hyundai Mobis

- Vicor

- Delta Electronics

- ZF Friedrichshafen

- onsemi

- Texas Instruments

- Littelfuse

第7章 市場機會與未來展望

The automotive DC-DC converter market is expected to grow from USD 3.28 billion in 2025 to USD 3.87 billion in 2026 and is forecast to reach USD 8.88 billion by 2031 at 18.04% CAGR over 2026-2031.

Rapid electrification, the shift to 48 V mild-hybrid architectures, and the move from 400 V to 800 V traction batteries underpin this substantial expansion. Bidirectional topologies that manage energy flow between high- and low-voltage domains now form the design baseline for next-generation electric platforms. Wide-bandgap semiconductors such as SiC and GaN continue to raise power density and efficiency, enabling smaller, lighter converter modules that simplify vehicle packaging requirements. Regionally, Asia-Pacific dominates due to Chinese production scale, while Europe grows fastest due to stringent CO2 targets and carbon-neutral mandates. Competitive dynamics are defined by collaboration between full-system suppliers and specialized semiconductor houses, pushing the performance envelope and accelerating time-to-market for advanced power electronics.

Global Automotive Dc-Dc Converter Market Trends and Insights

Surging BEV and PHEV Production

Global electric-vehicle build plans amplify demand for high-efficiency converters as automakers migrate to 800 V powertrains that shorten fast-charging times. Tesla's adoption of 48 V power distribution across its portfolio validates the shift toward slimmed-down wiring and better efficiency . Commercial players follow suit; Mack Trucks integrates multi-zone converters to supply traction, auxiliaries, and driver comforts without sacrificing reliability. Bidirectional topologies enable routine vehicle-to-grid export, turning parked fleets into energy assets and reinforcing volume pull for sophisticated converter designs. Higher production scale further drives down per-unit silicon cost, easing the pathway for advanced technology diffusion into mass-market segments. BYD's surge past Tesla in 2024 revenue underlines how production volume directly multiplies converter demand across vehicle price tiers.

Global 48 V Mild-Hybrid Mandates

CO2 compliance deadlines in Europe and tightening Corporate Average Fuel Economy targets in North America push OEMs to deploy 48 V systems that incrementally cut emissions without full electrification investment. The European Association of Automotive Suppliers projects the near-ubiquity of 48 V architectures in new mild-hybrid models by 2025. Heavy-duty segments follow: Eaton's 40-amp 48 V converters already power start-stop and e-PTO features in Class-8 trucks . Korean automakers are scaling similar technology to maintain export competitiveness in regulated markets. Harmonized standards under ISO 21780 ease cross-platform implementation, slashing development timelines and bolstering near-term converter shipments.

Thermal-Management Limits on Power Density

Converters exceeding a few kilowatts face silicon and magnetic core temperatures that can outpace traditional aluminum heat-sink solutions, especially in confined commercial-vehicle chassis. Bel Fuse introduced liquid-cooled 4 kW units to cope with junction-temperature constraints in heavy-equipment duty cycles. SiC and GaN devices, though efficient, still dissipate enough heat at 400 kHz switching to require advanced cooling plates or dielectric oil channels.

Other drivers and restraints analyzed in the detailed report include:

- Lower SiC/GaN Device Costs

- Vehicle-to-Load Functionality

- Automotive-Grade Passive-Component Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Commercial platforms recorded a 19.50% CAGR between 2026 and 2031, outpacing passenger models, holding 63.55% automotive DC-DC converter market share in 2025. Fleet buyers calculate payback on e-mobility through reduced fuel and maintenance bills, accelerating demand for rugged converters that power auxiliary hydraulic pumps, lifts, and climate control. The automotive DC-DC converter market size for commercial vehicles is projected to cross USD 2.18 billion by 2031, supported by state incentives for zero-emission trucks. Passenger cars retain volume leadership due to global light-vehicle output topping 80 million units in 2025, each embedding two to four low-power converters for infotainment, lighting, and ADAS domain controllers.

Adoption patterns differ: passenger car OEMs favor 48 V mild-hybrid systems to hit fleet-average emission targets, whereas truck makers leapfrog directly to high-voltage battery electrics or fuel cells to comply with urban no-idle zones. Commercial duty cycles also intensify stress on cooling plates and potting compounds, opening after-sales opportunities for thermal-interface material suppliers. Vehicle-to-grid revenue streams attract logistics operators that aggregate stationary power capacity during nightly depot charging, further lifting bidirectional converter shipments.

Battery electrics captured 73.12% of the automotive DC-DC converter market share in 2025 because every BEV needs at least one high-voltage converter for cabin loads. However, the automotive DC-DC converter market size tied to mild-hybrid shipments will post a 21.95% CAGR through 2031 as cost-sensitive segments adopt 48 V systems to skirt charging-infrastructure constraints. Bidirectional topologies bridge 12 V lead-acid accessories and 48 V lithium packs, demanding tight voltage-regulation accuracy to protect legacy electronics. Plug-in hybrids maintain relevance in markets with purchase incentives, but their converter count and rating sit between mild-hybrid and BEV extremes.

Fuel-cell electrics remain niche, yet each stack feeds high-voltage DC that must be down-converted to 12 V and sometimes boosted for battery load-leveling. Converter suppliers, therefore, develop modular boards that swap magnetics to suit 350 V, 450 V, or 800 V buses without re-spinning the control ASICs, compressing engineering timelines across propulsion variants.

Isolated converters held a 54.62% share in 2025, assured by safety requirements that galvanically separate traction and accessory circuits. Bidirectional units, however, will log a 22.05% CAGR, capturing incremental share as V2L and V2G features shift from premium to mainstream trims. These products integrate dual-phase interleaved topologies for smooth power flow in both directions, demanding digital control loops and real-time diagnostics. Non-isolated buck-boost stages target cost-constrained mild-hybrids where pack voltage stays below 60 V, easing creepage clearances.

Silicon carbide raises switching frequency above 200 kHz, trimming transformer turns and magnetic volume. Wolfspeed's 22 kW reference showcases how SiC modules shrink the bidirectional package, boosting peak efficiency. Firmware sophistication turns converters into data nodes that report efficiency, temperature, and fault codes over CAN-FD, laying the groundwork for predictive maintenance services.

The Automotive DC-DC Converter Market Report is Segmented by Vehicle Type (Passenger Vehicle, and More), Propulsion Type (BEV, and More), Product Type (Isolated Converter, and More), Input-Voltage Range (Below 40V, and More), Output-Power Rating (Below 3kW, and More), Application (12V Auxiliary Loads, and More), End-User (OEM Factory-Fit and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific leads the automotive DC-DC converter market with a 46.92% revenue share in 2025, driven by China's vehicle manufacturing scale and Japan's power-electronics expertise. China's electric-vehicle sales jumped from 6.9 million units in 2024 to an expected 11 million units by 2025, multiplying converter content across passenger and light-commercial segments. Japanese firms such as TDK present miniaturized planar magnetics that cut height by 30%, reinforcing the region's innovation edge. South Korean OEMs target 4.5 million zero-emission vehicles by 2030 under government roadmaps, spurring local semiconductor ecosystems to qualify SiC wafers for automotive volume. Though subsidies taper, domestic demand remains buoyed by city-level zero-emission zones and export pull to Europe.

Europe records the fastest 21.24% CAGR through 2031 on the back of fleet CO2 caps tightening to 57.5 g/km 2030. German suppliers co-design rare-earth-free e-motors with converters optimized for 800 V operation, emphasizing full-system efficiency. The EU Alternative Fuels Infrastructure Regulation requires bidirectional chargers to support grid-service protocols, elevating converter specification complexity. Partnerships like Valeo-ROHM bring together thermal-simulation software and SiC wafer leadership to accelerate industrialization schedules . Standardized test procedures under UNECE R-100 streamline cross-border homologation for converters, easing market access for new entrants.

- Bosch

- Denso

- Valeo

- Continental

- Infineon Technologies

- BorgWarner

- Toyota Industries

- TDK

- Panasonic

- Hella

- Aptiv

- Alps Alpine

- Marelli

- Hyundai Mobis

- Vicor

- Delta Electronics

- ZF Friedrichshafen

- onsemi

- Texas Instruments

- Littelfuse

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging BEV and PHEV Production

- 4.2.2 Global 48 V Mild-Hybrid Mandates

- 4.2.3 Lower Sic / Gan Device Costs

- 4.2.4 Shift To Zonal E/E Architectures.

- 4.2.5 Vehicle-To-Load (V2L) Functionality

- 4.2.6 On-Board E-Power (ePTO) Demand in Commercial EVs

- 4.3 Market Restraints

- 4.3.1 Thermal-Management Limits on Power Density

- 4.3.2 Automotive-Grade Passive-Component Shortages

- 4.3.3 Cyber-Security Homologation Overheads

- 4.3.4 Electromagnetic-Interference (EMI) Compliance At 400 Khz

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Vehicle Type

- 5.1.1 Passenger Vehicle

- 5.1.2 Commercial Vehicle

- 5.2 By Propulsion Type

- 5.2.1 Battery Electric Vehicle (BEV)

- 5.2.2 Plug-in Hybrid EV (PHEV)

- 5.2.3 Fuel-Cell EV (FCEV)

- 5.2.4 Mild-Hybrid (48 V MHEV)

- 5.3 By Product Type

- 5.3.1 Isolated Converter

- 5.3.2 Non-Isolated Converter

- 5.3.3 Bi-directional Converter

- 5.4 By Input-Voltage Range

- 5.4.1 Below 40 V

- 5.4.2 40 - 70 V

- 5.4.3 Above 70 V

- 5.5 By Output-Power Rating

- 5.5.1 Below 3 kW

- 5.5.2 3 - 6 kW

- 5.5.3 Above 6 kW

- 5.6 By Application

- 5.6.1 12 V Auxiliary Loads

- 5.6.2 48 V/12 V Bidirectional Systems

- 5.6.3 High-Voltage Traction Support

- 5.6.4 ADAS and Infotainment Power

- 5.6.5 Thermal-Management Systems

- 5.7 By End-User

- 5.7.1 OEM Factory-Fit

- 5.7.2 Aftermarket Retrofit

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Rest of North America

- 5.8.2 South America

- 5.8.2.1 Brazil

- 5.8.2.2 Argentina

- 5.8.2.3 Rest of South America

- 5.8.3 Europe

- 5.8.3.1 Germany

- 5.8.3.2 United Kingdom

- 5.8.3.3 France

- 5.8.3.4 Italy

- 5.8.3.5 Russia

- 5.8.3.6 Rest of Europe

- 5.8.4 Asia-Pacific

- 5.8.4.1 China

- 5.8.4.2 Japan

- 5.8.4.3 India

- 5.8.4.4 South Korea

- 5.8.4.5 Rest of Asia-Pacific

- 5.8.5 Middle-East and Africa

- 5.8.5.1 United Arab Emirates

- 5.8.5.2 Saudi Arabia

- 5.8.5.3 Turkey

- 5.8.5.4 Egypt

- 5.8.5.5 South Africa

- 5.8.5.6 Rest of Middle-East and Africa

- 5.8.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Bosch

- 6.4.2 Denso

- 6.4.3 Valeo

- 6.4.4 Continental

- 6.4.5 Infineon Technologies

- 6.4.6 BorgWarner

- 6.4.7 Toyota Industries

- 6.4.8 TDK

- 6.4.9 Panasonic

- 6.4.10 Hella

- 6.4.11 Aptiv

- 6.4.12 Alps Alpine

- 6.4.13 Marelli

- 6.4.14 Hyundai Mobis

- 6.4.15 Vicor

- 6.4.16 Delta Electronics

- 6.4.17 ZF Friedrichshafen

- 6.4.18 onsemi

- 6.4.19 Texas Instruments

- 6.4.20 Littelfuse

7 Market Opportunities & Future Outlook

汽車直流-直流轉換器市場:2026年至2032年全球市場預測(按拓撲結構、額定功率、輸入電壓、冷卻方式、車輛類型和最終用戶分類)AC-DC轉換器市場:2026-2032年全球市場預測(依輸出功率、輸入電壓、安裝類型、拓樸結構及最終用戶分類)

汽車直流-直流轉換器市場:2026年至2032年全球市場預測(按拓撲結構、額定功率、輸入電壓、冷卻方式、車輛類型和最終用戶分類)AC-DC轉換器市場:2026-2032年全球市場預測(依輸出功率、輸入電壓、安裝類型、拓樸結構及最終用戶分類) 全球汽車直流-直流轉換器市場報告(2026 年)直流高壓熱熔斷器市場(按額定電壓、額定電流、絕緣類型、安裝類型、安裝環境、應用和最終用戶分類)—2026-2032年全球預測

全球汽車直流-直流轉換器市場報告(2026 年)直流高壓熱熔斷器市場(按額定電壓、額定電流、絕緣類型、安裝類型、安裝環境、應用和最終用戶分類)—2026-2032年全球預測 汽車類比數位轉換器 (ADC) 市場規模、佔有率和成長分析(按產品類型、解析度、取樣率、介面、應用、最終用戶和地區分類)—2026-2033 年產業預測

汽車類比數位轉換器 (ADC) 市場規模、佔有率和成長分析(按產品類型、解析度、取樣率、介面、應用、最終用戶和地區分類)—2026-2033 年產業預測 電動車高壓 DC-DC 轉換器:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

電動車高壓 DC-DC 轉換器:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 汽車DC-DC轉換器市場:按DC-DC轉換器類型、按最終用戶、按系統、按車輛類型、按地區

汽車DC-DC轉換器市場:按DC-DC轉換器類型、按最終用戶、按系統、按車輛類型、按地區 汽車數位訊號控制器市場報告:2030 年趨勢、預測與競爭分析

汽車數位訊號控制器市場報告:2030 年趨勢、預測與競爭分析 汽車DC-DC轉換器市場{產品類型:隔離型、非隔離型;安裝類型:底盤安裝、SMD/SMT、DIN導軌安裝等; } - 全球產業分析、規模、佔有率、成長、趨勢和預測,2024-2034

汽車DC-DC轉換器市場{產品類型:隔離型、非隔離型;安裝類型:底盤安裝、SMD/SMT、DIN導軌安裝等; } - 全球產業分析、規模、佔有率、成長、趨勢和預測,2024-2034