|

市場調查報告書

商品編碼

1937290

金融科技領域人工智慧市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)AI In Fintech - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

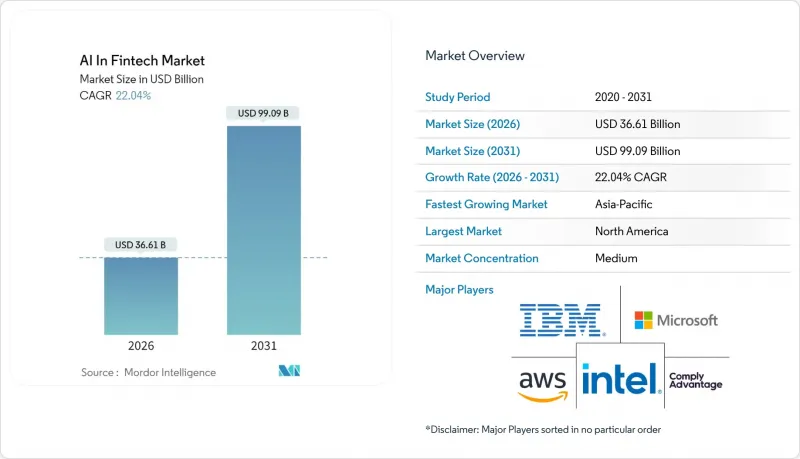

2025年,金融科技領域人工智慧的市場規模為300億美元,預計到2031年將達到990.9億美元,高於2026年的366.1億美元。

預測期(2026-2031 年)的複合年成長率預計為 22.04%。

成長的驅動力來自開放銀行政策(該政策釋放了分散的客戶資料)、日趨成熟的即時支付基礎設施以及雲端原生人工智慧平台(該平台降低了中型銀行的營運成本)。生成式人工智慧助理(Generative AI Copilot)將模型風險管理週期從數月縮短至數天,使金融機構能夠以前所未有的速度發布合規的風險模型。來自紐約梅隆銀行等金融機構的每月超過9兆美元的高頻支付數據正被輸入到人工智慧引擎中,從而增強詐欺檢測和流動性預測能力。這些因素的整合正在形成一個良性循環:更低的總體擁有成本推動了更廣泛的應用,而應用的廣泛又反過來創造了更豐富的資料集並提高了模型的準確性。

全球人工智慧市場趨勢及金融科技洞察

開放銀行監理加速人工智慧主導的流程自動化

諸如PSD3(第三版支付服務指示)之類的資料共用指示賦予人工智慧引擎對多家金融機構記錄進行一致且經授權的存取的能力,從而實現即時信用評分和高度個人化的優惠。隨著PSD3於2024年生效,歐洲各銀行正基於API優先架構重新設計產品開發流程,將先前孤立的資料集輸入機器學習模型。中型金融機構正透過將合規投資轉化為創新催化劑,並將監管成本轉化為收入成長,以提升自身競爭力。開放銀行採用率超過87%的金融機構市場,人工智慧服務的滲透率已顯著提高。

即時支付資料流的爆炸性成長

VisaNet+AI 對每筆核准交易的預測準確率高達 98%,而智慧結算預測則透過增加七天現金流預測來減少流動性緩衝。即時付款基礎能夠提供批次處理系統無法捕捉的行為訊號,使人工智慧能夠在詐騙活動發生後的幾毫秒內偵測到它們。研究表明,94% 的支付專業人士認為人工智慧對於預防詐欺至關重要,77% 的消費者希望他們的金融機構採用人工智慧。紐約梅隆銀行已實現了 90% 的支付指令處理自動化,使分析師能夠專注於增值任務。即時數據可用性還支援基於動態現金流指標的即時信貸決策。

特定領域人工智慧人才短缺

對具備機器學習技能和監管知識的專家的需求是供應量的2-4倍,74%的雇主表示招聘面臨挑戰。僅有25%的歐洲銀行擁有正式的生成式人工智慧培訓項目,加劇了人才缺口。相關職位的薪資比傳統金融職位高出40-60%,使得科技巨頭和頂級銀行更青睞這類人才。中型企業面臨人才短缺的風險,這將導致計劃工期延長、成本上升,並阻礙人工智慧技術的應用。

細分市場分析

預計到2025年,解決方案領域市場規模將達到214.4億美元,佔金融科技人工智慧市場71.45%的佔有率。企業傾向於選擇能夠將詐欺分析、客戶支援和管治整合到單一管理平台中的方案。 FICO基於區塊鏈的管治套件榮獲2025年創新獎,充分展現了整合解決方案為何正成為主流。目前規模較小的服務領域預計到2031年將以27.95%的複合年成長率成長,因為銀行正在尋求諮詢合作夥伴,以幫助他們建立複雜的生成式人工智慧流程並管理每天收到的234份監管通知。

顧問公司正在將合規義務轉化為模型設計,從而加快價值實現速度。這種需求使專業的系統整合商業務繁忙,服務費也逐漸成為可預測的收入來源。服務專業知識的普及吸引了先前因缺乏內部技能而推遲採用人工智慧的中型企業,從而擴大了金融科技領域的人工智慧基本客群。

到2025年,雲端環境將佔部署收入的81.35%,這主要得益於彈性運算能夠處理大量交易。摩根大通的架構將70%的應用程式部署在公共雲端上,而敏感工作負載則託管在一個價值20億美元的私有設施中。隨著監管機構收緊居住規則,以及銀行尋求降低單一供應商故障的風險,混合部署預計將以27.4%的複合年成長率成長。

混合模式兼具兩者的優勢:一方面,訓練流程保留在本地以確保資料主權;另一方面,推理處理則在雲端進行。這種柔軟性使混合模型成為一種永續的選擇,尤其適用於資料本地化執行嚴格的司法管轄區。

《金融科技領域的人工智慧》報告按類型(解決方案和服務)、部署模式(雲端和本地部署)、用例(詐欺和風險管理、聊天機器人和虛擬助理等)、組織規模(大型企業、中小企業、新型銀行)、最終用戶(零售銀行、保險等)和地區進行細分。

區域分析

預計到2025年,北美將佔據37.60%的收入佔有率,這得益於其成熟的金融基礎設施和清晰但分散的監管指導。摩根大通擁有2,000名人工智慧專家和超過400個應用案例,展現了其在本地的深厚技術實力。加拿大Neo Financial等新興銀行正將人工智慧擴展到服務不足的領域,而墨西哥則在利用人工智慧促進普惠金融。持續的公共和私人投資使北美成為創新試驗場,並將全球最佳實踐引入金融科技人工智慧市場。

預計到2031年,亞太地區將以33.1%的複合年成長率實現最快成長。中國將在2024年投資21億美元用於生成式人工智慧,企業採用率將達83%,遠超西方國家的滲透率。印度和日本正透過依賴人工智慧引擎的綜合貸款和量化交易平台迅速發展。該地區的金融科技收入預計將從2021年的2,450億美元成長到2030年的1.5兆美元,87%的銀行計劃與金融科技公司建立合作關係。新加坡是行動支付領域的主導,而澳洲和紐西蘭預計將獲得與其GDP不成比例的人工智慧價值佔有率。

合規負擔正在減緩歐洲人工智慧的普及速度。歐盟人工智慧立法引入了風險分級體系,雖然增加了管治成本,但確保了其合乎倫理的應用。英國的生成式人工智慧應用率已達70%,並正利用脫歐後的彈性為銀行客製化沙盒環境。德國和法國正在其主要企業內部建立人工智慧卓越中心,北歐國家則在試行綠色金融評估框架。東歐市場正嘗試將人工智慧應用於跨境工資匯款,從而重塑傳統的服務邊界。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 開放銀行政策將加速人工智慧主導的流程自動化。

- 即時支付資料流的激增

- 雲端原生人工智慧平台降低中型金融機構的總擁有成本

- 生成式人工智慧助理顯著縮短了模型風險管理週期時間

- 人工智慧驅動的ESG評分為綠色金融釋放獎勵

- 市場限制

- 特定領域人工智慧人才短缺

- 人工智慧模型管治方面的監管指導分散

- GPU供應鏈波動性加劇,推高推理成本。

- 價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 宏觀經濟因素如何影響市場

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 服務

- 透過部署模式

- 雲

- 本地部署

- 透過使用

- 詐欺和風險管理

- 聊天機器人和虛擬助手

- 信用評分和信用篩選

- 量化管理和資產管理

- 監理科技與合規分析

- 其他

- 按組織規模

- 主要企業

- 小型企業和新型銀行

- 最終用戶

- 零售銀行

- 保險

- 投資和資產管理

- 支付和匯款服務供應商

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 新加坡

- 澳洲

- 亞太其他地區

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Amazon Web Services, Inc.

- Microsoft Corporation

- International Business Machines Corporation

- Google LLC(Alphabet Inc.)

- Fair Isaac Corporation

- SAS Institute Inc.

- Intel Corporation

- NVIDIA Corporation

- Salesforce, Inc.

- Stripe, Inc.

- Plaid Inc.

- ComplyAdvantage Ltd.

- Onfido Ltd.

- Ripple Labs Inc.

- DataRobot, Inc.

- Upstart Holdings, Inc.

- ZestFinance, Inc.

- Darktrace Limited

- Truera, Inc.

- Active Intelligence Pte Ltd.

第7章 市場機會與未來展望

The AI in Fintech market was valued at USD 30 billion in 2025 and estimated to grow from USD 36.61 billion in 2026 to reach USD 99.09 billion by 2031, at a CAGR of 22.04% during the forecast period (2026-2031).

Growth is being propelled by open-banking mandates that liberate granular customer data, the maturation of real-time payment rails, and cloud-native AI platforms that trim operating costs for mid-tier banks. Generative AI copilots are compressing model-risk-management timelines from months to days, letting institutions release compliant risk models at unprecedented speed. High-frequency payment data, more than USD 9 trillion monthly at institutions such as BNY Mellon, feeds AI engines that sharpen fraud detection and liquidity forecasts. Convergence of these forces sustains a flywheel in which lower total cost of ownership invites wider adoption, and wider adoption produces richer datasets that reinforce model accuracy.

Global AI In Fintech Market Trends and Insights

Open Banking Mandates Accelerating AI-Led Process Automation

Mandatory data-sharing rules such as PSD3 grant AI engines consistent, permissioned access to multi-institution bank records, enabling real-time credit scoring and hyper-personalized offers. PSD3 went live in 2024, prompting European banks to redesign product origination workflows around API-first architectures that feed machine-learning models with previously siloed datasets. Mid-tier institutions gain competitive parity because compliance investments double as innovation enablers, turning regulatory cost into revenue growth levers. Markets where open-banking adoption exceeds 87% of institutions already display elevated AI service penetration.

Explosion of Real-Time Payments Data Streams

VisaNet +AI processes each authorization with 98% stability prediction accuracy, while its Smarter Settlement Forecast adds seven-day cash-flow projections that shrink liquidity buffers. Real-time rails broadcast behavioral signals that batch systems miss, letting AI flag fraud milliseconds after initiation . Surveys show 94% of payments professionals view AI as indispensable for fraud mitigation, and 77% of consumers expect institutions to deploy it. BNY Mellon automated 90% of back-office payment instruction handling, freeing analysts for value-added tasks. Instant data availability also powers live credit decisions based on dynamic cash-flow metrics.

Shortage of Domain-Specific AI Talent

Demand for professionals who blend machine-learning mastery with regulatory fluency exceeds supply by 2-4 times, with 74% of employers reporting hiring struggles. European banks note that only 25% have formal GenAI training pipelines, widening capability gaps. Salary premiums of 40-60% over traditional finance roles tilt the playing field toward tech giants and tier-one banks. Mid-tier firms risk stalled deployments as talent scarcity inflates project timelines and costs.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-Native AI Platforms Lowering TCO for Mid-Tier Financial Institutions

- GenAI Copilots Slashing Model-Risk-Management Cycle Times

- Fragmented Regulatory Guidance on AI Model Governance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions generated USD 21.44 billion in 2025, equal to 71.45% of the AI in Fintech market. Enterprises favor platforms that unify fraud analytics, customer support, and governance within a single control plane. FICO's blockchain-enabled governance suite, which won a 2025 innovation award, illustrates why integrated offerings dominate. The services segment is smaller today but is projected to grow at 27.95% CAGR through 2031 as banks seek advisory partners to configure complex GenAI pipelines and manage the daily swell of 234 regulatory notices.

Consultancies help translate compliance obligations into model design, accelerating time to value. This demand keeps specialized system integrators busy and cements service fees as a predictable revenue stream. As service expertise proliferates, mid-tier firms that once delayed AI adoption due to limited internal skill sets now jump in, broadening the AI in Fintech market customer base.

Cloud environments delivered 81.35% of deployment revenues in 2025 on the back of elastic compute that processes massive transaction volumes. JPMorgan Chase's architecture shows 70% of applications in public cloud while sensitive workloads reside in USD 2 billion private facilities. Hybrid deployments are forecast to advance at 27.4% CAGR as regulators tighten residency rules and banks look to limit exposure to single-vendor outages.

Hybrid models place training pipelines on-premise for sovereignty yet run inference in cloud, unlocking the best of both worlds. This flexibility positions hybrid as a durable choice, particularly in jurisdictions enforcing strict data localization.

The AI in Fintech Market Report is Segmented by Type (Solutions and Services), Deployment (Cloud and On-Premise), Application (Fraud and Risk Management, Chatbots and Virtual Assistants, and More), Organization Size (Large Enterprises and SMEs and Neo-Banks), End-User (Retail Banking, Insurance, and More), and Geography.

Geography Analysis

North America held 37.60% revenue share in 2025, supported by a mature financial stack and clear though fragmented regulatory guidance. JPMorgan Chase fields 2,000 AI specialists and over 400 live use cases, underscoring local skill depth. Canada's challenger banks such as Neo Financial scale AI to underserved segments, and Mexico leverages AI for financial inclusion. Continued public-private investment sustains North America as an innovation laboratory, feeding global best practices back into the AI in Fintech market.

Asia-Pacific is projected to register the fastest 33.1% CAGR through 2031. China poured USD 2.1 billion into generative AI in 2024 and records 83% enterprise usage, dwarfing western penetration rates. India and Japan extend momentum through inclusive credit and quantitative trading desks that rely on AI engines. The region's fintech revenue could move from USD 245 billion in 2021 to USD 1.5 trillion by 2030, with 87% of banks planning fintech partnerships. Singapore leads in mobile payments, while Australia and New Zealand expect disproportionate AI value capture relative to GDP.

Europe demonstrates strong adoption tempered by compliance overhead. The EU AI Act imposes a risk-tier system that elevates governance costs but assures ethical deployment. The UK reports 70% GenAI usage, leveraging post-Brexit agility to tailor banking sandboxes. Germany and France fund AI centers of excellence inside national champions, and the Nordics pilot green-finance scoring frameworks. Eastern markets experiment with AI for cross-border wage remittances, redrawing traditional service boundaries.

- Amazon Web Services, Inc.

- Microsoft Corporation

- International Business Machines Corporation

- Google LLC (Alphabet Inc.)

- Fair Isaac Corporation

- SAS Institute Inc.

- Intel Corporation

- NVIDIA Corporation

- Salesforce, Inc.

- Stripe, Inc.

- Plaid Inc.

- ComplyAdvantage Ltd.

- Onfido Ltd.

- Ripple Labs Inc.

- DataRobot, Inc.

- Upstart Holdings, Inc.

- ZestFinance, Inc.

- Darktrace Limited

- Truera, Inc.

- Active Intelligence Pte Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Open banking mandates accelerating AI-led process automation

- 4.2.2 Explosion of real-time payments data streams

- 4.2.3 Cloud-native AI platforms lowering TCO for mid-tier FIs

- 4.2.4 GenAI copilots slashing model-risk-management cycle-times

- 4.2.5 AI-powered ESG scoring unlocking green-finance incentives

- 4.3 Market Restraints

- 4.3.1 Shortage of domain-specific AI talent

- 4.3.2 Fragmented regulatory guidance on AI model governance

- 4.3.3 Rising GPU supply-chain volatility inflating inference costs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-premise

- 5.3 By Application

- 5.3.1 Fraud and Risk Management

- 5.3.2 Chatbots and Virtual Assistants

- 5.3.3 Credit Scoring and Underwriting

- 5.3.4 Quantitative and Asset Management

- 5.3.5 RegTech and Compliance Analytics

- 5.3.6 Others

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 SMEs and Neo-banks

- 5.5 By End-user

- 5.5.1 Retail Banking

- 5.5.2 Insurance

- 5.5.3 Investment and Wealth Management

- 5.5.4 Payments and Remittances Providers

- 5.5.5 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Malaysia

- 5.6.4.6 Singapore

- 5.6.4.7 Australia

- 5.6.4.8 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services, Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 International Business Machines Corporation

- 6.4.4 Google LLC (Alphabet Inc.)

- 6.4.5 Fair Isaac Corporation

- 6.4.6 SAS Institute Inc.

- 6.4.7 Intel Corporation

- 6.4.8 NVIDIA Corporation

- 6.4.9 Salesforce, Inc.

- 6.4.10 Stripe, Inc.

- 6.4.11 Plaid Inc.

- 6.4.12 ComplyAdvantage Ltd.

- 6.4.13 Onfido Ltd.

- 6.4.14 Ripple Labs Inc.

- 6.4.15 DataRobot, Inc.

- 6.4.16 Upstart Holdings, Inc.

- 6.4.17 ZestFinance, Inc.

- 6.4.18 Darktrace Limited

- 6.4.19 Truera, Inc.

- 6.4.20 Active Intelligence Pte Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

神經多樣性族群的金融素養和輔導平台市場預測(至2034年)-按解決方案類型、交付方式、經營模式、最終用戶和地區分類的全球分析

神經多樣性族群的金融素養和輔導平台市場預測(至2034年)-按解決方案類型、交付方式、經營模式、最終用戶和地區分類的全球分析 金融科技人工智慧市場規模、佔有率、趨勢和預測:按類型、部署模式、應用和地區分類,2026-2034年

金融科技人工智慧市場規模、佔有率、趨勢和預測:按類型、部署模式、應用和地區分類,2026-2034年 金融科技領域人工智慧(AI)市場規模、佔有率和成長分析:按組件、技術、部署模式、企業規模、應用、最終用戶和地區分類-2026-2033年產業預測

金融科技領域人工智慧(AI)市場規模、佔有率和成長分析:按組件、技術、部署模式、企業規模、應用、最終用戶和地區分類-2026-2033年產業預測 2026-2030年全球金融科技領域人工智慧市場

2026-2030年全球金融科技領域人工智慧市場 金融科技領域人工智慧市場-全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、應用、地區和競爭格局分類,2021-2031年

金融科技領域人工智慧市場-全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、應用、地區和競爭格局分類,2021-2031年 2026年全球利用人工智慧(AI)進行債務風險配置市場報告

2026年全球利用人工智慧(AI)進行債務風險配置市場報告 金融科技領域的人工智慧市場:按技術、組件、組織規模、部署類型、應用和最終用戶分類-2026-2032年全球市場預測2026年金融領域生成式人工智慧全球市場報告2026年金融科技領域人工智慧全球市場報告金融科技市場:依產品類型、經營模式、平台模式和最終用戶分類-2026-2032年全球預測

金融科技領域的人工智慧市場:按技術、組件、組織規模、部署類型、應用和最終用戶分類-2026-2032年全球市場預測2026年金融領域生成式人工智慧全球市場報告2026年金融科技領域人工智慧全球市場報告金融科技市場:依產品類型、經營模式、平台模式和最終用戶分類-2026-2032年全球預測